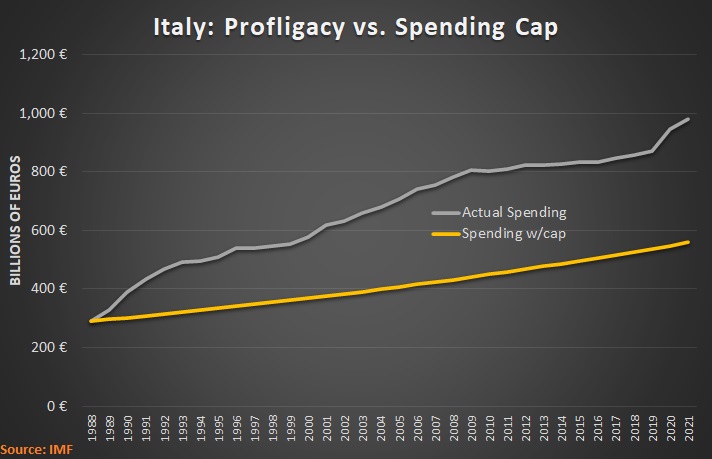

I wrote a two-part series (here and here) in 2022 predicting that Italy was at risk of suffering a fiscal crisis.

If and when it occurs, it will be because investors decide that Italy’s government might default (i.e., be unable to make payments on its debt). Interest rates would spike, financial markets would get shaky, banks would be a risk, and there would be a lot of pressure for a Greek-style bailout.

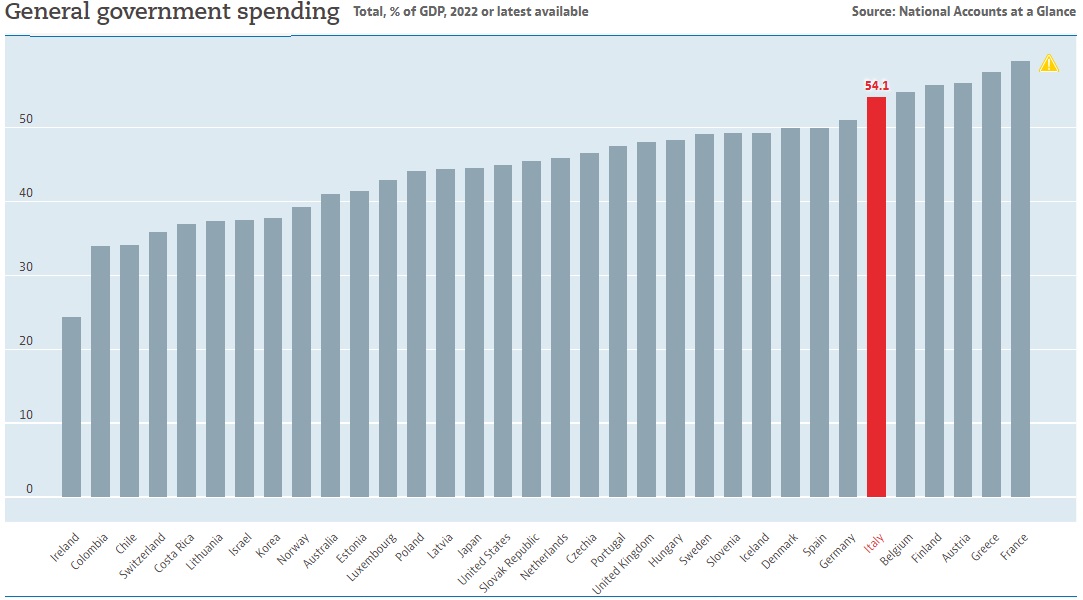

Should that happen, my role will be to point out that the real problem is that the burden of government spending in Italy is excessive (same message I delivered a dozen years ago).

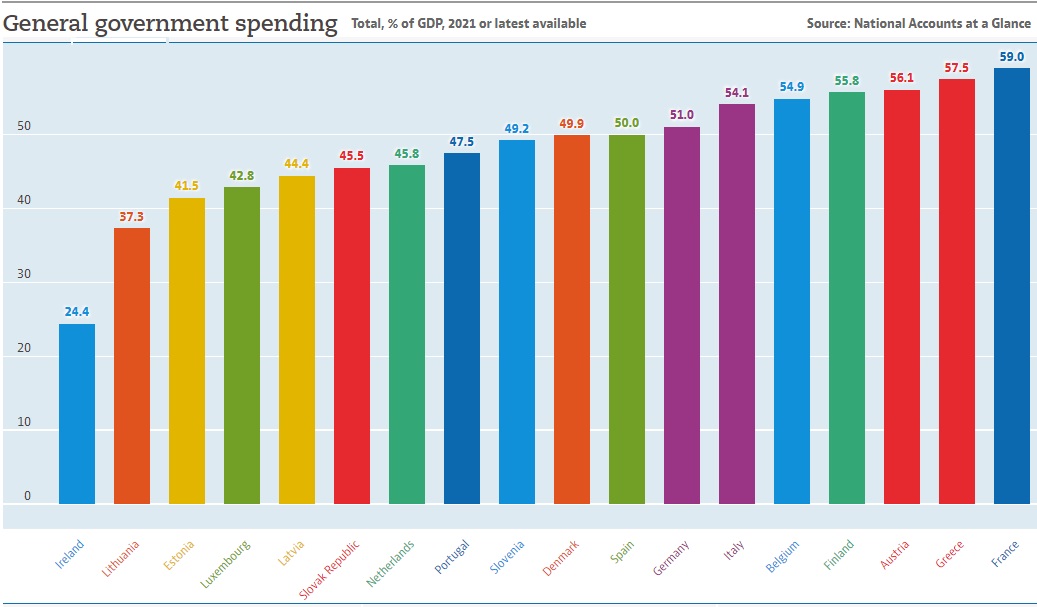

As shown by OECD data, it’s one of the most profligate nations in Europe.

And I suppose it’s worth mentioning that Italy’s demographic outlook is very grim, thus increasing medium- and long-run fiscal risks.

That’s the macro outlook.

Now let’s look at a specific example of why Italy is a fiscal mess. The Economist recently reported on a government giveaway that has become a nightmare.

…a home-improvements subsidy…has turned into the fiscal equivalent of King Kong: a monster running amok, wreaking havoc… Mr Giorgetti revealed that claims of the subsidy, known as the “superbonus”, made in the four years that the scheme has been running, together with claims of another that offsets the cost of renovating façades, would eventually drain the treasury of €219bn ($233bn). That is almost 10% of Italy’s GDP last year. …a left-populist coalition…introduced the superbonus in 2020… The idea was to stimulate the stricken economy… The government offered to pay homeowners 110% of the price of energy-saving renovations. …The cash was not to be reimbursed directly, but in the form of tax credits that could be sold on. …the superbonus has proved wildly popular. That should not have been a surprise: what is not to like about being repaid more than you have spent? Or not spent: since the tax credits are tradeable, many homeowners simply passed them on to their builders without having to part with a euro. A second reason is outright fraud. Last August Giorgia Meloni, Italy’s prime minister, said that contracts falsified to claim the subsidies constituted the biggest-ever rip-off of the Italian state. That was when they amounted to a mere €12bn; since then, the figure has risen to €16bn. A third problem is overpricing. Because the superbonus refund is greater than the outlay, actual or theoretical, it is in the interests of both the builder and the homeowner to inflate the cost of the work.

At the risk of understatement, this is one of the dumbest spending programs I’ve ever read about.

Okay, I’ll admit those bullet points are an oversimplification.

But there’s a reason for that.

Our book does show how we got into our current fiscal mess (because of too much spending).

And it shows why things will get worse in the future if we leave government on autopilot (because of too much spending).

Moreover, we have lots of evidence for the right way to avert a fiscal disaster. Richard Rahn wrote about our book in his Washington Times column.

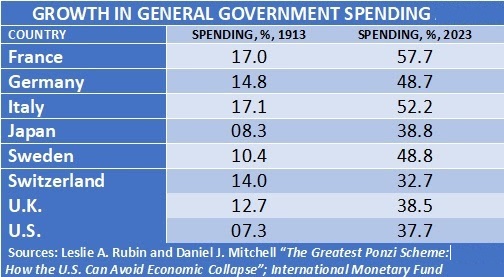

In a new book, “The Greatest Ponzi Scheme: How the U.S. Can Avoid Economic Collapse,” Leslie A. Rubin and Daniel J. Mitchell provide a well-written and informative history of how much of the world and particularly the United States managed to get into the current fiscal mess. …British Prime Minister Margaret Thatcher said it best: “The problem with socialism is that you eventually run out of other people’s money.” Before World War I, government spending in almost every country was a small share of gross domestic product. …In the United States, things began to change in the 1930s with the development of welfare programs… Mr. Rubin and Mr. Mitchell review many of the so-called entitlement programs that are the real budget busters. The payments from these programs consistently grow faster than the economy or tax revenue and now consume the bulk of the federal budget. Anyone who can do basic math can quickly understand the problem. When a country reaches the point where it is borrowing just to pay interest on the debt, game over.

That’s the bad news in the book. And Richard captures some of that bad news with this table showing how the burden of government spending has significantly increased over the past 100-plus years.

But our book also has good news, as Richard explains.

Fortunately, there are a number of success stories that serve as role models of what to do. …Switzerland is perhaps the best model for fiscal responsibility in a highly developed country, in that for the most part the Swiss keep government spending growing no more rapidly than the private sector.

As you might expect, I like his conclusion.

Mr. Rubin and Mr. Mitchell have done a great service in providing a highly understandable book, outlining the disaster about to engulf us if we do not change quickly, but equally important, a road map for getting out. Every policymaker and concerned citizen ought to buy this book and refer to it often — an economic bible of sin and salvation.

I want you to buy the book, but if you are a regular reader of this column, you already know the only practical way of averting a fiscal crisis in the United States. Simply follow the Golden Rule. And, because of its spending cap, Switzerland is a good role model.

As usual (2023, 2022, 2021, 2020, 2019, 2018, etc), let’s start the year by listing three things I’m hoping for and three things I worry may happen.

Let’s start with the potential good news. Here are the three things that plausibly could happen in 2024.

Libertarian policy in Argentina – Electing a genuine libertarian in a very statist country was miraculous. But that was the easy part. He can do some pro-market reforms using executive authority, but the biggest reforms will require assent from the legislature. Can he convince those politicians to implement his very good agenda? Will the special interest lobbies mount successful protests? I hope the answers to those two questions are yes and no.

Defeat of anti-school choice Republicans in Texas and Georgia – We have seen many states enact school choice the past few years, but Texas and Georgia did not join the club because some Republican politicians sided with teacher unions rather than students. That also happened a few years ago in Iowa, but Governor Kim Reynolds helped newcomers challenge – and defeat – many of those reprehensible hacks. And then school choice was approved in the Hawkeye State. I’m hoping Governor Abbott in Texas and Government Kemp in Georgia are able to do something similar, thus paving the way to expand the map of states with school choice.

Supreme Court overturns the Chevron Doctrine – Some people fret about the “deep state,” but practically speaking they should be concerned about the “administrative state.” The good news is that the Supreme Court may rule that bureaucrats don’t have leeway to impose more red tape in the absence of a clear legislative mandate.

One final note: Last year, I expressed hop that the Supreme Court would overturn the disgusting policy of civil asset forfeiture. That may still happen, though one year later than I hoped.

Now let’s contemplate potential bad outcomes. Here are the three things I fear will happen this year.

A Biden-Trump rematch – America’s biggest economic problem is entitlement spending and Biden and Trump both say they want to keep the status quo (Biden actually wants to make it worse). That’s a recipe for giant future tax increases on lower-income and middle-class households. So you can easily understand why I’m not excited by the prospect of two big-government politicians competing to see who can lead America into fiscal crisis.

A debt commission rather than a spending commission – Speaking of fiscal crisis, I’m increasingly worried that misguided and gullible Republicans will give their support to a debt commission, which will be a stalking horse for big tax increases. There’s nothing wrong with having a commission, but 100 percent-plus of America’s fiscal problem is excessive spending and any potential budget commission or budget deal should be entirely focused on restraining the growth of government.

Carbon protectionism in rich nations – Imposing higher taxes on imports from developing nations, based on energy use, is a very bad idea. Sadly, the European Union is moving forward with this scheme to undermine global trade, using global warming as an excuse. To make matters worse, there is growing interest in the United States. This is most unfortunate. I don’t think rich nations have an obligation to give foreign aid to poor nations (especially since that approach backfires), but I also think rich nation shouldn’t adopt big-government policies that hurt poor nations.

Landslide victory for TABOR in Colorado – If Milei’s victory was the best global election news of 2023, the defeat of Proposition HH was the best domestic election news of the year. Pro-spending lobbies have repeatedly tried to get rid of the TABOR spending cap.

Now for the three worst developments of 2023. And they are all related. Simply stated, I’m very worried about deterioration of global economic liberty and the failure to address festering problems.

Slouching toward fiscal crisis in the United States – Politicians in the United States generally care more about buying votes than in preserving or enhancing the economic well-being of citizens. Given demographic changes, that’s very bad news for the future.

But a fiscal crisis doesn’t happen simply because a country has too much government. It also matters how much of the spending burden is financed by borrowing. And much existing debt there already is.

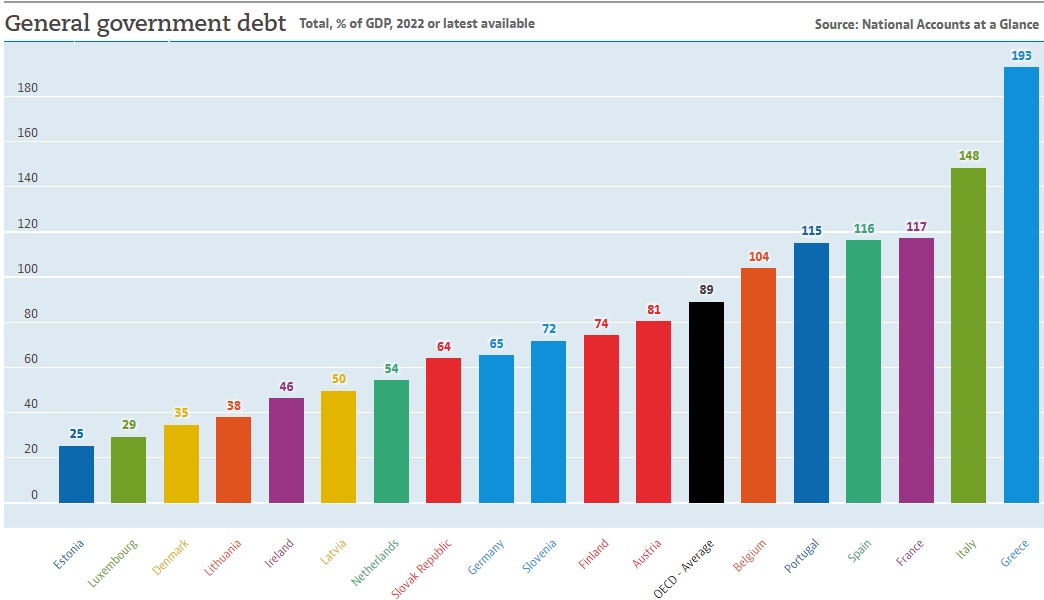

Speaking of which, here’s some OECD data on existing government debt in those nations.

