I’m going to add to that list today, but first let’s refresh our understanding of how government-caused “third-party payer” makes America’s health care system very expensive and inefficient.

The key insight is that consumers have little incentive to be smart shoppers when they perceive that other people are paying the bill. And health providers, needless to say, have little incentive to control costs when they know consumers care very little about prices.

Is this a big problem?

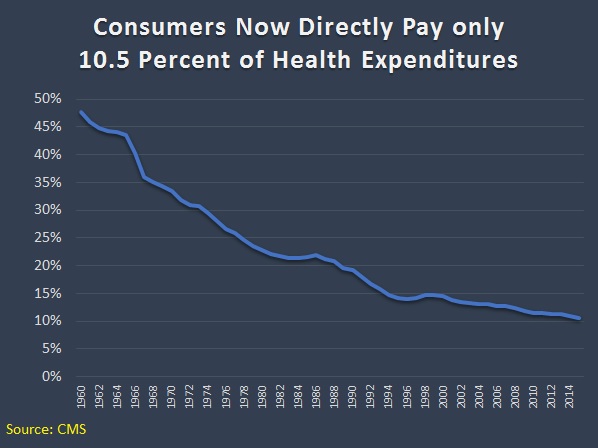

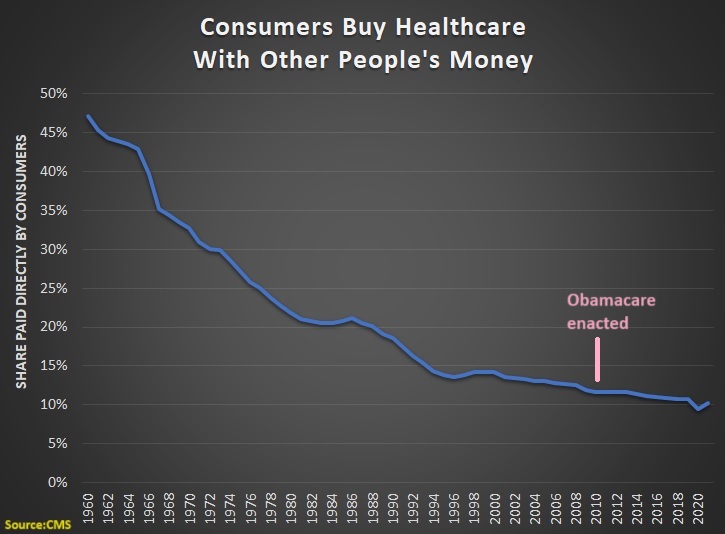

No, it is not a big problem. It is a giant problem. Here’s a chart, based on the federal government’s data, showing the share of health expenditures that are paid directly by consumers.

In the chart, I show the year that Obamacare was enacted. Notice that the legislation didn’t have an effect on the trendline, either the year it was enacted or in subsequent years as it was implemented.

And since Obamacare didn’t reduce the problem of third-party payer, one might guess that it didn’t solve the problem of rising health expenditures.

That guess would be correct, as shown in this column by Megan McArdle, which includes a predictably unsurprising headline.

…in 2022, the United States spent 16.6 percent of its gross domestic product on health care, while the next-highest spender, Germany, spent only 12.7 percent… As the Affordable Care Act took shape almost 15 years ago, its architects started looking for…savings… All these years later, we still haven’t found the magic money pot. …Obamacare contained a lot of elements that were expected to realize significant cost savings while actually improving the quality of care. …What this demonstrates is how hard it is to actually change the system in ways that generate major savings. …the wonks hunting for magic pots of money have mostly turned out to be chasing rainbows.

But there are countries where government causes even greater problems. So when I want to feel good about America’s clunky healthcare system, I look at the mess across the ocean.

The United Kingdom has a socialist health system. And it’s real socialism, with government running the hospitals and employing the doctors and nurses.

Ukrainian refugees who travelled to the UK to escape the war are risking their lives by returning to their homeland to seek urgent medical treatments after giving up on the NHS. Due the NHS pressures and long waiting lists for procedures, Ukrainians living with families across the UK are taking the perilous trip back into a war zone where they are treated by doctors immediately despite Russian bombardments of their towns and cities. …Maiia Habruk escaped Kyiv last spring along with around five million fellow citizens and found a safe haven with a couple in south east London. But she returned to Ukraine in mid-December after failing to get the treatment she needed from her local hospital in Lewisham. …She decided the only way to get the treatment she believed she required was to make the 24-hour trip back to Ukraine, which includes a flight to Poland and a long and dangerous train journey to Kyiv. …Maiia, who witnessed almost daily bombing raids by the Russians while in Kyiv, knows three other Ukrainians in London who sought emergency health procedures back in their war-torn country due to the lack of availability of quick treatment from the NHS.

These people were engaging in cost-benefit analysis. They compared the risk of death, injury, or suffering from Russian bombs to the risk of death, injury, or suffering from languishing on a waiting list in the United Kingdom.

And they decided Russian bombs were the better option.

This disaster is attracting attention in other nations. The Wall Street Journalopined two days ago about the NHS.

The American left can’t seem to quit its desire for single-payer Medicare for All. So it’s worth noting that the United Kingdom, which already has a system resembling that socialist dream, is rethinking it amid another winter of healthcare misery. …Waiting times for ambulances for the most serious calls are getting longer, with the average response time reaching 10 minutes 57 seconds in December, compared to a target of seven. Once patients reach the emergency room, 35% now face waits above four hours… As of November, some 7.2 million patients have been referred for treatment but are waiting for it to start. Of those, 2.9 million have been waiting more than 18 weeks. The NHS considers itself a success if it starts treatment within that four-month window, which is the epitome of defining failure down. …Excess deaths in 2022 were the most since 1951, excluding the pandemic. …The U.S. suffers a chronic problem of healthcare financing but not of health-care delivery. Britain shows that with single-payer you end up with both. The U.K. also shows that single-payer’s biggest victims are low-income people who can’t afford to opt out.

Allister Heath of the U.K.-based Telegraph has a grim assessment of his nation’s government-run system.

…the NHS is finished. It is broken beyond repair, ruining the lives of hundreds of thousands, and threatening the social fabric and economic performance of our nation. …this 75-year experiment in health socialism has failed appallingly, culminating in a surge in excess deaths, waiting lists that aren’t worthy of a civilised nation, inhumane strikes, intolerable delays for ambulances, explicit rationing… NHS spending is up 12 per cent in real terms since 2019-20; there are 13 per cent more doctors and 11 per cent more nurses, and yet the service delivered 5 per cent fewer treatments in the first nine months of 2022 than in the same period in 2019. …Its six pillars – that it is “free” at the point of use, the full state ownership of hospitals, its complete dependence on taxpayer funding, its supposed culture of altruism, its nature as a shared moral project uniting rich and poor, and its centrally planned workforce – are the very causes of its disintegration.

P.S. I can’t resist some closing comments about the politics of government-run health care.

The first story cited above includes these comments from left-of-center U.K. politicians.

Labour’s shadow health secretary Wes Streeting told i “Vladimir Putin is dropping bombs on Ukrainian hospitals, yet patients are travelling back to Kyiv rather than face NHS waiting lists. …Liberal Democrat health spokesperson Daisy Cooper said: “It’s a damning indictment of the government’s record on the NHS that Ukrainian refugees are returning to a war-torn country to access health care.”

Accurate criticisms, to be sure. But both Labour and the Lib Dems simply want to dump more money in the system.

But the so-called Conservative Party does exactly the same thing, as the Wall Street Journal noted in its editorial.

Former Prime Minister Boris Johnson in 2021 pledged an additional £36 billion over three years for the NHS and related home and nursing-home care, funded by a payroll-tax increase. Mr. Sunak and Chancellor Jeremy Hunt followed in November with another £3.3 billion a year for the next two years.

And Allister Heath made a similar observation in his column.

The Cameron-May-Johnson survival strategy was to “neutralise” the NHS by refusing to contemplate difficult reforms, genuflecting endlessly at its altar, prioritising it in every Budget, greatly boosting its funding after Brexit and worshipping it hysterically during the lockdowns; yet, in the end, it was the NHS that neutralised the Tories. Small-state, high-growth Toryism is incompatible with an unreconstructed NHS, with its need for ever-higher taxes. How long will the Conservatives continue to lie to themselves about this?

More specifically, politicians have enacted laws (everything from the tax code’s exclusion of fringe benefits to programs such as Medicare and Medicaid) that have produced a system overwhelmingly based on third-party payer.

And with so many people using (what they perceive to be) other people’s money to buy healthcare, we shouldn’t be surprised to see perverse results.

In a genuine free market, buyers and sellers directly interact. Both sides of the transaction have an incentive to get the best-possible outcome, and this process promotes efficiency and low prices.

In America’s healthcare system, however, government policies have saddled us with intermediaries that weaken, distort, or even eliminate normal market forces.

Which explains high costs and inefficiency, which is how we began this column.

To understand why third-party payer plays such a pernicious role, let’s look at a column that Dr. Ryan Neuhofel wrote for the Foundation for Economic Education.

He imagines a world where we buy food at the grocery store the same way we currently buy healthcare.

You enter the grocery store parking lot at 4:15 pm, having taken off work early because this particular store closes at 5:00 pm. This FoodMart wasn’t your personal preference based on quality, service, amenities, or price. You choose it, like all of your previous food choices, because it was included in your new food management plan’s network. …You are first greeted by a few women sitting behind a glass-enclosed desk. By greeted, I mean they ask you for your photo ID and food plan card and hand you a clipboard with a stack of forms to complete. The lobby is crowded, but you manage to find a seat… You have completed these types of forms dozens of times previously but dutifully do so again. (You still prefer 2 percent milk, don’t like more than four vegetables, and your peanut allergy is unchanged.) Forms completed, you check back in with the receptionist. After 20 minutes of waiting, she assigns you a cart, and you start to shop with your list in hand. …As you scurry up and down the aisles, you see there are no prices listed on anything, nor labels telling you what is a Bronze-Select item. …During check-out, the cashier rings up the items and asks you for a $30 copay. You are given a six-page receipt with indecipherable codes and then asked to sign a few other forms because some of your items will be billed to you later. …Several months in the future you get a bill for $276 from FoodMart. Although vaguely suspicious that you’ve been taken advantage of somehow, you are happy that you got a big discount on your $18 box of Tasty Flakes cereal.

