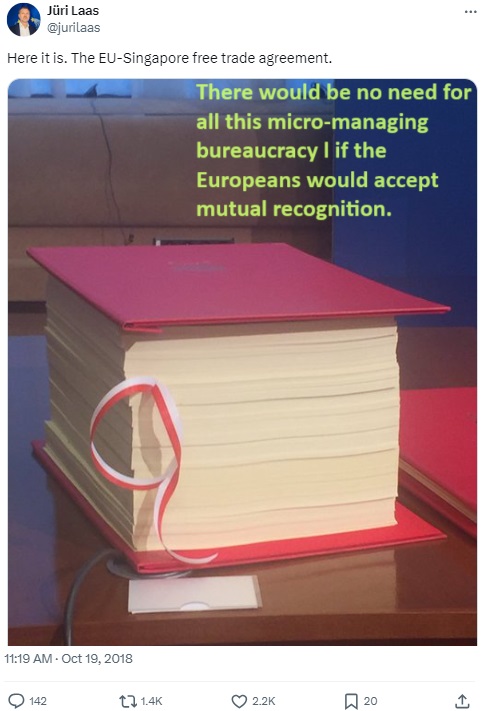

Almost exactly six years ago, I shared a column with this video of a member of the European Parliament explaining the principle of mutual recognition.

But that column was mostly about the benefits of jurisdictional competition and I only mentioned mutual recognition as a side issue.

So let’s examine today why mutual recognition is a good principle for cross-border economic relations.

Let’s start with a definition. Mutual recognition happens when two of more jurisdictions agree to have open trade and to respect each other’s laws.

So that means (as noted in the video) that, for example, Brits can buy food and other products from Germany and Germans can buy food and other products from the United Kingdom – regardless of the laws that govern production in the two nations.

For my American readers, here are three very real examples of why mutual recognition is a good idea.

As even AOC recognizes, it would allow Americans to buy superior sunscreens from Europe that our sluggish FDA bureaucrats have not approved.

It would prevented the 2022 baby formula crisis because American families could have purchased safe and nutritious European varieties.

Another reason to support mutual recognition is that it would make trade agreements much simpler. I wrote in 2019 that the ideal free trade agreement is one simple sentence prohibiting trade barriers.

But that’s only possible with a system of mutual recognition. Ryan Young and Kent Lassman of the Competitive Enterprise Institute recently wrote on this issue for National Review.

Here are some excerpts.

The core concept behind a simple FTA is mutual recognition of one another’s regulations. Under mutual recognition, if American regulators approve a product, then it is automatically approved in partner countries, and vice versa. With that sort of regulatory trade barrier lowered, consumers can quickly benefit from wider selection, more affordable prices, and faster access to new innovations. Producers would benefit from faster approval times and lower regulatory costs for pharmaceuticals, appliances, agricultural products, electronics, and countless other industries, while gaining access to new markets and new customers. Regulators would benefit by avoiding redundant approvals in each partner country, saving agency resources. …Mutual recognition is appropriate for strong allies in developed countries… Our regulations may not be identical but will be similar enough for trade purposes. …A mutual-recognition agreement with Switzerland or another close ally could set a precedent that can lead to larger agreements that would boost economies around the world while strengthening alliances against Russia and China.

Amen.

Simple trade agreements with allied nations should be based on mutual recognition.

I quoted Professor Michael Greve many years ago and he’s worth quoting again.

…the origin principle…is commonly called the principle of “mutual recognition.” …it is the only principle that is consistent with both a common economic market and political decentralization. Mutual recognition integrates member states without central intervention. …Mutual recognition, then, liberates commerce by eliminating the cost of complying with different, conflicting, and often incomprehensible rules. Beyond that, mutual recognition institutionalizes jurisdictional competition. …The ability of individuals and firms to vote with their feet, modems, and pocketbooks will liberate markets and discipline politicians. …Trade unions, environmental interests, and any other interest group whose agenda rests on redistribution consistently oppose mutual recognition: they cannot rob Peter to pay Paul if Peter is allowed to escape to more hospitable climes.

By the way, the United Kingdom seems to have some very sensible people with regards to mutual recognition, as illustrated by this Alex Tabarrok article and this tweet.

The UK has announced unilateral recognition for medicines approved overseas.

If Japan or the US approves a drug, you will be able to prescribe it in the UK.

Aiming to create fastest route to market in the world for new medicines.

P.S. The good news is that the European Union was founded in part on the principle of mutual recognition. The bad news is that politicians are increasingly replacing that sensible approach with the dirigiste model of harmonization. Bad globalism in action.

In part, the results are boring because – once again – Estonia has the best-designed tax system of all OECD nations.

To make things even more boring, the top four nations have been the same four years in a row.

Latvia is in second place. Again. New Zealand is in third place. Again. Followed by Switzerland in fourth place. Again.

Here are the full rankings (click to enlarge).

Colombia is in last place, so we can safely assume it is not on a path to becoming a rich nation. And Chile also gets a bad score (which is only partly the fault of the nation’s moronic president since Chile routinely has been near the bottom).

Among nations from Western Europe, France, Italy, and Portugal get the worst scores. Which seems to be an annual tradition.

Since more than three-fourths of my readers are American, let’s close with some analysis of the United States.

The bad news is that the United States is in the bottom half, ranking #21 out of 38 countries.

The good news is that the United States routinely used to be one of the five worst countries.

So be thankful for the 2017 tax legislation, which substantially improved America’s score for corporate tax (the US has always had a good score for consumption taxes, presumably in large part because we haven’t made the mistake of imposing a value-added tax).

P.S. One potential shortcoming of the Index is that there is no variable for the overall tax burden. This is a deliberate choice since the Tax Foundation wants to focus on the structure of the tax system. As noted in the Frequently Asked Questions, “The Index is concerned about how a tax system is structured; not how much revenue is raised by that system. …The Index is designed to help policymakers determine better ways to levy taxes rather than encourage high or low overall levels of tax

revenue.”

Nothing wrong with that approach, of course, but people interested in the structure and the burden of taxation should look at this Tax Foundation report in conjunction with the fiscal data from either Economic Freedom of the World and/or the Index of Economic Freedom.

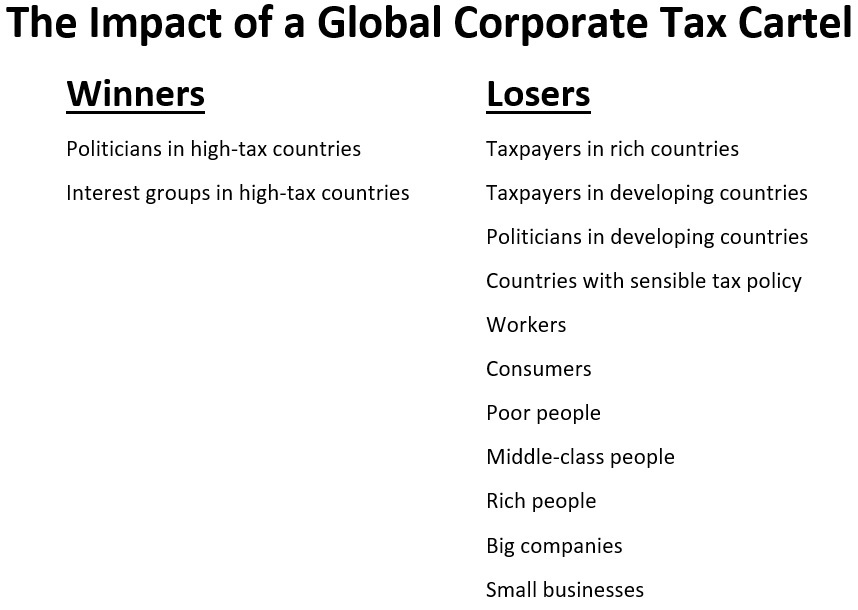

I think all the groups are correctly categorized, but my error was having an incomplete list of winners and losers.

Before identifying who they are, let’s start by looking at some excerpts from a Wall Street Journalcolumn by Aharon Friedman last August. He aptly summarizes the scheme.

Imagine if California and other left-wing states conspired to require every state to impose high taxes. …Under the conspiracy, if, say, Florida, refused to comply, the other states would tax companies on their income earned in Florida to make up the difference. …foreign governments and the Organization for Economic Cooperation and Development are working to enact exactly such a regime to increase taxes around the world to fund the left’s priorities. If Congress doesn’t comply, other countries would punish the U.S. by taxing American companies on income earned in the U.S. to make up the difference. …Americans generally dislike our Internal Revenue Code and Internal Revenue Service, but imagine a new global revenue code and global revenue service. There is no global supreme court to prevent foreign countries from taxing American companies in violation of our treaties.

Now that we have a description of the OECD’s plan, what were my sins of omission?

Who should be added to my list of winners and losers?

Well, this year Aharon explained in another WSJ column how the OECD’s tax cartel has rules that are bad for American competitiveness…and bad for American national security.

The U.S. Constitution specifies that Congress, not unelected bureaucrats or foreign adversaries, is in charge of crafting our nation’s tax laws. …Yet Treasury Secretary Janet Yellen is turning this bedrock principle on its head by writing a global tax code with the help of European bureaucrats that would redound to the benefit of Beijing. …Ms. Yellen is encouraging such taxation as a way to coerce Congress… The complex rules…favor companies that emphasize social activism over profits, as well as state-owned enterprises, at the expense of capitalist competitors. This will benefit countries that take a broad view of government power, especially China… the framework mandates an expansive information-sharing regime among countries that have adopted the global tax code. Providing such detailed information on American defense and tech companies to the likes of China… The global tax code is also likely to push low-income countries toward state-owned foreign investment—such as China’s Belt and Road initiative.

My losers list does include “big companies,” but perhaps it would be best to also specifically mention “American firms.”

We can also add “U.S. national security” in the minus column.

And we should probably add “China” to the winners list.

But there may also be another winner. All businesses will be hurt by a global tax cartel, but European companies may get a competitive advantage if the plan disproportionately hurts U.S. businesses.

Which is what will happen. In an April columnin the WSJ, Phil Gramm and Mike Solon summarize how American companies are being targeted by the OECD’s tax cartel.

President Biden has now spearheaded the international agreement to let foreign nations tax American companies… The OECD minimum-tax agreement is estimated to collect some $236 billion in new taxes… The Oxford Center for Business Taxation has estimated the U.S. will pay 64% of the profits tax, compared with 9.5% for China, 3.8% for the U.K., 1.6% for Germany and 0.7% for France. …the European Union, which dominates the OECD, is playing it with a willing American partner. It’s easy to understand why other countries are willing to agree to an international tax system in which Americans pay most of the taxes. But the White House’s championing of the tax reveals how committed the administration is to pushing big government everywhere and how desperate it is to raise U.S. corporate taxes.

The bottom line is that the OECD’s global corporate tax cartel is a terrible idea (see here, here, and here for more evidence).

Early in the Biden years, I wrote a three-part series (here, here, and here) to explain why a global minimum tax on companies is a bad idea.

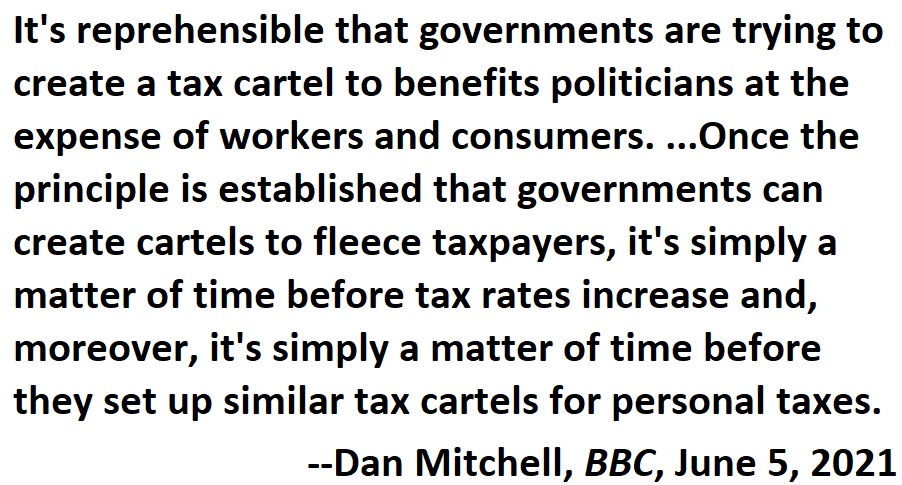

As I told the BBC back in 2021, this proposed tax cartel is a scheme to increase the tax burden and will be very bad news for workers, consumers, and shareholders.

Folks on the left, however, like the idea of politicians having more power and money. So they defend the cartel, which was organized by the bureaucrats at the Paris-based Organization for Economic Cooperation and Development.

In a column for the Washington Post, Natasha Sarin and Kimberly Clausing try to defend the OECD’s tax harmonization scheme.

Republican lawmakers…are attacking…the global minimum tax. …We both worked at Treasury when the agreement was forged, and we believe strongly that it represents an important step forward. …the deal brings together more than 135 jurisdictions, representing about 95 percent of the world economy, to stem the damaging race-to-the-bottom competition that allows the world’s largest multinational companies to shift income offshore rather than pay their fair share at home. The key mechanism is a 15 percent minimum tax — hence the name — and the agreement should be applauded, not pilloried.