Greece and Italy have the biggest debt burdens, but France, Spain, Portugal, and Belgium also have debt levels above 100 percent of GDP.

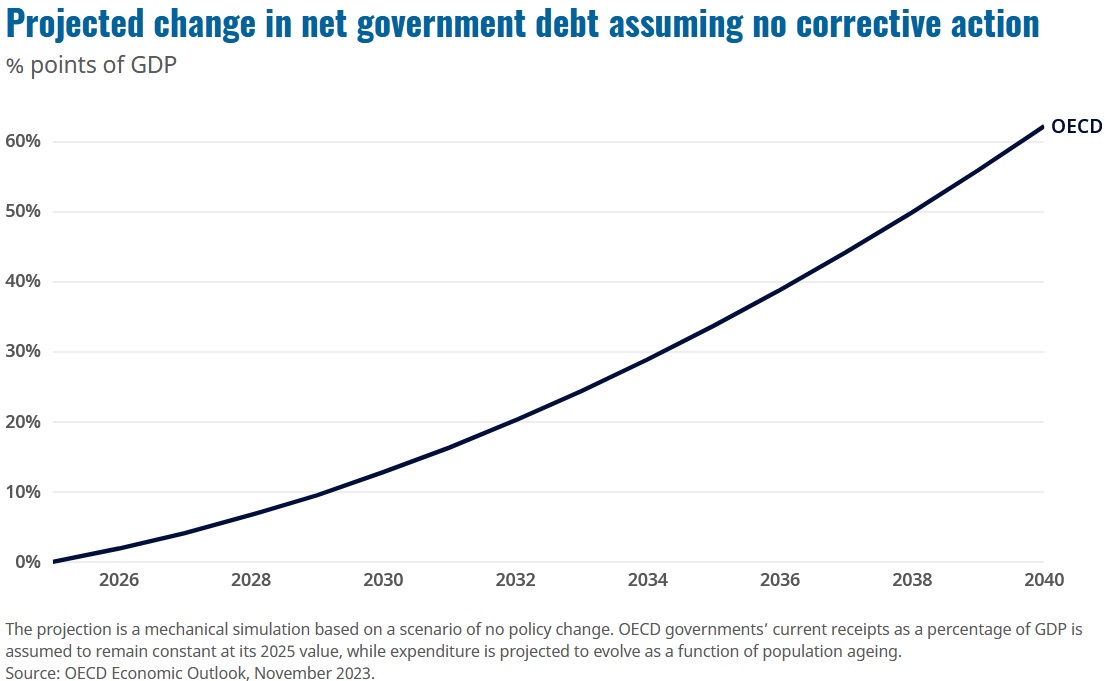

The OECD does not have country-specific projections of future debt, but here’s a chart from that bureaucracy’s recent Economic Outlook. It shows a 60 percent increase in debt for OECD governments over the next two decades.

I’m guessing a chart for eurozone nations would also show a big increase in debt levels (just like we saw a big jump last decade).

It is very likely that all the new spending and all the new debt will produce bad results.

Here are some excerpts from Desmond Lachman’s article in National Review.

Some 25 years after launching the euro, there has been continued divergence between the public finances and economic performances of the euro zone’s northern members and its southern periphery. While Germany and the other northern member countries have enjoyed prosperity and generally pursued responsible budget policies, income levels today in countries like Greece and Italy are practically unchanged from where they were some 15 years ago. Meanwhile, public-debt levels in the euro zone’s economic periphery have risen to record highs. …there is every reason to think that economic divergences will be exacerbated. That will raise new questions about the euro’s survivability once the European Central Bank (ECB) finally ends its bond-buying activities.

That bureaucracy enabled more spending and more debt, and that means an ever bigger bubble that will cause more damage when it bursts.

And Lachman writes that it’s a matter of when, not if.

Up until last year, high public-debt levels were not of much concern when interest rates were low and when the ECB was buying massive amounts of bonds to support the euro zone economy. However, those days are long gone. In the wake of the recent inflation spike, the ECB…is about to finally end its bond-buying program. That will substantially increase the cost of rolling over the large amount of public debt that will come due next year. All of this makes it all too likely that it is a question of when — and not if — we will have another round of the European sovereign-debt crisis.

For what it’s worth, I think he’s right about another debt crisis.

P.S. While the European Central Bank has contributed to the problem, the European Commission also has enabled more profligacy.

As originally envisaged…, the euro zone contained no provisions allowing for rescues financed from within the currency union. This was designed to stop the historically less fiscally responsible members from free-riding… But it did not work out… To avoid taking the currency union into territory where one or more of its members might default, the euro zone (after adopting various ad hoc financing mechanisms and participating in a number of bailouts) now has institutionalized an emergency-funding regime.

In an effort to ensure responsible budget policies, the euro zone adopted the so-called Maastricht criteria, which were meant to guide each country’s budget policy. Members were supposed to restrain their budget deficits to no more than 3 percent of GDP. They were also supposed to bring their public-debt levels down to 60 percent of GDP. It would be an understatement to say that the Maastricht criteria have been observed in the breach. …Greece, Italy, Portugal, and Spain…all had budget deficits in excess of 3 percent of GDP and public-debt-to-GDP ratios exceeding 100 percent.

The right solution is a Swiss-style spending cap, and even the German government seems to understand that’s the right approach. And if some nations don’t want to adopt this solution, they should be allowed to default.

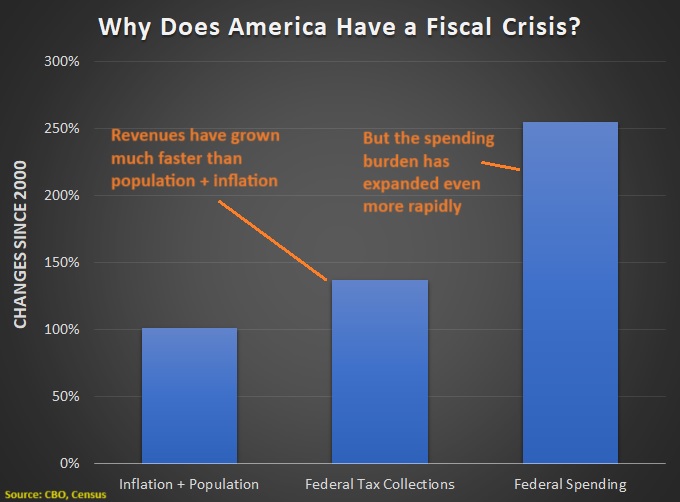

To understand the magnitude of the problem, let’s look at how fast taxes and spending have increased this century compared to population plus inflation.

There are two obvious takeaways from this data.

Washington receives more than enough tax revenue. Receipts have increases 137 percent since 2000, well beyond the 101 percent combined increase of inflation and population.

The crowd in Washington is grotesquely profligate. The federal spending burden has jumped 255 percent since 2000, more than 2-1/2 times faster than needed to keep pace with inflation plus population.

I’m sharing this data because reckless fiscal policy at some point will probably produce a crisis. James Capretta of the American Enterprise Institute recently wrote on this topic.

Here are some excerpts.

…the only reason a debt crisis has not already occurred is that market participants assume a tax and spending correction is coming at some point. …if and when the market consensus shifts toward assuming a fix is not coming after all, a debt crisis would emerge in short order. Demand for U.S. debt would fall, interest rates would rise (thus causing deficits to widen still further), and a crisis will have begun. …the U.S. has only about 20 years left before debt reaches a level that it could not be brought back under control without a wrenching break from today’s benign economic environment, such as an extended period of hyperinflation. …The U.S. is now operating with no margin for error… It would not take much at this point for the market to conclude that U.S. political dysfunction is a hardening reality and not a passing phenomenon. The follow-on conclusion that a rational and planned course correction will never be forthcoming could be the match that lights the fire.

The bottom line is that the profligacy of Bush, Obama, and Trump has led to anemic growth and rising dependency.

For what it’s worth, I think that’s already a crisis, albeit a slow-acting crisis akin to cancer.

Even though America’s long-run fiscal outlook is very grim, I wrote a two-part series earlier this year (here and here) to explain why the situation is not hopeless.

First and foremost, I noted that the only good solution is long-run spending restraint. Fortunately, that’s been done before. There have been three periods of good fiscal policy in recent decades.

In other words, we know the problem, we know how to solve it, and history shows that periods of fiscal restraint are possible.

I’m not the only one who is expressing optimism.

Two former Senators, Rob Portman (R-OH) and Kent Conrad (D-ND), have a column in yesterday’s Washington Post about the need to address America’s fiscal problems.

And they also don’t think the situation is hopeless. Here’s their core argument.

The deficit has doubled in the past year, and the national debt — some $33 trillion… — is diminishing our standing in the world. It is immoral to leave this level of debt to our children and grandchildren, and it is alreadyaffecting our economy. …But this is not a hopeless situation. …it is time to try an approach that removes some of our divisive politics from the picture: Congress must establish a bipartisan commission to put the country on a sustainable fiscal path. …Democrats will resist many of the necessary spending reductions, Republicans will resist needed revenue increases, and Democrats and Republicans alike will balk at the needed reforms to entitlement programs. But this approach has repeatedly helped move the country out of stalemate in the past. …our near- and long-term fiscal outlook is dangerously unsustainable. A fiscal commission should explain in objective terms the fiscal crisis we face and its consequences, scrutinize the entire federal budget, and make specific recommendations on revenue and spending, including what should be done to rescue our entitlement programs from insolvency. …A bipartisan commission might be our best chance to bestow upon future generations a stable financial future rather than an overwhelming financial burden and an America in decline.

I’m glad that these two former lawmakers are calling attention to our fiscal mess.

That being said, I have two big concerns with their argument.

They focus on red ink, which should be viewed as a symptom. The real problem is excessive spending. Real-world evidence shows that if you cure the underlying disease of excessive government, you automatically solve the symptom of deficits and debt.

Interestingly, the New York Times accidentally did some research that proves my case.

In an article back in 2011, Catherine Rampell looked at various bipartisan budget deal to measure the ratio of tax increases to (supposed) spending cuts.

What she found was that only one budget deal had zero tax increases, the one in 1997. Indeed, that budget deal actually cut taxes.

P.S. Senators Portman and Conrad seem to think that Simpson-Bowles budget plan is a good framework, but I explained in 2012 and 2013 why that plan would be an unmitigated disaster.

P.P.S. My opposition to higher taxes is practical rather than ideological. Back in 2012, I listed three big tax increases I would accept assuming politicians would be willing to make some long-overdue spending reforms. Suffice to say nobody on the left has been willing to accept that offer.

Mary Anastasia O’Grady warns in her Wall Street Journalcolumn that Argentina is on the verge of another economic meltdown.

Margaret Thatcher famously quipped that the trouble with socialism is that “you eventually run out of other people’s money.” …Argentina’s central bank is printing more pesos than the m arket wants to hold because the government, which is broke, needs them to pay its bills. This isn’t new in Argentina. Successive governments have generated repeated bouts of high inflation for decades. …Capital controls exacerbate shortages of hard currency. …Stagnating Argentine economic growth is no mystery. …On Aug. 13 Argentines vote in primaries for presidential candidates, and this issue is front and center. Yet promises of a cure are short on details, probably because it would mean upending the long tradition of Peronist populism that has bankrupted the country.

P.S. Writing for Law & Liberty, Marcos Falcone of Fundación Libertad explained that Argentina’s march in the wrong direction was aided and abetted by a constitution that evolved in the wrong direction.

…the 1853 Constitution…purposefully followed the model set by the American Founding Fathers so as to establish the kind of rule of law that a classically liberal society would need. …internal, bureaucratic barriers to free trade were to disappear; that no privileges would be extended by the government to anyone; and that private property was an inviolable right. …Ever since its inception, though, the Argentine Constitution has suffered from several changes…new articles incorporated into the Argentine Constitution have recognized social and collective ‘rights,’ the enforcement of which depends on increased government intervention. …Article 14 bis of the Constitution,…added in 1957…guarantees the existence of a minimum wage, mandates ‘fair’ salaries for workers, …and effectively bans the state from dismissing public employees. …The 1994 Convention…added the concept of ‘environmental rights’ in a way that implies proactive government intervention.

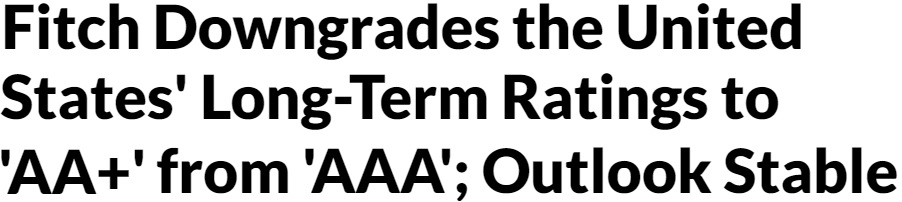

I’m not a big fan of Moody’s, Fitch, and Standard & Poor’s. As I explained in this 2011 interview, these credit rating firms don’t provide much insight, at least with regards to assessing whether governments can be trusted to honor their debts.

That being said, I don’t object to Fitch’s decision to reduce America’s rating from AAA to AA.

Here’s some of what the company wrote.

FitchRatings has downgraded the United States of America’s Long-Term Foreign-Currency Issuer Default Rating (IDR) to ‘AA+’ from ‘AAA’. …The rating downgrade of the United States reflects the expected fiscal deterioration over the next three years, a high and growing general government debt burden, and the erosion of governance relative to ‘AA’ and ‘AAA’ rated peers over the last two decades that has manifested in repeated debt limit standoffs and last-minute resolutions. …Additionally, there has been only limited progress in tackling medium-term challenges related to rising social security and Medicare costs due to an aging population.

While I agree with the downgrade, I have a couple of observations.

The US is in strong shape in the short run: There is zero chance that bondholders will lose money in the next 20 years. Even if Republicans and Democrats had a bigger-than-normal fight over the debt limit, leading to some bondholders not getting paid on time, lawmakers would fully compensate them in any eventual agreement.

The US is in terrible shape in the long run: American politicians are grotesquely irresponsible. They mostly understand that America faces an entitlement crisis, but most of them are unwilling to address the problem. Heck, some of them want to dig the hole deeper by expanding the welfare state.

America’s long-run fiscal problem is bipartisan: Starting with LBJ and Nixon, politicians from both parties have expanded the burden of government. The deterioration has continued this century with two Republican presidents and two Democratic presidents pushing for more spending.

By the way, there’s little reason for future optimism. Trump and Biden attack anyone who wants to do the right thing on entitlements, so that makes it more likely that politicians eventually will compound the damage of higher spending by enacting higher taxes.