He also imagines a world where our restaurant visits are akin to the current healthcare system.

…you are saddened to learn that Lola’s Cocina is not part of your GCGS plan. You decide to go down the street to Burrito King, which prominently displays “Proud to accept GCGS Bronze-Select members” in its window. …Upon checkout, you present the waiter your GCGS card, and you are asked to pay a $10 copay. (The billing statement weeks later reveals that the “plan discount” did reduce the initial charge from $64 to $37 and that GCGS paid Burrito King another $27 a few months later, which was applied to your deductible.) You question how a simple burrito can cost $37… Burrito King, a small restaurant, employs four cashiers out front and seven people in their business office in addition to the usual staff to cook and serve food. Their head chef, Bob, spends much of his time completing forms to justify why the Deluxe burrito you ordered included black beans instead of the standard pinto.

Dr. Neuhofel paints a dystopian vision, but can anyone doubt this is what would happen if government intervened in the food market the same way it does in the health market?

I’ve previously engaged in the same exercise, asking people to imagine what would happen if the market for homeowners insurance and auto insurance worked the same way as it does in the health sector.

Needless to say, the result would be higher costs and inefficiency.

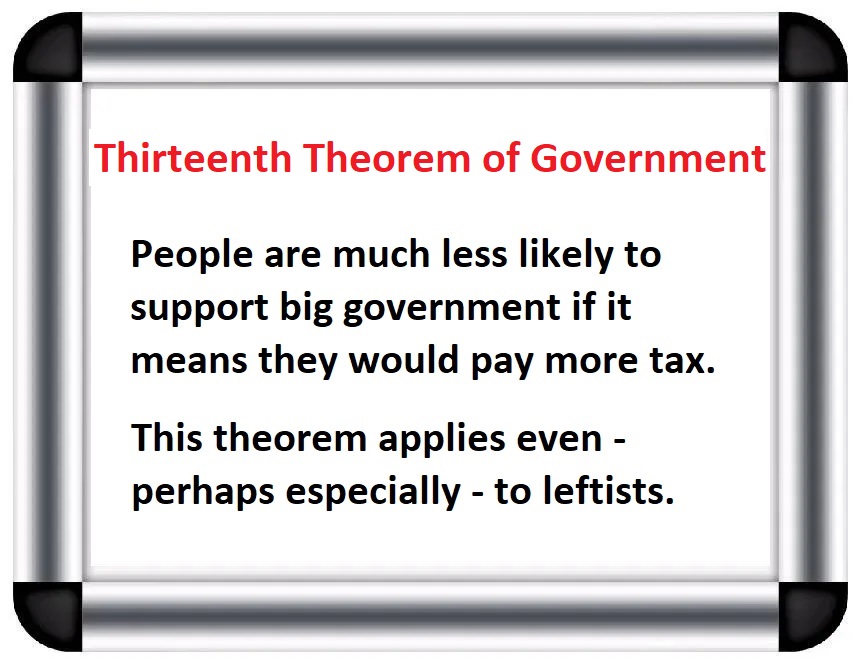

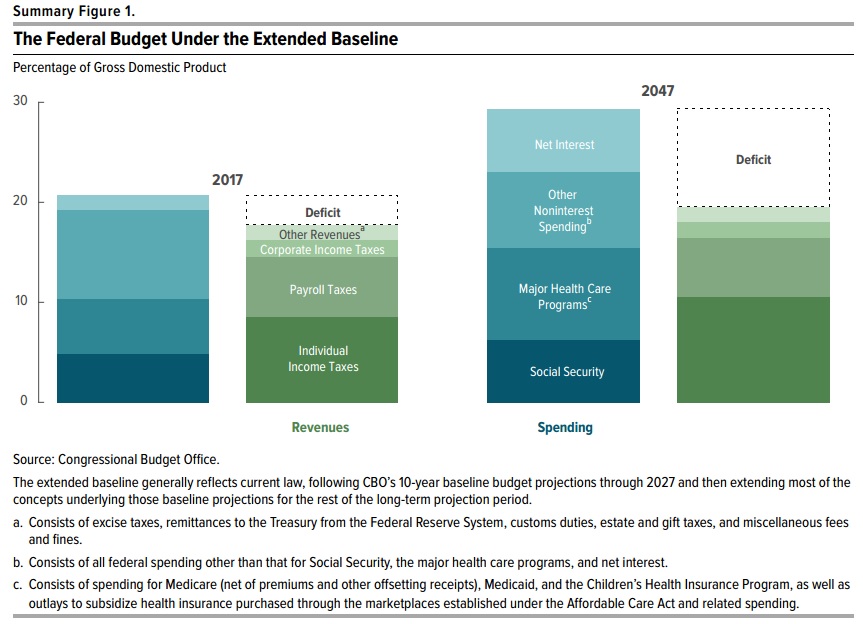

I wrote last month about a tax-and-spend proposal for single-payer healthcare in California (sort of a state version of “Medicare for All“).

I also analyzed the scheme in this discussion with Gene Tunny of Australia.

What’s remarkable, as Gene mentioned in his preface, is that the left’s push for single payer failed – even though Democrats have complete control of the Golden State, including more than three-fourths of the seats in both chambers of the state legislature.

Almost certainly, the biggest reason is that even folks on the left have second thoughts about the enormous tax increase that would have been required.

As I noted back in 2016, big government is only fun when somebody else is picking up the tab.

Which motivates me to unveil a Thirteenth Theorem of Government.

Let’s take a closer look at what happened with single payer in California.

Here are some excerpts from a report by Sophia Bollag for the Sacramento Bee.

Efforts to create a government-run health care system for all Californians stalled Monday when the lawmaker pushing the legislation announced he didn’t have the votes in time for a key deadline. Assembly Bill 1400 aimed to create a so-called single-payer health care system in California that would essentially replace private insurance with a state-run health system. …To fund it, lawmakers would have also needed to pass a separate bill to increase taxes… The taxes Kalra proposed would also require voter approval. …Kalra said the fight for single-payer health care won’t die with AB 1400. Lawmakers could craft a different bill to implement such a system in the future. The bill’s failure represents a blow to the California Nurses Association, which had backed the bill. …This isn’t the first time a bill to create a single-payer system has died in the Assembly. The Senate advanced a similar bill in 2017, but it died in the Legislature’s lower chamber. Gov. Gavin Newsom…has said he supports single-payer health care.

…higher taxes are a tough sell, even in the California Legislature where Democrats hold a super-majority. …Fiscal analyses estimate the bill could cost between $314 billion and $391 billion per year if it were implemented. That would dramatically increase total state spending; California’s current budget is $262 billion. To pay for it, Kalra proposed taxing businesses 2.3% of their income after the first $2 million through a proposed amendment to the California Constitution. His proposal would also have imposed a 1.25% payroll tax on employers of 50 or more people and an additional payroll tax on wages for California residents over $49,900 per employee. The measure would have added progressive income taxes starting at .5% for people making more than $149,500, up to 2.5% for people making more than about $2.5 million per year.

In a column for Forbes, Patrick Gleason points out that the failure of single payer in California is part of a pattern.

For progressive lawmakers and activists who want to enact a national single-payer health care system, rejection of a state-level “Medicare For All” proposal in one of the bluest states in the nation, where Democrats have sweeping control of state government, is seen as a major set back. …California isn’t the only state, let alone the only blue state, where single-payer health system legislation has crashed and burned. New York Assemblyman Richard Gottfried (D), the longest serving member of the history of the New York Assembly, has long pushed for the New York Health Act, a single-payer proposal for the Empire State. Assemblyman Gottfried’s bill was approved by the New York Assembly five times between 1992 and 2018, only to see the state senate decline to take it up. As in California, exorbitant cost projections have been the main obstacle to single-payer’s enactment. …it is single-payer champion Bernie Sanders’ state of Vermont where state-level Medicare-For-All first proved to be unworkable. More than a decade ago, Vermont state lawmakers enacted legislation to implement a single-payer system called Green Mountain Care. …Shortly after the single-payer bill was enacted in 2011, Vermont officials were confronted with the reality that “free” health care is actually pretty costly for taxpayers. Governor Shumlin and Vermont lawmakers discovered they would need to impose a new 11.5% state payroll tax and a 9.5 percentage point income tax increase to pay for the new entitlement. Together these tax increases would’ve represented a more than 150% hike in the state’s income tax.

If you want more information, I wrote about deep-blue Vermont’s disastrous (but fortunately temporary) experiment with single payer back in 2014.

The bottom line is that people (sadly) are willing to use government as a tool to steal from their neighbors. But the message of the Twelfth Theorem is that they generally don’t like to steal from themselves.

P.S. Here are the other 12 Theorems of Government.

The “First Theorem” explains how Washington really operates.

The “Second Theorem” explains why it is so important to block the creation of new programs.

The “Third Theorem” explains why centralized programs inevitably waste money.

The “Fourth Theorem” explains that good policy can be good politics.

The “Fifth Theorem” explains how good ideas on paper become bad ideas in reality.

The “Sixth Theorem” explains an under-appreciated benefit of a flat tax.

The “Seventh Theorem” explains how bigger governments are less competent.

The “Eighth Theorem” explains the motives of those who focus on inequality.

The “Ninth Theorem” explains how politics often trump principles.

The “Tenth Theorem” explains how politicians manufacture/exploit crises.

The “Eleventh Theorem” explains why big business is often anti-free market.

The “Twelfth Theorem” explains you can’t have European-sized government without pillaging the middle class.

The solution is free markets, and Hannah Cox points the way in this short video.

Ms. Cox is definitely correct to use cosmetic surgery as an example of how free markets work.

I’ve previously cited great research from Mark Perry showing how prices for various procedures have risen by less than the overall consumer price index.

And far less than prices for the parts of the health care system where government plays a big role (in the table, see the section outlined in red).