The column lists five claims supposedly made by congressional Republicans and the authors then give their response.

For purposes of today’s column, I’ll show their response and then give my response. Sort of a debunking of the debunking, except my main argument is that they are being evasive rather than dishonest.

1st Republican claim: “The agreement threatens U.S. tax sovereignty.”

Here’s how Sarin and Clausing respond.

In the past, some lawmakers have cautioned that we can’t afford to tax mobile corporate income because that income can simply be shifted to countries that offer lower rates. But with a universal 15 percent minimum rate, Congress’s options widen, giving policymakers the freedom to choose rates that align with the nation’s fiscal priorities.

The truth: The authors make it seem like this is a semantic issue – i.e., is a tax cartel a surrender of sovereignty or an expression of sovereignty. But that’s not important. What matters is whether it is good policy for governments to conspire against taxpayers. The answer unambiguously is no.

2nd Republican claim: “The agreement is an unconstitutional giveaway to foreign governments.”

Here is their response.

Here’s what the deal actually does: Say France implements the minimum tax, but a U.S. multinational with a French subsidiary retains the abileity to move income from France to a low- or no-tax jurisdiction to avoid it. France could then impose a tax topping up the effective rate to 15 percent.

The truth: I have no idea about the legality or constitutionality of the tax cartel, but the authors once again dodge the real issue, which is whether it is a good idea to to divert more money from the productive sector of the economy so that politicians (regardless of their location) can spend more.

3rd Republican claim: “The agreement harms the competitiveness of U.S. businesses.”

Their response:

By raising the “bottom” from zero to 15 percent, and in a way that affects companies regardless of the location of their headquarters, the agreement is a giant step toward a more level playing field, so U.S. businesses don’t end up at a competitive disadvantage.

The truth: Politicians (and the authors!) openly brag about how a global tax cartel will enable governments to grab ever-larger shares of business income. Of course this will harm American companies.

4th Republican claim: “The agreement hurts workers by harming the companies they work for.”

Their response:

A global minimum tax will help the U.S. government create a more balanced system that taxes the most profitable companies in the world at rates that are closer to what middle-class families pay. This means workers will shoulder less of the tax burden themselves.

The truth: As every public finance economist knows, only people pay taxes. Any tax on a business is really a tax on workers, consumers and shareholders. To make matters worse, the higher business tax burdens will reduce investment, which will lower productivity, and thus translate into lower wages for workers.

5th Republican claim: “The agreement harms U.S. government revenue.”

Their response:

Republican lawmakers have argued that the federal government will lose revenue once foreign governments are emboldened to tax U.S. companies. But…the global agreement makes the corporate tax base less porous by reducing profit-shifting to low-tax havens. …The whole point of the agreement was to ensure that countries that want to use the corporate tax to generate revenue can do so. Indeed, the Biden administration has proposed hundreds of billions in new corporate tax revenue

The truth: Since I want to reduce revenue for Washington, I have mixed feelings about this final point. I’ll simply note that the OECD’s own data shows that the global shift to lower tax rates has not led to lower revenues. Heck, the OECD has also produced research confirming there’s a strong Laffer Curve for corporate taxes.

The bottom line is that Sarin and Clausing believe in higher taxes and bigger government.

So it is understandable that they support global tax cartels. Unfortunately, they never explain in their column why a bigger burden of government is desirable.

P.S. Joe Biden deserves criticism for supporting the OECD’s proposed tax cartel, but let’s not forget that Donald Trump also was very bad on the issue.

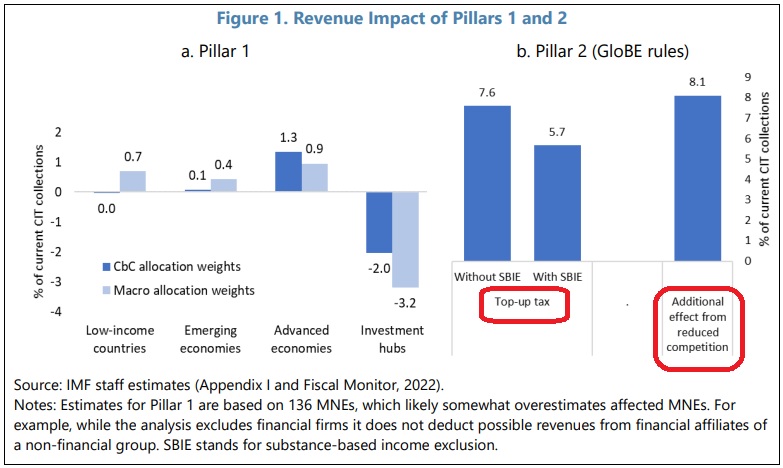

P1 is estimated to reallocate about 2 percent of total profits of MNEs, mainly from low-tax investment hubs to other countries, raising global Corporate Income Tax (CIT) revenue by $12 billion. …P2 would raise global CIT revenues by 5.7 percent, which is before any behavioral responses by firms (Figure 1b). According to staff simulations, 18.5 percent of global profit of MNEs is taxed below 15 percent ($1.47 trillion in 2019). On average, the current tax rate on these profits is 5 percent, so that profits exceeding the substance-based income exclusion would be subjected to a average top-up tax of 10 percent. …An additional positive revenue impact from P2 could come from reduced competition over corporate tax rates, which could boost global CIT revenues by an extra 8.1 percent. …a 1 percentage point increase in the world average CIT rate will, on average, induce a country to raise its own rate by 0.6 percentage points. By putting a floor of 15 percent, the simulations above suggest that 18.5 percent of MNE profit will indeed face a higher CIT burden, implying that countries will feel less pressure to keep their own tax rates low. Using simulations of the tax competition model, we find that the average CIT rate would rise from 22.2 to 24.3 percent due to the global minimum tax. The associated boost in global CIT revenues would be 8.1 percent, exceeding the direct effect on revenue.

By the way P1 is Pillar 1, which is the proposal to give powerful nations a bigger claim on the taxable income of big companies. By contrast, P2 is Pillar 2, which is the proposal for a mandatory minimum tax of at least 15 percent on corporate income.

Second, we should all be outraged that IMF bureaucrats (including the authors of the paper cited above) receive tax-free salaries while pushing for higher taxes on the rest of us.

Why? Because politicians are far more likely to keep tax rates low when they are afraid that jobs and investment can move to countries (or states) with better tax system.

It also explains why tax rates fell dramatically around the world after Ronald Reagan and Margaret Thatcher triggered a virtuous cycle of jurisdictional competition.

And it explains why politicians are fighting to curtail tax competition. They want taxpayers to be akin to captive customers. When that happens, they can push tax rates back up.

Given my cheerleading for tax competition, you won’t be surprised to learn that I get a jolt of pleasure anytime I read about a government being pressured to lower tax rates.

Which is why I’m going to share some excerpts from a story in the New York Times.

Dubai started the new year by suspending its 30 percent tax on alcohol, a move that could help the Gulf emirate attract more tourists and businesses amid growing regional competition. Dubai removed the tax on Sunday, along with the fee for a license that individuals need to buy alcohol, local beverage distributors said. …Offering significantly cheaper liquor is likely to bolster Dubai’s position as the Middle East’s center for tourism and business at a time when economists are warning of a global economic slowdown that could dent spending on travel and leisure. …The changes are likely to give a boost to the local hospitality industry… The decision was the latest in a series of measures that appear to be designed to cement Dubai’s position as the dominant hub for tourism and investment in the Middle East. …Dubai is facing increasing competition from Qatar and Saudi Arabia.

I’ve been to Dubai a few times, but never Qatar or Saudi Arabia, so I can’t personally comment on the relative attractiveness of the three jurisdictions.

But I’m glad that they feel pressure to compete with each other. The net result is more liberty.

P.S. I can’t resist pointing out that our leftist friends should not be overly upset about tax competition. After all, even data from the OECD shows that governments are collecting more money now that tax rates have significantly dropped. Though that data may not be very convincing if folks on the left are motivated by something other than greed for more tax revenue.

I’ve written manytimes about the importance of low tax rates, specifically low marginal tax rates on productive activity such as work, saving, investment, and entrepreneurship.

And I’ve explained that it is especially beneficial to have low tax burdens to attract people who play a big role in boosting economic growth.

The bottom line is that everyone should want their state or their country to be a magnet for the best and brightest.

Having more highly successful people is a great shortcut for boosting everyone’s income.

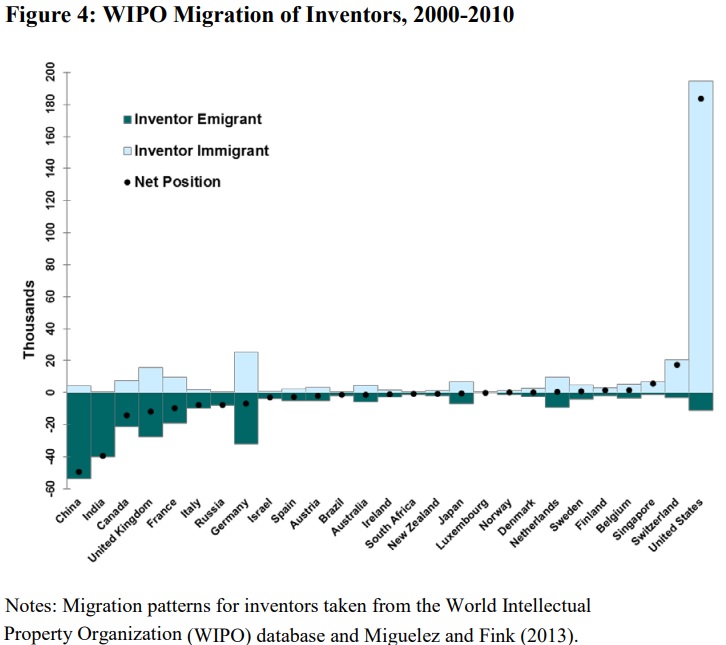

Today, we’re going to look at more evidence on this topic. In a working paper for the Harvard Business School, Sari Pekkala Kerr, Çağlar Özden, William Kerr, and Christopher Parsons examine the migratory patterns of highly skilled workers.

Highly skilled workers play a central and starring role in today’s knowledge economy. Talented individuals make exceptional direct contributions—including breakthrough innovations and scientific discoveries… The exceptional rise in the number of high-skilled migrants to OECD countries is the result of several forces, including increased efforts to attract them by policymakers as they recognize the central role of human capital in economic growth… For example, immigrants account for some 57 percent of scientists residing in Switzerland, 45 percent in Australia, and 38 percent in the United States (Franzoni et al. 2012). In the United States, 27 percent of all physicians and surgeons and over 35 percent of current medical residents were foreign born in 2010. …the global migration rate of inventors in 2000 stood at 8.6 percent, at least 50 percent greater in share terms than the average for high-skilled workers as a whole.

In the contest to attract skilled migrants, some nations do a better jobs than others.

…among OECD destinations, the distribution of talent remains skewed. Four Anglo-Saxon countries—the United States, the United Kingdom, Canada and Australia—constitute the destination for nearly 70 percent of high-skilled migrants (to the OECD) in 2010. The United States alone has historically hosted close to half of all high-skilled migrants to the OECD and one-third of high-skilled migrants worldwide.

Here’s a chart looking specifically at inventors.

So why do some nations get disproportionate numbers of skilled migrants.

As you might suspect, these highly productive people want to earn more money. And keep more money.

The core theoretical framework for studying human capital flows dates back to at least John Hicks (1932), who noted that “differences in net economic advantages, chiefly differences in wages, are the main causes of migration.” …the United States has a very wide earnings distribution and low tax levels and progressivity, especially compared to most source countries, including many high-income European countries. As a result, we can see why the United States would attract more high-skilled migrants, relative to low-skilled migrants and relative to other high-income countries.

Notice, by the way, that low-tax Singapore and low-tax Switzerland also are big winners in the above chart. Indeed, they may be ahead of the United States after adjusting for population.

Federalism is very desirable because it allows different parts of the country to make different decisions, and this helps to teach us about what works. And what doesn’t.

It also means Americans can “vote with their feet” by migrating across local borders and state borders.