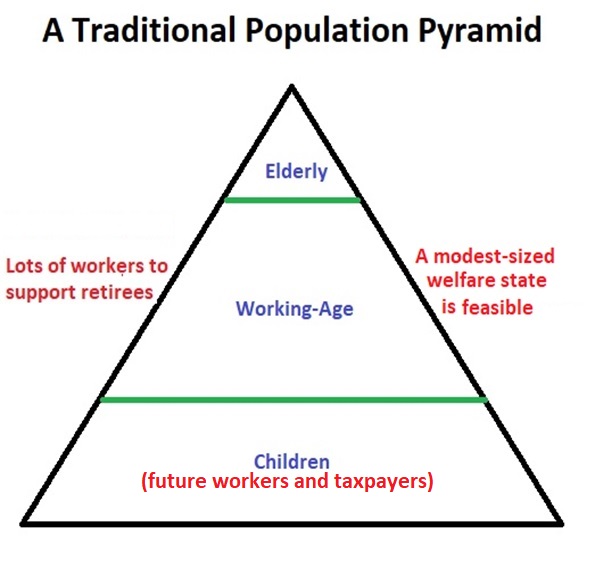

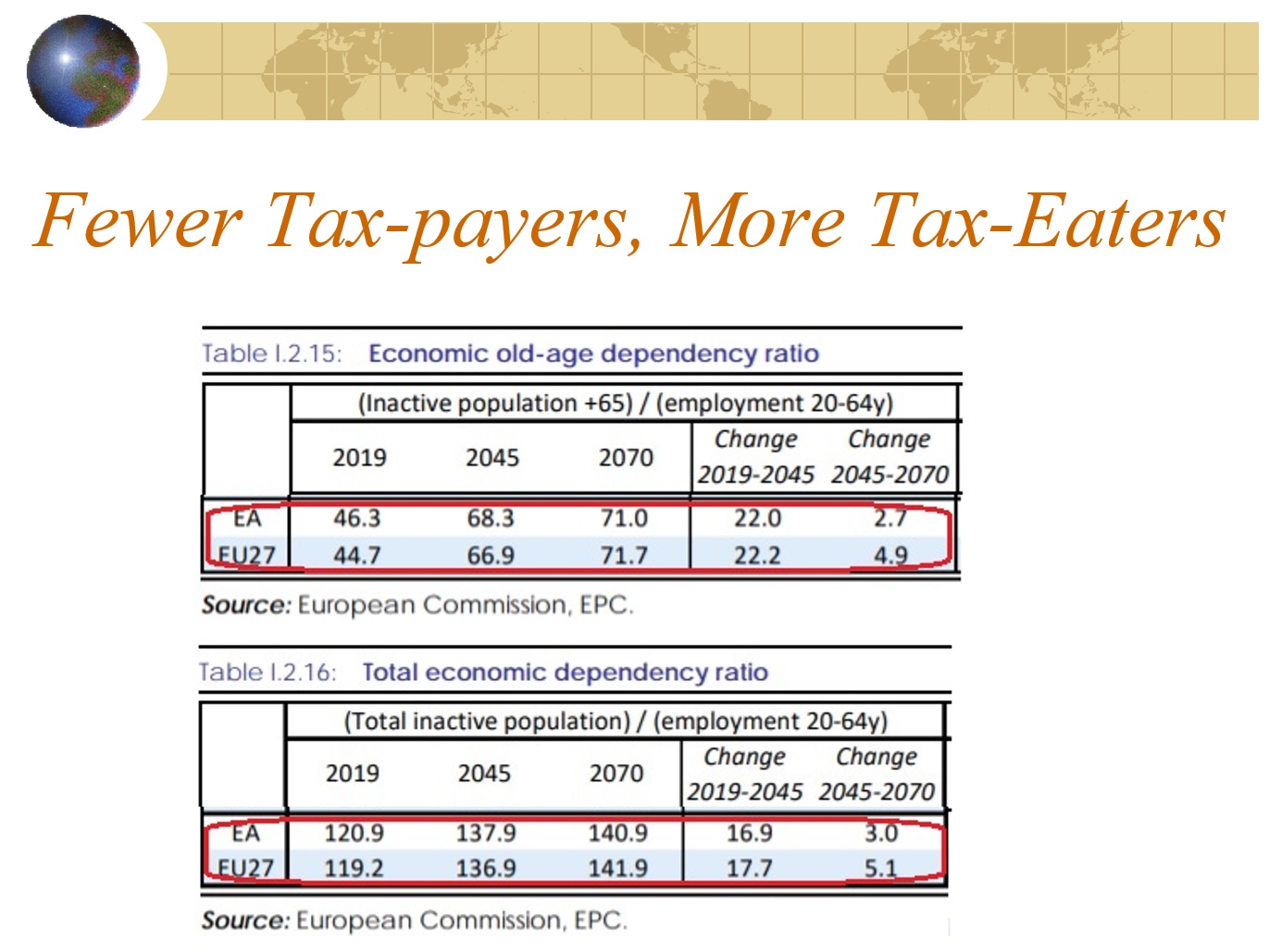

Our population pyramid is turning into a population cylinder, so there will not be enough working-age taxpayers in the future to finance all the benefits promised to the elderly. Not even close.

This inevitably and unavoidably means one or more of the following options.

Some readers may think I’m exaggerating in order to push a libertarian agenda. So let’s look at some analysis from non-libertarian sources.

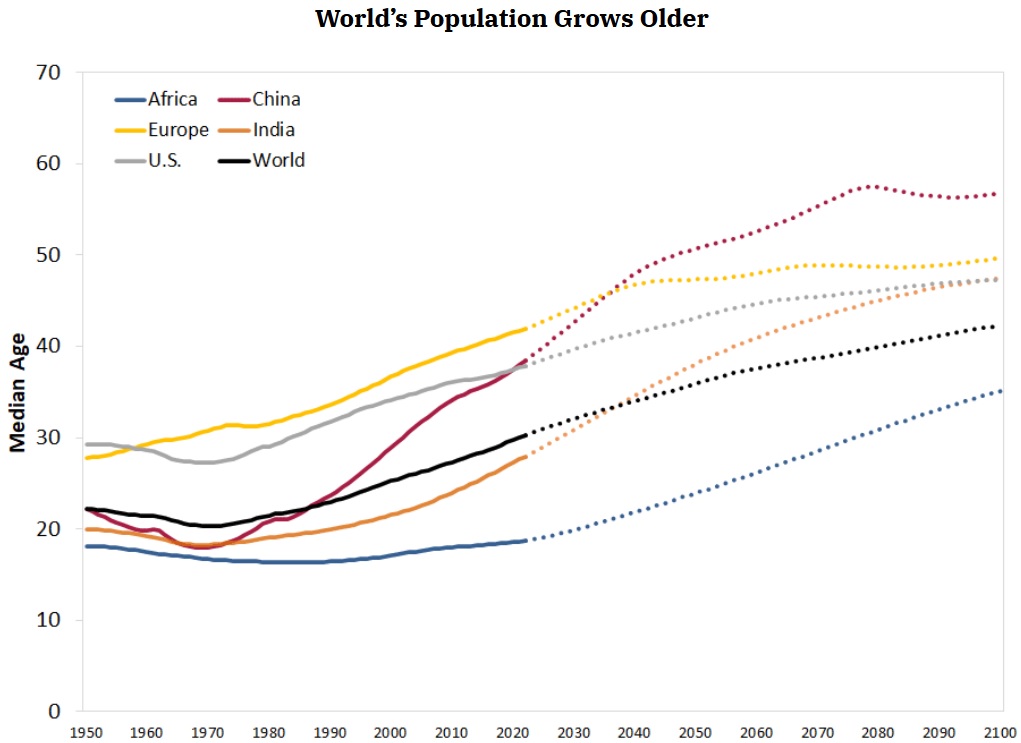

We’ll start with some excerpts from a recent report by the St Louse Federal Reserve Bank. Authored by Amy Smaldone and Mark L.J. Wright, it warns that the collapse in fertility is going to be a major problem for tax-and-transfer welfare states.

…the era of rapid population growth is coming to an end. …the world’s population will peak at around 10.5 billion people later this century before beginning to decline. …China’s population is expected to rapidly decline, ending the century around 800 million. Europe’s population has plateaued at approximately three-quarters of a billion people and will decline below 600 million by the end of the century, while the U.S. population is expected to level off at around 400 million. …The slowdown in population growth is due to a collapse in childbirth around the world. …the total fertility rate (TFR)—which represents the expected number of births over a woman’s life…for the world as a whole has fallen from about 5 in 1950 to around 2.3 today. Current TFRs are well below the “replacement rate” (or level needed to keep the population constant) of 2.1 in European countries (where they average 1.5), as well as in China (1.2), South Korea (0.9) and Japan (1.3)… Declining fertility and increased lifespans have resulted in a rapidly aging population. The figure below plots the median age of the population—the age at which half of the people are younger and half are older—around the world. As recently as 1973, half of the world’s inhabitants were under age 21. By the end of the 21st century, more than half will be middle-aged or elderly (40 or older). …the world as a whole will need to contend with a declining share of young workers. It is likely that pension and health care benefits will come under pressure with a shrinking tax base to pay for them.

I’ll add an editorial comment. It’s not “likely” that pension and health care benefits will come under pressure. That’s a given.

To understand why it’s a given, here’s a chart from the report.

As you can see, the average age is going to dramatically increase in all parts of the world.

The U.K.-based Economist also wrote about this topic in its latest issue. It also concludes that changing demographics could lead to fiscal crises.

Across much of the world the fertility rate, the average number of births per woman, is collapsing. Although the trend may be familiar, its extent and its consequences are not. …The largest 15 countries by GDP all have a fertility rate below the replacement rate. That includes America and much of the rich world, but also China and India… a shrinking population creates problems. …The obvious one is that it is getting harder to support the world’s pensioners. …whereas the rich world currently has around three people between 20 and 64 years old for everyone over 65, by 2050 it will have less than two. The implications are higher taxes, later retirements, …and, possibly, government budget crises.

Once again, I’ll add an editorial comment. It’s not that budget crises will “possibly” happen. They will happen.

However, I’ll conclude with a bit of optimism for the United States.

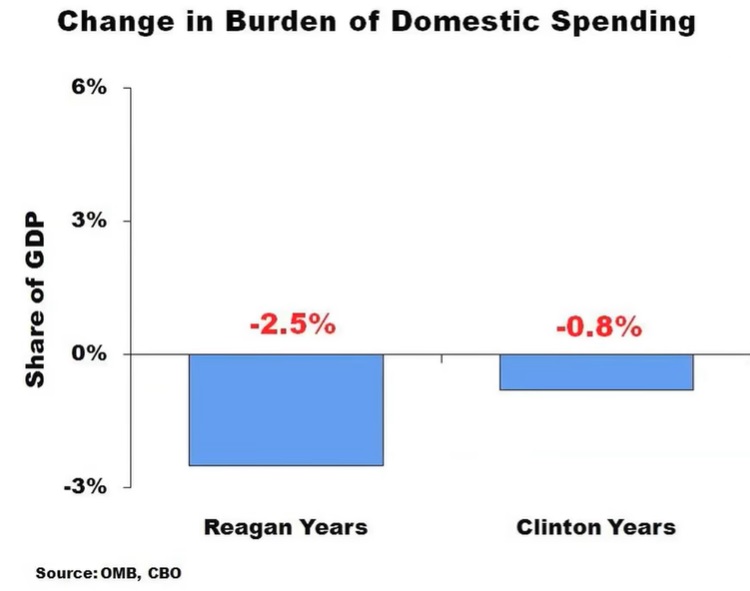

Unfortunately, that reformist energy was blunted by Obama and it then largely evaporated under Trump.

But something similar may happen again. Other nations (probably led by Italy) are going to suffer a fiscal crisis in the not-too-distant future. And when that happens, I hope it will be another learning experience for American lawmakers.

Maybe, just maybe, they’ll then decide to do what’s best for the country.

P.S. For more information about the demographic change and entitlement crisis, click here and here.

Because the burden of government spending, which already was excessive, increased even further.

And with taxes already very onerous in those countries, much of that new spending was financed with borrowing.

Investors then realized it was very risky to finance the various spending sprees. And when they stopped buying bonds from these governments (or started demanding higher interest rates to compensate for risk), that triggered the crises.

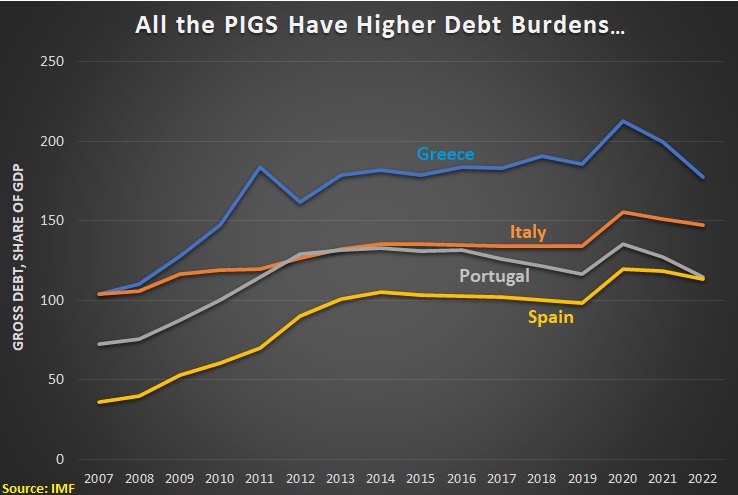

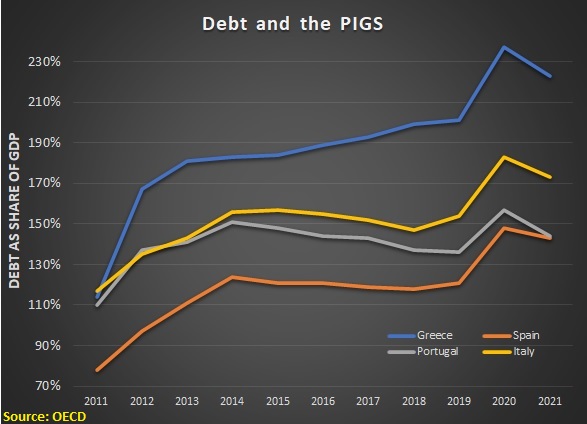

One would think that the nations most affected – Portugal, Italy, Greece, and Spain (the PIGS) – would have learned a lesson.

As you can see from this IMF data, those governments did not use the post-crisis recovery as an opportunity to get debt under control. Instead, every nation has more debt today than it did when the crisis occurred.

And why do these nations have higher debt levels?

For the simple (and predictable) reason that they have not reduced the burden of government spending.

To make a bad situation even worse, the European Central Bank cranked up the figurative printing press starting in 2020 by massively expanding its balance sheet.

Dumping all that money into the system quite predictably caused prices to soar. And now that the ECB is belatedly trying to undo its mistake.

That puts the PIGS under more pressure, as Desmond Lachman explained for National Review.

Christine Lagarde, the president of the European Central Bank (ECB)…has to raise interest rates at a time when governments in the euro zone’s economic periphery are more indebted today than they were at the time of the 2010 euro zone sovereign-debt crisis. This more hawkish interest-rate policy, coupled with a shift to quantitative tightening, now risks triggering another round of the euro zone debt crisis. …One of the ECB’s problems in having to raise interest rates aggressively to contain inflation is that such a course risks exacerbating the cracks that are now emerging in the European banking system. …if current trends continue, then another round of euro zone sovereign-debt crisis, where investors lose faith in the government’s ability to repay its debt, could be just around the corner. …This is especially true for Italy, where until recently the ECB had been buying Italian government bonds equivalent to that government’s net borrowing needs.

By the way, Lachman seems to think the Fed should allow continued inflation in order to help bail out Italy and the other PIGS.

That would be a big mistake. The long-run damage of that approach would be much greater than the long-run damage (actually, long-run benefits) of letting Italy and the others go bankrupt.

