Given Social Security’s enormous long-run financial problems, the program eventually will need reform.

But what should be done? Some folks on the left, such as Barack Obama and Hillary Clinton, support huge tax increases to prop up the program.  Such an approach would have a very negative impact on the economy and, because of built-in demographic changes, would merely delay the program’s bankruptcy.

Such an approach would have a very negative impact on the economy and, because of built-in demographic changes, would merely delay the program’s bankruptcy.

Others want a combination of tax increases and benefit cuts. This pay-more-get-less approach is somewhat more rational, but it means that today’s workers would get a really bad deal from Social Security.

This is why I frequently point out that personal retirement accounts (i.e., a “funded” system based on real savings) are the best long-run solution. And to help the crowd in Washington understand why this is the best approach, I explain that dozens of nations already have adopted this type of reform. And I’ve written about the good results in some of these jurisdictions.

Now it’s time to add Sweden to the list.

I actually first wrote about the Swedish reform almost 20 years ago, in a study for the Heritage Foundation co-authored with an expert from Sweden. Here’s some of what we said about the nation’s partial privatization.

Swedish policymakers decided that both individual workers and the overall economy would benefit if the old-age system were partially privatized. …Workers can invest 2.5 percentage points of the 18.5 percent of their income that they must set aside for retirement.

…the larger part-16 percent of payroll-goes to the government portion of the program. …What makes the government pay-as-you-go portion of the pension program unique, however, is the formula used for calculating an individual’s future retirement benefits. Each worker’s 16 percent payroll tax is credited to an individual account, although the accounts are notional. …the government uses the money in these notional accounts to calculate an annuity (annual retirement benefit) for the worker. …the longer a worker stays in the workforce, the larger the annuity received. This reform is expected to discourage workers from retiring early… There are many benefits to Sweden’s new system, including greater incentives to work, increased national savings, a flexible retirement age, lower taxes and less government spending.

While that study holds up very well, let’s look at more recent research so we can see how the Swedish system has performed.

I’m a big fan of the fully privatized portion of the Swedish system (the “premium pension”) funded by the 2.5 percent of payroll that goes to personal accounts.

But let’s first highlight the very good reform of the government’s portion of the retirement system. It’s still a tax-and-transfer scheme, but there are “notional” accounts, which means that benefits for retirees are now tied to how much they work and how much they pay into the system.

A new study for the American Enterprise Institute, authored by James Capretta, explains the benefits of this approach.

Sweden enacted a reform of its public pension system that combines a defined-contribution approach with a traditional pay-as-you-go financing structure. The new system includes better work incentives and is more transparent to participants. It is also permanently solvent

due to provisions that automatically adjust payouts based on shifting demographic and economic factors. …A primary objective…in Sweden was to build a new system that would be solvent permanently within a fixed overall contribution rate. …pension benefits are calculated based on notional accounts, which are credited with 16.0 percent of workers’ creditable wages. …The pensions workers get in retirement are tied directly to the amount of contributions they make to the system. …This design improved incentives for work… To keep the system in balance, this rate of return is subject to adjustment, to correct for shifts in demographic and economic factors that affect what rate of return can be paid within the fixed budget constraint of a 16.0 percent contribution rate.

The final part of the above excerpts is key. The system automatically adjusts, thus presumably averting the danger of future tax hikes.

Now let’s look at some background on the privatized portion of the new system. Here’s a good explanation in a working paper from the Center for Fiscal Studies at Sweden’s Uppsala University.

The Premium Pension was created mainly for three purposes. Firstly, funded individual accounts were believed to increase overall savings in Sweden. …Secondly, the policy makers wanted to allow participants to take account of the higher return in the capital markets as well asto tailor part of their pension to their risk preferences. Finally, an FDC scheme is inherently immune against financial instability, as an individual’s pension benefit is directly financed by her past accumulated contributions. The first investment selections in the Premium Pension plan took place in the fall of 2000, which is known as the “Big Bang” in Sweden’s financial sector. …any fund company licensed to do business in Sweden is allowed to participate in the system, but must first sign a contract with the Swedish Pensions Agency that specifies reporting requirements and the fee structure. Benefits in the Premium Pension Plan are paid out annually and can be withdrawn from age 61.

