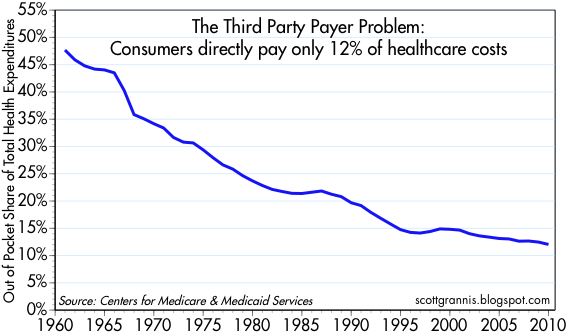

I’m going to add to that list today, but first let’s refresh our understanding of how government-caused “third-party payer” makes America’s health care system very expensive and inefficient.

The key insight is that consumers have little incentive to be smart shoppers when they perceive that other people are paying the bill. And health providers, needless to say, have little incentive to control costs when they know consumers care very little about prices.

Is this a big problem?

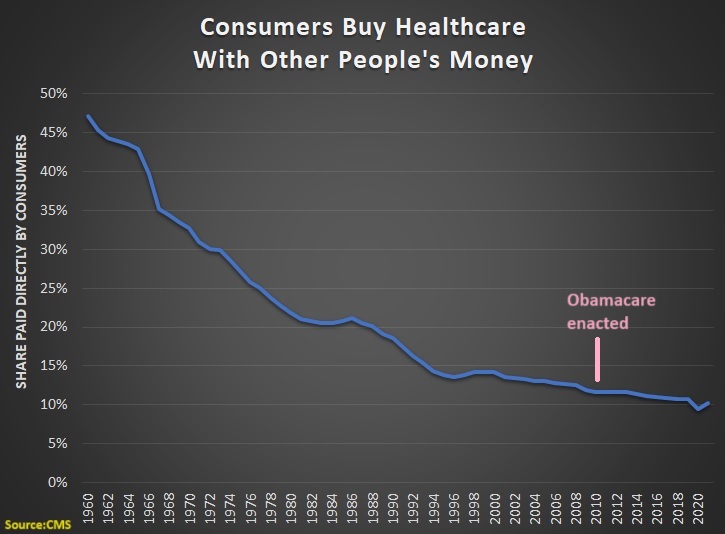

No, it is not a big problem. It is a giant problem. Here’s a chart, based on the federal government’s data, showing the share of health expenditures that are paid directly by consumers.

In the chart, I show the year that Obamacare was enacted. Notice that the legislation didn’t have an effect on the trendline, either the year it was enacted or in subsequent years as it was implemented.

And since Obamacare didn’t reduce the problem of third-party payer, one might guess that it didn’t solve the problem of rising health expenditures.

That guess would be correct, as shown in this column by Megan McArdle, which includes a predictably unsurprising headline.

…in 2022, the United States spent 16.6 percent of its gross domestic product on health care, while the next-highest spender, Germany, spent only 12.7 percent… As the Affordable Care Act took shape almost 15 years ago, its architects started looking for…savings… All these years later, we still haven’t found the magic money pot. …Obamacare contained a lot of elements that were expected to realize significant cost savings while actually improving the quality of care. …What this demonstrates is how hard it is to actually change the system in ways that generate major savings. …the wonks hunting for magic pots of money have mostly turned out to be chasing rainbows.

When I followed public policy in my younger days, I periodically would see stories about legislation that was approved by the House of Representatives with only one dissenting vote.

My memory isn’t perfect, I’m sure, but it seems that Ron Paul was always that lonely member. And my recollection is that he was (as usual) always on the correct side, voting for liberty and against government.

Something similar happened yesterday, except this time six members of Congress voted against a repeal of the “Cadillac Tax” that is part of Obamacare.

It was an eclectic group, but it included Justin Amash and Chip Roy, who are two of the most committed and principled supporters of free markets and limited government in Congress.

From the right, I recommend this analysis from Alan Viard at the American Enterprise Institute.