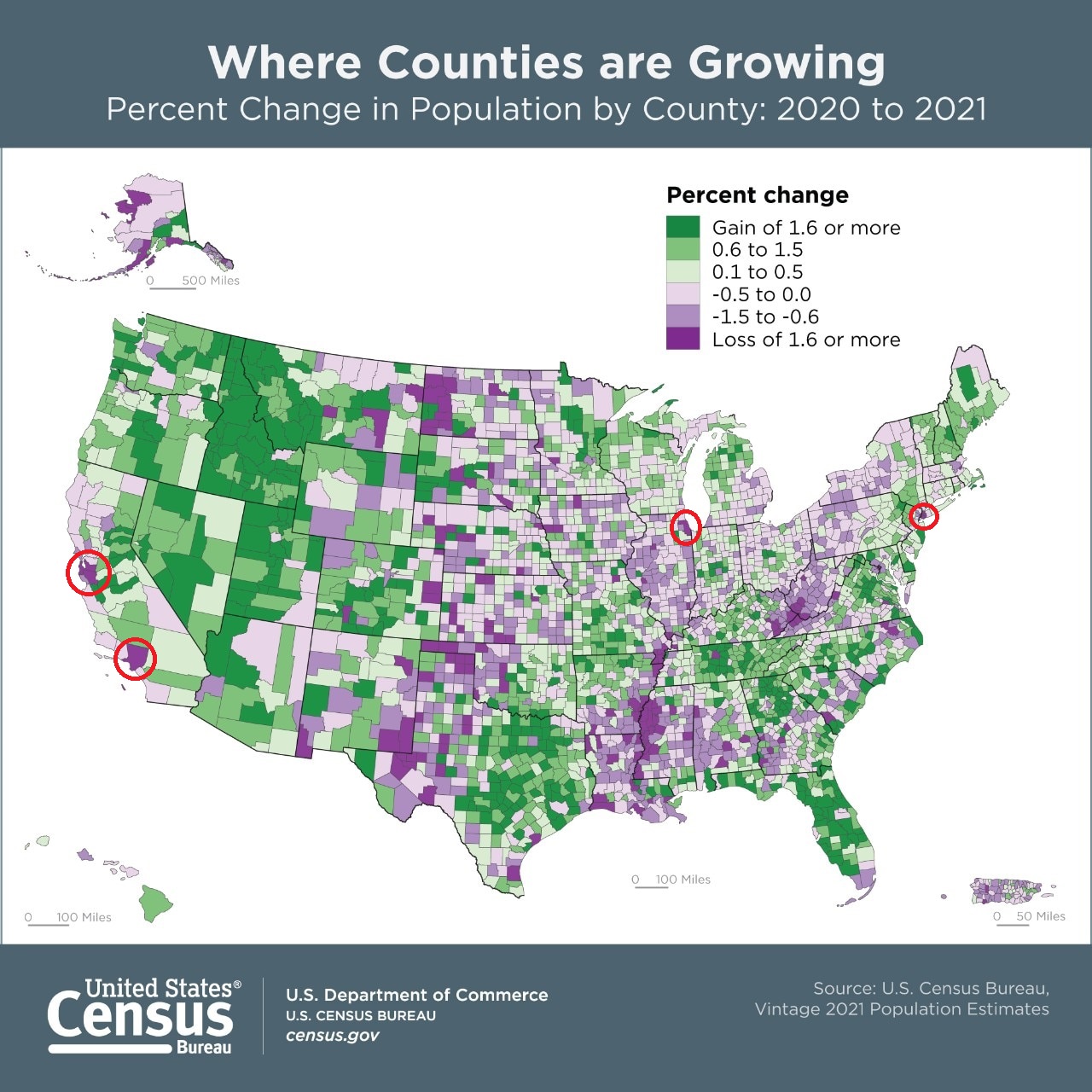

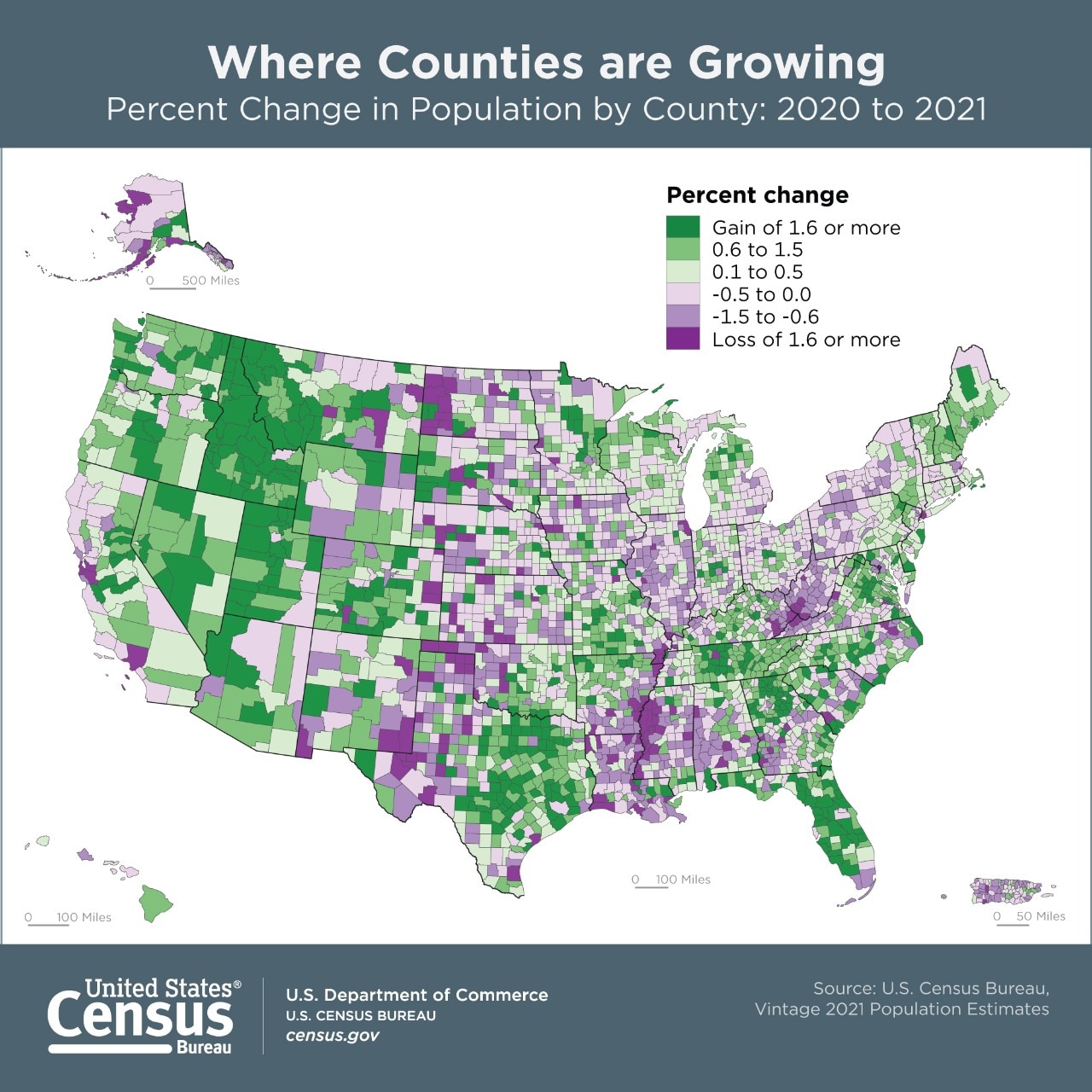

This happens a lot, as illustrated by this map from the Census Bureau.

While this map is fascinating, it also can be deceiving because some counties have very few people and others have millions of people.

It appears that internal migration might be a wash for states such as California and New York, for instance, since parts of both states are both green and purple.

Why? Because big losses in some heavily populated cities (circled in red above) easily outweighed population gains in rural counties.

So why are people leaving some places? Are there lessons to be learned?

One obvious takeaway is that Americans are fleeing states governed by the left, as Kerry McDonald explains for the Foundation for Economic Education.

US Census Bureau data released in December showed that restrictive states such as California, Illinois, New York, and Massachusetts lost population between July 2020 and July 2021, while states with less-restrictive virus policies like Texas, Arizona, and Florida gained population during that time. …Fight or flight is a tough choice for families, but at least it’s a choice that Americans can enjoy thanks to federalism and the ability to vote with our feet.

And Americans are fleeing localities governed by the left, as Michael Barone explains in the Washington Examiner.

…the biggest losses, in both population and percentage loss, came in four of the nation’s six largest metropolitan areas: San Francisco/San Jose (-2.6 percent), New York (-1.8 percent), Chicago (-1.1 percent) and Los Angeles/Riverside (-0.8 percent). Each of the first three, in just 15 months from April 2020 to July 2021, lost a population that equaled 20 percent of their total population gain in the 20 years between 2000 and 2020. …it’s also noteworthy, and probably more permanent, that people with modest educations and incomes have fled far beyond the exurbs. …the nation’s population growth and its economic dynamism had been concentrated disproportionately in the exurbs, which typically have reasonable tax rates and development-friendly regulations. …the self-harm that liberal and progressive politicians have inflicted…voters even in New York, Chicago, Los Angeles, and San Francisco are recoiling.

The moral of the story is that voters sometimes make the mistake of voting for tax-and-spend politicians, but at least they have enough sense to then escape the places being harmed by statist policies.

But there are other examples of decentralized systems, with Canada also deserving plenty of praise.

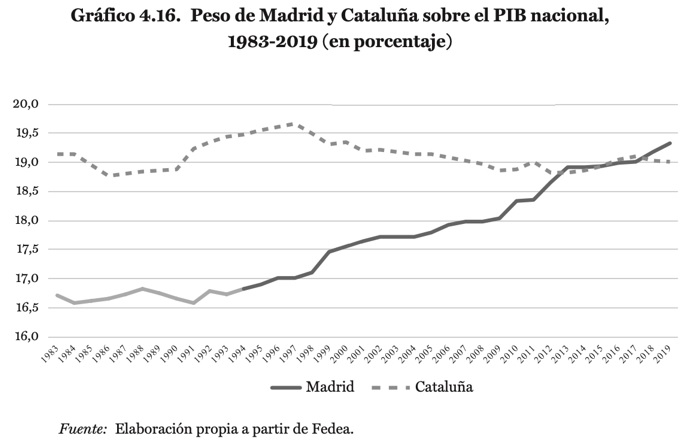

Today, though, I want to write about Spain.

I had an opportunity to learn about the Spanish system while giving speeches last week in Castellon, Barcelona, and Madrid as part of the Free Market Road Show.

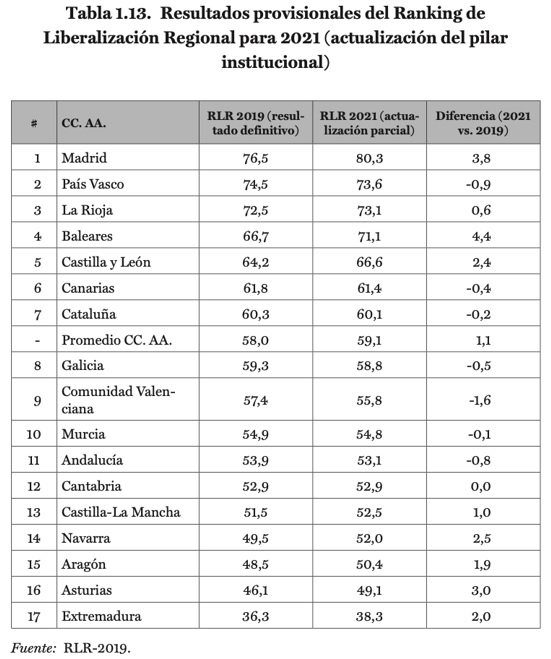

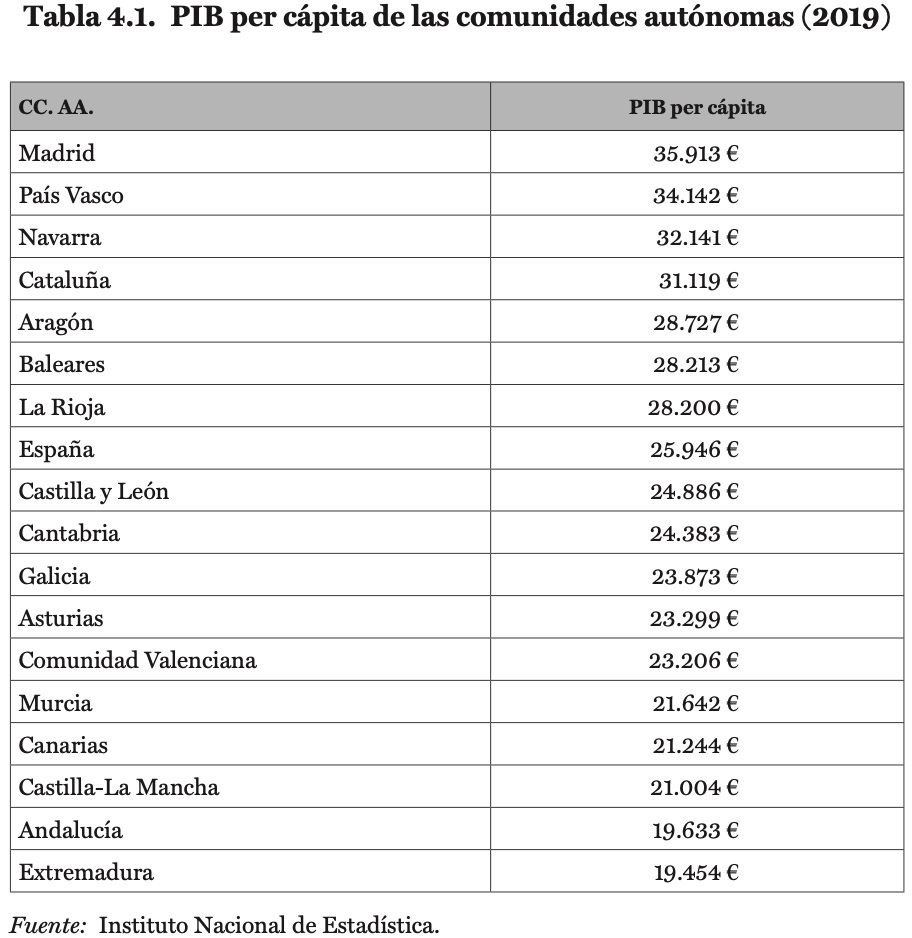

Let’s look at some data from Liberalismo a la madrileña, written by Diego Sánchez de la Cruz, the head of Foro Regulación Inteligente.