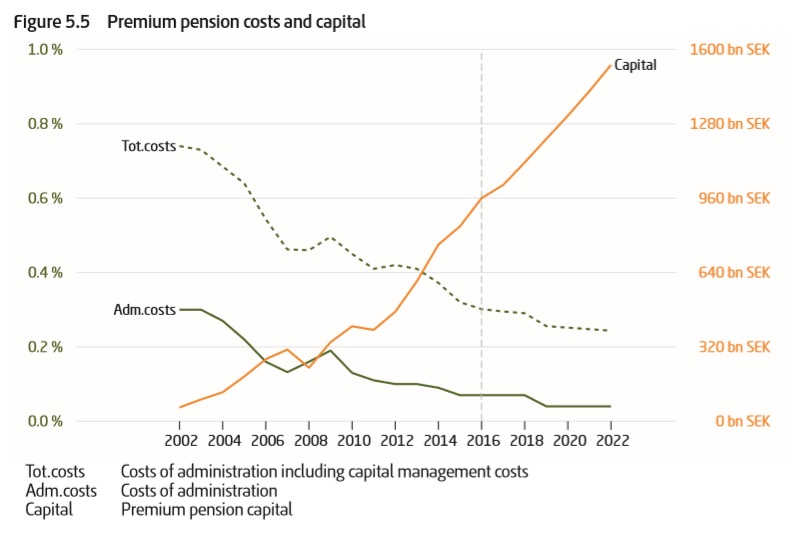

And here’s a chart from the Swedish Pension Agency’s annual report showing that pension assets are growing rapidly (right axis), in part because “premium pension has provided a 6.7 percent average value increase in people’s pensions per year since its launch.” Moreover, administrative costs (left axis) are continuously falling. Both trends are very good news for workers.

Let’s close by citing another passage from Capretta’s AEI study.

He looks at Sweden’s long-run fiscal outlook to other major European economies.

According to European Union projections, Sweden’s total public pension obligations will equal 7.5 percent of GDP in 2060, which is a substantial reduction from the…8.9 percent of GDP it spent in 2013. …In 2060, EU countries are expected to spend 11.2 percent of GDP on pensions. Germany’s public pension spending is projected to increase…to 12.7 percent of GDP in 2060. …The EU forecast shows France’s pension obligations will be 12.1 percent of GDP in 2060 and Italy’s will be 13.8 percent of GDP.

I think 8.9 percent of GDP is still far too high, but it’s better than diverting 11 percent, 12 percent, or 13 percent of economic output to pensions.

And the fiscal burden of Sweden’s system could fall even more if lawmakers allowed workers to shift a greater share of their payroll taxes to personal accounts.

But any journey begins with a first step. Sweden moved in the right direction. The United States could learn from that successful experience.

P.S. Pension reform is just the tip of the iceberg. As I wrote two years ago, Sweden has implemented a wide range of pro-market reforms over the past few decades, including some very impressive spending restraint in the 1990s. If you’re interested in more information about these changes, check out Lotta Moberg’s video and Johan Norberg’s video.

[…] Kong, Netherlands, the Faroe Islands, Denmark, Israel, and Sweden, all of which show that it is possible to fully or partially replace debt-based systems with […]

[…] Kong, Netherlands, the Faroe Islands, Denmark, Israel, and Sweden, all of which show that it is possible to fully or partially replace debt-based systems with […]

[…] Kong, Netherlands, the Faroe Islands, Denmark, Israel, and Sweden show that it is possible to fully or partially replace debt-based systems with savings-based […]

[…] P.S. If you are not Biden or Trump and want to do what’s best for America, I suggest learning about reforms in Australia, Chile, Switzerland, Hong Kong, Netherlands, the Faroe Islands, Denmark, Israel, and Sweden. […]

[…] P.S. The better option is a shift to retirement systems based on private savings, like the ones in Australia, Chile, Switzerland, Hong Kong, Netherlands, the Faroe Islands, Denmark, Israel, and Sweden. […]

[…] P.S. If you are not Biden or Trump and want to do what’s best for America, I suggest learning about reforms in Australia, Chile, Switzerland, Hong Kong, Netherlands, the Faroe Islands, Denmark, Israel, and Sweden. […]

[…] They can shift to retirement systems based on private savings, like Australia, Chile, Switzerland, Hong Kong, Netherlands, the Faroe Islands, Denmark, Israel, and Sweden. […]

[…] in 2018, I wrote about Sweden’s pension reforms, and I cited a study I co-authored back in 2000 for the Heritage […]

