I’ve shared lots of analysis (both serious and satirical) about the mess in Greece and I feel obliged to comment on the latest agreement for another bailout.

But how many times can I write that the Greek government spends too much money and has a punitive tax system (and a crazy regulatory regime, a bloated bureaucracy, etc)?

So let’s try a different approach and tell a story about the new bailout by using some images.

Here’s an amusing perspective on what actually happened this weekend.

I explained a few days ago that the bailouts have simultaneously enabled the delay of much-needed spending reforms while also burdening Greece with an impossible pile of debt.

But the Greek bailouts, like the TARP bailout in the United States, were beneficial to powerful insiders.

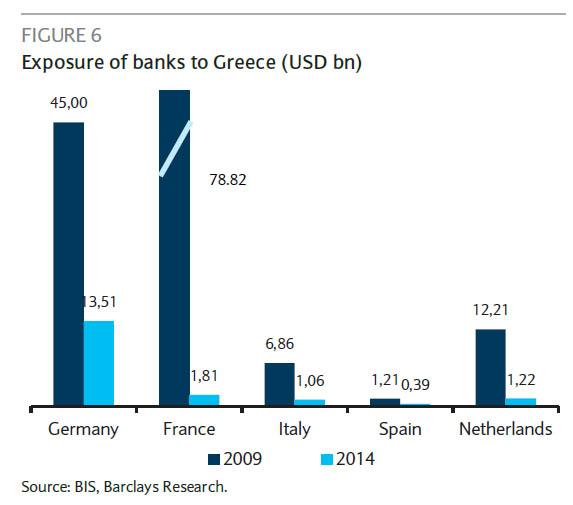

Here’s a look at how banks in various European nations have been able to reduce their exposure to Greek debt.

Sure, the banks almost surely still lost money, but they also transferred a lot of the losses to taxpayers.

To get a sense of the magnitude of handouts, here’s a chart from a Washington Post story.

And now, assuming the deal gets finalized, that pile of foolish and unsustainable debt will be even bigger.

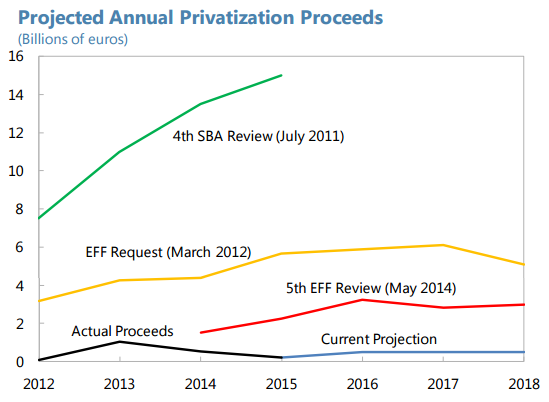

One of the main components of the new agreement is that Greece supposedly will raise revenue by selling $50 billion of state-owned assets.

Don’t believe that number. But not because there aren’t plenty of assets to sell, but rather because the track record on privatization proceeds suggests that there is a giant gap between what Greece promises and what Greece delivers.

To understand why assets aren’t being sold, just keep in mind that most of the assets are under the control of the government in order to provide unearned benefits to different interest groups.

If you’re an overpaid unionized worker at a government-owned port, for instance, the last thing you want is to have that port sold to a private investor who presumably would want to link pay to productivity.