…employer-provided health insurance gets a big tax break. Workers pay income and payroll taxes on their cash wages, but not on their health insurance benefits. …the tax break is poorly targeted because it applies even to high-cost “Cadillac” health plans. The tax system should not artificially encourage Cadillac plans, which boost demand for medical services and drive up health care costs for everyone. Although the Cadillac tax does not directly change the tax break for high-cost employer plans, it offsets the break by imposing a separate 40 percent tax on those plans. That round-about approach is far from ideal, but it gets the job done. …the Cadillac tax has won support from economists across the ideological spectrum.

From the left, here’s some of what Bruce Bartlett wrote for the New York Times.

Although obviously a form of income to the worker, the Internal Revenue Service nevertheless ruled that it was not taxable, although businesses could still deduct the cost. This anomalous tax treatment was a fabulous tax loophole for both businesses and workers… Congress codified the I.R.S. ruling.. Various tax expenditures for health cost hundreds of billions of dollars in lost revenue per year, according to the Congressional Research Service. Eliminating them could finance a significant reduction in tax rates. …If the Republicans are serious about using tax reform to improve the competitiveness of American businesses, the best thing they can do is reform employer-based health insurance.

For honest folks on the left, they should be motivated by the fact that this exclusion overwhelmingly benefits upper-income taxpayers.

I very much suspect Obama partisans and Trump partisans won’t like this column, but the sad reality is that both Obamacare and Trump’s protectionism have a lot in common.

In both cases, government is limiting the freedom of buyers and sellers to engage in unfettered exchange.

In both cases, the fiscal burden of government increases.

In both cases, politicians misuse statistics to expand the size and scope of government.

Today, let’s add another item to that list.

In both cases, the Washington swamp wins thanks to increased cronyism and corruption.

To see what I mean, let’s travel back in time to 2011. I wrote a column about Obamacare and cited some very persuasive arguments by Tim Carney that government-run healthcare (or, to be more accurate, expanded government control of healthcare) was creating a feeding frenzy for additional sleaze in Washington.

Congress imposes mandates on other entities, but gives bureaucrats the power to waive those mandates. To get such a waiver, you hire the people who used to administer or who helped craft the policies. So who’s the net winner? The politicians and bureaucrats who craft policies and wield power, because this combination of massive government power and wide bureaucratic discretion creates huge demand for revolving-door lobbyists.

I then pointed out that the sordid process of Obamacare waivers was eerily similar to a passage in Atlas Shrugged.

Wesley Mouch…issued another directive, which ruled that people could get their bonds “defrozen” upon a plea of “essential need”: the government would purchase the bonds, if it found proof of the need satisfactory. …One was not supposed to speak about the men who…possessed needs which, miraculously, made thirty-three frozen cents melt into a whole dollar, or about a new profession practiced by bright young boys just out of college, who called themselves “defreezers” and offered their services “to help you draft your application in the proper modern terms.” The boys had friends in Washington.

Well, the same thing is happening again. Only this time, as reported by the New York Times, protectionism is the policy that is creating opportunities for swamp creatures to line their pockets.

The Trump administration granted seven companies the first set of exclusions from its metal tariffs this week and rejected requests from 11 other companies, as the Commerce Department began slowly responding to the 20,000 applications that companies have filed for individual products. …several companies whose applications were denied faced objections from American steel makers. …companies that have applied for the exclusions criticized the exercise as both long and disorganized. “This is the most screwed-up process,” said Mark Mullen, president of Griggs Steel, a steel distributor in the Detroit area. “This is a disservice to our industry and the biggest insult to our intelligence that I have ever seen from the government.”

From an economic perspective, it certainly is true that this new system is “disorganized” and “a disservice” and an “insult to our intelligence.” Those same words could be used to describe the welfare state, the EEOC, farm subsidies, the tax code, and just about everything else the government does.

But there’s one group of people who are laughing all the way to the bank, The lobbyists, consultants, fixers, and other denizens of the swamp are getting rich. Whether they’re preparing the applications, lobbying for the applications, or lobbying against the applications, they are getting big paychecks.

And the longer this sordid protectionist process continues, we will see a repeat of what happened with Obamacare as senior-level people in government move through the revolving door so they can get lucrative contracts to help clients manipulate the system (yes, Republicans can be just as sleazy as Democrats).

First, it is very bureaucratic and inefficient to use insurance for routine medical expenses. Sort of like using auto insurance to cover the cost of getting an oil change.