[…] P.S. If you are not Biden or Trump and want to do what’s best for America, I suggest learning about reforms in Australia, Chile, Switzerland, Hong Kong, Netherlands, the Faroe Islands, Denmark, Israel, and Sweden. […]

[…] P.S. If you are not Biden or Trump and want to do what’s best for America, I suggest learning about reforms in Australia, Chile, Switzerland, Hong Kong, Netherlands, the Faroe Islands, Denmark, Israel, and Sweden. […]

[…] P.S. If you are not Biden or Trump and want to do what’s best for America, I suggest learning about reforms in Australia, Chile, Switzerland, Hong Kong, Netherlands, the Faroe Islands, Denmark, Israel, and Sweden. […]

[…] P.S. If you are not Biden or Trump and want to do what’s best for America, I suggest learning about reforms in Australia, Chile, Switzerland, Hong Kong, Netherlands, the Faroe Islands, Denmark, Israel, and Sweden. […]

[…] P.S. Chile and Australia have created personal retirement accounts. You can also learn about reforms in Switzerland, Hong Kong, Netherlands, the Faroe Islands, Denmark, Israel, and Sweden. […]

[…] P.S. Chile and Australia have created personal retirement accounts. You can also learn about reforms in Switzerland, Hong Kong, Netherlands, the Faroe Islands, Denmark, Israel, and Sweden. […]

[…] is something that already exists to varying degrees in other European nations such as Switzerland, Sweden, Denmark, and the […]

[…] P.P.S. I mentioned that Chile and Australia have created personal retirement accounts. You can also learn about reforms in Switzerland, Hong Kong, Netherlands, the Faroe Islands, Denmark, Israel, and Sweden. […]

[…] P.P.S. I mentioned that Chile and Australia have created personal retirement accounts. You can also learn about reforms in Switzerland, Hong Kong, Netherlands, the Faroe Islands, Denmark, Israel, and Sweden. […]

[…] an ideal world, Americans would have personal retirement accounts, just like workers in Australia, Sweden, Chile, Hong Kong, Israel, Switzerland, and a few dozen other […]

[…] an ideal world, Americans would have personal retirement accounts, just like workers in Australia, Sweden, Chile, Hong Kong, Israel, Switzerland, and a few dozen other […]

[…] an ideal world, Americans would have personal retirement accounts, just like workers in Australia, Sweden, Chile, Hong Kong, Israel, Switzerland, and a few dozen other […]

[…] an ideal world, Americans would have personal retirement accounts, just like workers in Australia, Sweden, Chile, Hong Kong, Israel, Switzerland, and a few dozen other […]

[…] Sweden is a good case study for the benefits of Social Security privatization and the Laffer […]

[…] an ideal world, Americans would have personal retirement accounts, just like workers in Australia, Sweden, Chile, Hong Kong, Israel, Switzerland, and a few dozen other […]

[…] an ideal world, Americans would have personal retirement accounts, just like workers in Australia, Sweden, Chile, Hong Kong, Israel, Switzerland, and a few dozen other […]

[…] an ideal world, Americans would have personal retirement accounts, just like workers in Australia, Sweden, Chile, Hong Kong, Israel, Switzerland, and a few dozen other […]

[…] an ideal world, Americans would have personal retirement accounts, just like workers in Australia, Sweden, Chile, Hong Kong, Israel, Switzerland, and a few dozen other […]

[…] while Australia, Denmark, Chile, Switzerland, Hong Kong, Netherlands, Faroe Islands, and Sweden are a few of the many other jurisdictions that have fully or partially shifted to systems based […]

[…] while Australia, Denmark, Chile, Switzerland, Hong Kong, Netherlands, Faroe Islands, and Sweden are a few of the many other jurisdictions that have fully or partially shifted to systems based […]

[…] while Australia, Denmark, Chile, Switzerland, Hong Kong, Netherlands, Faroe Islands, and Sweden are a few of the many other jurisdictions that have fully or partially shifted to systems based […]

[…] By the way, Singapore is the role model for pre-funding, but many other nations have adopted that approach for retirement income (such as Israel, Denmark, Switzerland, Hong Kong, Netherlands, Faroe Islands, and Sweden). […]