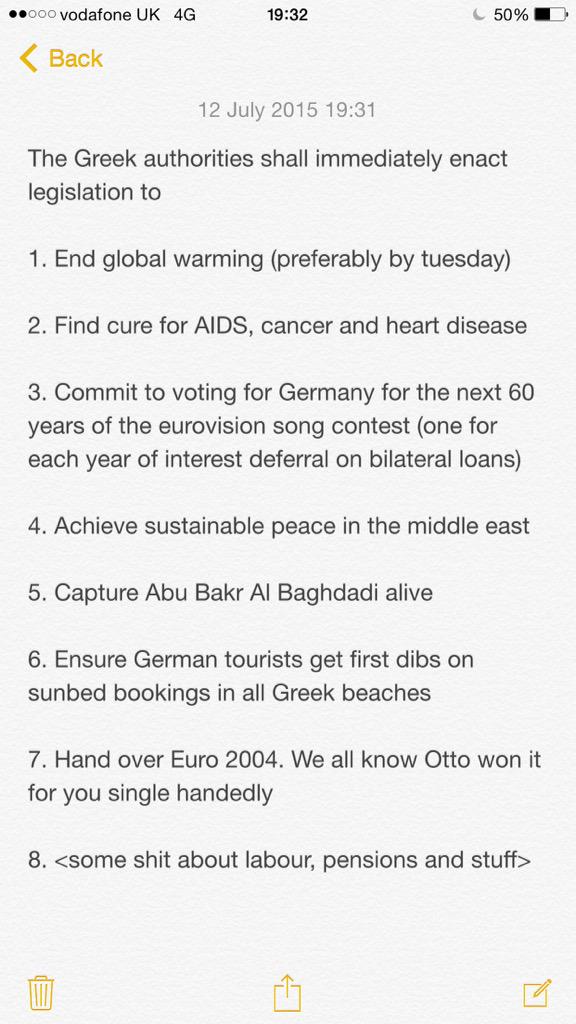

Here’s the best bit of humor I’ve seen about the negotiations this past weekend. It purports to show a list of demands from Germany to Greece.

While this image is funny, it’s also wrong.

Germany isn’t imposing anything on Greece. The Germans are simply stating that Greek politicians need to make some changes if they want more handouts.

Moreover, it’s quite likely that Germany will wind up being a big loser when the dust settles. Here’s some of what Gideon Rachman wrote for the U.K.-based Financial Times.

If anybody has capitulated, it is Germany. The German government has just agreed, in principle, to another multibillion-euro bailout of Greece — the third so far. In return, it has received promises of economic reform from a Greek government that makes it clear that it profoundly disagrees with everything that it has just agreed to. The Syriza government will clearly do all it can to thwart the deal it has just signed. If that is a German victory, I would hate to see a defeat.

So true.

I fear this deal will simply saddle Greece with a bigger pile of debt and set the stage for a more costly default in the future.

The title of this column is about pictures. But let’s close with some good and bad analysis about the Greek mess.

Writing for Real Clear Markets, Louis Woodhill has some of the best insight, starting with the fact that the bailout does two things.

First, this new bailout is largely just a mechanism to prevent default on past bailouts. Sort of like making a new loan to your deadbeat brother-in-law to cover what he owes you on previous loans.

…the €53.5 billion in new loans…would just be recycled to Greece’s creditors (the IMF, the EU, and the ECB) to pay the interest and principal on existing debts.

Second, it prevents the full meltdown of Greek banks.

The key point is that a bailout agreement would restore European Central Bank (ECB) “Emergency Liquidity Assistance” (ELA) to the Greek banking system. This would allow Greeks that still have deposits in Greek banks (€136.5 billion as of the end of May) to get their money out of those banks.

That’s good news if you’re a Greek depositor, but that’s about it.

In other words, those two “achievements” don’t solve the real problem of Greece trying to consume more than it produces.

Indeed, Woodhill correctly identifies a big reason to be very pessimist about the outcome of this latest agreement. Simply stated, Greek politicians (aided and abetted by the Troika) are pursuing the wrong kind of austerity.

…what is killing Greece is a lack of economic growth, and the meat of Tsipras’ bailout proposal consists of growth-killing tax hikes. The media and the economics profession have been framing the alternatives for Greece in terms of a choice between “austerity” and “stimulus.” Unfortunately for Greece, austerity has come to mean tax increases, and stimulus has come to mean using “other people’s money” (mainly that of German taxpayers) to support Greek welfare state outlays. So, if “other people” aren’t willing to fund more Greek government spending, then the only option the “experts” can imagine is to raise taxes on an economy that is already being crushed by excessive taxation.

Let’s close with the most ridiculous bit of analysis about the Greek situation. It’s from Joe Stiglitz,

Joseph Stiglitz accused Germany on Sunday of displaying a “lack of solidarity” with debt-laden Greece that has badly undermined the vision of Europe. …”Asking even more from Greece would be unconscionable. If the ECB allows Greek banks to open up and they renegotiate whatever agreement, then wounds can heal. But if they succeed in using this as a trick to get Greece out, I think the damage is going to be very very deep.”