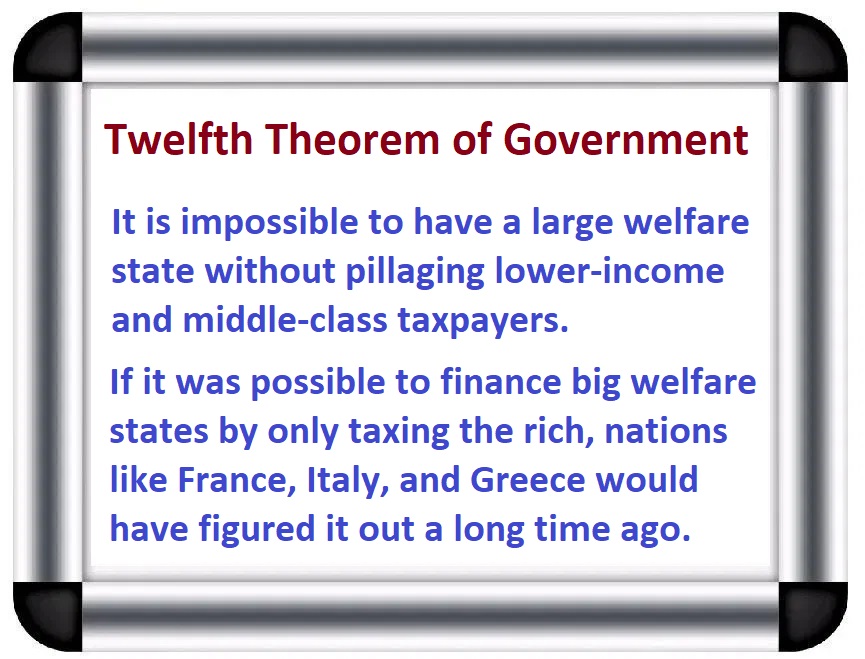

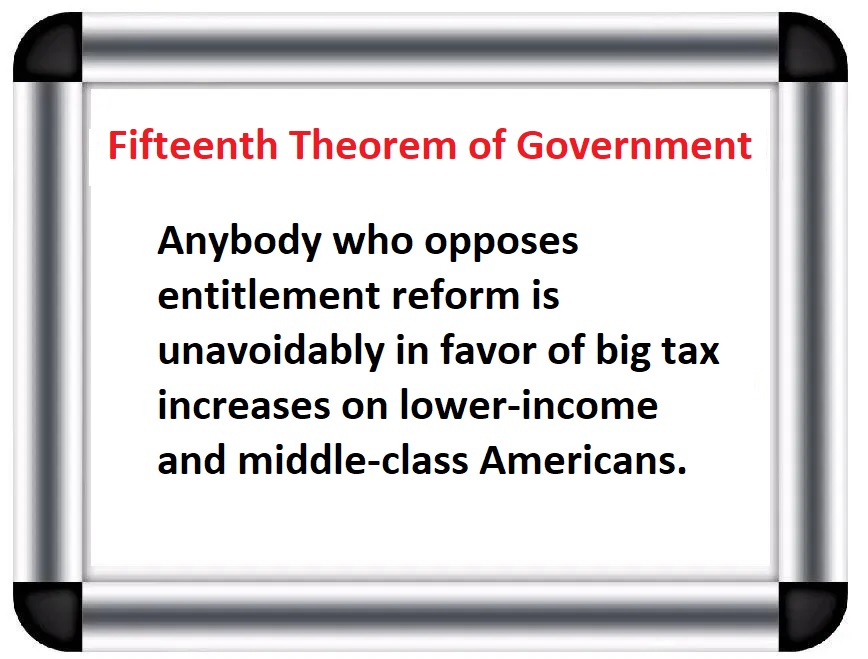

However, that means they want big tax increases on lower-income and middle-class household.

To emphasize this point, I unveiled my Fifteenth Theorem of Government, which drives home the point that you can’t have big government without pillaging ordinary people.

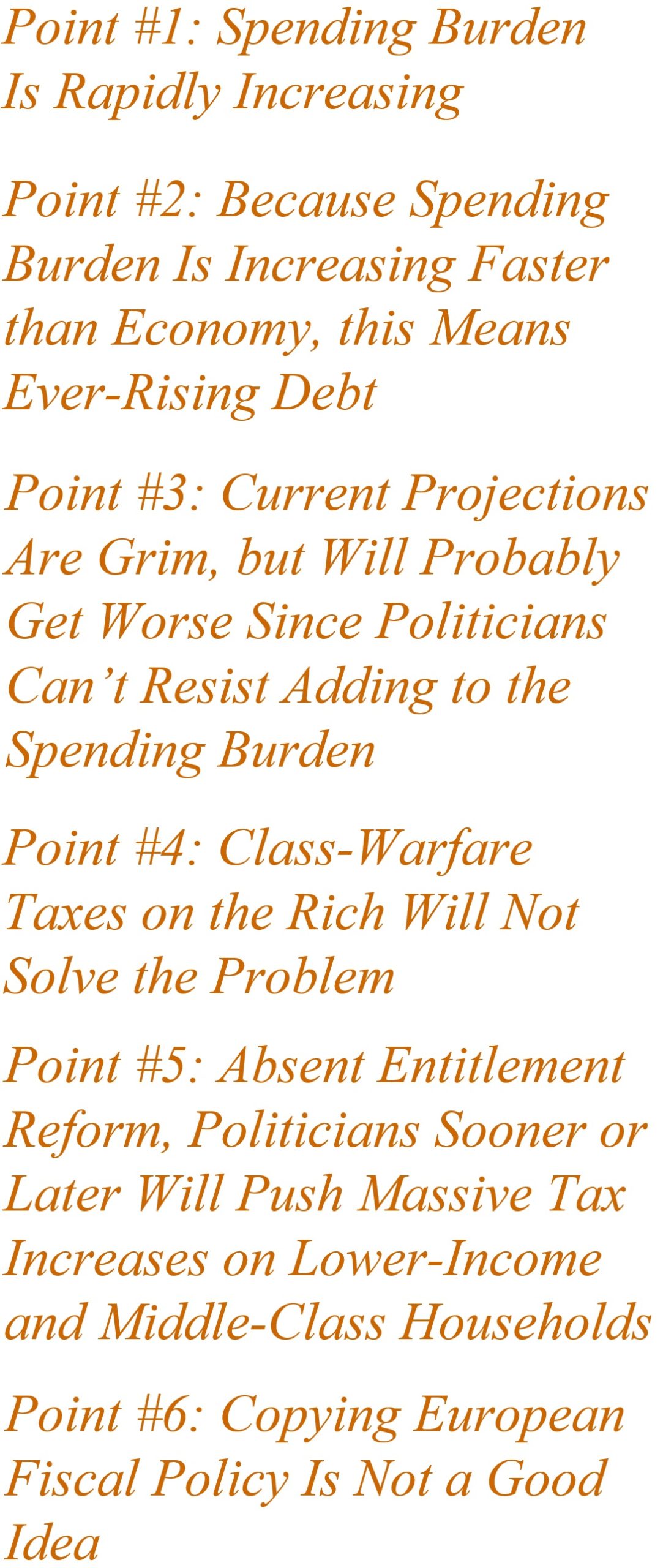

I pontificated on this issue today in a MoneyShow presentation.

There were lots of charts to justify my two theorems, but these six points hopefully are a good summary of my argument.

For what it’s worth, the first five points are basic math.

My final point is where the honest leftists and I have a big disagreement. They think it would be a good thing to copy Europe. But I think that would be crazy since European living standards are much lower because of bloated welfare states.

But even this modest reform is an outrage to some French leftists. In a column for the Washington Post, Rokhaya Diallo denounces the proposed change as an assault on “the French welfare model.”

Like tens of thousands of others, I was proud to be on the Place de la République recently to defend the legacy of the French welfare state. …Across the country, millions have gathered in periodic protests to defend one of the crown jewels of the French welfare model: the pension system. President Emmanuel Macron is determined to reform the pension system and to increase the retirement age from 62 to 64 (he first intended to push it to 65). …According to Macron, the calculus is simple: The French system cannot sustain itself financially, and because life expectancy is increasing, people have to work longer. …Big companies, however, have far more resources at their disposal than individual citizens, and raising corporate taxes would be a fairer way of increasing government revenue. …The fact that we live longer does not mean that we should spend our lives working for companies. Why should we subordinate our lives to the needs of capitalism?

At the risk of being snarky, Ms. Diallo is complaining about the reality of math rather than “the needs of capitalism.”

Though, by proposing higher taxes on French companies, she sort of acknowledges that the status quo is untenable.

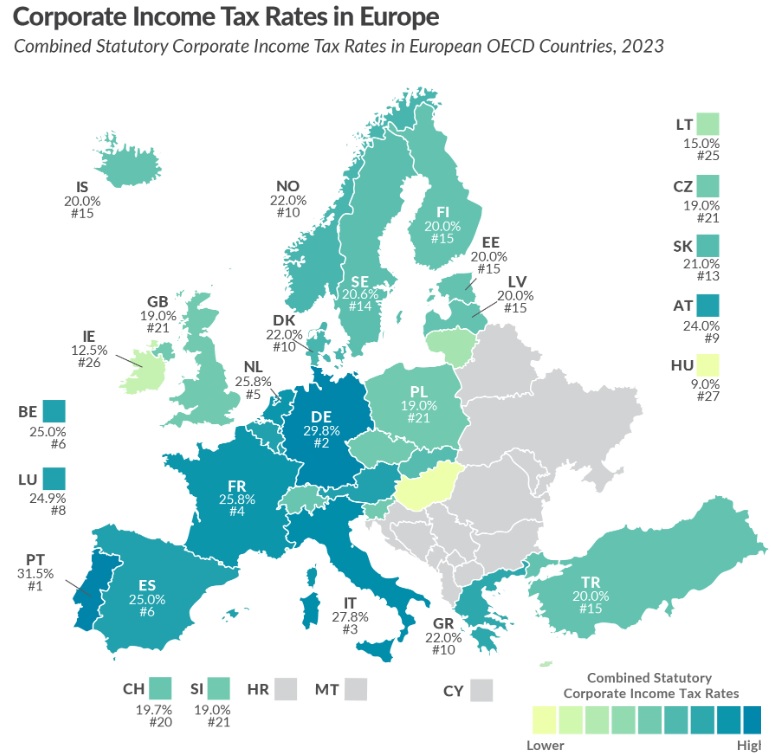

So is Ms. Diallo’s proposed policy of higher taxes on workers, consumers, and shareholders a feasible solution to France’s ever-growing fiscal burden? Could all the built-in new spending (12 percentage points of GDP) be financed by a higher corporate tax rate?

No. Not even close. The French corporate tax rate currently is 25.8 percent and it collects about 2.3 percent of GDP according to OECD data.

Given her economic naivete, Ms. Diallo might support a very radical approach, such as doubling the corporate rate to more than 50 percent. And she might think that change would boost receipts from 2.3 percent of GDP to 4.6 percent of GDP.

But she would be wrong. Wildly wrong. As shown by this map from the Tax Foundation, France already has the fourth-highest corporate tax rate in Europe. Any increase (especially a big increase) will simply cause more business activity to leave France and go to nations with less-onerous tax policy.

In other words, a higher rate would not lead to a big increase in revenue. Indeed, it might do so much damage to the business climate that the government would collect less revenue.

And don’t forget that an additional 2.3 percent of GDP in revenue (assuming it magically materialized) is still far less than the built-in spending increase of 12 percent of GDP. So her math is wrong in two ways.

The bottom line is that France has two choices.

Stick with the status quo and eventually suffer a horrific fiscal crisis.

Enact reforms to prevent an ever-growing spending burden.

Macron’s reforms are grossly inadequate, but at least he wants to take a small step in the right direction. Ms. Diallo wants to put her head in the sand.

P.S. In her column, Ms Diallo notes that lower-income workers don’t live as long.

…mortality numbers vary among social classes. Nurses live seven years less than other women: 20 percent of them and 30 percent of nursing assistants retire with disabilities. Blue-collar workers live six years less than executives, so that one-quarter of the poorest men die by age 62, while 94 percent of the rich are still alive at 64. Only 40 percent of the poorest survive to 80, whereas 75 percent of the wealthiest do.

For all intents and purposes, both the current president and his predecessor want to kick the can down the road, which surely is a recipe for massive future tax increases and may cause drastic changes to promised benefits.

Given their advanced ages, they probably won’t be around next decade when the you-know-what hits the fan.

But the rest of us will have to deal with a terrible situation thanks to their selfish approach.

Other nations are more fortunate, with leaders who put the national interest above personal political ambition.

Johan Norberg has a new column in the Wall Street Journal about how Swedish lawmakers adopted personal retirement accounts and undertook other reforms to strengthen their pension system.

President Biden refuses to consider any reforms, and so do many Republicans. But that won’t save the program; it’ll doom it. …Sweden faced the same problem in the early 1990s. The old pay-as-you-go pension system had promised too much. With fewer births and longer lives, projections showed the system would be insolvent a decade later. …Its politicians chose not to deceive the voters. …In 1994 the Social Democrats agreed with the four center-right parties to create an entirely new system based on the principle that pensions should correspond to what the beneficiary pays into the system—a system in which the contribution, not the benefits, is defined. …Sweden introduced partial privatization of the kind the American left derides as a Republican plot… The Swedish government withholds roughly 2.3% of wages and puts it into individual pension accounts. Workers are allowed to choose up to five different funds in which to invest this money…the average Swede has made an impressive average return of roughly 10% a year since its inception in 1995, despite the dot-com crash, the financial crisis and the pandemic. …Sweden’s pension system was recently described as the world’s best by the insurance group Allianz, based on a combination of sustainability and adequacy.

Back in 2018, I wrote about Sweden’s pension reforms, and I cited a study I co-authored back in 2000 for the Heritage Foundation.

Readers who want to learn more about the details of the Swedish system should read those publications.

For purposes of today’s column, though, let’s zoom out and see how Sweden’s system compares to other nations.

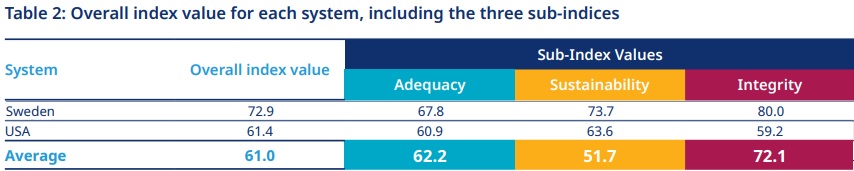

We’ll start by looking at a report by Mercer and the Chartered Financial Analyst Institute, which compared retirement systems in 43 developed countries. You can click here to view the full report and full rankings, but let’s focus on the United States and Sweden.

As you can see, Sweden beats America in every category, including a giant lead for integrity.

It’s also worth noting that Sweden is above average in every category while the United States is below average in two of the three categories.

Based on the Mercer/CFA report, we know Sweden’s system is good for workers.

But what about taxpayers?