The bottom line is that we get lower costs and greater efficiency when buyers and sellers directly interact without lots of interference from government.

Ms. Cox also wrote about this topic, to augment what she said in the video.

If you’re somehow under the impression that the problems with our healthcare system were created by “capitalism,” you have been lied to. …If we were to cut the insurance companies and the government out of the picture, prices would naturally have to fall to meet what the market could actually afford to pay. No more $100,000 knee surgeries. A model of this can easily be found in the plastic surgery industry, which is a rare niche in the healthcare market that both the government and insurance companies have largely not touched. Because it is seen as an elective service, insurance does not cover these services, and therefore the government hasn’t been able to get its grubby hands on the industry. And because of that, the quality of service has consistently risen while the prices have fallen simultaneously. …True capitalists want the entire healthcare system to look like the cosmetic industry. But that can only happen if we get the government out of the way.

Economists refer to the problem Ms. Cox is discussing as “third-party payer,” and it exists because government policies (everything from the tax code’s healthcare exclusion to programs such as Medicare and Medicaid) have crippled market forces by creating a big wedge between buyers and sellers.

How much of a wedge?

Well, consumers directly pay for only 10.5 percent of healthcare expenditures.

P.S. Here’s my first-hand story of dealing with the problems caused by third-party payer.

P.P.S. Regardless of one’s views on abortion, it’s another example of how markets can work in healthcare.

P.P.P.S. This video from Reason is a compelling real-world illustration of how markets can succeed in the health sector. And here are two other excellent videos.

But let’s ignore the immature theatrics from Trump and Biden and focus on one of their policy disagreements.

The two candidates squabbled over whether creating a government-administered health plan (see page 31 for a description of Biden’s so-called “public option“) would lead to the demise of the current system of employer-provided health insurance.

For what it’s worth, there are two big reasons why I’m not a fan of the current employer-based system.

That being said, I’m very aware of the fact that politicians are always capable of making things worse (the “lather-rinse-repeat cycle” of government failure).

So let’s consider this key question: Government intervention has made our health system expensive and inefficient, but would a “public option” make things better or worse?

About two months ago, I shared this video which explains why the so-called public option will wind up being an expensive boondoggle.

But does that mean it also would be a threat to the employer-based system of private health insurance?

I think the answer is yes, largely because the subsidies that will make the system more expensive are also the subsidies that will make the public option seem like a good deal.

Let’s use two analogies to get this point across.

Fannie Mae and Freddie Mac dominate housing finance, not because government-created entities are efficient, but because they use subsidies from the federal government to under-price private competitors.

Parents know private schools produce much better educational outcomes than government schools, but most families opt for the inferior option because it’s already being financed by their tax dollars.

I fear the same thing will happen with the so-called public option. Politicians (in their never-ending efforts to but votes) will keep increasing the subsidies. That will make employer-based health plans seem less attractive by comparison.

And there will also be political pressure to provide an ever-more-extensive set of benefits (as illustrated by the cartoon). That will also make employer-based health plans seem less attractive by comparison.

The net result of all this is that even though the vast majority of workers are happy with their current employer-provided health plans, Biden’s public option will slowly but surely squeeze them out of the market.

The bottom line is that we’ll wind up with single-payer, government-run healthcare, but politicians would be sneaking it in the back door.

Even though Joe Biden has embraced a very left-wing agenda, I suspect many of the items on his wish list are designed to placate Bernie-type activists who have considerable influence in the Democratic Party.

As such, I don’t think Biden will push “Medicare for All” if he’s elected. But I fear he may support a “public option” that is less radical but still misguided.

The strongest argument in the video is that a government-created competitor to private insurance companies will be much more expensive than politicians are promising.

This is what always happens with government programs (see Medicare, Medicaid, and Obamacare) because politicians have a never-ending incentive to buy votes with other people’s money. And it will happen with any new program.

But I think the video overlooks an argument that would be even more politically effective, which is the fact that a public option would slowly but surely begin to strangle employer-based health insurance.

Simply stated, vote-buying politicians will deliberately under-price the cost of the public option. And the presence of a subsidized and under-priced government health plan will make employer-based policies less attractive over time – especially since the subsidies almost certainly will expand.

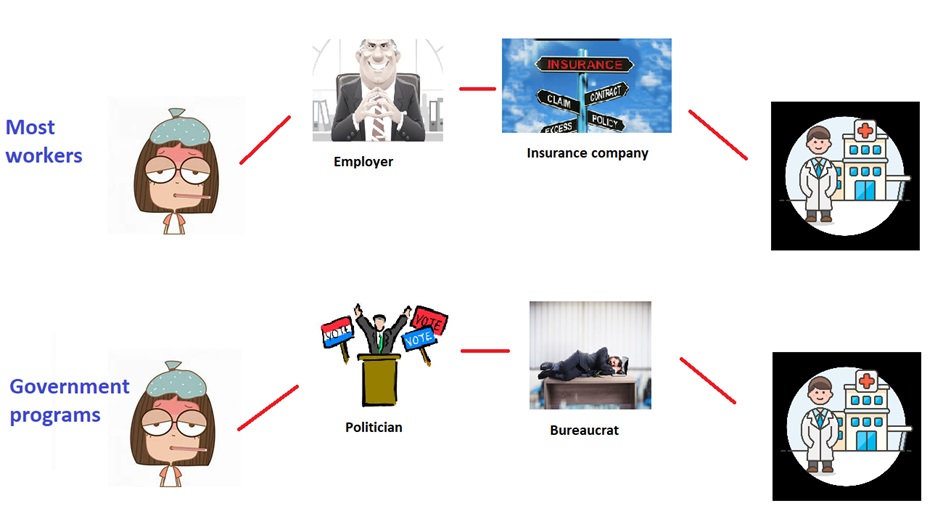

However, people generally like their employer-based health plans and presumably will be skeptical of any plan that threatens that system (and it’s probably safe to assume that health insurance companies will have an incentive to educate people about that likely outcome).

But with the public option, the best-case scenario is that many people over time will get pushed from the top line of this image to the bottom line.

And that’s also the worst-case scenario since no problems will be fixed, but overall costs will be even higher thanks to greater government involvement.

For what it’s worth, some advocates of the public option claim it can actually save money by lowering reimbursement rates to doctors and hospitals. That could happen in theory, but exploding costs for Medicare, Medicaid, and Obamacare show that it doesn’t happen in reality.

The bottom line is that more government intervention in health care won’t solve the problems caused by existing levels of government intervention in health care (a tragic example of Mitchell’s Law). Which is why I fear that the public option ultimately would be a slow-motion version of Medicare for All.

Near the beginning of the croronavirus crisis, I observed that “government-run health systems have not done a good job” of dealing with the pandemic.

And I’ve repeatedlynoted the failure of government bureaucracies to respond effectively in the United States.

Is there, perhaps, a lesson to be learned about what happens when politicians get more control of the health sector?

Let’s consider the different experiences of two European nations.

Kai Wess of the Austrian Economics Center in Vienna has a column for CapX on the performance of the German system.

…the responses of national governments to the crisis have been starkly different. …Germany’s approach is particularly interesting. …the death rate of Germany has been hovering around 0.2% to 0.5% for the entirety of March, only rising to the current 1.1% in the last days after deaths spiked in the first days of April. And yet, 1.1% is still light years away from Spain’s 8.7% Italy’s 11.7%, Britain’s 7.11%, and France’s 6.8%. …Germany’s lockdown has also been somewhat more lenient than in other European countries. …So why is Germany doing comparatively well? For one thing, mass testing has taken place for weeks… The second key factor is the good condition of Germany’s health sector. The number of critical care beds in Germany previously stood at 29.2 per 100,000 inhabitants – the highest of the countries most affected by Covid-19 other than the US (34.7). …why does Germany have these testing capacities? And why is the health sector so well-equipped? One of the main answers is that, at least relatively speaking, Germany’s health sector is more decentralised and leaves more room for competition… Germany does not have an NHS-style one-size-fits-all approach, but an insurance-based system. Everyone has to have health care and the government bears the cost for poorer patients. …there is competition between different insurance plans and individuals can pick their preferred plan. The health sector’s revenue comes from the premiums paid by patients as well as their employer – not through state funding. …The testing system has also been very decentralised, with a mixture of government agencies, private enterprise, and research organisations working on expanding testing capabilities – indeed, the January test was made possible by a private biotech entrepreneur. …when it comes to testing, Germany does not have a centralised diagnostic system, but a network of local authorities. As Christian Drosten explain, “Germany does not have a public health laboratory that would restrict other labs from doing the tests.”

Writing for the Telegraph, Charles Moore opines on its less-than-impressive track record.

The Government’s policy of lockdown is in significant part dictated by the demands not of patients, but of the NHS, and by its lack of adaptability and readiness. …A significant reason for the slow development, arrival and use of the antigen tests (“Have I got it?”) and the antibody tests (“Have I had it?”) seems to be the reluctance of the health service, and of Public Health England, to look outside their own spheres for help. In a culture almost proudly hostile to the private sector and mistrustful of independent academic work, the NHS’s first instinct is to defend bureaucratic territory. …the NHS belatedly admitted within government that it had failed to get enough ventilators. …University College Hospital, Formula I and Mercedes Benz got together to produce the CPAP… Next week, the repurposed Mercedes Benz F1 factory in Brixworth expects to produce 1,000 CPAPs a day. …the amazing 4,000-bed capacity Nightingale field hospital at the ExCeL centre in east London, opened yesterday… For two weeks after it was proposed, NHS top brass opposed it. When they finally admitted they needed it, the Army and the private contractors were the ones who made it happen in nine days. …Ten days ago, government contacts found the only company in Britain with expertise in making reagent for antigen swab tests. The firm was put on to the NHS, but at the time of writing, the health service had still not had a conversation with it. …That system is the problem. …The defects are baked into our system of national bureaucratic command. People have noticed that Germany has been more successful in managing the virus spread through testing. This is not a coincidence. Germany does not have our lumbering central diagnostic system, because it does not have, in our sense, a national health service.

These two columns are very instructive, not only because they show the adverse consequences of too much government, but also because they show that there are big differences in European health systems.