His book documents how pro-market reforms in the Madrid region have resulted in greater prosperity.

We’ll start with a look at the level of economic freedom in different Spanish regions. Madrid is at the top and Extremadura (bordering Portugal) is at the bottom.

Does a higher level of economic freedom produce better results, as measured by per-capita economic output?

The answer is yes. Madrid ranks first and Extremadura ranks last.

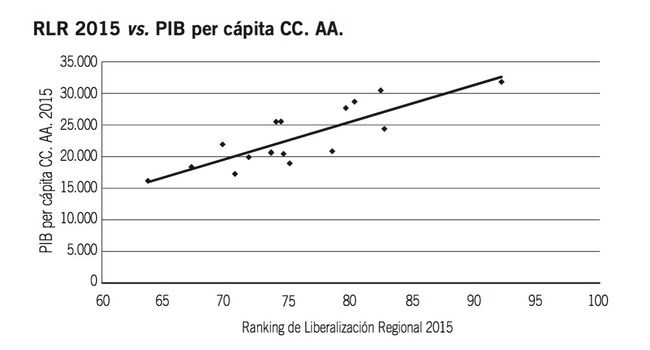

And one of Diego’s earlier publications graphed the relationship between economic freedom and per-capita output.

Definitely a strong correlation.

But what about causation? For instance, some of my left-leaning friends may wonder if there’s some other reason for the superior performance of the Madrid region. Maybe it was always the richest part of Spain and its current prosperity has nothing to do with current policy.

People always should be skeptical about data, particularly when looking at one-year snapshots.

That’s why I’m a big fan of looking at long-run trends. And this chart showing how Madrid has overtaken Catalonia helps confirm that good policy produces good results.

To elaborate, Madrid enjoyed rapid convergence over the past two decades, a period where there was lots of economic liberalization (including de jure elimination of a wealth tax and de facto abolition of a death tax).

By the way, based on current trends, Madrid and Catalonia now may become members of the anti-convergence club.

P.S. There has been some discussion of decentralizing in Australia and the United Kingdom, but no actual progress so far.

Why? Because if they’re not constrained by the fear that taxpayers can escape, I worry that short-sighted politicians (i.e., “stationary bandits“), will over-tax and over-spend.

And that can lead to Greek-like fiscal and economic chaos, which I’ve referred to as “goldfish government.”

Now let’s consider a wonky aspect of this debate. In order for tax competition to be an effective constraint on the greed of politicians, taxpayers need an ability to actually benefit from better tax policy in other jurisdictions.

These jurisdictions had very strong human-rights laws with regard to financial privacy and – equally important – they did not view it as their responsibility or obligation to help enforce the bad tax policies of high-tax governments.

All of which explains why those high-tax governments were so determined to destroy financial privacy as part of their broader fight to replace tax competition with tax harmonization.

In part, this was a fight over fiscal policy. High-tax governments wanted the ability to track money around the world so they could impose extra layers of tax on income that is saved and invested.

But this was also a fight about legal principles, especially the concept of “dual criminality” – which is the idea that governments only help each other enforce laws where there is mutual agreement about what’s legal and illegal.

The tax havens not only had strong human rights laws regarding privacy, but they also had various types of tax laws (no income taxes, territorial tax systems, no tax bias against saving and investment) that were incompatible with the onerous tax policies in most nations.

The net result was that high-tax governments couldn’t track and tax the money. And this made me happy because politicians from those nations instead faced pressure to lower tax rates.

But I’m not happy any more. Sadly, the big nations of the world have largely prevailed in their anti-tax competition campaign. At least with regards to financial privacy.

Even the Swiss agreed to weaken their human rights policies so high-tax nations could impose extraterritorial tax enforcement, notwithstanding the absence of dual criminality (in this case, Goliath beat David).

This was bad news. No longer constrained by the principle of dual criminality, politicians now feel more empowered to boost tax rates.

As you might imagine, my leftist friends usually dismiss my concerns. But I’m guessing they will change their tune about extraterritoriality after reading this column in the New York Times.

The authors (David S. Cohen, Greer Donley and Rachel Rebouché) are very worried that some states want to impose their abortion laws outside their borders. Here are some excerpts.

Some states will go beyond banning abortion within their borders. They will try to impose their policy preferences on other states, in an attempt to stop their citizens from getting abortions anywhere at all. …it will be up to abortion-supportive states to determine the future of abortion law and access. …All states have statutes that require their civil and criminal courts to assist in another state’s depositions, subpoenas and legal processes. Abortion-supportive states could amend these laws; such states could prohibit their courts from cooperating with out-of-state civil and criminal cases that stem from abortions that took place legally within their borders. To further protect abortion providers, states could block their law enforcement agencies from cooperating with out-of-state investigations related to the provision of otherwise lawful abortions. And they could change their extradition laws to refuse to extradite abortion providers… States where abortion remains legal can instruct their medical boards and in-state malpractice insurance companies to abstain from taking any adverse action against providers who give out-of-state patients abortions that are legal in the provider’s state.

In a world where people are intellectually honest, they will have consistent views on dual criminality, regardless of the underlying laws.

I strongly suspect, however, that most of my left-leaning friends will now embrace the principle of dual criminality as a constraint on extraterritoriality while still thinking it is good that low-tax jurisdictions have been coerced into acting as vassal tax collectors for high-tax governments.

Heck, some of my right-wing friends also will be hypocrites. They will support fiscal sovereignty but embrace extraterritoriality for abortion laws.

The bottom line – regardless of how we feel about tax policy or abortion policy – is that the power of governments should be constrained by borders.

If you don’t like the tax laws of Jurisdiction A or the abortion laws of Jurisdiction B, work to change those laws by devoting your time, energy, and money to an issue campaign. That’s the right approach, especially when compared to trying to achieve the same goals by using the laws of Jurisdiction C or Jurisdiction D.

P.S. The battle over the taxation of online sales was really a fight over whether businesses in some states could be forced into enforcing the tax laws of other states.

P.P.S. As a result of my efforts to protect tax havens, I’ve been subjected to slurs, attacks, and even potential imprisonment.

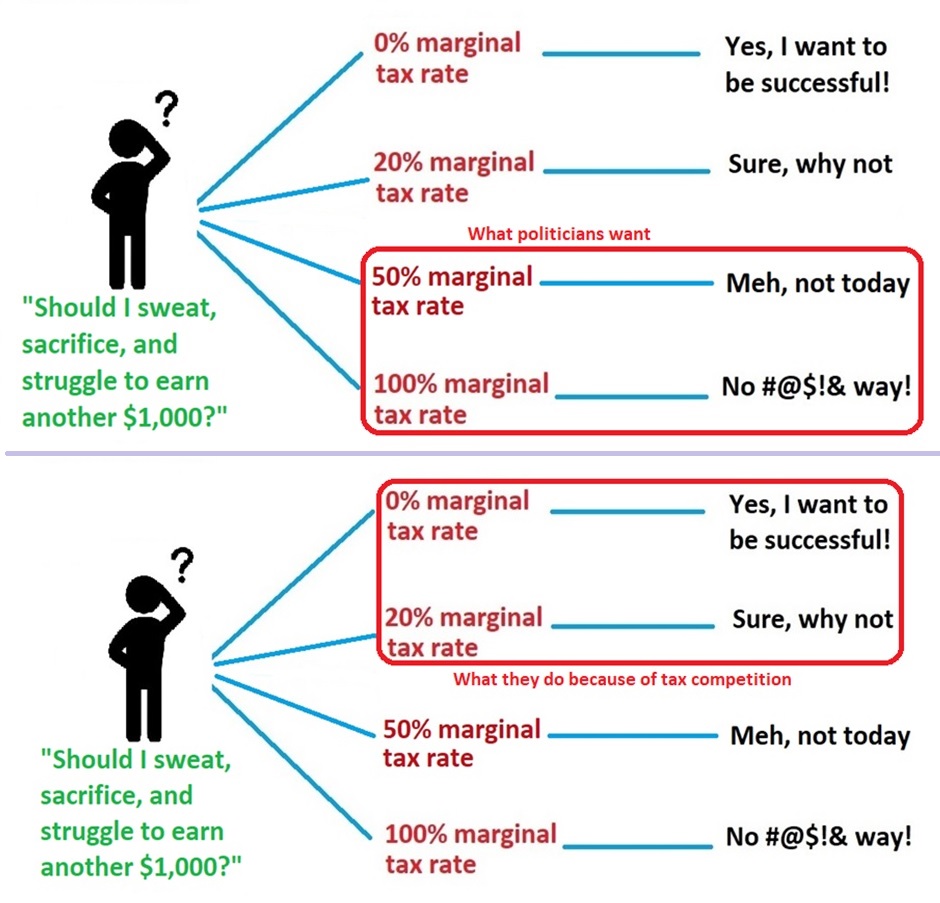

From the perspective of politicians, it’s easy to understand why they want a tax cartel. it’s a way for them to get their hands on more money. Just as gas stations would want a system that rigs gas prices at a high level. Or grocery stores would want a system to rig high food prices.

From the perspective of taxpayers, however, tax competition is much better. Politicians have a much harder time raising tax rates (and in many cases feel pressure to lower tax rates) when they know that jobs and investment can shift across borders from high-tax nations to low-tax nations.

As illustrated by this visual.

To explore this issue in greater detail, let’s look at a new article, written by Sven Larson for the European Conservative.

First, a quick history of the global campaign against low taxes. …it has been spearheaded by the Organization for Economic Cooperation and Development, OECD. This government-funded international think tank has built an international cartel of more than 130 governments to battle tax competition. …People who want to keep more of their own money, and who want to enjoy strong privacy laws, are being told by the OECD and the tax cartel that their financial planning is “harmful.” The purpose behind the OECD-led campaign is both sinister and transparent: to make sure taxpayers in high-tax countries have no low-tax options. …It won a big victory this past summer when the countries in the G-7 group complied with the directives of the OECD and agreed to create a global minimum corporate-income tax.

Sven also makes a great point about how the corporate tax cartel is just the beginning.

This tax cartel is only the beginning. Once countries with costly governments have created a Berlin Wall around their high-tax jurisdictions, they will be free to collude on other taxes beyond the corporate income tax. Personal income taxes, wealth taxes, death taxes… there is no end to the imagination of a government that does not have to worry about tax competition.

You should read the entire article. But for purposes of my column, I’m going to highlight one additional point – which is Sven’s observation about how human rights are better protected in a world where people can safely invest their money where national governments can’t grab it.

There are also reasons related to individual freedom to preserve low-tax jurisdictions. To take just one example, in 2017, …Turkish President Erdogan accused investors of “treason” if they moved their assets out of the country. Erdogan’s comments, France24 explains, came on the heels of Turkish prosecutors seizing the assets of an investor who had testified in a court in New York on how a Turkish bank circumvented U.S. sanctions against Iran. The asset seizure easily comes across as retaliatory and meant to send a signal to others who might act in ways that would displease Mr. Erdogan. A total of 23 individuals were affected by the asset seizure. If these individuals had been able to shield their assets from the Turkish government, they would have been free to oppose the Erdogan regime while working, investing, and developing their businesses.

Especially when you consider that politicians have a very strong tendency to over-tax and over-spend (leading to goldfish government) in the absence of some sort of external constraint.

Remember the supposedly breathtaking revelations from the “Panama Papers” back in 2016?

We were told those stolen documents were an indictment against so-called tax havens, but the real lesson was that politicians and other government insiders are very prone to corruption.

Well, it’s happened again. Thieves stole millions of documents (the “Pandora Papers”) from various firms around the world that specialize in cross-border investment.

Some journalists want us to believe that these documents are scandalous, but I poured cold water on this hysteria in an interview with the BBC.

If you don’t want to listen to me pontificate for about five minutes, here are the main points from the interview.

International investment is a good thing (much like international trade) and it necessarily requires the use of “offshore” entities such as companies, funds, and bank accounts.

Politicians don’t like cross-border investment because economic activity tends to migrate to places with lower tax rate, and this puts downward pressure on tax rates.

There is no evidence that people in the private sector use “offshore” entities in ways that are disproportionately dodgy.

By contrast, there is considerable evidence that politicians use “offshore” in ways that are disproportionately dodgy.

More than 99 percent of people engage in legal tax avoidance and that’s a good thing because it keeps money out of the hands of profligate politicians.

People should not have to share their private financial affairs, such as bank accounts and investment holdings, with the general public.

It’s not worth a separate bullet point, but my favorite part of the interview is when I noted the grotesque hypocrisy of the International Monetary Fund, which pimps for higher taxes all around the world, yet its employees get tax-free salaries.

The bottom line is that tax competition and so-called tax havens should be applauded rather than persecuted.

Since we’re on this topic, let’s also enjoy some excerpts from an article in Reason by Steven Greenhut.