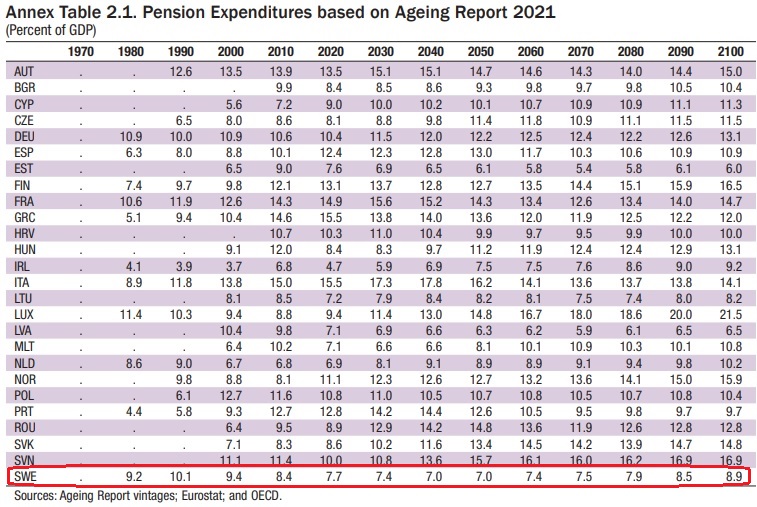

Here’s a table showing the fiscal burden of old-age programs in European nations, taken from a report by the International Monetary Fund.

As you can see for both the present and the future, Swedish taxpayers face one of the lowest burdens, with old-age spending consuming significantly less than 10 percent of economic output.

I’ll close with a couple of very important observations about the international data.

Sweden is not the top nation in the Mercer/CFA report. It trails Australia, Denmark, Iceland, Israel, Netherlands, and Norway – all of which have systems that are fully or partly based on mandatory private savings.

Sweden does have the lowest spending burden in the IMF. The Baltic nations all do better – and all of those countries have systems that are partly based on mandatory private savings.

It’s almost as if there’s a lesson to be learned, even if Biden and Trump want to bury their heads in the sand.

P.S. Here’s my short video making the case for personal retirement accounts.

Near the end of my testimony (about 4:55) I discuss “prioritization,” which is what would happen if the debt limit is not raised and the Treasury Department has to decide which payments are made (and which payments are delayed).

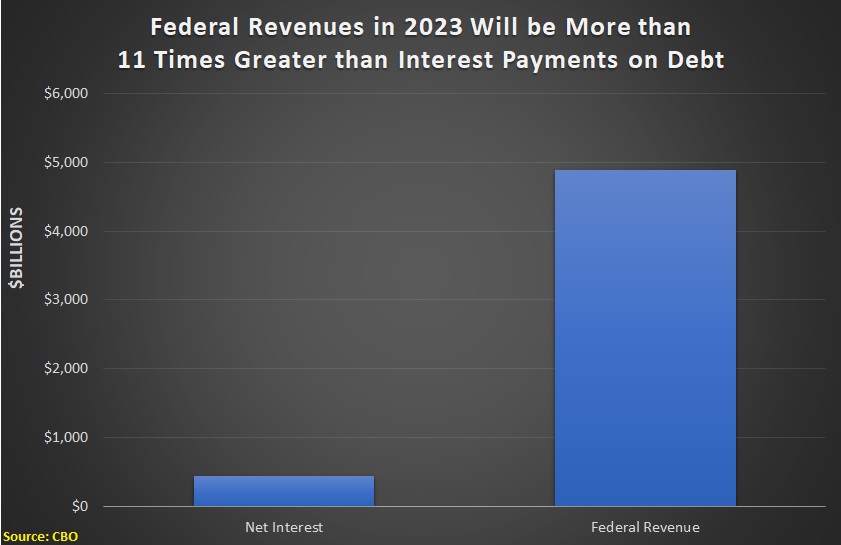

I then pointed out that federal tax revenues in 2017 were expected to be 11 times greater than annual interest payments.

As such, there obviously would have been plenty of cash available to make interest payments, as well as to finance other economically or politically sensitive items (I assume, for instance, that Treasury would have prioritized monthly Social Security benefits as well).

Would this have been messy? Yes. Would it have been uncharted territory not covered by the law? Yes. But would it have been better than default, which would have caused turmoil in financial markets? Another yes.

Which now brings us to the present day. We’re now in another debt limit fight, so I decided to look at the most-recent data from the Congressional Budget Office to see whether the federal government will still have plenty of cash so that interest payments on the debt can be prioritized.

Lo and behold, annual tax revenue this fiscal year is going to be more than 11 times greater than annual interest payments. Just like in 2017.

In other words, we presumably can sleep easy. There’s plenty of money to pay interest on the debt.

There would only be a default if Joe Biden or Janet Yellen (the Treasury Secretary) deliberately chose not to prioritize. And the odds of that happening presumably are way below 1 percent.

Some people may wonder why we should accept even that small risk? Why not simply increase the debt limit so that the odds of a default are 0 percent?

That’s a fair point, but it must be balanced by the recognition that the United States is on a path to long-run economic and fiscal chaos. So I can also understand why some lawmaker say the debt limit should only be raised if accompanied by some much-need spending restraint.

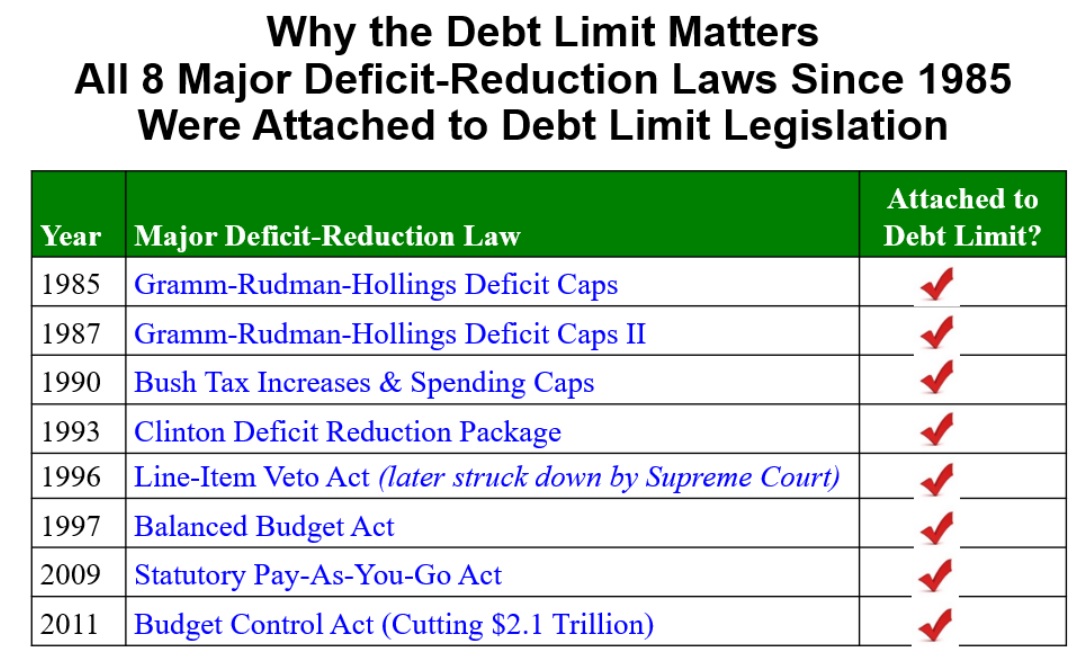

And, for those who care about real-world evidence, that’s what has happened in the past. Indeed, Brian Riedl notes that it’s the only plausible vehicle for altering the nation’s fiscal trajectory.

I’ll close by expressing pessimism that House Republicans will achieve anything in the current fight over the debt limit.

We won’t get something really good, like a spending cap. But I start with very low expectations, so I guess I’m happy that Republicans are at least pretending to care once again about excessive government spending.

A journey of a thousand miles begins with a first step!

P.S. I partially disagree with Brian Riedl’s list. The 1990 Bush tax increase was not a “deficit-reduction law.” And it was post-1994 spending restraint that produced a balanced budget, not Clinton’s 1993 tax increase.

Today, I want to underscore why it is important to focus on “the right kind” of reform.

On paper, you can save money with “means testing” of benefits, but that creates an indirect penalty on work, saving, and investment.

You can also, on paper, save money by imposing price controls on health care, but that policy has a long track record of failure.

At the risk of understatement, either of those approaches represents “the wrong kind” of entitlement reform. Indeed, those policies are not really reform. Instead, they are tinkering with systems that are fundamentally broken.

For what it is worth, most politicians do not support good reform or bad reform.

As predicted by “public choice,” their preferred approach is kicking the can down the road.

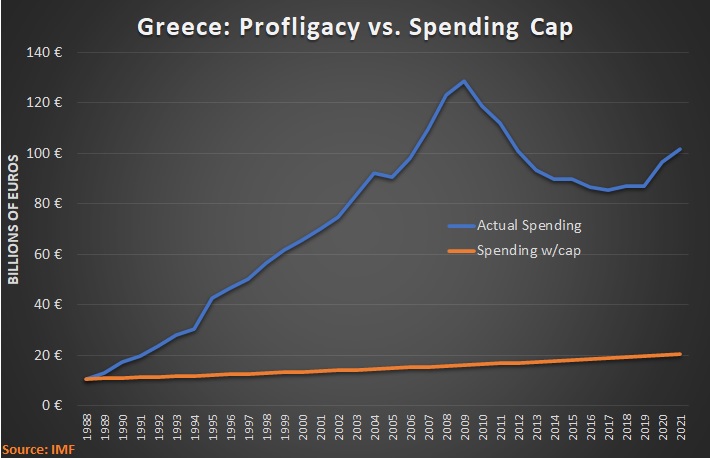

Which is what Greek politicians did for many years.

But they learned in Greece that ignoring a problem does not make it disappear. Instead, it is a recipe for fiscal crisis (and we will probably have to re-learn that lesson in Italy).

So my other goal today is to show why something needs to be done.

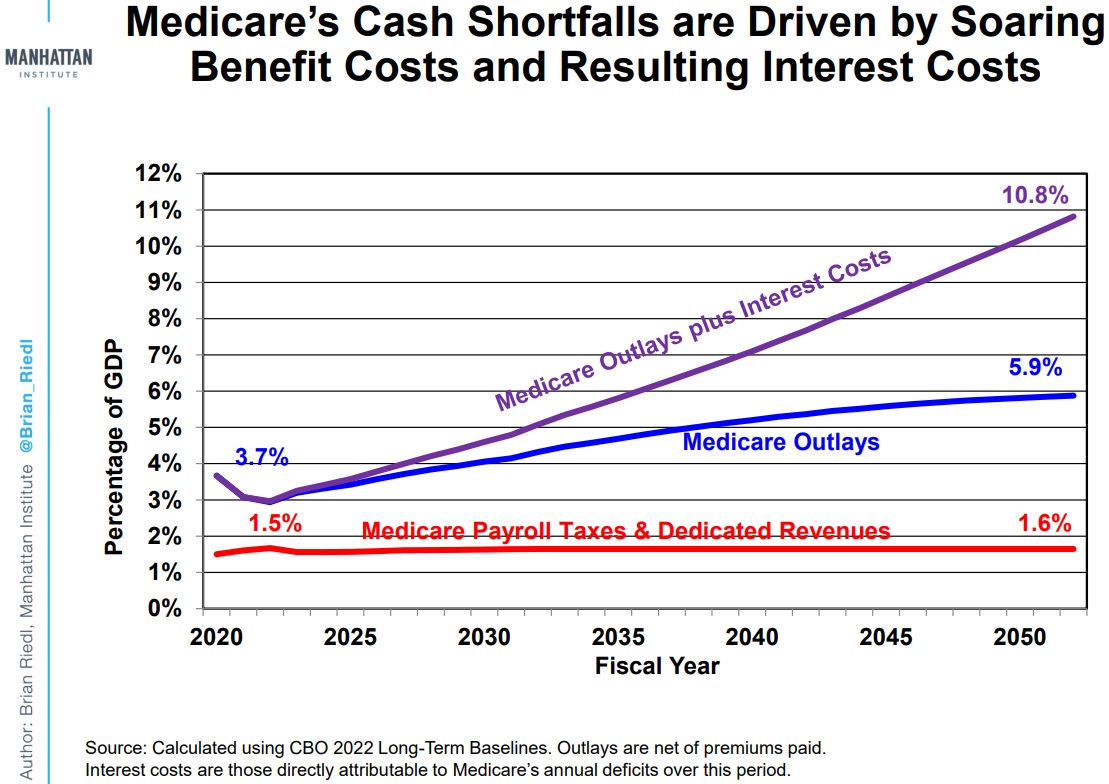

We’ll start with a look at Medicare from Brian Riedl’s chartbook.

That’s a very sobering image, so now I’ll share some very sobering words.

James Capretta of the American Enterprise Institute summarizes America’s grim fiscal future.

In 2001, the Treasury estimated the government’s net unfunded liabilities, in present value terms, at $6.5 trillion, or 61 percent of GDP, with federal debt accounting for $3.3 trillion of the measured obligations. …By 2021, the government’s net position had deteriorated to minus $29.9 trillion, or 128 percent of GDP, with federal debt accounting for $22.3 trillion of the liabilities. The government’s unfunded commitments beyond public debt had grown by $2.9 trillion over ten years. …The financial hole is actually deeper than these numbers reveal because they exclude the dramatic effects of Social Security and Medicare. …with Social Security and Medicare included in the assessment, the federal government’s unfunded liabilities in 2021 are $93.1 trillion, or nearly 400 percent of annual GDP. That compares with $11.1 trillion as calculated in the 2001 Treasury report, which was 105 percent of GDP. …The problem posed by unfunded public liabilities is a relatively new one in U.S. history. It has only been over the past half century that the combination of an aging population and the modern entitlement system has pushed the federal government toward a financial crisis.

Having shared all this depressing data, I’ll now close with a couple of observations.

Second, “funded liabilities” are hardly an improvement over “unfunded liabilities” since that simply means debt-financed spending becomes tax-financed spending. From the frying pan to the fire, or vice-versa.

As I said in the above video, we need the right kind of entitlement reform so that we save money and have better policy for old people and poor people.

My assessment is very mainstream, at least with regards to what will happen to national budgets in European nations.

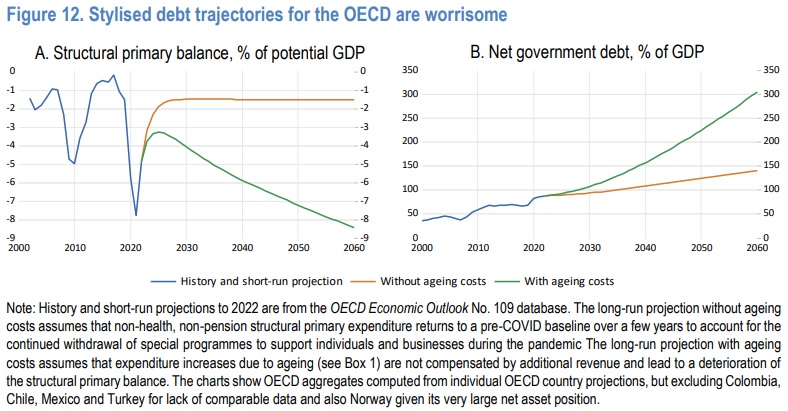

A study from the Organization for Economic Cooperation and Development, authored by Yvan Guillemette and David Turner, examines the long-run fiscal position of member nations.