Many people have the (very!) inaccurate belief that the United States has a market-based system. And many of them also share the mistaken belief that all European nations have systems where everything is financed and provided by government.

In reality, there’s a wide divergence of policies across the globe.

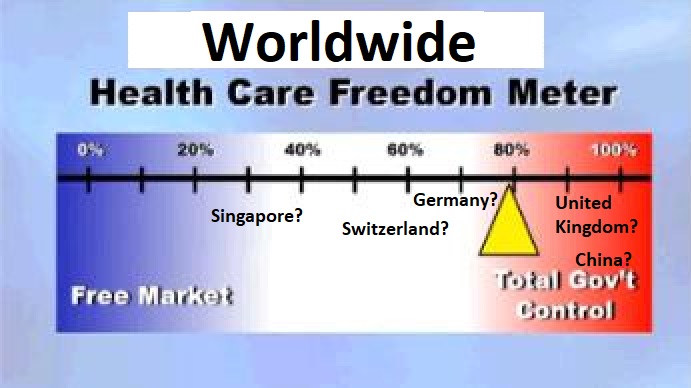

Back in 2013, I created a back-of-the-envelope “Freedom Meter” to illustrate how Obamacare was best viewed as in incremental step on a long (and well-traveled) road to a government-dominated health care system.

Simply stated, we already greatly reduced the role of markets thanks to a range of programs and policies (Medicare, Medicaid, the tax code’s healthcare exclusion, etc).

Obamacare simply added another layer of taxes, spending, and regulation.

I actually suspect many nations that supposedly have “government-run healthcare” actually would be closer to the free-market side of the Freedom Meter than the United States.

Sort of like what I’m depicting in this revised, worldwide version.

Though I admit I’m just guessing that Germany and Switzerland might be better than the United States.

Only instead of a fiscal ranking based on factors such as income taxes, business taxes, property taxes, and consumption taxes, we’d have a health ranking based on factors such as third-party payer, degree of centralization, consumer choice, regulatory burden, financing mechanisms, and extent of direct government provision.

If anybody’s aware of anything like this, please share.

It’s also a bad idea to head the wrong direction at 50 miles per hour.

In a column for the Wall Street Journal, Lanhee Chen exposes the reckless nature of the so-called public option that is supported by other candidates.

Joe Biden, Pete Buttigieg and Mike Bloomberg claim they’re proposing a moderate, less disruptive approach to health-care reform when they advocate a public option—a government policy offered as an alternative to private health insurance—in lieu of Medicare for All. Don’t believe it. …those effects are predicated on two flawed assumptions: first, that the government will negotiate hospital and provider reimbursement rates similar to Medicare’s fee schedules and far below what private insurers pay; second, that the government would charge “actuarially fair premiums,” which cover 100% of provided benefits and administrative costs.

Mr. Chen explains that politicians can’t resist buying votes by offering ever-more goodies at ever-lower costs (I made similar points in a video explaining why Obamacare would be a fiscal boondoggle).

Political pressure upended similar financing assumptions in Medicare Part B only two years after the entitlement’s creation. The Johnson administration in 1968 and then Congress in 1972 had to intervene to shield seniors from premium increases. Objections from health-care providers to low reimbursement rates have regularly led to federal spending increases in Medicare and Medicaid.

And when politicians offer more goodies at lower cost, that means someone else will have to pay.

Either taxpayers today (higher income taxes and payroll taxes) or taxpayers tomorrow (more borrowing).

If premiums can’t rise to cover program costs, or reimbursement rates are raised to ensure access to a reasonable number of providers, who’ll pay? Taxpayers… If Congress’s past behavior is a guide, a public option available to all individuals and employers would add more than $700 billion to the 10-year federal deficit. The annual deficit increase would hit $100 billion within a few years. Some 123 million people—roughly 1 in 3 Americans—would be enrolled in the public option by 2025, broadly displacing existing insurance. These estimates don’t include the costs of additional Affordable Care Act subsidies and eligibility expansions proposed by Messrs. Biden, Buttigieg and Bloomberg. …if tax increases to pay for a politically realistic public option were limited to high-income filers, the top marginal rate would have to rise from the current 37% to 73% in 2049… Congress could enact a new broad-based tax similar to Medicare’s 2.9% Hospital Insurance payroll tax. The new tax would be levied on all wage and salary income and would reach 4.8% in 2049.

Mr. Chen also reminds us that the public option would surely have a very bad effect on private insurance.

Beyond fiscal considerations, the public option would quickly displace employer-based and other private insurance. …Consumers seeking coverage would be left with fewer insurance options and higher premiums. …Longer wait times and narrower provider networks would likely follow for those enrolled in the public option, harming patients’ health and reducing consumer choice.

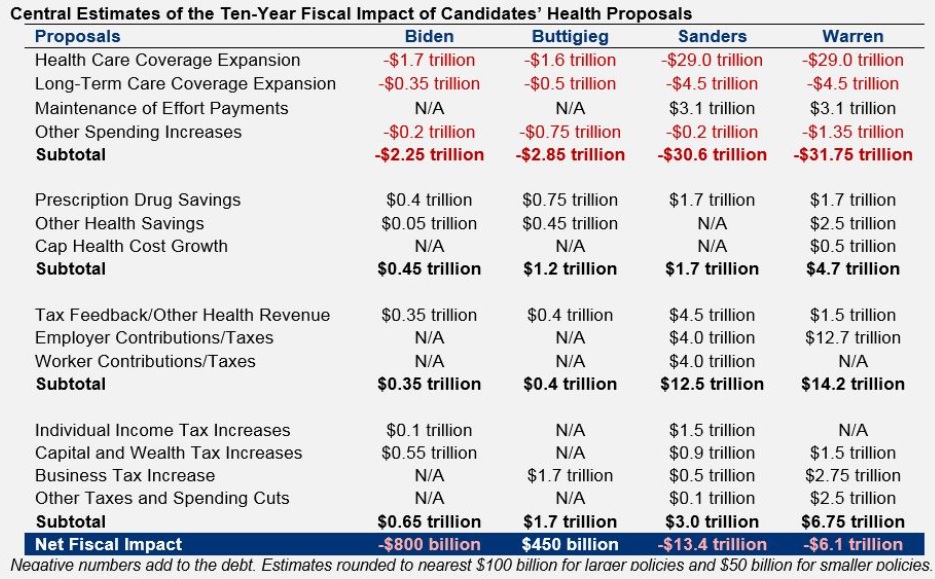

For those of you who like lots of numbers, I also recommend a new report from the Committee for a Responsible Federal Budget.

The folks at CRFB are a bit misguided in that they focus too much on deficits and debt when they should be mostly concerned about the size of government.

We’ll start with this table looking at the details of the plans that have been put forth by Biden, Buttigieg, Sanders, and Warren. The red numbers are new spending. The black numbers are offsets (mostly tax increases).

As you can see from the above table, Warren and Sanders are definitely in the go-rapidly-in-the-wrong-direction camp.

But that shouldn’t distract us from the fact that Biden and Buttigieg also are proposing a big expansion in the burden of government.

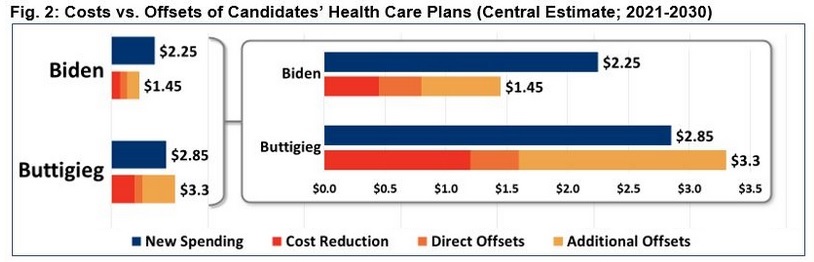

Here’s another graphic from the CRFB report, but I’m focusing solely on the numbers for Biden and Buttigieg so that it’s clear to see that they both want about $2 trillion of new spending over the next decade.

If you look closely at the numbers for Buttigieg in Figure 2, you’ll notice that his health plan supposedly will reduce the deficit by $415 billion over 10 years (the difference between $3.3 trillion of new spending and $2.85 trillion of cost reductions and offsets).

Does that make his plan desirable? Of course not. What he’s really proposing (and this is how CRFB should have presented the data) is $1.65 trillion of net new spending (the difference between his “new spending” and his “cost reductions” ) accompanied by $2.1 trillion of new taxes.

P.S. Most of the “cost reductions” in Buttigieg’s plan are achieved with price controls on prescription drugs. At the risk of understatement, that’s a very costly way of trying to save money.

P.P.S. And if his plan is ever enacted, don’t forget that the actual amount of “new spending” will be much higher than the estimate of “new spending.”

Here’s the other part of the interview, which revolved around a very bad idea to copy nations that impose price controls on prescription drugs.

In some sense, this is a debate on price controls, which have a long history (going all the way back to Ancient Rome) of failure.

But my comments focused primarily on the adverse consequences of Pelosi’s approach.

And if you want more details, Doug Badger explained how Pelosi’s approach would backfire in a report for the Heritage Foundation. He starts with an explanation of the legislation.

The Lower Drug Costs Now Act of 2019 (H.R. 3), introduced last week with the backing of House Speaker Nancy Pelosi, D-Calif., would double down on the failures of existing government policies that have distorted prescription drug prices and contributed to higher health care costs. …H.R. 3 would establish a system in which the U.S. government bases prices for cutting-edge drug treatments on those set by foreign governments. The measure would set an upper price limit at 1.2 times a drug’s average price in six other countries (Australia, Canada, France, Germany, Japan, and the United Kingdom). The secretary of health and human services then would seek to “negotiate” prices below that upper limit for at least 25—and as many as 250—drugs each year. …A manufacturer that declined to negotiate the price of any of its products would incur an excise tax of up to 95% of the revenues it derived from that product in the preceding year.

Doug then warns against an expansion of government power.