Leftists are thrilled by the Biden administration’s plan to stamp out the bogeyman of tax havens—low-tax jurisdictions where corporations and other investors can keep their money away from the prying hands of the government. …Let’s dispense with the outrage about tax havens. There is nothing wrong with companies and individuals that shelter their earnings from governments, which are like organized mobs that can never seize enough revenue. …If you believe that tax havens are immoral, then you should not claim any deductions on your tax bill. President Joe Biden apparently thinks it’s wrong for corporations to locate their headquarters in low-tax Bermuda, Ireland, and Switzerland, yet why does his home of Delaware house so many U.S. corporate headquarters? …Tax havens provide pressure on big-spending governments to limit tax rates, and lower tax rates boost economic activity, create jobs, and incentivize investors to invest more. …Those who oppose tax havens simply want the government to take more money and have more power.

Here’s the segment where I explain why it would be bad for developing nations.

At the risk of stating the obvious, Joe Biden is pushing this policy because he wants more tax revenue to fund his misguided plan for a bigger welfare state in the United States.

And the same is true for politicians in other big nations such as France, Japan, and Germany.

So as negotiations continue and rules are decided, rest assured that those countries will look after themselves and politicians from developing nations will be lucky to get a few crumbs from the table.

This discussion gives me a good excuse to put together this list of the potential winners and losers from a global tax cartel.

Since I slapped this together in five minutes, I won’t pretend it’s comprehensive.

But it’s hopefully more complete than a simple statement that politicians are the winners and people in the private sector are the losers.

Speaking of losers, my list includes “Nations with sensible tax policy,” and that’s a good reason to share this story from the New York Times. It’s about Janet Yellen’s efforts to convince Irish politicians to sacrifice their nation’s economic advantage.

The United States is hopeful that Ireland will drop its resistance to joining the global tax agreement… The agreement, which gained the support of the Group of 20 nations on Saturday, would usher in a global minimum tax of at least 15 percent. It would also change how taxing rights were allocated, allowing countries to collect levies from large, profitable multinational firms based on where their goods and services were sold. …Ms. Yellen held high-stakes meetings in Brussels this week with Paschal Donohoe, Ireland’s finance minister… She needs Mr. Donohoe’s support because the European Union requires unanimity among its members to formally join the deal.

So you may be wondering what Ms. Yellen said? Did she have some clever and insightful argument of how Ireland would benefit (or at least not be hurt) if politicians create a global tax cartel?

Nope. The best she could come up with is that Ireland’s tax system wouldn’t be as bad as the one she wants for the United States.

Ms. Yellen told her Irish counterpart that Ireland’s economic model would not be upended if it increased its tax rate from 12.5 percent…it would still have a large gap between its rate and the 21 percent tax rate on foreign earnings that the Biden administration has proposed.

The bottom line is that Ireland has reaped enormous benefits from its decision to enact a low corporate tax rate. But if a global tax cartel is imposed, it would simply be a matter of time before that country gets relegated to being an economic backwater on the periphery of Europe.

P.S. Part of the discussion in the video was about developing nations having the right to copy the economic model (no income tax and no welfare state) that enabled North American and Western Europe to become rich in the 1800s. Sadly, I don’t think many politicians in the developing world are interested in that approach nowadays, but rich nations shouldn’t make it impossible.

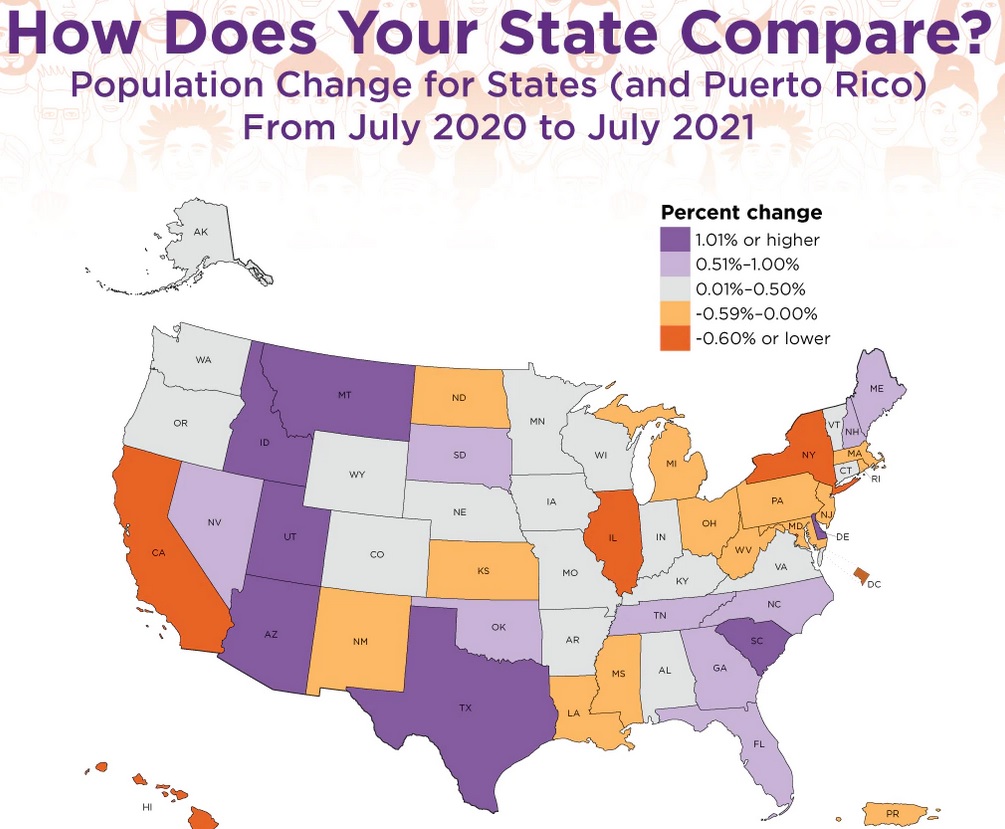

If you ask normal people about the biggest thing that happened in 2020, they’ll probably pick coronavirus, though some might say the 2020 election.

But if you ask a policy wonk, you may get a different answer. Especially if we’re allowed to tweak the question a bit and contemplate the most under-appreciated development of 2020.

In which case, my answer would be interstate tax migration.

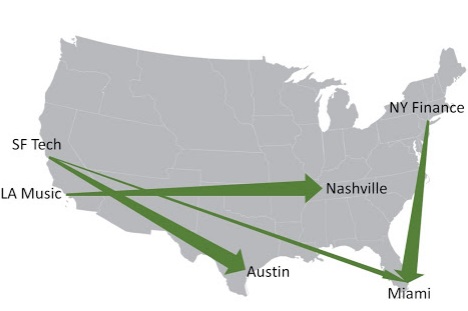

I’ve been writing about this topic for years, but it seems that there’s been an acceleration. And, as illustrated by this map, people are moving from high-tax states to low-tax states.

The map comes from an article by Scott Sumner of the Mercatus Center, and here’s some of his analysis.

The movement of these industries is toward three states that have one thing in common—no state income tax. …Progressives often discount the supply side effects of tax changes, pointing to examples such as Kansas where tax cuts had little effect. But Kansas…tax cuts were relatively modest. If you are looking for a low tax state on the Great Plains, South Dakota has no state income tax at all. The top rate in Kansas (5.7%) is higher than in Massachusetts (5.0%). That won’t get the job done. …I’m certainly not a rabid supply sider who thinks that tax rates are all important. But a person would have to be pretty blind to ignore the migration of firms from places like New York, New Jersey and California, to lower tax places. …Washington State has no income tax, which is unique for a northern state with a big city. Washington is also home to the two of the three richest people on the planet (the other–Elon Musk–just announced he’s moving from California to Texas.) …Washington is also experiencing rapid population growth, which is also unique for a northern state with a big city. …last year more that half of the US population growth occurred in just two states—Texas and Florida. …Add in Tennessee and Washington and you are at nearly two thirds of the nation’s population growth.

Wow, four states (all with no income tax) accounted for the bulk of America’s population growth. That’s a non-trivial factoid.

And I also think his observations about Kansas are spot on. Yes, the state improved it’s tax system, but it should have been bolder, like North Carolina.

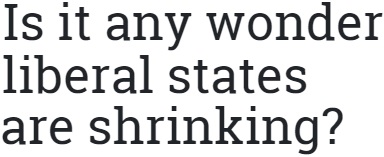

The Washington Examiner recently opined on internal migration and also noted that people are escaping high-tax states.

…the state of Illinois has been a laggard in population growth. It has lost eight congressional districts since the 1950s. But new census estimates show that this decade, something very special has happened. …the land of Lincoln has lost a net 308,000 residents over the last seven years… And Illinois’s rapid shrinkage is occurring even as the United States grew by nearly 7% since the last census. …Illinois is not alone. The same census data point to two other big states that are also driving away residents with similarly impractical, ideologically leftist policies — California and New York. …New York, as a consequence, has also lost about 42,000 residents in the last decade. Its population peaked in 2015, and in the time since, it has lost about 320,000. A similar phenomenon is occurring in California, …with about 70,000 net residents vanishing in 2020. …residents are actually giving up and abandoning its beautiful, scenic inhabited areas. …the same census numbers show that people are gravitating toward states that have low or no income tax.

And a recent editorial in the Wall Street Journal echoed these findings.

California’s population shrank for the first time as far back as records go (-69,532). According to a separate state government survey, a net 261,000 residents moved to other states during the period…many large businesses are shifting workforces to other states. …Last year Charles Schwab announced it is relocating its corporate headquarters to the Dallas region from San Francisco. Apple is building a new campus in Austin. Facebook this fall bought REI’s headquarters outside of Seattle. Oracle and Hewlett Packard Enterprise recently announced relocations to Texas. …Over the last decade, Illinois has lost 243,102 in population, about the size of Peoria and Naperville combined. …Democratic states in the Northeast last year lost population, led by New York (-126,355), Connecticut (-9,016) and New Jersey (-8,887). …By raising taxes again and again to pay for generous collective-bargained benefits, public unions are making Democratic states less competitive.

The final sentence is the above excerpt is especially insightful.

Among the states facing fiscal challenges, a common theme is that politicians and bureaucrats have a very cozy and corrupt relationship resulting in absurdly lavish (and unaffordable) compensation levels.

Let’s close with a bit of humor from the great cartoonist, Eric Allie. With all the interstate migration that happened last year, no wonder Santa Claus had some problems.

I’m not a fan of the European Union, which has morphed from something good (a free-trade pact) to something bad (a pro-centralization,wannabe United States of Europe that exacerbates the continent’s tax-and-spend mentality).

Indeed, that’s why I’m a huge fan of Brexit. The United Kingdom is wise to escape the sinking ship.

Why? Because many of the nations that joined that common currency did a lousy job when they had national currencies. Italy and Greece, for instance, routinely used their central banks as printing presses to help finance bloated budgets.

And that inflation exacerbated all the other economic problems that existed.

The bottom line is that many nations would benefit if they took monetary policy away from their politicians and instead adopted the currency of a nation with a better track record.

That happened in Europe when the euro was adopted since it means – for all intents and purposes – that Mediterranean nations use a currency that is controlled by Germany.

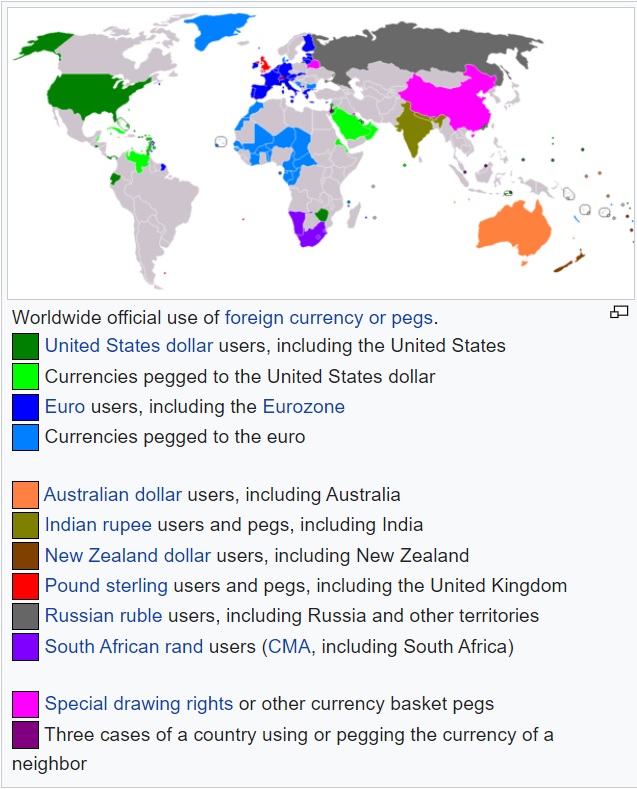

This lesson should be applied elsewhere in the world, which is why “dollarization” can be a good idea.

Professor Steve Hanke of Johns Hopkins University wrote a good description of this concept for National Review.