It warns that government debt levels will increase dramatically if they don’t change current policies.

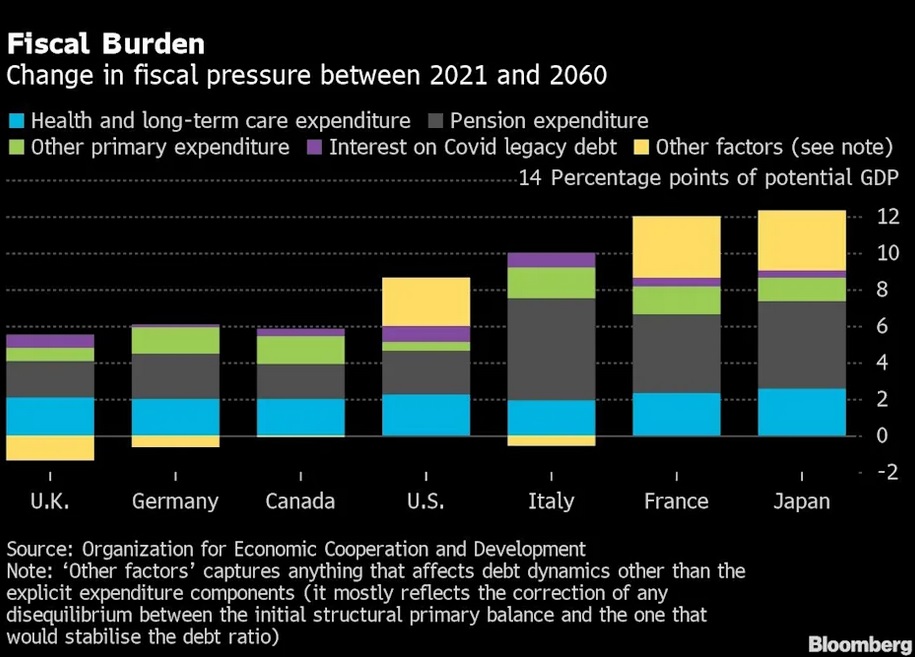

… secular trends such as population ageing and the rising relative price of services will keep adding pressure on government budgets. Without policy changes, maintaining current public service standards and benefits while keeping public debt ratios stable at current levels would increase fiscal pressure in the median OECD country by nearly 8 percentage points of GDP between 2021 and 2060, and much more in some countries. …governments will need to re-assess long-run fiscal sustainability in the context of higher initial government debt levels…when considering expenditure pressures associated with ageing…, the OECD structural primary balance would deteriorate rapidly and net government debt would more than double as a share of GDP by 2050 (Figure 12).

Here is the aforementioned Figure 12. As you can see, both deficits (left chart) and debt (right chart) are driven by the cost of age-related entitlement programs.

The report also explains that the increase in red ink is being caused by a bigger burden of government spending.

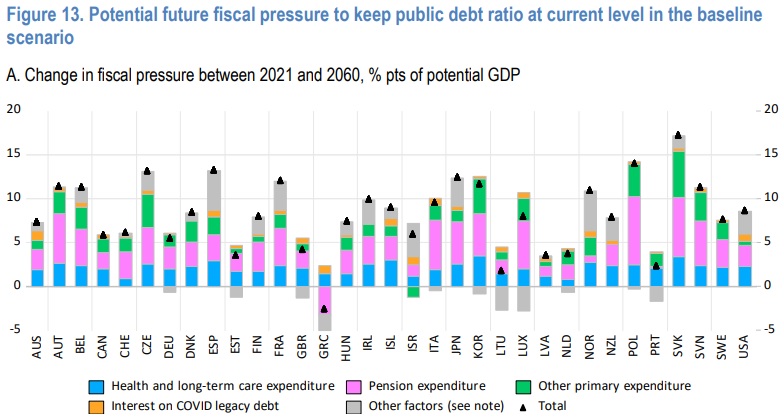

Under a ‘business-as-usual’ hypothesis, in which no major reforms to government programmes are undertaken, public expenditure is projected to rise substantially in most countries… Public health and long-term care expenditure is projected to increase by 2.2 percentage points of GDP in the median country between 2021 and 2060… Public pension expenditure is projected to increase by 2.8 percentage points of GDP in the median country between 2021 and 2060… Other primary expenditures are projected to rise by 1½ percentage points of GDP in the median country between 2021 and 2060 (Figure 13, Panel A). This projection excludes potential new sources of expenditure pressure, such as climate change adaptation.

Here’s Figure 13, mentioned above. Notice the projected increases in spending in most European nations.

Since more government spending is the problem, you might think the OECD would recommend ways to restrain budgetary expansion.

But that would be a mistake. As is so often the case, OECD bureaucrats think giving politicians more money is the best approach.

The present study…uses an indicator of long-run fiscal pressure that is premised on the idea that governments would seek to stabilise public debt ratios at projected 2022 levels by adjusting structural primary revenue from 2023 onward. … all OECD governments would need to raise taxes in this scenario to prevent gross government debt ratios from rising over time… The median country would need to increase structural primary revenue by nearly 8 percentage points of GDP between 2021 and 2060, but the effort would exceed 10 percentage points in 11 countries.

To be fair, the authors acknowledge that there might be some complications.

Raising taxes…appears feasible in some countries…, in other countries it may present a substantial challenge. In Belgium, Denmark, Finland and France, for instance, structural primary revenue is already around 50% of GDP… Pushing mainstream taxes on incomes or consumption further up, even by only a few percentage points of GDP, may be politically difficult and fiscally counter-productive if it means reaching the downward-sloping segment of the Laffer curve… Lundberg…identifies five OECD countries where top effective marginal tax rates (accounting for income, payroll and consumption taxes) are already beyond revenue-maximizing levels (Austria, Belgium, Denmark, Finland and Sweden). Thus, if taxes are to rise, it might be necessary to look to other bases, such as housing, capital gains, inheritance or wealth. Recent international efforts to establish a minimum global corporate tax could also enable more revenue to be raised from corporate taxes.

I’m happy that the study acknowledges the Laffer Curve, though that is not much of a concession since even Paul Krugman agrees that it exists.

And even when OECD bureaucrats admit that it may be unwise to increase some taxes, their response is to suggest that other taxes can be increased.

Today, here are my thoughts on why there should not be a bailout if/when a crisis occurs.

I have moral objections to bailouts, but let’s focus in this column on the practical impact.

And let’s start with this chart, which shows debt levels in Portugal, Italy, Greece, and Spain (the so-called PIGS) ever since the misguided bailout of Greece about a dozen years ago.

As you can see, OECD data reveals that there’s been no change in these poorly governed nations. They have continued to over-spend and accumulate ever-higher levels of debt.

Defenders of bailouts assert that Greece was forced to engage in “austerity” as a condition of getting a bailout.

I have two problems with that argument.

First, notice how Greece’s debt has continued to go up. If that’s a success, I would hate to see an example of failure.

Second, the main effect of the so-called austerity is a much higher tax burden and a somewhat higher spending burden.

If there’s a bailout of Italy (or any other nation), I suspect we’ll see the same thing happen. Higher taxes, higher spending, and higher debt.

I’ll close by acknowledging that there are costs to my approach. If Italy is not given a bailout, the country may have a “disorderly default,” meaning the government simply stops honoring its commitments to pay bondholders.

That is bad for individual bondholders, but it also could hurt – or even bankrupt – financial institutions that foolishly decided to buy a lot of Italian government bonds.

But there should be consequences for imprudent choices. Especially if the alternative is bailouts that misallocate global capital and encourage further bad behavior.

The bottom line is that the long-run damage of bailouts is much greater than the long-run damage of defaults.

I’m in Europe to give a couple of speeches about fiscal policy, so I’m going to spend all week commenting on the continent’s (mostly miserable) fiscal policy.

Let’s start with comments about Italy, the nation most likely to suffer a crisis.

But I’ve also noted that governments sometimes spend so much money and incur so much debt that investors decide it is very risky to buy or hold debt from those governments. In other words, they begin to fear default.

When investors (sometimes known as “bond vigilantes”) reach that stage, they probably try to get rid of their holdings and definitely refuse to buy more debt. The net result is that profligate governments have to offer much higher interest rates to compensate for the risk of a possible default.

And if peruse this data from the OECD, you find that Italian government debt has jumped to levels that may be unsustainable.

So why has Italy avoided a crisis?

As noted in this article by Desmond Lachman, published by Inside Sources, the nation is being propped up by the European Central Bank.

In Europe, when the European Central Bank (ECB) soon dials back its bond-buying program, we are likely to find out that it is the Italian economy that has been swimming naked. This should be of deep concern for the Eurozone and world economies. While the Italian economy might be too large for its Eurozone partners to allow it to fail, it also might prove to be too large for them to bail it out. …The main factor that has allowed the Italian government to finance its ballooning budget deficit on favorable terms has been the ECB’s massive government bond-buying…the ECB used its emergency bond-buying program to more than fully finance the Italian government’s borrowing needs. …it must be only a matter of time before we have another round of the Italian sovereign debt crisis. …no longer being able to count on ECB bond-buying, the Italian government will have to increasingly finance itself in the market. It will have to do so with its public finances in a worse state than they were in during the 2012 debt crisis.

In the article, Lachman thinks a crisis is all but inevitable because the ECB is unwinding its pandemic-era money creation.

I agree about the ECB’s harmful role, but I fear the central bankers in Frankfurt will continue to do the wrong thing.

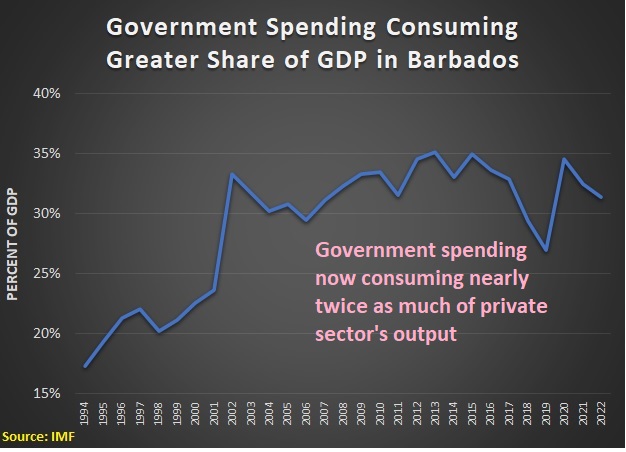

I realize few readers are interested in small, faraway countries. But I periodically write about nations such as Jordan, Cyprus, Latvia, Vanuatu, Panama, and Pakistan because they offer important lessons – mostly negative, but sometimes positive – about fiscal policy.

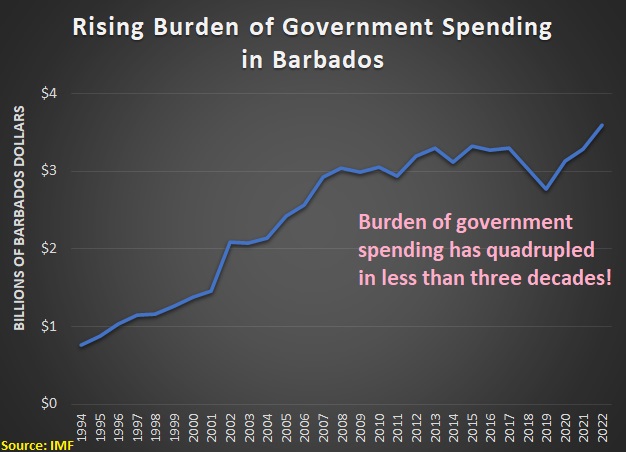

Today, let’s see what we can learn from Barbados.

That island nation in the Caribbean wound up in fiscal trouble a few years ago and Abrahm Lustgarten of the New York Times wrote a lengthy article last week about that experience.

Here’s the situation as of 2018.

Barbados was out of money. It was so broke that it was taking out new loans just to pay the interest on the old ones, even as its infrastructure was coming undone. Soon the nation would have no choice but to declare itself insolvent, instigating a battle with the dozens of banks and creditors that held its $8 billion in debt and triggering austerity measures that would spiral the island into further poverty. …Mottley, the first woman to lead Barbados, had been working…to develop a plan that would restructure the country’s soaring debts in a way that would free up money to invest in Barbados’s economy.

While the preceding excerpts are mostly to illustrate what was happening, I can’t resist two editorial comments.

Second, government spending rarelyacts as productive investment.

Now let’s get back to the story.

Prime Minister Mottley’s plan involved going to the International Monetary Fund, then headed by Christine Lagarde, for a bailout.

Mottley knew that banks and investors would work with her only if Barbados were participating in a formal I.M.F. program… Mottley wanted Lagarde to endorse an economic program that would still allow her to raise salaries of civil servants, build schools and improve piping and wiring for water and power. …No one was sure how Lagarde would respond. Would she trust Mottley to spend on Barbados first? …the director’s surprising reply: She was extremely supportive of what Mottley was proposing.

Needless to say, I don’t like bailouts. And a bailout that enables more government spending seems especially foolish.

But I like to check the numbers before making sweeping pronouncements.

So let’s see whether Barbados somehow was being hurt by inadequate levels of government spending.

But it turns out that total government spending today is more than four times greater than it was in 1994.

And if we look at government spending as a share of gross domestic product, we can see that government has nearly doubled in size.

To be fair to Ms. Mottley, the politicians in office from 1994-2008 were the most profligate.

But none of that changes the fact that government is far bigger today than it was in the recent past. So the notion that Barbados needs a bigger government budget is nonsense.

Sadly, the reporter did not bother to share any of these numbers. Indeed, in a story that ran more than 10,000 words, there were only 50 words that even hinted at the real problem.

…a mixture of poor management and corruption had eroded the country’s economy. …the country had developed a “dysfunctional” fiscal culture in which government agencies and departments took loans and negotiated deals without consulting the central bank, accumulating sprawling debt… The country’s response was to print more money and borrow more.

I’ll close by observing that Barbados never would have gotten into trouble if it had a Swiss-stylespending cap. If government spending had been allowed to grow only 3 percent each year starting in 1994, Barbados would be enjoyed a huge budget surplus today.

P.S. Ironically, economists at the IMF have written in favor of spending caps on multiple occasions. Too bad the political hacks in charge of the bureaucracy don’t pay attention to that research.

On the minus side, the party largely punted on the issue once Trump took over.

To be sure, punting is the easy route from a “public choice” perspective. Politicians like offering freebies to voters and many voters like getting handouts.

The Wall Street Journaleditorialized about the downside of making America more like Europe last October.

The result of…expanded entitlements is likely to be reduced incentives to work and invest, slower economic growth, lower living standards, and less fiscal space for essential public goods like national defense. That’s the lesson from Europe’s cradle-to-grave welfare states… Europe’s little-discussed secret is that its cradle-to-grave welfare states are financed by the middle class via value-added and payroll taxes. The combined employer-employee social security tax rate is 36% in Spain, 40% in Italy and 65% in France. Value-added taxes in most European economies are around 20%. There simply aren’t enough rich to finance their entitlements.

And what’s remarkable (and discouraging) is that some politicians in the U.S. want to expand entitlements even though many European governments now realize they made big mistakes and need to scale back.