The bill represents an unprecedented exercise of raw government power. The federal government already imposes price curbs across a range of programs, requiring manufacturers to pay the government rebates… These provisions all are confined to federal programs, but nonetheless have distorted drug prices throughout the health sector. It’s one thing for the government to dictate the prices it pays in programs it finances. It is quite another for the government to impose a price for a product’s private sale and to extract money from a company on a long-ago settled transaction.

He then concludes by showing some of the negative consequences.

…aggressive government price-setting has damaged innovation and limited access to new treatments in all six of the countries whose price controls the bill would import. If the U.S. adopts price controls, it risks the same results here. Access to new drugs is much greater in the U.S. than in countries with price controls, in part because of having shunned price controls. …This lack of access can have damaging effects. A study by IHS Markit…concluded that Americans gained 201,700 life years as a result of faster access to new medicines. …Countries with price controls also suffer a decline in pharmaceutical research and development. In 1986, European firms led the U.S. in spending on pharmaceutical research and development by 24%. After the imposition of price control regimes, they fell behind. By 2015, they lagged the U.S. by 40%. …the president’s Council of Economic Advisers…concluded that while price controls might save money in the short term, they would cost more money in the long run. Government price-setting, it wrote, “makes better health care costlier in the future by curtailing innovation.”

As you can see, price controls have a deadly effect in the short run (the 201,700 life years).

But as I stated in the interview, the far greater cost – in terms of needless deaths – would become apparent in the long run as new drugs no longer come to market.

By the way, it’s not just me, or folks on the right, who recognize that there will be adverse consequences from price controls.

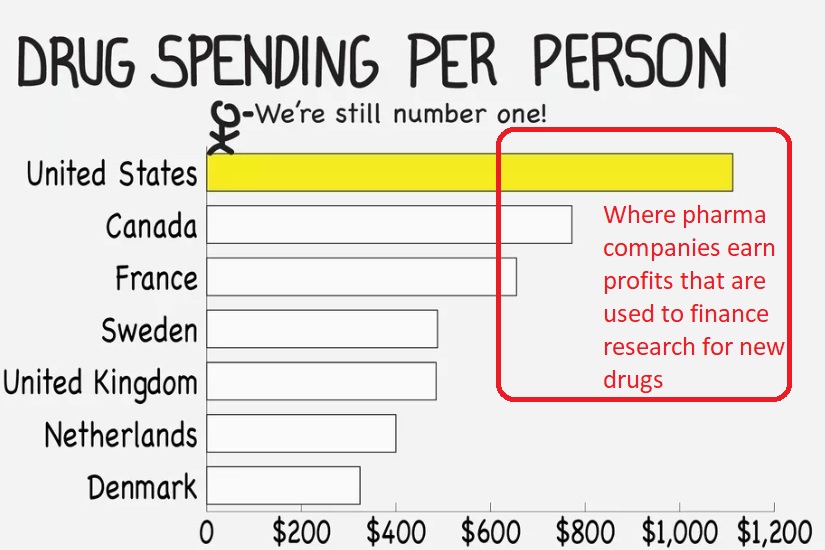

Writing for left-leaning Vox, Sarah Kliff acknowledges that there are trade-offs.

The United States is exceptional in that it does not regulate or negotiate the prices of new prescription drugs when they come onto market. …And the problems that causes are easy to see, from the high copays at the drugstore to the people who can’t afford lifesaving medications. What’s harder to see is that if we did lower drug prices, we would be making a trade-off. Lowering drug profits would make pharmaceuticals a less desirable industry for investors. And less investment in drugs would mean less research toward new and innovative cures. …In other words: Right now, the United States is subsidizing the rest of the world’s drug research by paying out really high prices. If we stopped doing that, it would likely mean fewer dollars spent on pharmaceutical research — and less progress developing new drugs for Americans and everybody else.

Here’s a chart from her article, which I’ve modified (in red) to underscore how other nations are free-riding because American consumers are picking up the tab for research and development.

By the way, I have no idea where the red lines actually belong. I’m just trying to emphasize that consumers who pay the market price (or closer to the market price) are the ones why underwrite the cost of discovering new drugs and treatments.

And Ms. Kliff definitely agrees this trade-off exists.

Every policy decision comes with trade-offs… If the United States began to price regulate drugs, medications would become cheaper. That would mean Americans have more access to drugs but could also expect a decline in research and development of new drugs. We might have fewer biotech firms starting up, or companies deciding it’s worth bringing a new drug to market. …Are we, as a country, comfortable paying higher prices for drugs to get more innovation? Or would we trade some of that innovation to make our drugs more accessible to those of all income levels?

For what it’s worth, I don’t actually think there’s much of a trade-off. I choose markets, both for the moral reason and because I want to maximize long-run health benefits for the American people.

P.S. Because pharmaceutical companies got in bed with the Obama White House to support Obamacare, some people may be tempted to say Pelosi’s legislation is what they deserve. While I fully agree that it’s despicable for big companies to get in bed with big government, please remember that the main victims of Pelosi’s legislation will be sick people who need new treatments.

I’ve always considered Senator Bernie Sanders to be the most clueless and misguided of all presidential candidates.

But I also think “Crazy Bernie” is actually sincere. He really believes in socialism.

Elizabeth Warren, by contrast, seems more calculating. Her positions (on issues such as Social Security, corporate governance, federal spending, taxation, Wall Street, etc).) are radical, but it’s an open question whether she’s a true believer in statism. It’s possible that she simply sees a left-wing agenda as the best route to winning the Democratic nomination.

Regardless of motive, though, her proposals are economic lunacy. So maybe it’s time to give her “Looney Liz” as a nickname.

Consider, for instance, her new Medicare-for-All scheme. She got hammered for promising trillions of dollars of new goodies without specifying how it would be financed, so she’s put forward a plan that ostensibly fits the square peg in a round hole.

But as Chuck Blahous of the Mercatus Center explains, her plan is a farce.

…presidential candidate Sen. Elizabeth Warren released her proposal to ostensibly pay for the costs of Medicare for All (M4A) without raising taxes on the middle class. As published, the plan would not actually finance the costs of M4A. …the Warren proposal understates M4A’s costs, as quantified by multiple credible studies, by about 34.2%. Another 11.2% of the cost would be met by cutting payments to health providers such as physicians and hospitals. Approximately 20% of the financing is sought by tapping sources that are unavailable for various reasons, for example because she has already committed that funding to other priorities, or because the savings from them was already assumed in the top-line cost estimate. The remaining 34.6% would be met by an array of new and previous tax proposals, most of it consisting of new taxes affecting everyone now carrying employer-provided health insurance, including the middle class.

Here’s a pie chart showing that Warren is relying on smoke and mirrors for more than 50 percent of the financing.

By the way, the supposedly real parts of her plan, such as the new taxes, are a very bad idea.

Brian Riedl of the Manhattan Institute unleashed a flurry of tweets exposing flaws in her proposal.

Since I’m a tax wonk, here’s the one that grabbed my attention.

Combination of 35% corporate rate (worldwide, no deferral), “Real corporate profits tax,” curtail depreciation, huge capital gains taxes, financial transactions tax, bank tax, and 6% wealth tax is economic fantasyland. Taxes on capital would be through the roof. 9/

If ever enacted, the United States presumably would drop to last place in the Tax Foundation’s competitiveness ranking.

And let’s not forget that Medicare-for-All would dramatically increase the burden of government spending. In one fell swoop, we’d become Greece.

Actually, that probably overstates the damage. Based on my Lassez-Faire Index, I’m guessing we’d be more akin to Spain or Belgium (in other words, falling from #6 in the rankings to the #35-#40 range according to Economic Freedom of the World).

P.P.S. Looney Liz’s plan is terrible fiscal policy, but keep in mind it’s also terrible health policy since it would exacerbate the third-party payer problem.

When I followed public policy in my younger days, I periodically would see stories about legislation that was approved by the House of Representatives with only one dissenting vote.

My memory isn’t perfect, I’m sure, but it seems that Ron Paul was always that lonely member. And my recollection is that he was (as usual) always on the correct side, voting for liberty and against government.

Something similar happened yesterday, except this time six members of Congress voted against a repeal of the “Cadillac Tax” that is part of Obamacare.

It was an eclectic group, but it included Justin Amash and Chip Roy, who are two of the most committed and principled supporters of free markets and limited government in Congress.

From the right, I recommend this analysis from Alan Viard at the American Enterprise Institute.

…employer-provided health insurance gets a big tax break. Workers pay income and payroll taxes on their cash wages, but not on their health insurance benefits. …the tax break is poorly targeted because it applies even to high-cost “Cadillac” health plans. The tax system should not artificially encourage Cadillac plans, which boost demand for medical services and drive up health care costs for everyone. Although the Cadillac tax does not directly change the tax break for high-cost employer plans, it offsets the break by imposing a separate 40 percent tax on those plans. That round-about approach is far from ideal, but it gets the job done. …the Cadillac tax has won support from economists across the ideological spectrum.

From the left, here’s some of what Bruce Bartlett wrote for the New York Times.

Although obviously a form of income to the worker, the Internal Revenue Service nevertheless ruled that it was not taxable, although businesses could still deduct the cost. This anomalous tax treatment was a fabulous tax loophole for both businesses and workers… Congress codified the I.R.S. ruling.. Various tax expenditures for health cost hundreds of billions of dollars in lost revenue per year, according to the Congressional Research Service. Eliminating them could finance a significant reduction in tax rates. …If the Republicans are serious about using tax reform to improve the competitiveness of American businesses, the best thing they can do is reform employer-based health insurance.

For honest folks on the left, they should be motivated by the fact that this exclusion overwhelmingly benefits upper-income taxpayers.

There are two visuals from my presentation I want to highlight.

First, I took Milton Friedman’s explanation of the how people care about cost and quality depending on whether they’re spendingf their own money and whether they’re buying for themselves, and I then showed how it applies to America’s healthcare system.

Ideally, purchases are made in quadrant 1. Thanks to government distortions, however, most health spending in America occurs in quadrants 2, 3, and 4.

When purchases occur in quadrant 1, buyers and sellers directly interact and there are incentives on both sides to get the most value.

That’s not the case, though, with purchases in the other quadrants.