Before the rise in central banking (monetary nationalism), the world was dominated by unified currency areas, or blocs, the largest of which was the sterling bloc. As early as 1937, the great Austrian economist and Nobel winner Friedrich von Hayek warned that the central banking fad, if it continued, would lead to currency chaos and the spread of banking crises. …Indeed, for most emerging‐market countries with central banks, hot money flows are frequent and so are exchange‐rate and domestic banking crises. What to do? The obvious answer is for vulnerable emerging‐market countries to do away with their central banks and domestic currencies, replacing them with a sound foreign currency. Today, 32 countries are “dollarized” and rely on a foreign currency as legal tender. …Panama, which was dollarized in 1903, illustrates the important features of a dollarized economy. …The results of Panama’s dollarized money system and internationally integrated banking system have been excellent when compared with other emerging-market countries… Emerging-market countries should follow Panama’s lead and “dollarize.” Most central banks in emerging countries produce junk currencies, banking crises, instability, and economic misery. These central banks should have been mothballed and put in museums long ago.

And there are many nations that would benefit if they used the U.S. dollar.

Back in 2018, Mary Anastasia O’Grady opined in the Wall Street Journal that Argentina should dollarize.

Another currency crisis is roiling Argentina… The question that seems to be on everyone’s lips: Why is this happening again… The answer: Because Argentina still has a central bank. To fix the problem once and for all, it should dollarize. …an IMF package can’t cure what ails the peso. This is a long-term political problem that has manifested itself in repeated economic crises since the mid-20th century. The government lives beyond its means while taxes and regulations, particularly on labor, make many businesses uncompetitive. The net effect is always the same: ballooning debt and a lethargic economy followed by devaluation or default or both. …The fastest way to restore confidence would be to put an end to the misery caused by the peso and to adopt the dollar. Argentines could then get on with the business of saving and investing in their beautiful country.

The Wall Street Journal has editorialized in favor of dollarization in Argentina.

Dollarizers face resistance from the Peronist party, which relies on the inflation tax to fund its populism when revenues run low. Yet demand for dollars suggests…popular backing for adopting the greenback as the national currency. …Panama has used the dollar as legal tender since 1904, and El Salvador and Ecuador dollarized in 2000. Ecuador did it to resolve a banking crisis and El Salvador did it to bring down interest rates. El Salvador and Panama now have the lowest domestic borrowing rates in Latin America and the longest maturities. Ecuador has price stability not seen in at least a half century.

Here’s the real shocker. As reported by Reuters, Venezuela is on the verge of dollarizing.

Venezuelan President Nicolás Maduro embraced the currency of his bitter rival the United States on Sunday, calling it an “escape valve” that can help the country weather its economic crisis… The official currency, the bolivar, has depreciated more than 90% this year, while hyperinflation in the first nine months of the year clocked in at 4,680%… “I don’t see it as a bad thing … this process that they call ‘dollarization,’” Maduro said in an interview broadcast on the television channel Televen. “It can help the recovery of the country, the spread of productive forces in the country, and the economy … Thank God it exists,” the socialist leader said.

Writing for National Review, Professor Steve Hanke explains that Maduro has no choice but to move in the right direction.

Maduro, in a rare display of good judgment, is taking a necessary step toward what I have been advocating for many years: official dollarization in Venezuela. …Venezuela’s bolivar is worthless, and its annual inflation rate is the world’s highest…2,156 percent per year. Not surprisingly, Venezuelans get rid of their bolivars like hot potatoes and replace them with U.S. dollars. So, Venezuela is, to a large extent, unofficially dollarized. Official “dollarization” is a proven elixir. I know because I operated as a state counselor in Montenegro when it dumped the worthless Yugoslav dinar in 1999 and replaced it with the Deutsche mark. I also watched the successful dollarization of Ecuador in 2001… Countries that are officially dollarized produce lower, less variable inflation rates and higher, more stable economic growth rates than comparable countries with central banks that issue domestic currencies. There is a tried-and-true way to stabilize the economy…since more than 80 percent of transactions in Venezuela take place in U.S. dollars, it doesn’t seem unreasonable to think that the approval rating would now exceed 80 percent. So, it’s not surprising that Maduro has embraced the dollarization idea. After all, the public already does.

In another column for National Review, Steve Hanke and Craig Richardson cite what’s been happening in Zimbabwe.

They begin by pointing out that part of that nation has avoided problems by using the dollar.

Zimbabwe’s economy has gone through the wringer. In just 20 short years, it has witnessed two episodes of hyperinflation. And, if that wasn’t bad enough, Zimbabwe’s real GDP per capita has plunged by 21 percent over that same period. …But,…when you enter the town of Victoria Falls, it’s as if you have walked into an alternative African economic universe. Victoria Falls is an island of stability in Zimbabwe, a country that has descended into monetary and fiscal chaos. How could this be? …Victoria Falls…has long operated under very different monetary rules. …the glue that holds Victoria Falls together is the U.S. dollar. It’s the coin of the realm in Victoria Falls. Yes, Victoria Falls is officially dollarized. It only accepts U.S. dollars for payment of property taxes and keeps its books in U.S. dollars as well.

But they also note that the entire nation enjoyed the benefits of dollarization, at least until venal politicians opted out because they wanted the power to finance more spending by printing money.

…in February 2009, a unity government was formed. …In one of its first acts, the unity government scrapped the Zimbabwe dollar and officially dollarized the country. In so doing, the printing presses were shut down; the U.S. dollar became legal tender, taxes were required to be paid in dollars, and government accounts were kept in dollars. With the imposition of a hard budget constraint, the fiscal deficit disappeared, and the economy boomed. That rebound persisted during the term of the national unity government, which lasted until July 2013. Indeed, during this period, real GDP per capita surged at an average annual rate of 11.2 percent. Zimbabwe’s period of stability was short lived, however. With the collapse of the unity government and the return of Mugabe’s ZANU-PF party, government spending and fiscal deficits surged, resulting in economic instability. To finance its deficits, the government created a “New Zim dollar,” and Zimbabwe de-dollarized. …The money supply exploded, as did inflation.

This column has focused on dollarization, but there are other currencies that are serve the same role. And there are currency boards/pegs as well.

This map from Wikipedia provides a helpful summary.

Simply stated, red tape makes it more expensive for people and businesses to do things, much as adding obstacles makes it more difficult for someone to get from Point A to Point B.

So a relevant question is whether proposed regulations generate enough benefits to justify the added expense (I’m generally skeptical, but those are empirical matters).

But there’s another question we should ask, which is why governments create new rules and red tape in the first place?

But one thing that never occurred to me is that we may get more regulation if we live in a state or nation with lots of people.

That’s a topic that James Bailey, James Broughel, and Patrick A. McLaughlin investigated in a new study from the Mercatus Center. Here’s a description of their methodology.

…very few academic studies have advanced scholars’ understanding of the relationship between regulation and population. This article is intended to help fill this gap in the literature. We aim to test whether this population-regulation connection holds using more recent, more refined, and more comprehensive measures of regulation. …This study is the first to use RegData to measure why some polities are more regulated than others, the first to use the full State RegData (released in October 2019) for any econometric analysis, and the first to combine federal and state RegData for the United States with RegData datasets for other countries (Australia and Canada).

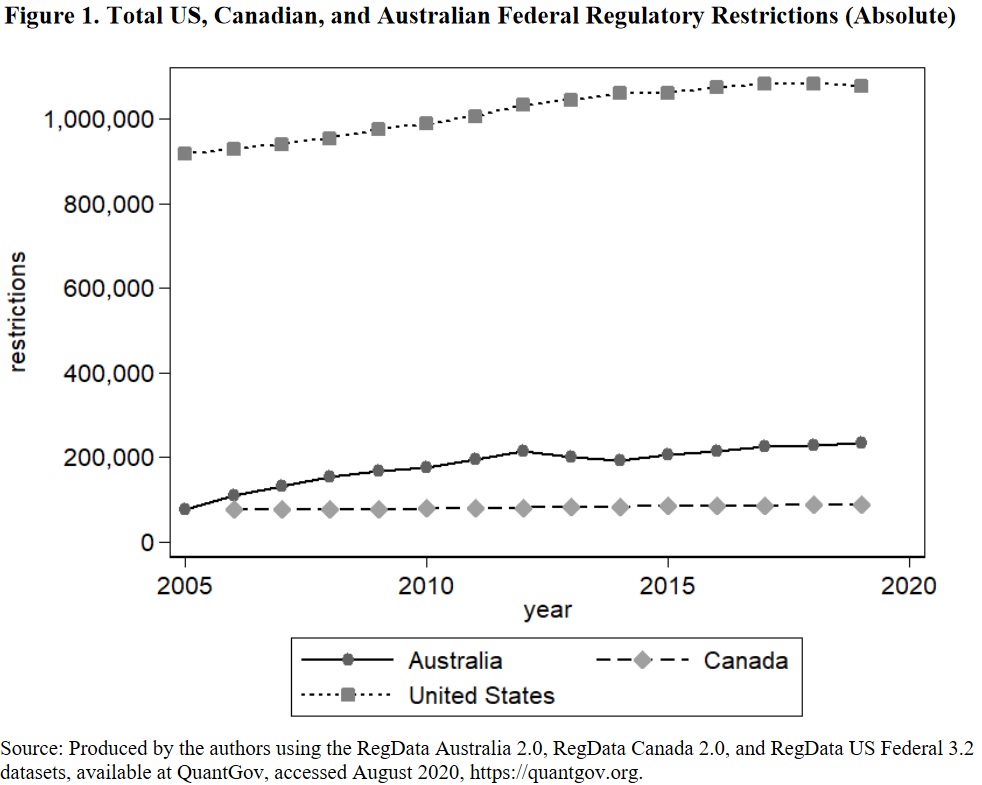

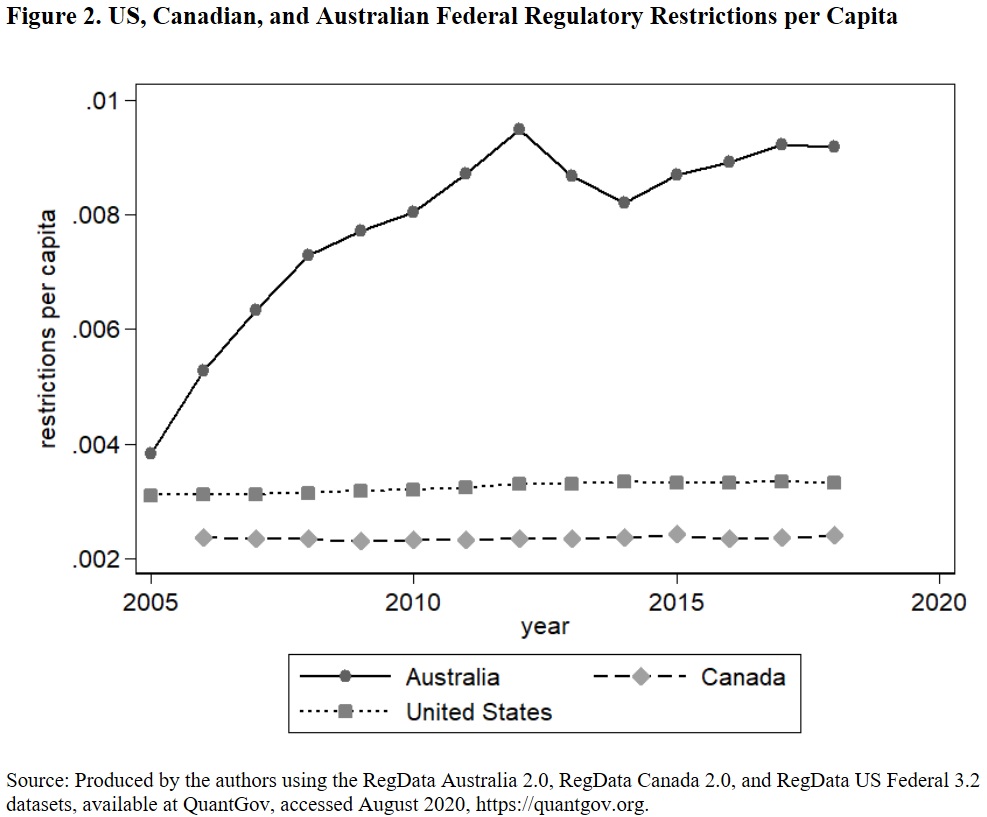

Here is some of the key data from the United States, Canada, and Australia.

The United States has about an order of magnitude more people than Canada, along with about an order of magnitude more regulatory restrictions than Canada. Conversely, Australia is less populous than Canada but has nearly twice as many regulatory restrictions. On a per capita basis, Canada, with only 0.0023 restrictions per capita for the entire time period examined, appears somewhat less regulated than the United States (at about 0.0032 restrictions per capita) and significantly less regulated than Australia (whose restrictions per capita rise from about 0.0053 in 2005 to a peak of 0.0095 in 2012, and taper slightly to 0.0092 in 2018). We note, however, that both the Canadian and the Australian regulatory systems are fairly decentralized compared to that of the United States, delegating a considerable amount of autonomy and authority to provincial governments.

The study includes some interesting charts.

First, we see that there are a lot more regulatory restrictions in the United States than in Canada and Australia.

Though if you adjust for population size, Australia has the most red tape.

Kudos to Canada for having the lowest level of red tape, both in absolute terms and in per-capita terms. As I wrote a few years ago, there are many Canadian policies we should emulate.

One common feature of the U.S., Canada, and Australia is that all three nations have some degree of federalism, which means that some government policies are handled at the state/provincial level.

And this means the Mercatus study has another way of measuring the relationship between population and red tape. In the United States, we learn that more people means more regulations.