The irony is that some European governments have tried to reform their tax and welfare systems to become more competitive. Germany and Sweden over two decades reformed their welfare and labor policies. …Other European governments are also pushing welfare-state reforms. French President Emmanuel Macron has passed pension reform and cut the corporate tax rate to 26.5% from 33% in 2017… Greece is pulling out of its debt trap with Prime Minister Kyriakos Mitsotakis’s tax, pension and regulatory reforms.

For what it’s worth, I’m happy about these reforms, but I fear many European nations are in the too-little-too-late category.

But if (or when) that happens, maybe American politicians will finally wake up and realize we need good reforms to prevent Social Security, Medicare, and Medicaid from causing a similar collapse on this side of the Atlantic Ocean..

Hopefully that epiphany will take place before it is too late for the United States.

P.S. For those who are interested in the history of fiscal policy, John Cogan of the Hoover Institution wrote about pre-20th-century entitlements earlier this year.

Here are excerpts from his column in the Wall Street Journal.

The history of U.S. entitlements is a 230-year record of continuous expansion… The first major entitlement, Revolutionary War disability benefits, was initially restricted to members of the Continental Army and Navy who were injured in battle and survivors of those killed in wartime. Eligibility was then expanded, first to state militia soldiers, then to veterans whose disabilities were unrelated to wartime service, and eventually to virtually all people who served during the war regardless of disability. Civil War disability pensions followed the same…process, except on a far grander scale. Pensions were initially confined to U.S servicemen who suffered wartime injuries and survivors of those killed in battle. Eventually they were extended to virtually all union Civil War veterans regardless of disability. …Congress followed the same liberalizing process with 20th-century entitlements.

If this excerpt doesn’t satisfy your curiosity, here’s Cogan discussing the topic for 46 minutes.

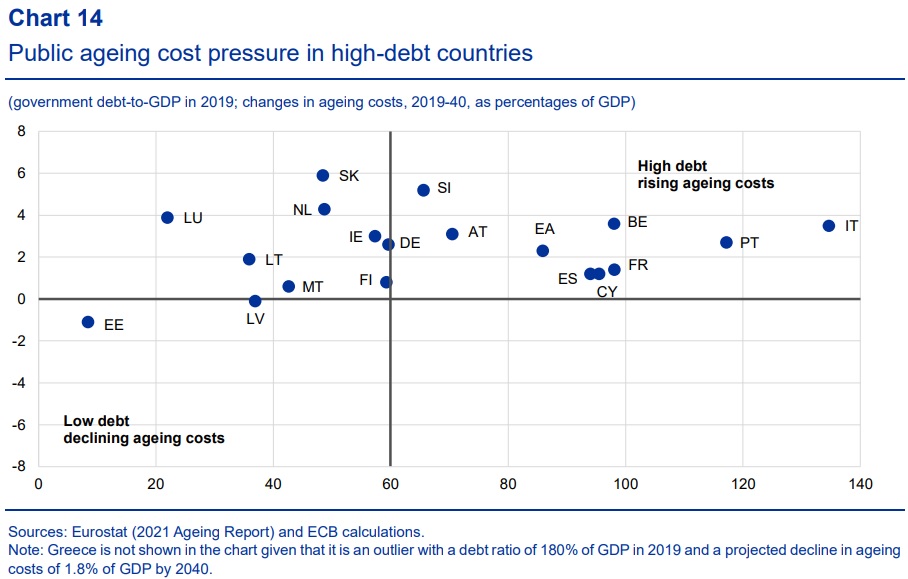

It showed which European nations were in the unfortunate position of facing big future spending increases (the vertical axis) combined with already-high levels of government debt (the horizontal axis).

The bottom line is that Italy, Portugal, France and Belgium face a very difficult fiscal future.

And Estonia (at least relatively speaking) is in the best shape.

Today we are going to augment those ECB numbers by looking at some data from the OECD’s recent report on Estonia.

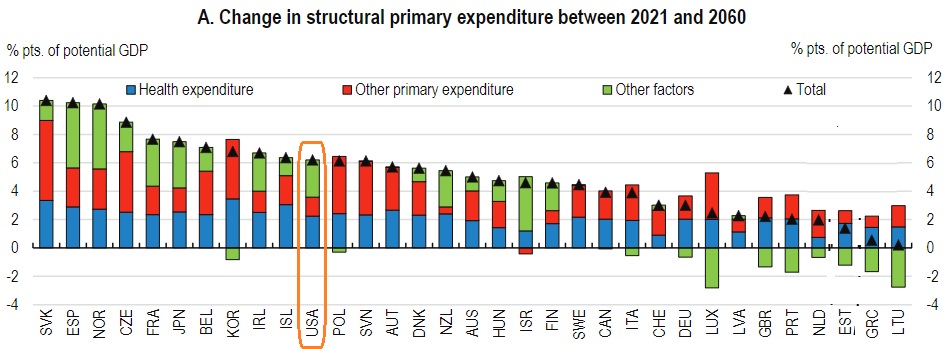

Here’s a chart showing how the burden of government spending is going to increase in various nations between now and 2060.

Slovakia, Spain, Norway, and the Czech Republic have the biggest problem.

Lithuania is in the best shape, surprisingly followed by Greece (I assume because that nation already hit rock bottom, not because of good policy).

I also highlight the United States, which will have to face the challenge of above-average spending increases.

But if you want to know which nation will be the next to suffer fiscal collapse, you also need to know whether (or the degree to which) it has the capacity – or “fiscal space” – to endure a bigger burden of government spending.

James Capretta addressed that topic in an article for the Bulwark.

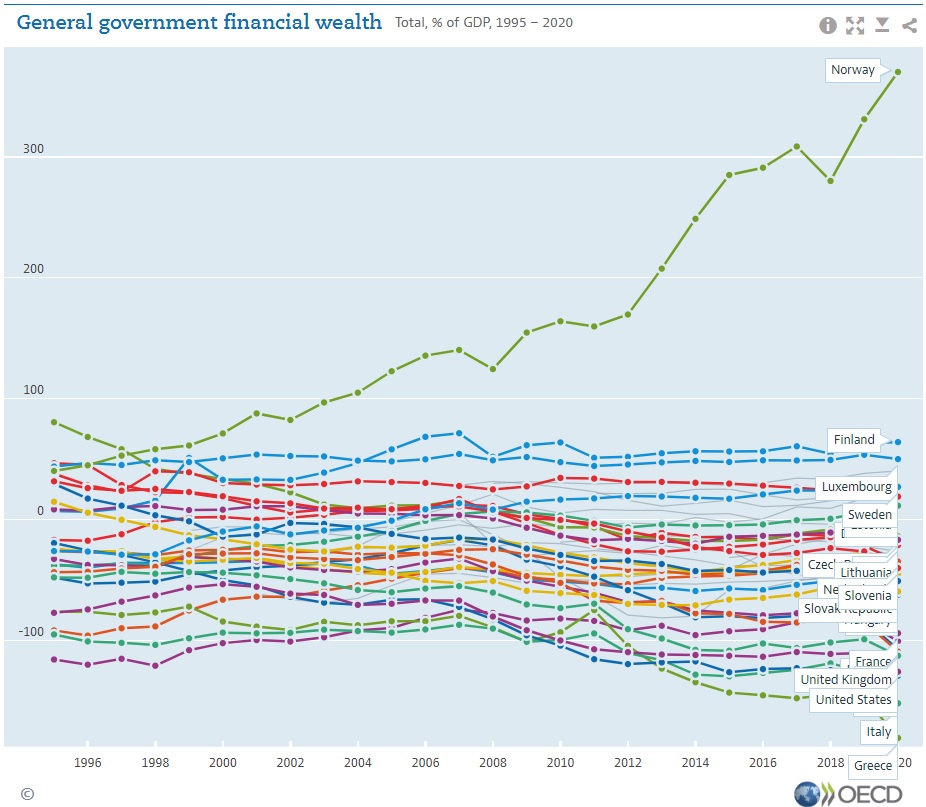

Which governments have exercised budgetary restraint in recent years, even while confronting sequential global crises? Which have been more profligate? And what do the differences portend for their differing abilities to handle an era when servicing debt may be more expensive than it has been in many years? …Accuracy…requires assessing both assets and liabilities. …The Organization for Economic Cooperation and Development…’s most comprehensive measure of fiscal resilience is the “financial net worth” of the reporting countries, which includes the main sources of accumulated liabilities (especially public debt) along with financial assets owned by governments.

And here’s a chart showing how developed nations (with the exception of oil-rich Norway) have been spending themselves into a fiscal ditch.

Here are some of Capretta’s observations.

Among the twenty-seven OECD countries that reported data every year from 1995 to 2020, the average deterioration in their net financial position, weighted by population size, was equal to 48 percent of GDP. …Several countries stand out for the steepness of their declines. Japan’s net financial position was -20 percent of GDP in 1995, and in 2020 it was -129 percent of GDP—in other words, in just 25 years it worsened by over 100 percent of the country’s annual GDP. Similarly, the United Kingdom experienced a serious deterioration, with a net financial position in 2020 equal to -109 percent of GDP. In 1995, it was -26 percent. …France, Greece, Italy, and Spain are regularly criticized for their uneven approaches to fiscal discipline. The OECD data showing a substantial deterioration of their net financial positions over the last quarter century provides more evidence that each of these countries needs to take further steps to lower the risk of a fiscal crisis in future years.

The United States obviously is not in good shape, though I think the OECD’s methodology is imperfect.

Yes, America will have to deal with a fiscal crisis if we don’t figure out a way of controlling spending, but I suspect many other countries will reach that point before the U.S. (with Italy quite likely being the next to go belly up).

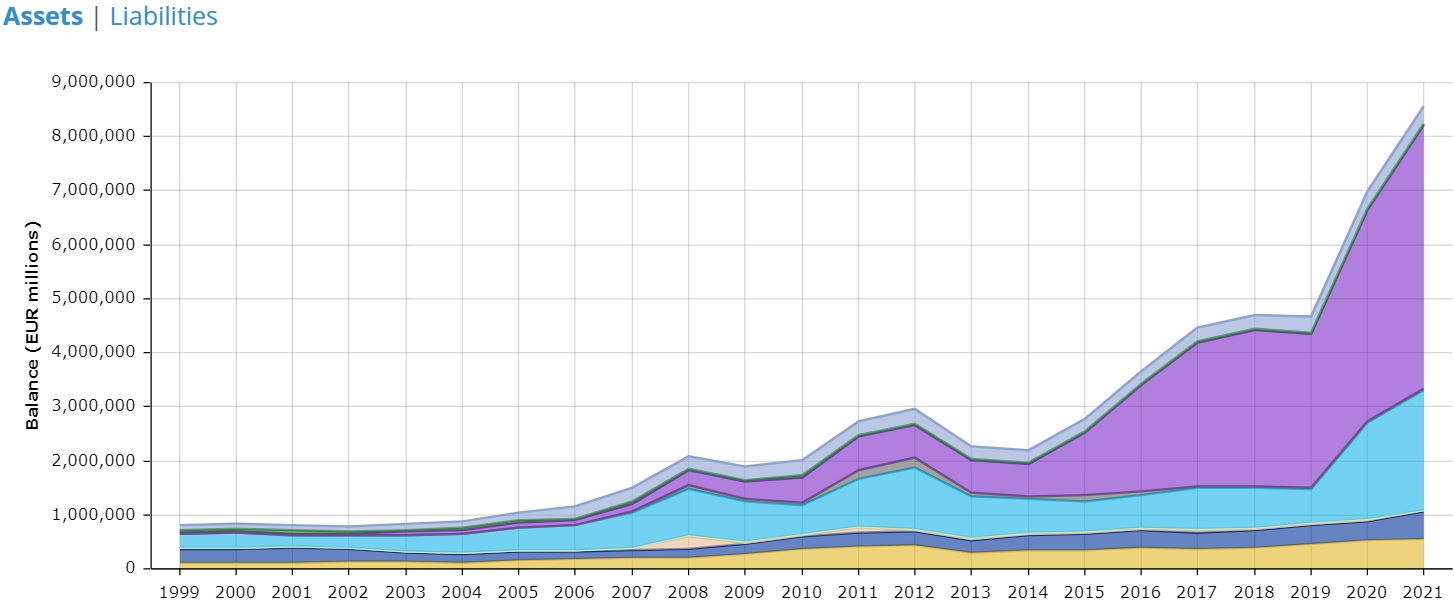

The Federal Reserve is not the only central bank to make this mistake.

Here’s the balance sheet for the Eurosystem (the European Central Bank and the various national central banks that are in charge of the euro currency). As you can see, there’s also been a dramatic increase in liquidity on the other side of the Atlantic Ocean.

Why should American readers care about what’s happening with the euro?

But this is more than a lesson about monetary policy. What’s happened with the euro may have created the conditions for another European fiscal crisis (for background on Europe’s previous fiscal crisis, click here, here, and here).

In an article for Project Syndicate, Willem Buiter warns that the European Central Bank sacrificed sensible monetary policy by buying up the debt of profligate governments.

…major central banks have engaged in aggressive low-interest-rate and asset-purchase policies to support their governments’ expansionary fiscal policies, even though they knew such policies were likely to run counter to their price-stability mandates and were not necessary to preserve financial stability. The “fiscal capture” interpretation is particularly convincing for the ECB, which must deal with several sovereigns that are facing debt-sustainability issues. Greece, Italy, Portugal, and Spain are all fiscally fragile. And France, Belgium, and Cyprus could also face sovereign-funding problems when the next cyclical downturn hits.

Mr. Buiter shares some sobering data.

All told, the Eurosystem’s holdings of public-sector securities under the PEPP at the end of March 2022 amounted to more than €1.6 trillion ($1.7 trillion), or 13.4% of 2021 eurozone GDP, and cumulative net purchases of Greek sovereign debt under the PEPP were €38.5 billion (21.1% of Greece’s 2021 GDP). For Portugal, Italy, and Spain, the corresponding GDP shares of net PEPP purchases were 16.4%, 16%, and 15.7%, respectively. The Eurosystem’s Public Sector Purchase Program (PSPP) also made net purchases of investment-grade sovereign debt. From November 2019 until the end of March 2022, these totaled €503.6 billion, or 4.1% of eurozone GDP. In total, the Eurosystem bought more than 120% of net eurozone sovereign debt issuances in 2020 and 2021.

Other experts also fear Europe’s central bank has created more risk.

Two weeks ago, Desmond Lachman of the American Enterprise Institute expressed concern that Italy had become dependent on the ECB.

…the European Central Bank (ECB) is signaling that soon it will be turning off its monetary policy spigot to fight the inflation beast. Over the past two years, that spigot has flooded the European economy with around $4 trillion in liquidity through an unprecedented pace of government bond buying. The end to ECB money printing could come as a particular shock to the Italian economy, which has grown accustomed to having the ECB scoop up all of its government’s debt issuance as part of its Pandemic Emergency Purchase Program. …the country’s economy has stalled, its budget deficit has ballooned, and its public debt has skyrocketed to 150 percent of GDP. …Italy has had the dubious distinction of being a country whose per capita income has actually declined over the past 20 years. …All of this is of considerable importance to the world economic outlook. In 2010, the Greek sovereign debt crisis shook world financial markets. Now that the global economy is already slowing, the last thing that it needs is a sovereign debt crisis in Italy, a country whose economy is some 10 times the size of Greece’s.