I illustrated the problem with a slide that looks at the layers that exist between health consumers and health providers.

Doctor Scott Atlas, in a column for today’s Wall Street Journal, concisely explains the problem of government-created third-party payer.

In an effort to bring down the costs of medical care, the Trump administration wants to make prices visible to patients, and it’s moving aggressively to make that happen. …A new executive order will require providers paid by Medicare to post prices for a range of procedures. Meanwhile, the Centers for Medicare and Medicaid Services recently finalized its mandate requiring pharmaceutical manufacturers to disclose the list price of prescription drugs in direct-to-consumer television advertisements. …Yet these moves won’t be enough to bring down prices. Transparency, though essential, is not sufficient. Nor does it always need to be legislated. Laws aren’t required to force sellers of food, computers or clothing to post prices. That information is driven by consumers who actively seek value for their money. …But patients typically don’t even ask about prices, because they figure “it’s all covered by insurance.” The harmful U.S. model is unfortunately that insurance should minimize any out-of-pocket payment. Health care may be the only good or service in America that is bought and used without knowing its cost. Unfortunately, the Affordable Care Act instilled even broader coverage requirements and added counterproductive subsidies that encouraged more-widespread adoption of bloated insurance, reinforcing a model of coverage that prevents patients from caring about prices.

How do we fix the problem?

Dr. Atlas says people need to have control over their healthcare dollars.

To bring prices down, …patients must have stronger incentives to consider price. …But as long as insurance minimizes the patient’s share of cost, the patient won’t bother price shopping. For price-transparency to have the most impact, it must increase visibility of the only price relevant to patients—out-of-pocket costs at the time of purchase. Cheaper insurance policies with higher deductibles, coupled with large, liberalized-use, permanently owned health savings accounts, are also important to motivate consideration of price. …We can make medical care more affordable without moving to a single-payer system. Centralized models uniformly regulate costs by restricting health-care use, generating lengthy delays for needed care, limiting access to important drugs and technology, and ultimately resulting in worse disease outcomes. The better path will involve reducing the cost of medical care itself by creating the conditions that bring down prices in every other area of the economy: incentivizing empowered consumers and increasing the supply of medical care to stimulate competition among providers.

Amen.

That means reforming Medicare and Medicaid, where the government directly creates third-party payer.

At the risk of upsetting some people, it even means defending the “Cadillac tax,” a provision of Obamacare.

And even agreeing with the Washington Post, which opined today in favor of that provision.

Consider the House supermajority, made up of Democrats and Republicans favoring repeal of the excise tax on high-cost health insurance plans, which would otherwise take effect in 2022. …the bill is backed by a potent lobbying coalition including insurance companies, labor unions — and even ExxonMobil. …Known as the “Cadillac tax” because it applies to especially generous “Cadillac” health plans, the tax equals 40 percent of the value of private-sector health benefits exceeding $11,200 for single coverage and $30,150 for family coverage in 2022. Albeit indirectly, the tax chips away at one of the largest subsidies in the health-insurance system, the tax exclusion for employer-paid health insurance… A wide consensus of economists identifies the tax exclusion as a major source of distortion in the U.S. system, building a higher floor under costs… The Cadillac tax would curb these tendencies… killing the Cadillac tax… The United States’ already out-of-whack health-care system will become more so, and bipartisan profligacy and pandering will have triumphed again.

Let’s close with a bit of dark humor.

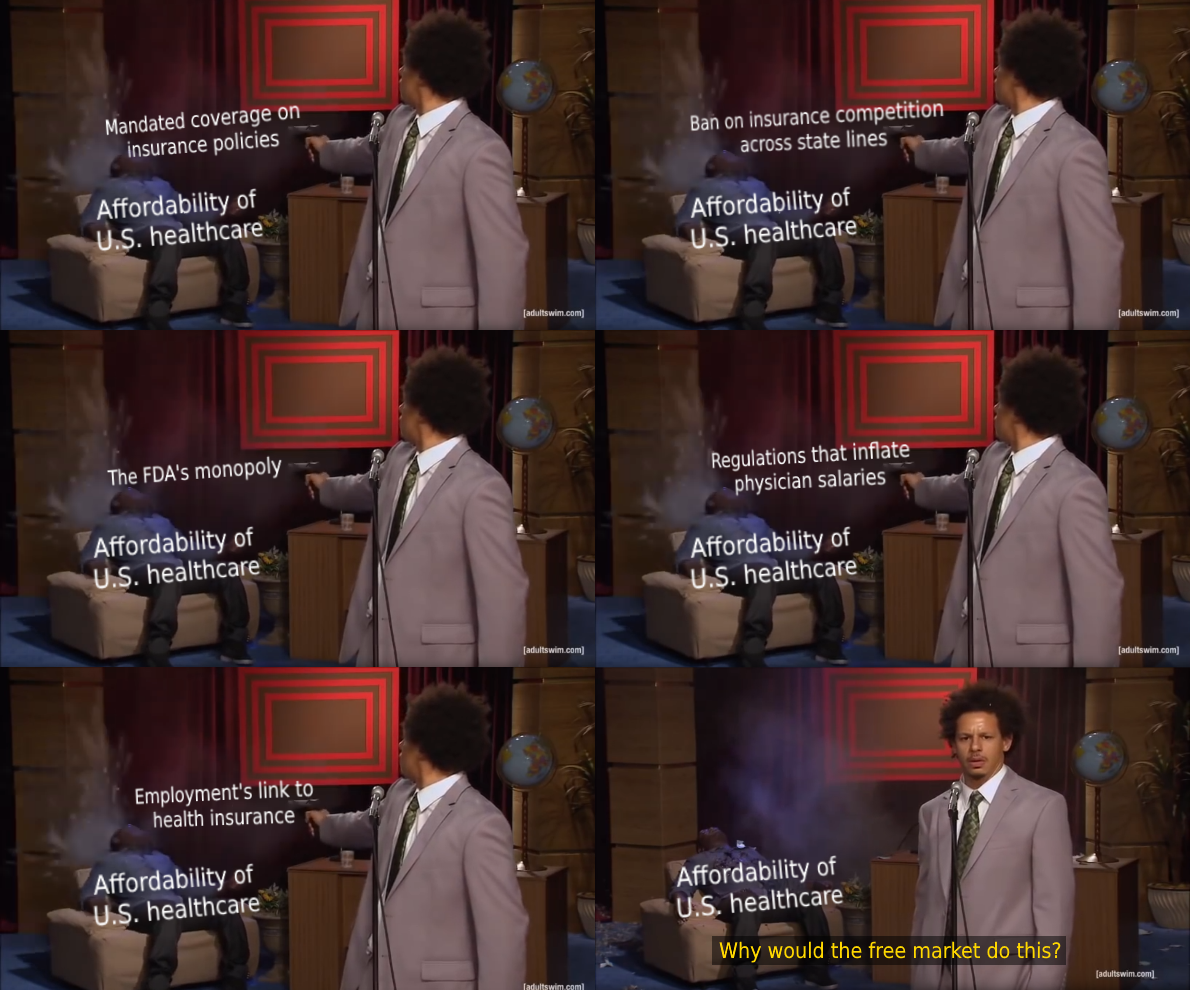

One of my many frustrations is that people blame the free market for the various government-caused problems in healthcare. Here’s a way of visualizing it.

Government intervenes, which causes problems, and those problems are then used as an excuse for additional intervention. Sort of a turbo-charged version of Mitchell’s Law.

Ultimately, this process may lead politicians to adopt something really crazy, such as “Medicare for All.”

But the most expensive item on the list is “Medicare for All,” which is a scheme concocted by Bernie Sanders to have the government pay for everything.

Would this be a good idea? In a column for Forbes, Sally Pipes of the Pacific Research Institute explains that government-run healthcare in the United Kingdom has some very unfriendly features.

Nearly a quarter of a million British patients have been waiting more than six months to receive planned medical treatment from the National Health Service, according to a recent report from the Royal College of Surgeons. More than 36,000 have been in treatment queues for nine months or more. …Consider how long it takes to get care at the emergency room in Britain. Government data show that hospitals in England only saw 84.2% of patients within four hours in February. …Wait times for cancer treatment — where timeliness can be a matter of life and death — are also far too lengthy. According to January NHS England data, almost 25% of cancer patients didn’t start treatment on time despite an urgent referral by their primary care doctor. …And keep in mind that “on time” for the NHS is already 62 days after referral.

If this sounds like the VA health care system, you’re right.

And both produce bad outcomes. Here’s some of the data from the British system.

Unsurprisingly, British cancer patients fare worse than those in the United States. Only 81% of breast cancer patients in the United Kingdom live at least five years after diagnosis, compared to 89% in the United States. Just 83% of patients in the United Kingdom live five years after a prostate cancer diagnosis, versus 97% here in America.

The best part of Sally’s column is that she explains how the flaws in the U.K. system are being copied by Bernie Sanders and other supporters.

Great Britain’s health crisis is the inevitable outcome of a system where government edicts, not supply and demand, determine where scarce resources are allocated. Yet some lawmakers are gunning to implement precisely such a system in the United States. The bulk of the Democratic Party’s field of presidential candidates — including Senators Kirsten Gillibrand, Kamala Harris, and Elizabeth Warren — co-sponsored Senator Bernie Sanders’s 2017 “Medicare for All” bill. That plan would abolish private insurance and put all Americans on a single government-run plan… Britons face long waits for poor care under their country’s single-payer system. That’s not the sort of healthcare model the American people are looking for.

The bottom line is that Medicare for All would further exacerbate the third-party payer problem that already plagues the health care system.

And that means ever-escalating demand, rising costs, and inefficiencies.

Taxpayers in the U.K. endure higher burdens than their counterparts in America, But they also suffer from the second option for dealing with the cost spiral, which is rationing.

Some of the data was in Ms. Pipes’ column.

If you want more examples (and some horrifying examples), you can click stories from 2017, 2016, 2015, 2014, 2013, and 2012.

America’s healthcare system is a mess, largely because government intervention (Medicare, Medicaid, Obamacare, and the tax code’s healthcare exclusion) have produced a system where consumers almost never directly pay for their medical services.