Needless to say, I’m not sure why it’s “solidarity” for one nation to mooch in perpetuity from another nation. I suspect Stiglitz is mostly motivated by an ideological desire to redistribute from the richer Germans to the poorer Greeks,

But I’m more interested in why he isn’t showing “solidarity” to me. I’m sure both his income and his wealth are greater than mine. So if equality of outcomes is desirable, why doesn’t he put his money where his mouth is by sending me a big check?

Needless to say, I won’t be holding my breath waiting for the money. Like most leftists, Stiglitz likes to atone for his feelings of guilt by redistributing other people’s money.

And I also won’t be holding my breath waiting for a good outcome in Greece. As I wrote five-plus years ago, Greece needs the tough-love approach of no bailouts, which would mean a default but also an immediate requirement for a balanced budget.

Last but not least, I’m going to confess a possible mistake. I always thought that Margaret Thatcher was right when she warned that the problem with socialism is that you eventually run out of other people’s money. But this latest bailout of Greece shows that maybe politicians from other nations are foolish enough to provide an endless supply of other people’s money.

[…] did many European nations, most notablyGreece, suffer fiscal crises about a dozen years […]

[…] did many European nations, most notably Greece, suffer fiscal crises about a dozen years […]

[…] don’t like rewarding investors who make imprudent decisions, and it really galls me to bail out the (mostly) rich people who bought Greek […]

[…] simply note that there are many state-owned enterprises in Greece and the government has been dragging its feet about auctioning them to the private sector. So Greece is definitely closer to socialism than […]

[…] In the real world, though, I have zero faith in the first option and very little hope for the second option. Consider, for instance, the mess in Greece. For all intents and purposes, the European Commission took control of that nation’s fiscal policy almost 10 years ago. The results have not been pretty. […]

Fine analysis except for the sympathetic approach towards Germany. They did not bailout Greece with all these billions. Greece gets nothing out of this ‘help’ – this is just misleading propaganda because German politicians do not want to admit to their taxpayers that they bailed out their banks pretending that the billions -supposedly received by Greeks- would be paid back.

[…] For more information, here’s my five-picture explanation of the Greek […]

[…] (and a desire to bail out their big banks), instead decided to undermine the euro by creating a bigger mess in Greece and sending a very bad signal about bailouts to other welfare […]

[…] (and a desire to bail out their big banks), instead decided to undermine the euro by creating a bigger mess in Greece and sending a very bad signal about bailouts to other welfare […]

[…] state intervention. The government was supposed to engage in sweeping privatizations, but the gap between projections and performance is […]

[…] state intervention. The government was supposed to engage in sweeping privatizations, but the gap between projections and performance is […]

[…] For more information, here’s my five-picture explanation of the Greek […]

[…] States, and that turned out to be a corrupt mess. Second, we had the Greek bailout, which has squandered hundreds of billions of euros to prop up a welfare state. Now we have a third big bailout, with China seeking to stabilize that […]

[…] we had the Greek bailout, which has squandered hundreds of billions of euros to prop up a welfare […]

[…] understandable reasons, the fiscal mess in Greece has dominated the European economic […]

[…] understandable reasons, the fiscal mess in Greece has dominated the European economic headlines. But there are other developments that deserve […]

[…] understandable reasons, the fiscal mess in Greece has dominated the European economic […]

Greece should go to the US proposed Fairtax. It is simple and very easy to implement. The economy will explode. The only problem will be that the ruling political leaders will realize their days are number and they will lose power unless they adopt the Fairtax.

Mitchel: “maybe politicians from other nations are foolish enough to provide an endless supply of other people’s money.”

Governments are “stationary bandits” (Mancur Olson). All have discovered that delayed and hidden theft (debt) can supplement direct theft (taxes and fines). Within each country, debt is operated as a Ponzi scheme, with new debt paying the interest on the current debt.

The European Union is a collection of governments running individual Ponzi schemes, with the hope that monetary and political union will provide higher growth and greater control for the participating governments. They would like the prosperity of the US, to tax it, and are applying Cargo Cult reasoning: The US is a collection of states with much tax revenue, so we will become a collection of states, and therefore … more tax revenue.

The downside is that each EU country has to steal at the same rate, so as not to burden the others. But, Greece has broken through the limits.