Over the past two years, the ECB’s bond-buying programs have kept countries in the eurozone’s periphery, including most notably Italy, afloat. In particular, under its €1.85 trillion ($2 trillion) pandemic emergency purchase program, the ECB has bought most of these countries’ government-debt issuance. That has saved them from having to face the test of the markets.

The ECB engaged in a large-scale bond-buying program over the past two years…, as did the U.S. Federal Reserve. The size of the ECB’s balance sheet increased by a staggering four trillion euros (equivalent to $4.4 billion), including €1.85 trillion under its Pandemic Emergency Purchasing Program. …The ECB’s massive bond buying activity has been successful in keeping countries in the eurozone’s periphery afloat despite the marked deterioration in their public finances in the wake of the pandemic.

Unlike bailouts and easy money, which exacerbate the underlying problems.

P.S. For what it is worth, I do not think a common currency is necessarily a bad idea. That being said, I wonder if the euro can survive Europe’s awful politicians.

P.P.S. While I think Mr. Buiter’s article in Project Syndicate was very reasonable, I’ve had good reason to criticize some of his past analysis.

We’ll start with this video from Kite and Key Media, which correctly observes that entitlement programs are the main cause of red ink.

I like that the video pointed out how tax-the-rich schemes wouldn’t work, though it would have been nice if they added some information on how genuine entitlement reform could solve the problem (as you can see here and here, I’ve also nit-picked other debt-themed videos).

But my main message, which I’ve shared over and over again, is that deficits and debt are merely a symptom. The underlying disease is excessive government spending.

Now let’s look at some recent articles on the topic.

We’ll start with Eric Boehm’s column for Reason, which explains how red ink has exploded in recent years.

America’s national debt exceeded $10 trillion for the first time ever in October 2008. By mid-September 2017 the national debt had doubled to $20 trillion. …data released by the U.S. Treasury confirmed that the national debt reached a new milestone: $30 trillion. …Entitlements like Social Security and Medicare are in dire fiscal straits and will become even more costly as the average American gets older. Even without another unexpected crisis, deficits will exceed $1 trillion annually, which means the debt will continue growing, both in real terms and as a percentage of the economy. The Congressional Budget Office estimates that the federal government will add another $12.2 trillion to the debt by 2031.

As already stated, I think the real problem is the spending and the debt is the symptom.

But it is possible, of course, that debt rises so high that investors (the people who buy government bonds) begin to lose faith that they will get repaid.

At that point, governments have to pay higher interest rates to compensate for perceived risk of default, which exacerbates the fiscal burden.

And if there’s not a credible plan to fix the problem, a country can go into a downward spiral. In other words, a debt crisis.

This is what happened to Greece. And I think it’s just a matter of time before it happens to Italy.

Could the United States also be hit by a debt crisis? Will we reach a “tipping point” that leads to the aforementioned loss of faith?

That’s one of the possibilities mentioned in the New York Timescolumn by Peter Coy.

It’s hard to know how much to worry about the federal debt of the United States. …Either the United States can continue to run big deficits and skate along with no harm done or it’s at risk of losing investors’ confidence and having to pay higher interest rates on its debt, which would suppress economic growth. …the huge increase in federal debt incurred during and after the past two recessions — those of 2007-09 and 2020 — has used up a lot of the “fiscal space” the United States once had. In other words, the federal government is closer to the tipping point where big increases in debt finally start to become a real problem. …any given amount of debt becomes easier to sustain as long as the growth rate of the economy (and thus the growth rate of tax revenue) is higher than the interest rate on the debt. In that scenario, interest payments gradually shrink relative to tax revenue. …but it doesn’t explain how much more the debt can grow. …Past a certain point, there’s a double whammy of more dollars of debt plus higher interest costs on each dollar. …sovereign debt crises tend to be self-fulfilling prophecies: Investors get nervous about a government’s ability to pay, so they demand higher interest rates, which raise borrowing costs and produce the bad outcome they feared. It’s a dynamic that Argentines are familiar with — and that Americans had better hope they never experience.

For what it’s worth, I think other major nations will suffer fiscal crisis before the problem becomes acute in the United States.

I realize this will make me sound uncharacteristically optimistic, but I’m keeping my fingers crossed that this will finally lead politicians to adopt a spending cap so we don’t become Argentina.

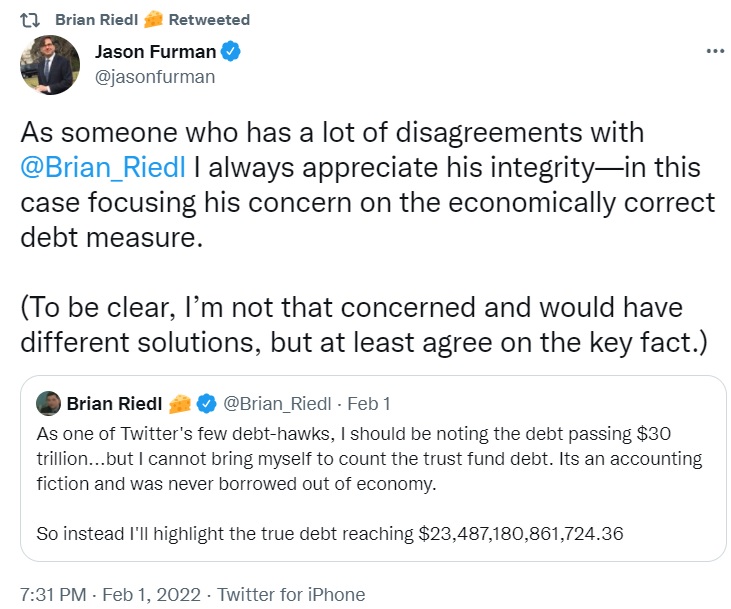

P.S. The Wall Street Journal recently editorialized on the issue of government debt and made a very important point about the difference between the $30 trillion “gross debt” and the “debt held by the public,” which is about $6 trillion lower.

…the debt really isn’t $30 trillion. About $6 trillion of that is debt the government owes to itself in Social Security and other IOUs. …The debt held by the public is some $24 trillion, which is bad enough.

As I’ve noted when writing about Social Security, the IOUs in government trust funds are not real.

Indeed, if you want to know whether some is both honest and knowledgeable about budget matters, ask them which measure of the national debt really matters.

As you can see from this exchange of tweets, competent and careful budget people (regardless of whether they favor big government or small government) focus on “debt held by the public,” which is the term for the money government actually borrows from credit markets.

If you want to know the difference between the various types of government debt – including “unfunded liabilities” – watch this video.

This battle will be decided in next 12 months, hopefully with a defeat for Biden’s dependency agenda.

Regardless of how that fight is resolved, though, we’re eventually going to get to a point where sensible people are back in charge. And when that happens, we’ll have to figure out how to restore the nation’s finances.

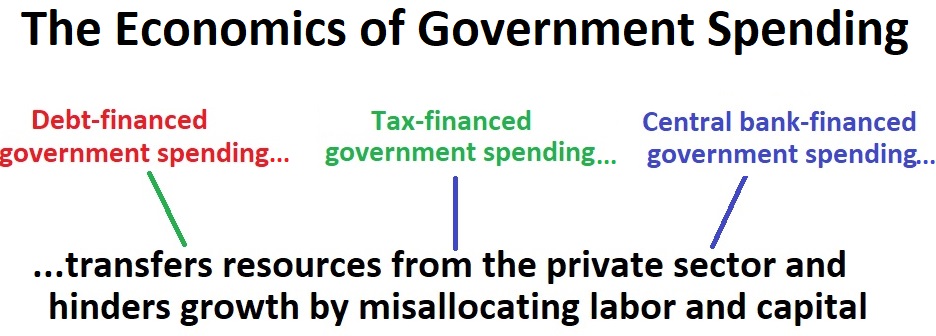

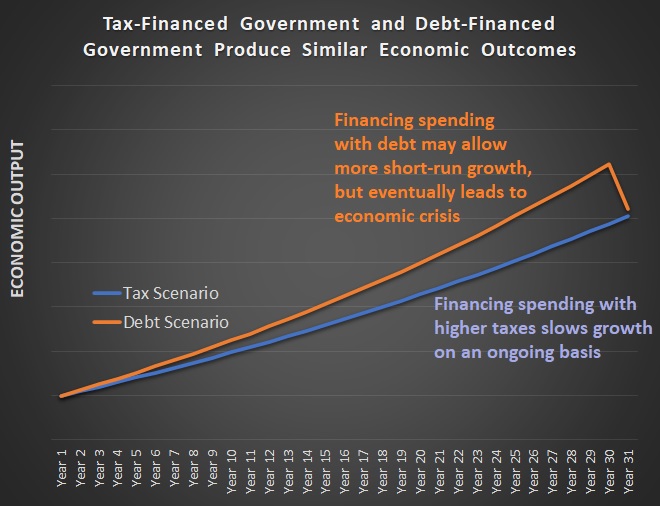

That requires figuring out the appropriate goal. Here are two options:

Keeping taxes low.

Controlling debt.

These are both worthy objectives.

But, as a logic teacher might say, they are necessary but not sufficient conditions.

Here’s a chart showing how a policy of low taxes (the orange line) presumably enables faster growth, but also creates the risk of an eventual economic crisis if nothing is done to control spending and debt climbs too high (think Greece).

By contrast, the chart also shows that it’s theoretically possible to avoid an economic crisis with higher taxes (the blue line), but it means less growth on a year-to-year basis.

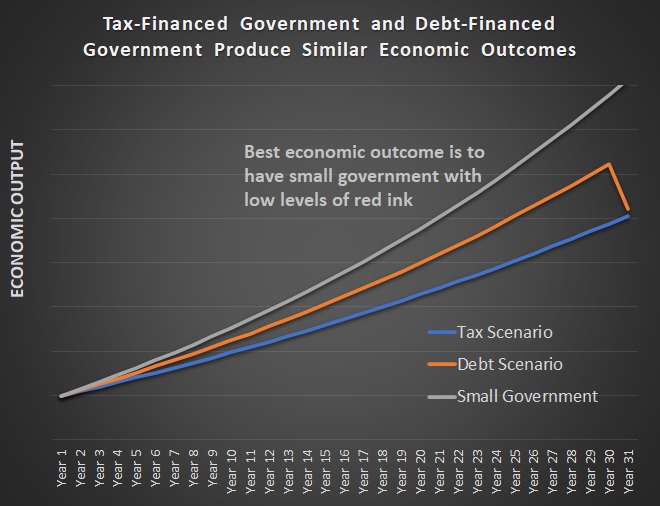

The economic benefits of this approach are illustrated in this second chart. We enjoy faster year-to-year growth. And, because spending restraint is the best way of controlling debt, the risk of a Greek-style economic crisis is averted.

Now for some caveats.

I made a handful of assumptions in the above charts.

The economy grows 2.0 percent annually for the next 31 years with tax-financed spending

The economy grows 2.5 percent annually with debt-financed spending, but suffers a 10 percent decline in Year 31.

The economy grows 3.0 percent annually for the next 31 years with smaller government (thus enabling low taxes and less debt).

Anyone can create their own spreadsheet and make different assumptions.

So feel free to make your own assumptions about the strength of these effects, but let’s never lose sight of the fact that spending restraint should bethe main goal for post-Biden fiscal policy.

Instead, I pointed out about five years ago that they have allowed the spending burden to rise, as measured by outlays as a share of economic output.

Well, things have since gone even further in the wrong direction, exacerbated by long-run factors such as demographic decline and short-run factors such as the coronavirus pandemic.

So what’s the net result?

Writing for the Hill, Desmond Lachman of the American Enterprise Institute is concerned about the possibility of a new round of fiscal chaos in Europe.

In 2010, the Eurozone experienced a sovereign debt crisis that shook the world economy. Today…, it appears that the Eurozone could be well on the way to another such debt crisis. It is not only that the public finances of several key countries in the Eurozone periphery are considerably worse than they were on the eve of the 2010 sovereign debt crisis. It is also that inflation has risen to a level that will make it difficult for the European Central Bank (ECB) to continue to keep the Eurozone periphery governments afloat by a continuation of bond purchases on the massive scale that it has been doing to date. …Over the past 18 months, in response to the pandemic and with a view to stimulating the European economy, the ECB increased the size of its balance sheet by more than $4 trillion. …The fly in the ointment for countries such as Italy and Spain is that they cannot expect that the ECB will continue to buy their bonds on a large scale forever. …Another reason to fear an early end to the ECB’s massive bond-buying program is the strong resistance to such bond buying by the Eurozone’s northern member countries in general and by Germany in particular. These countries view the ECB’s bond-buying activities as a move to a fiscal union through the backdoor.

Excellent points, particularly with regard to the malignant role of the European Central Bank, which has created the conditions for a much bigger crisis by enabling bigger government and more debt.

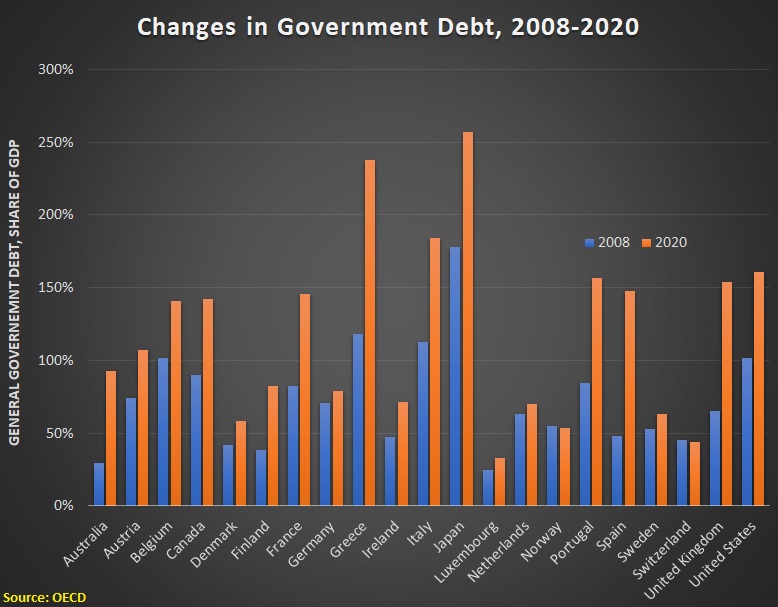

If you want to understand how much worse the debt problem is today, here’s a chart based on OECD data for European nations (with the U.S. and Japan added for purposes of comparison.

But there’s one future crisis that we already know about, and I recently spoke about that issue to the Liberty International World Conference in Medellin.

At first, I wasn’t planning to share this video, particularly since I covered much of the same material in a speech back in January.

But then I saw a story in Yahoo Finance that includes this very sobering chart about how the burden of government spending will climb in G-7 nations over the next four decades.

That includes the United States. The four-decade outlook for America isn’t as bad as it is in nations such as France and Japan, but government will grow more than the fiscal burdens in Canada, Germany, and the United Kingdom.

And here are some details from the story.

The Covid-19 pandemic may have bloated public debt…, but that’s nothing compared to the fiscal difficulties brewing in the coming decades, the OECD said. …states will face rising costs, particular from pensions and health care. To maintain public services and benefits while stabilizing debt in that environment, governments would have to raise revenues by nearly 8% of gross domestic product, the OECD said. In some countries, including France and Japan, the size of the challenge would amount to more than 10% of output, and the economists didn’t even account for new expenditures such as climate change adaptation.