Second, insurance coverage means third-party payer, which means birth control will become more expensive(albeit financed by premiums rather than out of pocket).

Fifth, if politicians and bureaucrats really want birth control to be more affordable, they would make the pill available over the counter instead of requiring a prescription.

President Trump recently announced that his Administration would relax the mandate. I think that is good news for the above reasons.

Critics are very upset. But rather than argue about the desirability of insurance coverage and the wisdom of Washington mandates, they’re actually claiming that the White House has launched some sort of war on birth control. I’m not joking.

Jeff Jacoby of the Boston Globeanalyzes the issue. He starts by observing that nobody is proposing to ban birth control

…the Supreme Court ruled, in Griswold v. Connecticut, that government may not ban anyone from using contraceptives. …That freedom is a matter of settled law, and hasn’t been challenged in the slightest by President Trump or his administration.

He then points out that some folks on the left have gone ballistic.

Hillary Clinton accused Trump of showing “blatant disregard for medicine, science, & every woman’s right to make her own health decisions.” Elizabeth Warren, denouncing “this attack on basic health care,” claimed that the GOP’s top priority is to deprive women of birth control.

Their arguments, however, are utter nonsense. If Person A no longer has to subsidize Person B, that doesn’t mean Person B can’t buy things. It simply means there won’t be third-party payer.

Jacoby agrees.

News flash to Warren, et al.: There is no attack on health care, and no in America is being deprived of birth control. You are losing nothing but the power to force nuns to pay for your oral contraceptives. …As a matter of economics and public policy, the Affordable Care Act mandate that birth control be supplied for free is absurd. …Especially since birth control will remain as available and affordable as ever.

Indeed, the Trump Administration was actually far too timid. There should be no birth-control mandate for any insurance plan. It should be something negotiated by employers and employees.

…the new White House rule leaves the birth-control mandate in place. Trump’s “tweak won’t affect 99.9 percent of women,” observes the Wall Street Journal, “and that number could probably have a few more 9s at the end.” Washington will continue to compel virtually every employer and insurer in America to supply birth control to any woman who wants one at no out-of-pocket cost.

Jacoby closes his column with some very sensible observations and recommendations.

…there is no legitimate rationale for such a mandate. Americans don’t expect to get aspirin, bandages, or cold medicine — or condoms — for free; by what logic should birth control pills or diaphragms be handed over at no cost? …By and large, birth control is inexpensive; as little as $20 a month without insurance. …access to birth control, as the Centers for Disease Control reported in 2010, was virtually universal before Obamacare. The White House is right to end the burden on religious objectors. But it is the birth-control mandate itself that should be scrapped. Contraception is legal, cheap, and available everywhere. Why are the feds meddling where they aren’t needed?

The last sentence is key. The federal government (heck, no level of government) should be involved with birth control. They shouldn’t ban it. And they shouldn’t mandate it, either.

P.S. About five years ago, Sandra Fluke got her 15 minutes of fame by asserting that she had a right to third-party-financed birth control. That led to some clever jokes, including this cartoon and this video.

For what it’s worth, I think this cartoon is the best summary of the issue.

P.P.S. Predictably, the United Nations supports a “right” to taxpayer-financed birth control.

In the eight years of writing this column, I’ve periodically confessed to certain fantasies. But you’ll notice that these fantasies don’t involve supermodels from Victoria’s Secret (though they did make a cameo appearance in one column).

Instead, either because I’m getting old or because I’m a dorky libertarian, my fantasies involve public policy. Here are imaginary things that have caused my pulse to quicken.

Trump…can restore the Constitution’s limits on executive power, provide relief to Americans suffering under Obamacare, and hasten repeal.

Michael has a 14-point list, but here are the ones that matter for our purposes today.

First, put pressure on Congress.

1. End Congress’s illegal Obamacare exemption. Obamacare threw members of Congress and congressional staff out of their health plans and in effect cut their pay by up to $12,000 per year. Obama ignored the law and made illegal payments to private insurance companies on behalf of members of Congress and their staff for six years — all to prevent Congress from reopening the law. Trump should announce that he will end those illegal payments immediately, and that he will veto any bill restoring the pay cut that Obamacare dealt Congress, until Congress earns that money by repealing and replacing the law. Congress shouldn’t get an exemption from Obamacare until the American people do. Democrats who actually voted for Obamacare especially should have to live under it.