This “third-party payer” system basically means market forces are absent. Consumers have very little reason to focus on cost, after all, if taxpayers or insurance companies are picking up the tab for nearly 90 percent of expenses.

As a result, we get ever-higher prices.

But we also get a lot of featherbedding and inefficiency because providers want to take advantage of this system.

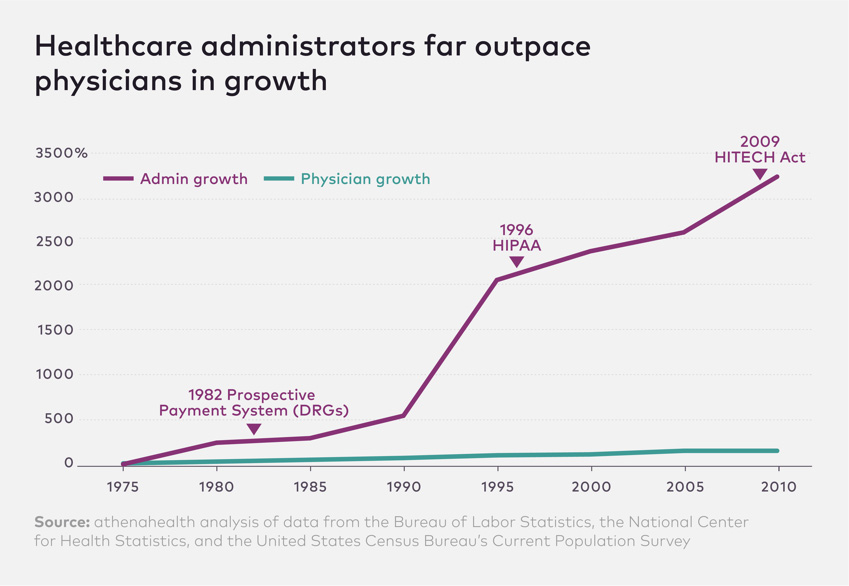

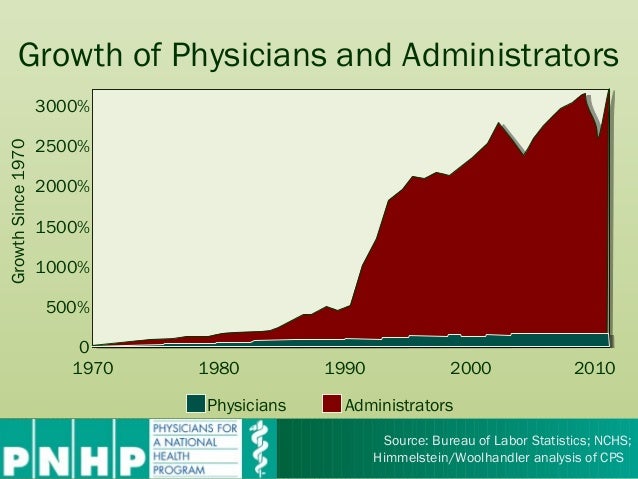

The number of physicians in the United States grew 150 percent between 1975 and 2010, roughly in keeping with population growth, while the number of healthcare administrators increased 3,200 percent for the same time period. Yes, that’s 3,200 percent in 35 years…the growing number of administrators is…driven by…ever-more-complex regulations. (To cite just a few industry-disrupting regulations, consider the Prospective Payment System of 1983; the Health Insurance Portability & Accountability Act of 1996; and the Health Information Technology for Economic and Clinical Act of 2009.) Critics say the army of administrators does little to relieve the documentation burden on clinicians, while creating layers of high-salaried bureaucratic bloat in healthcare organizations.

And here’s the chart that succinctly captures so much of what is wrong with America’s government-distorted healthcare regime.

By the way, the chart implies that the rising number of administrators is driven by additional regulations from Washington. I certainly won’t disagree with the notion that more red tape is counterproductive, but I suspect that third-party payer is the primary cause of the problem.

Third-party payer is what causes prices to climb, and then the government and insurance companies respond with various cost-control measures that require lots of paperwork and monitoring. Hence, more administrators.

In other words, third-party payer is the problem and regulations and administrators are both symptoms.

I’ll close by noting that I shared a version of this chart last year and warned that the numbers might be exaggerated. But there’s no question about the trend of more bureaucracy, red tape, and inefficiency.

P.S. Because it’s so important to fix the third-party payer problem, I’ve actually defended one small provision of Obamacare.

The only good policies I could find in the United States, by contrast, were food stamp reforms in Maine, Wisconsin, and Kansas.

This year has a depressingly small list of victories. Indeed, the only good thing I had on my initial list was the tax bill. So to make 2017 appear better, I’m turning that victory into three victories.

Limits on the deductibility of state and local taxes – It would have been preferable to totally abolish the deduction for state and local taxes, but a $10,000 cap will substantially curtail the federal tax subsidy for higher taxes by state and local government. The provision is only temporary, so it’s not an unambiguous win, but the whining and complaining from class-warfare politicians in New York and California is music to my ears.

No border-adjustment tax – Early in 2017, I was worried that tax reform was going to be tax deform. House Republicans may have had good intentions, but their proposed border-adjustment tax would have set the stage for a value-added tax. I like to think I played at least a small role in killing this bad idea.

Regulatory Rollback – The other bit of (modest) good news is that the Trump Administration has taken some steps to curtail and limit red tape. A journey of a thousand miles begins with a first step.

Now let’s look elsewhere in the world for a victory. Once again, there’s not much.

Macron’s election in France – As I scoured my archives for some good foreign news, the only thing I could find was that a socialist beat a socialist in the French presidential election. But since I have some vague hope that Emanuel Macron will cut red tape and reduce the fiscal burden in France, I’m going to list this as good news. Yes, I’m grading on a curve.

Illinois tax increase – If there was a contest for bad state fiscal policy, Illinois would be a strong contender. That was true even before 2017. And now that the state legislature rammed through a big tax increase, Illinois is trying even harder to be the nation’s most uncompetitive state.

Kansas tax clawback – The big-government wing of the Kansas Republican Party joined forces with Democrats to undo a significant portion of the Brownback tax cuts. Since this was really a fight over whether there would be spending restraint or business-as-usual in Kansas, this was a double defeat.

Failure to control spending – I pointed out early in the year that it would be easy to cut taxes, control spending, and balance the budget. And I did the same thing late in the year. Unfortunately, there is no desire in Washington to restrain the growth of Leviathan. Sooner or later, this is going to generate very bad economic and political developments.

Venezuela’s tyrannical regime is still standing – Since I had hoped the awful socialist government would collapse, the fact that nothing has changed in Venezuela counts as bad news. Actually, some things have changed. The economy is getting worse and worse.

First, it is very bureaucratic and inefficient to use insurance for routine medical expenses. Sort of like using auto insurance to cover the cost of getting an oil change.

Second, insurance coverage means third-party payer, which means birth control will become more expensive(albeit financed by premiums rather than out of pocket).

Fifth, if politicians and bureaucrats really want birth control to be more affordable, they would make the pill available over the counter instead of requiring a prescription.

President Trump recently announced that his Administration would relax the mandate. I think that is good news for the above reasons.

Critics are very upset. But rather than argue about the desirability of insurance coverage and the wisdom of Washington mandates, they’re actually claiming that the White House has launched some sort of war on birth control. I’m not joking.

Jeff Jacoby of the Boston Globeanalyzes the issue. He starts by observing that nobody is proposing to ban birth control

…the Supreme Court ruled, in Griswold v. Connecticut, that government may not ban anyone from using contraceptives. …That freedom is a matter of settled law, and hasn’t been challenged in the slightest by President Trump or his administration.

He then points out that some folks on the left have gone ballistic.

Hillary Clinton accused Trump of showing “blatant disregard for medicine, science, & every woman’s right to make her own health decisions.” Elizabeth Warren, denouncing “this attack on basic health care,” claimed that the GOP’s top priority is to deprive women of birth control.

Their arguments, however, are utter nonsense. If Person A no longer has to subsidize Person B, that doesn’t mean Person B can’t buy things. It simply means there won’t be third-party payer.

Jacoby agrees.

News flash to Warren, et al.: There is no attack on health care, and no in America is being deprived of birth control. You are losing nothing but the power to force nuns to pay for your oral contraceptives. …As a matter of economics and public policy, the Affordable Care Act mandate that birth control be supplied for free is absurd. …Especially since birth control will remain as available and affordable as ever.

Indeed, the Trump Administration was actually far too timid. There should be no birth-control mandate for any insurance plan. It should be something negotiated by employers and employees.

…the new White House rule leaves the birth-control mandate in place. Trump’s “tweak won’t affect 99.9 percent of women,” observes the Wall Street Journal, “and that number could probably have a few more 9s at the end.” Washington will continue to compel virtually every employer and insurer in America to supply birth control to any woman who wants one at no out-of-pocket cost.

Jacoby closes his column with some very sensible observations and recommendations.

…there is no legitimate rationale for such a mandate. Americans don’t expect to get aspirin, bandages, or cold medicine — or condoms — for free; by what logic should birth control pills or diaphragms be handed over at no cost? …By and large, birth control is inexpensive; as little as $20 a month without insurance. …access to birth control, as the Centers for Disease Control reported in 2010, was virtually universal before Obamacare. The White House is right to end the burden on religious objectors. But it is the birth-control mandate itself that should be scrapped. Contraception is legal, cheap, and available everywhere. Why are the feds meddling where they aren’t needed?

The last sentence is key. The federal government (heck, no level of government) should be involved with birth control. They shouldn’t ban it. And they shouldn’t mandate it, either.

P.S. About five years ago, Sandra Fluke got her 15 minutes of fame by asserting that she had a right to third-party-financed birth control. That led to some clever jokes, including this cartoon and this video.

For what it’s worth, I think this cartoon is the best summary of the issue.

P.P.S. Predictably, the United Nations supports a “right” to taxpayer-financed birth control.

Right after Obamacare was enacted in 2010, I wrote a column suggesting four principles that should guide and motivate supporters of free markets and limited government.