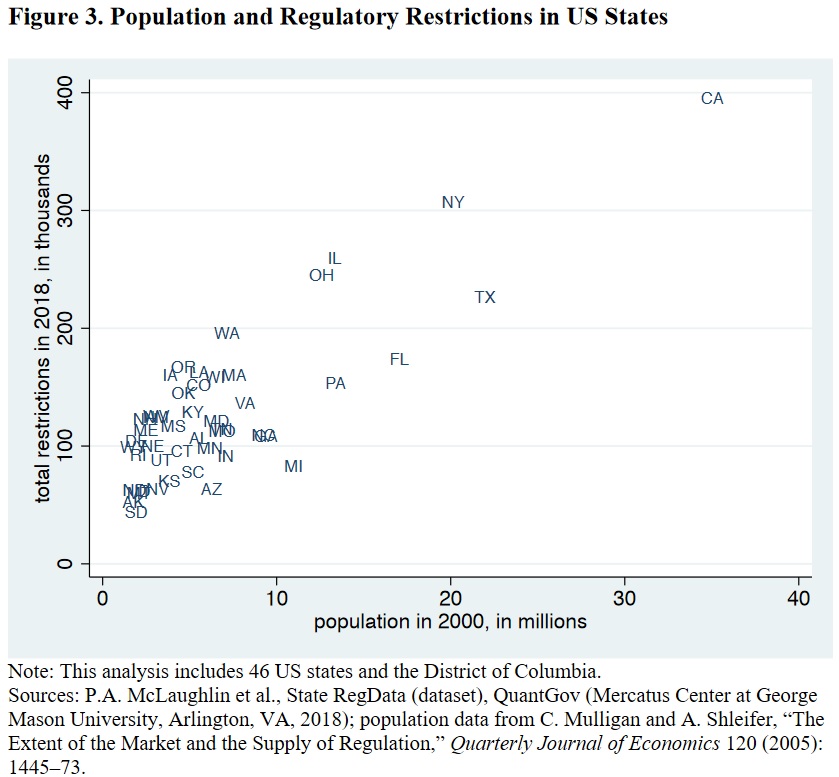

Figure 3 compares the 2000 population and 2018 regulatory restriction counts of 46 US states and the District of Columbia. We see a strong positive correlation between population and regulatory restrictions. Running a basic linear regression with no controls, we find that, on average, an increase in population of 1,000 people is associated with a statistically significant increase of 9 regulatory restrictions. …we next take the log of both population and regulatory restrictions and run a simple linear regression on these variables…which show that, on average, a 10 percent increase in population is associated with a 3.27 percent increase in regulatory restrictions.

Here’s the relevant chart from the study.

Congratulations to South Dakota for having the lowest level of red tape (the state also scores well on fiscal policy).

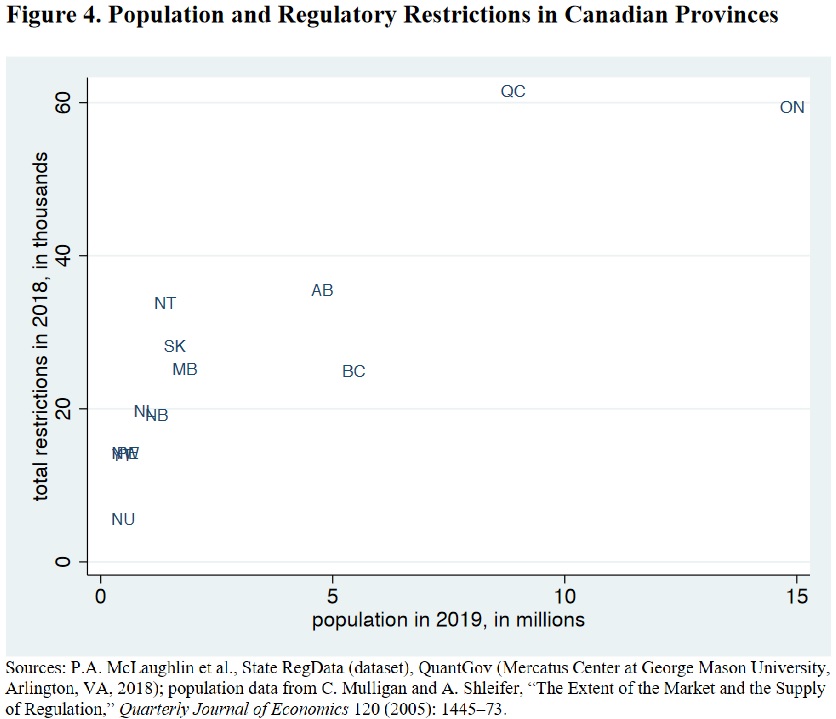

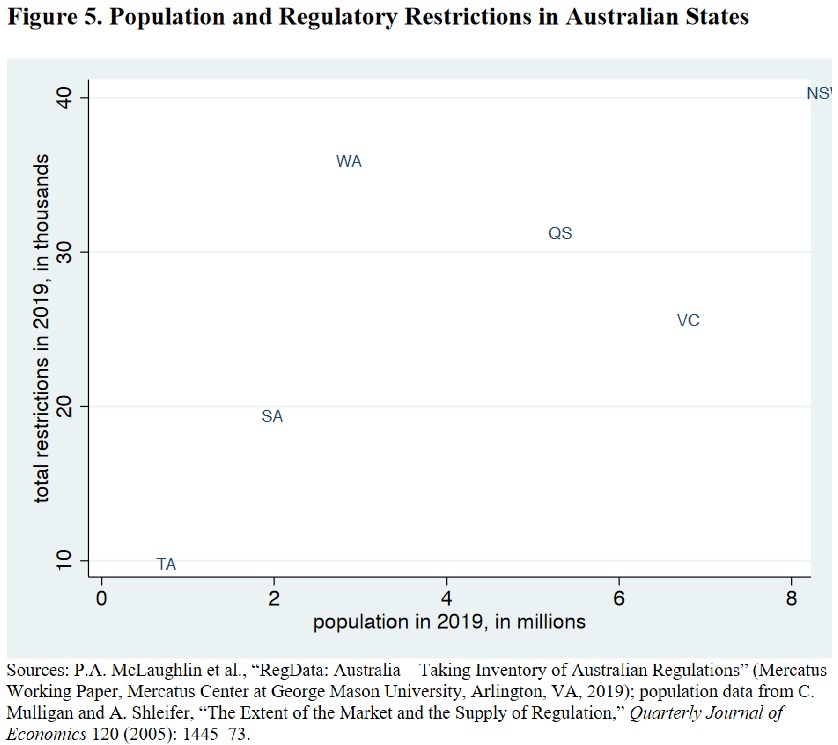

Canada and Australia have fewer subnational governments, but the study finds a similar relationship between population size and regulatory restrictions.

While Canada and Australia do not have enough provinces to support proper regression analysis, Figures 4 and 5 plot their subnational populations against their subnational regulatory restrictions. The results are also suggestive of a positive population-regulation correlation.

Here’s the chart for Canada.

And here’s the chart for Australia.

The relationship between red tape and population isn’t a perfect fit, either in the U.S. or in the other two countries. But there certainly seems to be some level of correlation.

But why?

The authors offer some potential answers.

…we show that larger polities consistently have more regulation. This provides support for previous theoretical work that posited a fixed cost associated with regulating. Specifically, the fixed costs of establishing new bureaus, staffing them, and funding them to implement and enforce regulations may fall on a per capita basis with a larger population. In addition to the fixed cost explanation, Mulligan and Shliefer offer other alternative explanations for why regulation may increase with population levels…the scope of activities to regulate becomes larger as population increases.

But it’s not the worst state, at least according to the Tax Foundation, which calculates that the Empire State is ranked #49 in the latest edition of the State Business Tax Climate Index.

Some politicians from New York must be upset that New Jersey edged them out for last place (and the Garden State does have some wretched tax laws).

So in a perverse form of competition, New York lawmakers are pushing a plan to tax unrealized capital gains, which would be a form of economic suicide for the Empire State and definitely cement its status as the place with the worst tax policy.

The tax, part of a new “Make Billionaires Pay” campaign by progressive lawmakers and activists, would impose a new form of capital gains tax on New Yorkers with $1 billion or more in assets. …“It’s time to stop protecting billionaires, and it’s time to start working for working families,” Rep. Alexandria Ocasio-Cortez, D-N.Y., said… Currently, taxpayers pay capital gains tax on assets only when they sell. The new policy would tax any gain in value for an asset during the calendar year, regardless of whether it’s sold. Capital gains are taxed in New York at the same rate as ordinary income, so the rate would be 8.8%.

Given her track record, I’m not surprised that Ocasio-Cortez has embraced this punitive idea.

That being said, the proposal is so radical that even New York’s governor understands that it would be suicidal.

Gov. Andrew Cuomo said raising taxes on billionaires and other rich New Yorkers will only cause them to move to lower-tax states. …“If they want a tax increase, don’t make New York alone do a tax increase — then they just have the people move… Because if you take people who are highly mobile, and you tax them, well then they’ll just move next door where the tax treatment is simpler.”

Actually, they won’t move next door. After all, politicians from New Jersey and Connecticut also abuse and mistreat taxpayers.

In a column for the New York Post, E.J. McMahon points out that residents already have been fleeing.

…there were clear signs of erosion at the high end of New York’s state tax base even before the pandemic. Between 2010 and 2017, according to the Internal Revenue Service, the number of tax filers with incomes above $1 million rose 75 percent nationwide, but just 49 percent in New York. …Migration data from the IRS point to a broader leakage. From 2011-12 through 2017-18, roughly 205,220 New Yorkers moved to Florida. …their average incomes nearly doubled to $120,023 in 2017-18, from $63,951 at the start of the period. Focusing on wealthy Manhattan, the incomes of Florida-bound New Yorkers rose at the same rate from a higher starting point— to $244,936 for 3,144 out-migrants in 2017-18, from $124,113 for 3,712 out-migrants in 2011-12.

What should worry New York politicians is that higher-income residents are disproportionately represented among the escapees.

And the author also makes the all-important observation that these numbers doubtlessly will grow, not only because of additional bad policies from state lawmakers, but also because the federal tax code no longer includes a big preference for people living in high-tax states.

These figures are from the period ending just before the new federal tax law temporarily virtually eliminated state and local tax deductions for high earners, raising New York’s effective tax rates higher than ever. …soak-the-rich tax sloganeering is hardly a welcome-home signal for high earners now on the fence about their futures in New York.

The bottom line is that it’s a very bad idea for a country to tax unrealized capital gains.

And it’s a downright suicidal idea for a state to choose that perverse form of double taxation. After all, it’s very easy for rich people to move to Florida and other states with better tax laws.

And since the richest residents of New York pay such a large share of the tax burden (Investor’s Business Dailypoints out that the top 1 percent pay 46 percent of state income taxes), even a small increase in out-migration because of the new tax could result in receipts falling rather than rising.

After Barack Obama took office (and especially after he was reelected), there was a big uptick in the number of rich people who chose to emigrate from the United States.

There are many reasons wealthy people choose to move from one nation to another, but Obama’s embrace of class-warfare tax policy (including FATCA) was seen as a big factor.

Joe Biden’s tax agenda is significantly more punitive than Obama’s, so we may see something similar happen if he wins the 2020 election.

Given the economic importance of innovators, entrepreneurs, and inventors, this would be not be good news for the American economy.

The New York Timesreported late last year that the United States could be shooting itself in the foot by discouraging wealthy residents.

…a different group of Americans say they are considering leaving — people of both parties who would be hit by the wealth tax… Wealthy Americans often leave high-tax states like New York and California for lower-tax ones like Florida and Texas. But renouncing citizenship is a far more permanent, costly and complicated proposition. …“America’s the most attractive destination for capital, entrepreneurs and people wanting to get a great education,” said Reaz H. Jafri, a partner and head of the immigration practice at Withers, an international law firm. “But in today’s world, when you have other economic centers of excellence — like Singapore, Switzerland and London — people don’t view the U.S. as the only place to be.” …now, the price may be right to leave. While the cost of expatriating varies depending on a person’s assets, the wealthiest are betting that if a Democrat wins…, leaving now means a lower exit tax. …The wealthy who are considering renouncing their citizenship fear a wealth tax less than the possibility that the tax on capital gains could be raised to the ordinary income tax rate, effectively doubling what a wealthy person would pay… When Eduardo Saverin, a founder of Facebook…renounced his United States citizenship shortly before the social network went public, …several estimates said that renouncing his citizenship…saved him $700 million in taxes.

Here are some excerpts from a 2017 Bloomberg story.