Second, put pressure on insurance companies.

2. End Obamacare’s unconstitutional cost-sharing subsidies. In House v. Burwell, a federal judge ruled that the Obama administration “violate[d] the Constitution” by paying billions of dollars in “cost-sharing” subsidies to private insurance companies without a congressional appropriation. Trump should immediately drop the Obama administration’s appeal of that decision, stop the unconstitutional payments, and prevent insurers from canceling Obamacare plans until 2018.

3. End Obamacare’s illegal “reinsurance” payments. The Government Accountability Office found that the Obama administration illegally diverted additional billions of dollars in “reinsurance” payments from the Treasury to private insurance companies. Trump should immediately stop the diversion of those funds and demand that insurers repay the more than $3 billion in unlawful payments they have received.

4. Block Big Insurance’s “risk-corridor” raid on the Treasury. The Obama administration tried to circumvent a statutory cap on “risk-corridor” payments to private insurance companies by offering to settle lawsuits filed by the insurers. Trump should immediately announce that his administration will not settle but will instead vigorously defend taxpayers’ interests in all such lawsuits.

Needless to say, the combination of angst-ridden folks on Capitol Hill and angst-ridden bigwigs from insurance companies would probably be more than enough to get weak-kneed Republicans to climb on board for repeal.

Indeed, in my fantasy, Trump uses his bully pulpit (and Twitter account) to specifically pressure those callow Republicans who voted for major repeal in 2015 and then flip-flopped and voted against various (usually partial) repeal proposals earlier this month.

Various media sources certainly agree that Trump has a huge amount of leverage.

Ending the CSR subsidies, paid monthly to insurers, is one way that Trump could hasten Obamacare’s demise without legislation, by prompting more companies to raise premiums in the individual market or stop offering coverage. …health-care analyst Spencer Perlman at Veda Partners LLC said in a research note that there’s a 30 percent chance Trump will end CSR payments, which may “immediately destabilize the exchanges, perhaps fatally.” …Many insurers have already dropped out of Obamacare markets in the face of mounting losses, and blamed the uncertainty over the future of the cost-sharing subsidies and the individual mandate as one of the reasons behind this year’s premium increases.

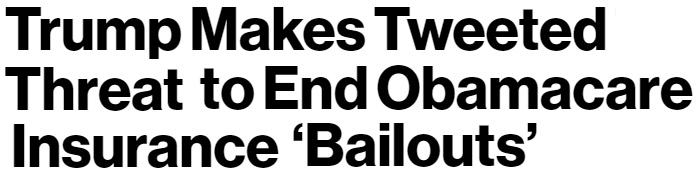

President Donald Trump announced on Saturday that if Congress doesn’t act soon on health care, he could end federal “BAILOUTS” for insurance companies, which could effectively force Congress to act or else put health insurance companies in the difficult position of having to raise rates on people who can’t afford to pay them or to leave Obamacare exchanges entirely. …The “BAILOUTS” to insurance companies Trump referred to in his tweet are “cost sharing reduction” payments… If Trump were to withhold these funds from health insurance companies, it would likely result in many insurers choosing to leave the Obamacare health insurance exchanges… If health insurance companies choose to leave the insurance exchanges, which is the most likely response, it could catalyze the collapse of the Obamacare exchange system, making it more difficult for members of Congress to wait on implementing a repeal and replace bill.

And here are passages from a Wall Street Journalstory.

President Donald Trump made one of his most explicit threats to cut off payments to insurance companies to force senators and lobbyists back to the bargaining table for a GOP health-care bill, and saying, for the first time, that he was also willing to cancel some of lawmakers’ health-care benefits. …Those payments have been challenged in court by House Republicans, who argue the funds were never authorized by Congress. A federal judge has sided with the House but allowed the payments to continue until the litigation concludes. Democrats have said that cutting off the payments would be tantamount to sabotaging the insurance markets… Mr. Trump’s Saturday tweet…also the first to mention that he was open to another idea proposed by conservative activists to pull lawmakers back to the task of a health-care bill: cutting off their existing health benefits. …some lawmakers contending that it is an end-run around a provision in the 2010 health law that requires members of Congress to get their health coverage like other Americans.