[…] P.P.S. Shifting back to social security reform, here are some of the other nations (beside Israel, Chile, and Australia) that now benefit from private savings instead of empty political promises: Denmark, Switzerland, Hong Kong, Netherlands, Faroe Islands, and Sweden. […]

[…] the best option, Australia, Denmark, Chile, Switzerland, Hong Kong, Netherlands, Faroe Islands, and Sweden are a few of the many jurisdictions that have fully or partially shifted to systems based on real […]

[…] Sweden […]

[…] system, the Chilean system, the Hong Kong system, the Swiss system, the Dutch system, the Swedish system. Heck, I even like the system in the Faroe […]

[…] system, the Chilean system, the Hong Kong system, the Swiss system, the Dutch system, the Swedish system. Heck, I even like the system in the Faroe […]

[…] Sweden […]

[…] P.P.S. And we have specific data from Sweden showing how that nation lost ground after it adopted the big welfare state (and has subsequently gained ground thanks to pro-market reforms such as nationwide school choice and partial pension privatization). […]

[…] Sweden […]

“Sweden’s Push to Get Rid of Cash Has Some Saying, ‘Not So Fast’”

By Liz Alderman

Nov. 21, 2018

Cash is disappearing in the country faster than anyone thought it would. Now, officials are trying to slow its demise as they determine the societal costs.

[…] Sweden […]

[…] system, the Chilean system, the Hong Kong system, the Swiss system, the Dutch system, the Swedish system, or even the system in the Faroe […]

[…] system, the Chilean system, the Hong Kong system, the Swiss system, the Dutch system, the Swedish system, or even the system in the Faroe […]

[…] favorably about the Chilean system, the Hong Kong system, the Swiss system, the Dutch system, the Swedish system. Heck, I even like the system in the Faroe […]

I feel like if we did this in the U.S. that Democrats on TV (elected, pundits, and anchors) would demagogue the bleep out of it. It wouldn’t go anywhere because the ideologues (both idealistic and evil) would kill it.

and:

The Failure of the Swedish Establishment

by Nima Gholam Ali Pour

https://www.gatestoneinstitute.org/7860/sweden-establishment

what lessons can we learn?

‘Sweden: What You Won’t See in This Book…’

by Bruce Bawer

https://www.gatestoneinstitute.org/11035/last-night-sweden

I just wish the bastards would let me take care of my own retirement in my own way…. After paying into “there” retirement/ponzi scheme I’ve managed to buy and have now fully paid for 11 rental properties,,, they generate a lot better retirement than our SS system. And in the long run when SS goes under I’m going to be living way better than a lot of you depending on Uncle Sugar Santa.

And yes, I did it the hard way, 60hr weeks, leftovers for lunch, no dining out, no wasted money on smokes, booze, drugs, used cars, etc…

Bonus,, at 66 I’m super healthy, slim and trim, still working hard and looking at buying another property…

PS,,, anyone trusting government to take care of them is obviously delusional,,, meaning they have a mental defect!!!

Dan, you may wish to have a look at my infography about the Spanish Public Pensions system, https://wp.me/p4yd7V-iL and this two https://wp.me/p4yd7V-hf

These are all Sanders’ favorite nations for their welfare/social net programs. Yet he’s out here to give millions more to the SSA and not even acknowledge that there exists a problem with it (at least, not one that can’t be solved by just raising taxes on the rich…)

The best system would we to transfer what’s been paid into Social Security into an equity fund or mutual retirement account. If they followed the market, year-over-year returns could be as much as 3 times those earned now…

Only problem is, they don’t have that money on them. It’s all being invested in Treasuries or being paid out. That’s the problem with a pyramid scheme…

And two, it would be political suicide to “INVEST our RETIREMENT in WALLL STREEETTT!!!”

…even if it would make most people better off.

We know several ways to make social, security viable, and self-correcting politically and economically.. What we lack is the will. Kicking the can down the road is the preferred approach until what? The Greek/Venezuela reality – no funds/credit/growth with people leaving/starving/demonstrating. This is the modern model of the Great Depression. One not very clear, but rising in the horizon, is the subordination of the country to its debtors…e.g.,.the Chinese. They save, invest internationally, and convert their debtors into economic lackeys of consumption, that they “own.” There is a self-correcting, escalating mechanism used in the past….seizure, be it by mercantile trade, colonialism, or war…approximations or mirror images of useful slavery, isolation, and genocide. Unthinkingly, we are choosing extinction, and learning the love the bomb.