As part of that article, I pointed out that Obamacare wasn’t a dramatic change. Instead, it was just another layer of government imposed on a health system that already was burdened by a huge amount of intervention.

The way to think of Obamacare is that we are shifting from a healthcare system 68 percent controlled/directed by government to one that…is 79 percent controlled/directed by government. Those numbers are just vague estimates, to be sure, but they underscore why Obamacare is just a continuation of a terrible trend, not a profound paradigm shift.

Later that year, the Center for Freedom and Prosperity released a video that elaborated, pointing out that Obamacare simply made a system dominated by government into a system even more controlled by government.

With predictable bad results.

That video included two charts based on my back-of-the envelope calculation, and I shared them in a 2013 column that further discussed the incremental damage of Obamacare.

Our healthcare system as a mess before Obamacare. Normal market forces were crippled by government programs such as Medicare and Medicaid and also undermined by government intervention in the tax code that resulted in pervasive over-insurance that exacerbated the third-party payer problem. These various forms of intervention led to all sorts of problems, such as rising prices and indecipherable complexity…Obamacare was enacted in 2010, and it was perceived to be a paradigm-shifting change in the healthcare system, even though it was just another layer of bad policy on top of lots of other bad policy. …Not surprisingly, all of the same problems still exist, but now they’re exacerbated by the mistakes in Obamacare.

In other words, we’re not going to fix the healthcare system by merely repealing Obamacare.

Yes, that’s a necessary step, but much more needs to happen.

Which is why I’m very happy that Prager University has a new video pointing out that health insurance doesn’t work nearly as well as car insurance and homeowners insurance. Why? Because it’s become an inefficient form of pre-paid health care rather than protection against large and unexpected expenses.

Though I wish the video went even further by explaining how the healthcare exclusion in the tax code encourages over-insurance.

And here’s a video from the Foundation for Economic Education that also explains how government intervention is distorting the health market.

Here’s the most important factoid from the video, which comes from the accompanying FEE article.

According to the Consumer Price Index and Medical-care price index from 1935 to 2009, the health care spending crisis didn’t start until the mid 1960s, around the same time when Medicare and Medicaid were signed into law, and at the same time that we began requiring doctors to go through all sorts of expensive licensing procedures beyond medical school. Since then, health care spending has doubled, even adjusted for inflation.

But let’s keep everything in perspective. Our system is needlessly expensive and inefficient because of government, but it still manages to deliver some decent outcomes.

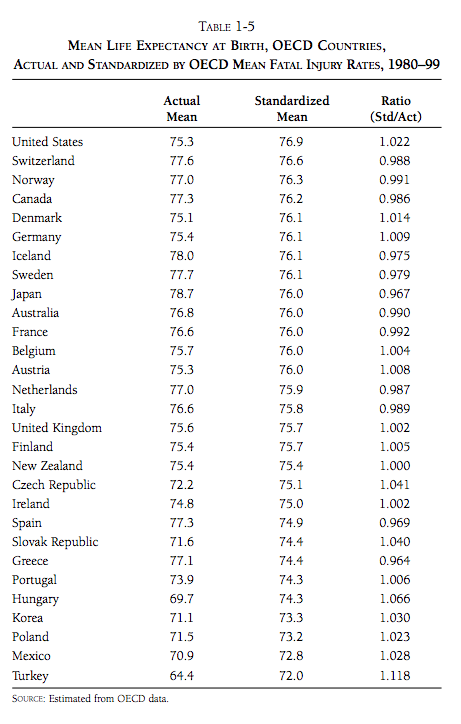

US healthcare is famous for…poor outcomes. …their overall outcome on the most important variable—overall life expectancy—is fairly poor.

I get this factoid thrown in my face repeatedly when speaking overseas, so I was delighted to find out that it has nothing to do with the quality of our healthcare.

…consider the main two ingredients that go into health outcomes. One is health, and the other is treatment. If latent health is the same across the Western world, we can presume that any differences come from differences in treatment. But this is simply not the case. Obesity is far higher in the USA than in any other major developed country. Obviously it is a public health problem, but it’s unrealistic to blame it on the US system of paying for doctors, administrators, hospitals, equipment and drugs. In fact in the US case it’s not even obesity, or indeed their greater pre-existing disease burden, that is doing most of the work in dragging their life expectancy down; it’s accidental and violent deaths. It is tragic that the US is so dangerous, but it’s not the fault of the healthcare system; indeed, it’s an extra burden that US healthcare spending must bear.

Indeed, it turns out that the American system produces very good results on life expectancy once you adjust for these behavioral factors.

…simply normalising for violent and accidental death puts the USA right to the top of the life expectancy rankings.

And here’s the relevant chart from the article.

By the way, health spending in the United States would probably be high compared to other nations even if we removed all government intervention and changed our risky behaviors.

But only because richer nations can afford – even demand – new technology, cutting-edge research, and new treatments. In his Bloombergcolumn, Professor Tyler Cowen discusses some of these factors

…viewed through the lens of consumption behavior, American health-care spending is typical of this nation’s habits and mores. Relative to GDP, Americans consume a lot more than Europeans, and our health-care spending is another example of that tendency. …Consumption in the U.S., per capita, measures about 50 percent higher than in the European Union. American individuals command more resources than people in countries such as Norway or Luxembourg, which have higher per capita GDP. The same American consumption advantage is evident if you look at dwelling space per person or the number of appliances in a typical home. …To put it most simply, we Americans spend a lot on health care because we spend a lot period.

Tyler includes a graph mapping healthcare expenditures with overall consumption. The basic takeaway is that what makes America an outlier is our ability to consume, with healthcare being an example.

So what’s all this mean for policy?

Peter Suderman offers some very sage advice in a column for the New York Times.

…when it comes to health care, Republicans don’t know what they want, much less how to get it. …Democrats, on the other hand, share a distinct vision of robust universal coverage guaranteed by the government and paid for by a combination of delivery-system efficiencies and higher taxes. What Republicans need, then, is a set of guiding principles — a health care vision that should work from the ground up, that imagines a more affordable and more effective system.

Peter then suggests some principles.

…it would mean giving up on comprehensive universal coverage. Otherwise, Republicans will just end up bargaining on the terms set by Democrats, as they are now. …a second principle: unification, not fragmentation. …employer-provided coverage…is subsidized implicitly through the tax code, which does not tax health benefits provided by employers as income. This tax break is the original sin of the United States health care system. Worth more than $250 billion annually, it has enormously distorted the market, creating an incentive for employers to provide ever-more-generous insurance while insulating individuals from the true cost of care. …the third principle comes in: Health coverage is not the same as health care. Instead, it is a financial product, a backstop against financial ruin. Health care policy should treat it as one. …For noncatastrophic, nonemergency medical expenses, Republicans ought to promote affordability rather than subsidies. …encourage supply-side innovations in addition to demand-side reforms. The tangle of regulations governing health care can make it difficult for providers to respond to market signals and innovate. Doctor-owned hospitals are restricted by law, for example, and certificate-of-need requirements force medical providers to obtain licenses in a process that effectively requires them to ask permission from competitors to expand.

In other words, we wind up this column where we started.

Americans get good health care, but it’s needlessly expensive and inefficient as I explained in Part I and Part II of a recent series. If we can somehow unravel, or even bypass, all the bad government policy that currently exists, we could have a much better system.

How much better? Well, check out this Reason video on a free-market health center in Oklahoma, which recently was featured in a story in Time. Based on my personal experiences, that’s a big step in the right direction.

In the eight years of writing this column, I’ve periodically confessed to certain fantasies. But you’ll notice that these fantasies don’t involve supermodels from Victoria’s Secret (though they did make a cameo appearance in one column).

Instead, either because I’m getting old or because I’m a dorky libertarian, my fantasies involve public policy. Here are imaginary things that have caused my pulse to quicken.

Trump…can restore the Constitution’s limits on executive power, provide relief to Americans suffering under Obamacare, and hasten repeal.

Michael has a 14-point list, but here are the ones that matter for our purposes today.

First, put pressure on Congress.

1. End Congress’s illegal Obamacare exemption. Obamacare threw members of Congress and congressional staff out of their health plans and in effect cut their pay by up to $12,000 per year. Obama ignored the law and made illegal payments to private insurance companies on behalf of members of Congress and their staff for six years — all to prevent Congress from reopening the law. Trump should announce that he will end those illegal payments immediately, and that he will veto any bill restoring the pay cut that Obamacare dealt Congress, until Congress earns that money by repealing and replacing the law. Congress shouldn’t get an exemption from Obamacare until the American people do. Democrats who actually voted for Obamacare especially should have to live under it.

Second, put pressure on insurance companies.

2. End Obamacare’s unconstitutional cost-sharing subsidies. In House v. Burwell, a federal judge ruled that the Obama administration “violate[d] the Constitution” by paying billions of dollars in “cost-sharing” subsidies to private insurance companies without a congressional appropriation. Trump should immediately drop the Obama administration’s appeal of that decision, stop the unconstitutional payments, and prevent insurers from canceling Obamacare plans until 2018.

3. End Obamacare’s illegal “reinsurance” payments. The Government Accountability Office found that the Obama administration illegally diverted additional billions of dollars in “reinsurance” payments from the Treasury to private insurance companies. Trump should immediately stop the diversion of those funds and demand that insurers repay the more than $3 billion in unlawful payments they have received.

4. Block Big Insurance’s “risk-corridor” raid on the Treasury. The Obama administration tried to circumvent a statutory cap on “risk-corridor” payments to private insurance companies by offering to settle lawsuits filed by the insurers. Trump should immediately announce that his administration will not settle but will instead vigorously defend taxpayers’ interests in all such lawsuits.

Needless to say, the combination of angst-ridden folks on Capitol Hill and angst-ridden bigwigs from insurance companies would probably be more than enough to get weak-kneed Republicans to climb on board for repeal.

Indeed, in my fantasy, Trump uses his bully pulpit (and Twitter account) to specifically pressure those callow Republicans who voted for major repeal in 2015 and then flip-flopped and voted against various (usually partial) repeal proposals earlier this month.

Various media sources certainly agree that Trump has a huge amount of leverage.