The other EU governments want to keep the big Ponzi going along with their hopes for political greatness. Unfortunately, Greece is part of the group. The EU must prevent an idea from forming: Greece is much like us and part of the EU, so what prevents another EU country from failing like Greece? The EU will pay much to prevent the idea that Greece is the first sign of general rot, to keep the Ponzi going.

Socialist by night at the Greek “Taverna”, and inspired by the common good, …by day, …our poor port authority worker will hang on tooth and nail to his modest but unearned income. He will do anything short of picking up arms to defend his now entrenched mediocrity.

Ms Merkel has a formidable opponent in trying to get two years of free work from such s person, and the hundreds of millions like him.

She will face a pan-European revolt from the many port authority like majority of Europe, trying to impose modest market reforms on this strong majority. It’s too little too late, dear European-lemmings. The time to pick a different course has long passed. The path towards a welfare state cannot be regurgitated. Much pain and decline lies ahead before it finally hits bottom and finally implodes. We seem to still be some ways from that. The north still has some money left, but declining fast as even their growth rates cannot match half the world average.

American progressives must be biting their nails, lest their model continent goes visibly down before they have completed their HopNChange reforms.

Alas, they have won already. America has entered the death spiral. In 2008, under the problems brought on by statism, Americans elected the “remedy” of a statist on steroids. It was then that the vicious cycle closed. Europe entered this cycle in the early 70s. In America it seems to have finally achieved majoritarian support in 2008. But it won’t take fourth years for America to decline. In s way, it is already happening, as out baseline growth trendline seems to have already retreated, permanently.

It won’t be long before Americans start voting like Europeans. Already look at how little impact European events and destiny have on American political orientation.

On a personal note:

Observe, judge probabilities, and take personal action. Prepare your salvage boat now. Once the water reaches the decks, the exit chutes will be jammed. It does not matter that you were first to point out that the ship was sinking. The pitchforks will make you drown too, regardless.

Led by such economic freedom giants as France,… … Greece is poised to prosper enough to repay two entire years of GDP in loans…. …Loans made by a group of nations that are growing at one quarter the average world growth long term trendline.

so…

If all goes per German plan for Greece, in a few years Greece will have become France, or Belgium. Poised to repay a 170% of GDP loan.

Meanwhile :

European baseline structural growth trendline: ~1.5%

World average: 4%

Annual compounding growth deficit for European continent: ~2.5%

…a very fast convergence towards becoming a middle income continent.

Need I say anything more?

All Greeks can hope for is for the Brussels bureaucratic apparatus to slowly and meticulously come up with more permanent institutionalized north to south wealth transfers. That may give Greeks enough time for Europe’s overall growth deficit to compound, so that another crisis shifts focus from Greece to something bigger, like Italy, Spain or France.

But to the extent that Eurocrats manage to maintain Europe’s inevitable decline more orderly and steady, Greece will once again be the country in the limelight in a few years. The red herring of a fast declining continent.

My prediction:

Europe is in for more generalized turmoil.

Because in the grand scheme of things, decline will bring discord. It’s inevitable. People will look for scapegoat narratives.

Details:

In classic voter lemming suicide behavior, euro-lemming voters will attribute Europe’s inevitable low motivation welfare decline, to the modest pro-market reforms imposed by a now shaky German conservative minority.

That modestly pro-free economy northern minority has a slim margin in the Northern European countries themselves. The entire south of Europe including France are virtually all statist.

So the total voter tally in a Europe is:

Moderately pro market: around 70 million

Statists: 260 million

How long will this minority be able to hang on in a Europe that continues to unify (ironically with German support) and where sooner or later every European’s vote will count equally?

The modest overall concessions that Germany seems to have extracted from Greece are a Pyrrhic victory.

Europe continues its downward trajectory, as encapsulated by their growth trendline relative to world average.

The rest is details. Spicy ones, but details.

[…] By Dan Mitchell […]

If I understand correctly, the condition for the bailout (whatever you name it) is Greece turing over assets to Europe for privatization. Effectively, it strips a bit of sovereignity from Greece. As far as i know its a first time such a measure is taken. I am sure in case of Greece it will not be the last time. It does not make me happy but it confirms my analysis that the state of Greece has ceased to exist.

Dan Sir – good analysis but using language like this degrades the dialogue and runs counter to your goals which is to further understanding –

Thanks for the perspective – however –