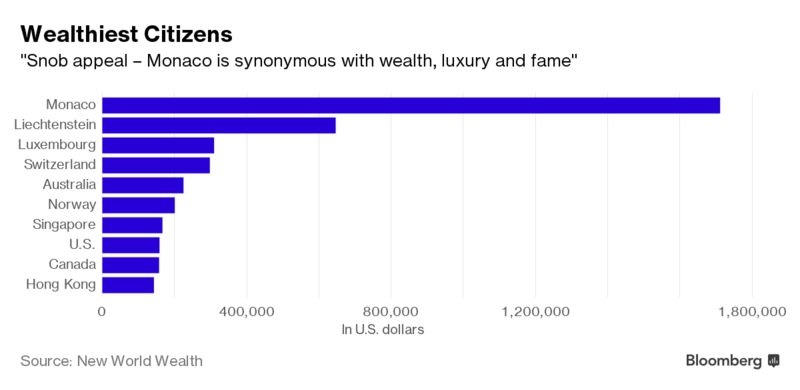

Australia is luring increasing numbers of global millionaires, helping make it one of the fastest growing wealthy nations in the world… Over the past decade, total wealth held in Australia has risen by 85 percent compared to 30 percent in the U.S. and 28 percent in the U.K… As a result, the average Australian is now significantly wealthier than the average American or Briton. …Given its relatively small population, Australia also makes an appearance on a list of average wealth per person. This one is, however, dominated by small tax havens.

Here’s one of the charts from the story.

As you can see, Australia is doing very well, though the small tax havens like Monaco are world leaders.

I’m mystified, however, that the Cayman Islands isn’t listed.

But I’m digressing.

Let’s get back to our main topic. It’s worth noting that even Greece is seeking to attract rich foreigners.

The new tax law is aimed at attracting fresh revenues into the country’s state coffers – mainly from foreigners as well as Greeks who are taxed abroad – by relocating their tax domicile to Greece, as it tries to woo “high-net-worth individuals” to the Greek tax register. The non-dom model provides for revenues obtained abroad to be taxed at a flat amount… Having these foreigners stay in Greece for at least 183 days a year, as the law requires, will also entail expenditure on accommodation and everyday costs that will be added to the Greek economy. …most eligible foreigners will be able to considerably lighten their tax burden if they relocate to Greece…nevertheless, the amount of 500,000 euros’ worth of investment in Greece required of foreigners and the annual flat tax of 100,000 euros demanded (plus 20,000 euros per family member) may keep many of them away.

The system is too restrictive, but it will make the beleaguered nation an attractive destination for some rich people. After all, they don’t even have to pay a flat tax, just a flat fee.

Italy has enjoyed some success with a similar regime to entice millionaires.

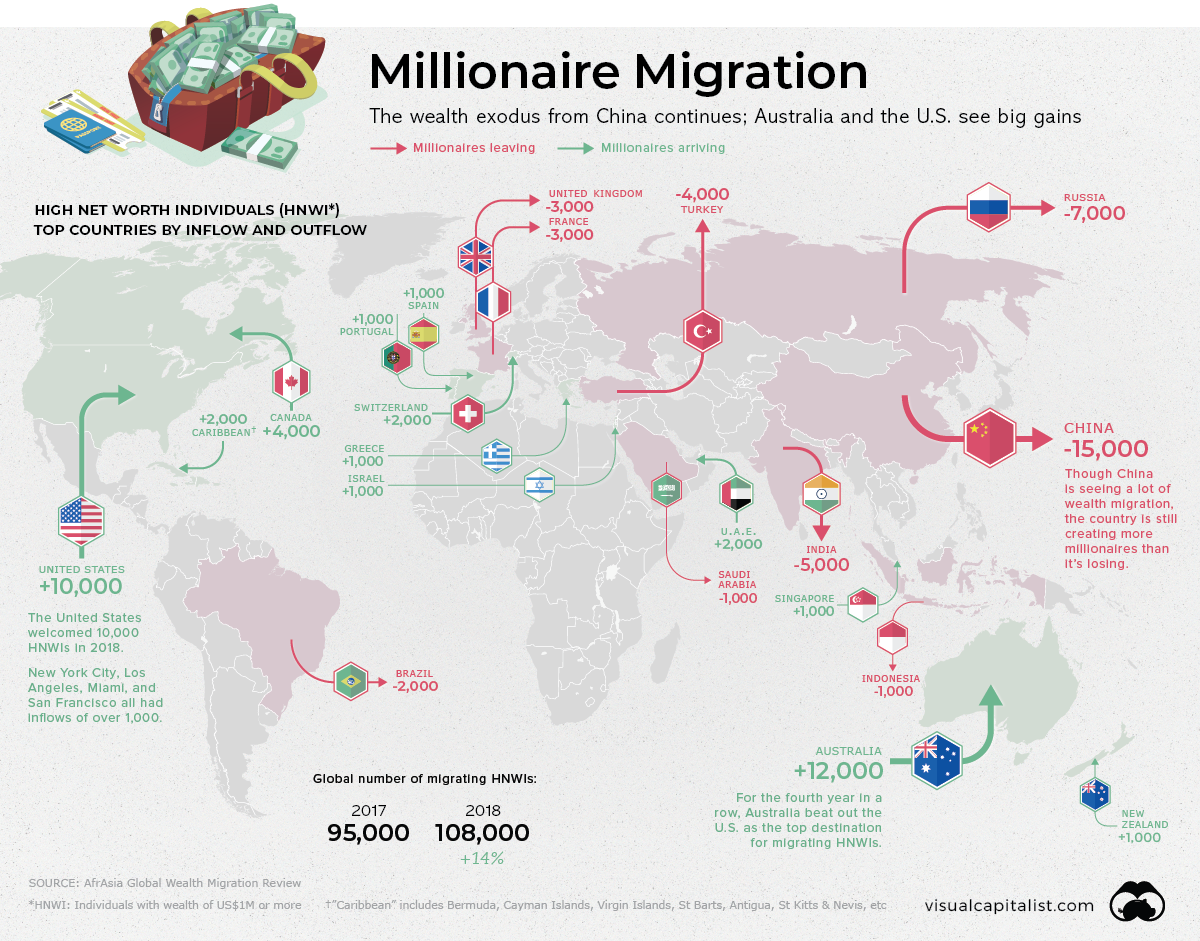

Last but not least, an article published last year has some fascinating details on the where rich people move and why they move.

The world’s wealthiest people are also the most mobile. High net worth individuals (HNWIs) – persons with wealth over US$1 million – may decide to pick up and move for a number of reasons. In some cases they are attracted by jurisdictions with more favorable tax laws… Unlike the middle class, wealthy citizens have the means to pick up and leave when things start to sideways in their home country. An uptick in HNWI migration from a country can often be a signal of negative economic or societal factors influencing a country. …Time-honored locations – such as Switzerland and the Cayman Islands – continue to attract the world’s wealthy, but no country is experiencing HNWI inflows quite like Australia. …The country has a robust economy, and is perceived as being a safe place to raise a family. Even better, Australia has no inheritance tax

Here’s a map from the article.

The good news is that the United States is attracting more millionaires than it’s losing (perhaps because of the EB-5 program).

The bad news is that this ratio could flip after the election. Indeed, it may already be happening even though recent data on expatriation paints a rosy picture.

The bottom line is that the United States should be competing to attract millionaires, not repel them. Assuming, of course, politicians care about jobs and prosperity for the rest of the population.

P.S. American politicians, copying laws normally imposed by the world’s most loathsome regimes, have imposed an “exit tax” so they can grab extra cash from rich people who choose to become citizens elsewhere.

P.P.S. I’ve argued that Australia is a good place to emigrate even for those of us who aren’t rich.

Since I don’t have any expertise on epidemiology, I’m not arguing that the economy should be opened immediately. I’m simply stating that the people who do make such decisions should be guided by the unavoidable tradeoff that exists between lives lost from disease and lives lost from foregone prosperity.

Which then raises the question of who should make such decisions.

As reported by the New York Post, President Trump claims he has all the authority.

President Trump on Monday said the decision to reopen the country’s ailing economy ultimately rests with him, not state leaders, as he feuds with governors over when to allow Americans to return to work. …Trump is now looking at reopening the economy by May 1, putting him on a collision course with state leaders who are pushing back, saying it would be dangerous to “take our foot off of the accelerator” in the war against the virus. …Rebuffing the president’s claims Monday, constitutional experts say it is state leaders who have the power to police their citizens under the 10th Amendment.

Trump is wrong.

He’s wrong in part because the Constitution limits the powers of the central government.

But he’s also wrong because – as explained by scholars from the Austrian School of Economics – we’re far more likely to get better choices when they’re decentralized.

In some cases, that means allowing individuals to make informed choices about how much risk to take.

But, to the extent government must be involved, it makes more sense to have state and local officials make choices rather than the crowd in Washington.

Opining for the Wall Street Journal, Walter Olson explains why federalism is the right approach.

Public-health merits aside, the president can’t legally order the nation back to work. The lockdown and closure orders were issued by state governments, and the president doesn’t have the power to order them to reverse their policies. In America’s constitutional design, …the national government is confined to enumerated powers. It has no general authority to dictate to state governments. Many of the powers government holds, in particular the “police power” invoked to counter epidemics, are exercised by state governments and the cities to which states delegate power. …Modernizers have long scoffed at America’s federalist structure as inefficient and outdated, especially in handling emergencies. …Today you won’t find these critics scoffing at the states or overglamorizing Washington. One federal institution after another, including the Food and Drug Administration and Centers for Disease Control and Prevention, has been caught flat-footed by Covid-19. …State governments, by contrast, with some exceptions here and there, have responded to the emergency more skillfully and in a way that has won more public confidence. …The record of federal systems—some of the best known are in Canada, Germany and Switzerland—suggests there’s a lot of resilience packed into the model.

Michael Brendan Dougherty elaborates in an article for National Review.

Writer Molly Jong-Fast complains, “So the states are basically governing themselves because our president doesn’t know how to president at all?” Well, no. It’s simple: Our president doesn’t have dictatorial powers, even in a national emergency. The president doesn’t have authority to shut down your local gin joint. Your state governor does have this power, in extraordinary circumstances. That so many governors have done so, often responding to popular demand for shutdowns, demonstrates America’s genuine practice of federalism — a system that is allowing us to respond to this crisis even faster than the states of Europe… One of the reasons federalism can act faster is that it allows decentralization. It is less politically risky to impose measures in one state than on an entire nation. You can respond where the hotspots are, rather than imposing costs evenly across an undifferentiated mass of the nation where the overall average risk may be low.

Professor Ilya Somin wrote on this same topic for Reason. He noted limitations on federalism in a pandemic, but also pointed out the benefits of decentralization.

The US is a large and diverse nation, and it is unlikely that a single “one-size-fits-all” set of social distancing rules can work equally well everywhere. In addition, state-by-state experimentation with different approaches can increase our still dangerously limited knowledge of which policies are the most effective. Moreover, if one policymaker screws up, his or her errors are less likely to have a catastrophic effect on the whole nation. …There is, in fact, a long history of state and local governments taking the lead in battling the spread of contagious disease. During the 1918-19 flu pandemic, state and local restrictions were the primary means of inhibiting the spread of the virus, while the federal government did very little.

John Daniel Davidson of the Federalist echoes the benefits of having choices made at the state and local level.

The founders wisely chose a federal republic for our form of government, which means sovereignty is divided between states and the federal government. The powers of the federal government are limited and enumerated, while all powers not granted to the feds are reserved for the states, including emergency police powers of the kind we’re seeing states and localities use now. …Much of the media seems wholly unaware of this basic feature of our system of government. …Trump explained that many governors might have a more direct line on this equipment and if so they should go ahead and acquire it themselves, no need to wait on Washington, D.C. This is of course exactly the way federalism is supposed to work. …We should expect the government power that’s closest to affected communities to be the most active, while Washington, D.C., concern itself with larger problems.

And those “larger problems” are the ones enumerated in Article 1, Section 8.

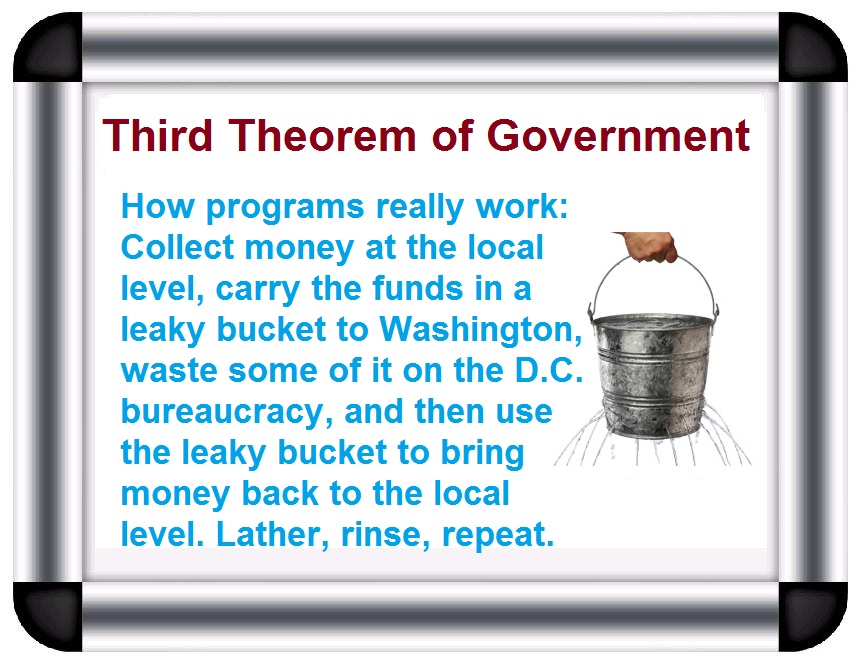

The bottom line is that we should always remember the Third Theorem of Government, which helps to explain one of the reasons why it’s generally a bad idea to give the folks in Washington more power and authority.