Keep in mind, by the way, that this isn’t just a matter of political brinksmanship. The various payments to insurance companies are either not authorized by the law, or they were authorized and Congress has declined to appropriate funds. In other words, these payments make a mockery of the rule of law. They are illegal and/or unconstitutional.

Moreover, my former Heritage colleague Mike Needham has a good explanation of how the Obama Administration preposterously decided to classify Congress as a small business in order to enable subsidies that were not part of the Obamacare legislation. Once again, throwing the rule of law overboard for political convenience (which was a pattern with the previous Administration).

So even if Trump didn’t want to get rid of Obamacare, these payments should end.

But we may as well make a policy virtue out of legal necessity by getting rid of these payments as part of a campaign to pressure Capitol Hill to do what’s right and get rid of the disastrous Obamacare legislation.

P.P.S. From the moment he emerged on the national stage, I’ve been worried that Donald Trump would preside over an expansion in the burden of government. But if there’s a libertarian bone in his body, it becomes apparent when he tweets. Not only did he tweet a very appropriate and effective threat against Obamacare yesterday, he also tweeted a very appropriate and effective threat about a government shutdown back in May.

P.P.S. It wasn’t one of my fantasies, but here’s something from 2013 about a libertarian fantasy dealing with ammo and sex.

Senate Republicans have produced their Obamacare repeal legislation, though as I noted at the end of this interview, it’s really more a bill about Medicaid reform than Obamacare repeal.

But critics are savaging this idea, implying that “deep cuts” will hurt the quality of care. Indeed, some of them are even engaging in poisonous rhetoric about people dying because of cutbacks.

There’s one small problem with the argument, however. Nobody is proposing to cut Medicaid. Republicans are merely proposing to limit annual spending increases. Yet this counts as a “cut” in the upside-down world of Washington budgeting.

The Washington Post contributes to innumeracy with a column explicitly designed to argue that the program is being cut.

…the Senate proposal includes significant cuts to Medicaid spending…the Senate bill is more reliant on Medicaid cuts than even the House bill…spending on the program would decline in 2026 by 26 percent…That’s a decrease of over $770 billion on Medicaid over the next 10 years. …By 2026, the federal government would cut 1 of every 4 dollars it spends on Medicaid.

An article in the New York Times has a remarkably inaccurate headline, which presumably isn’t the fault of reporters. Though the story has its share of dishonest rhetoric, especially in the first few paragraphs.

Senate Republicans…took a major step…, unveiling a bill to make deep cuts in Medicaid… The Senate measure…would also slice billions of dollars from Medicaid, a program that serves one in five Americans… The Senate bill would also cap overall federal spending on Medicaid: States would receive a per-beneficiary allotment of money. …State officials and health policy experts predict that many people would be dropped from Medicaid because states would not fill the fiscal hole left by the loss of federal money.

“Loss of federal money”?

I’d like to lose some money using that math. Here’s a chart showing the truth. The data come directly from the Congressional Budget Office.

At the risk of pointing out the obvious, it’s not a cut if spending rises from $393 billion to $464 billion.

Federal outlays on the program will climb by about 2 percent annually.

By the way, it’s perfectly fair for opponents to say that they want the program to grow faster in order to achieve different goals.

But they should be honest with numbers.

Now that we’ve addressed math, let’s close with a bit of policy.

The Wall Street Journal recently opined on the important goal of giving state policymakers the power and responsibility to manage the program. The bottom line is that recent waivers have been highly successful.

…center-right and even liberal states have spent more than a decade improving a program originally meant for poor women and children and the disabled. Even as ObamaCare changed Medicaid and exploded enrollment, these reforms are working… The modern era of Medicaid reform began in 2007, when Governor Mitch Daniels signed the Healthy Indiana Plan that introduced consumer-directed insurance options, including Health Savings Accounts (HSAs). Two years later, Rhode Island Governor Donald Carcieri applied for a Medicaid block grant that gives states a fixed sum of money in return for Washington’s regulatory forbearance. Both programs were designed to improve the incentives to manage costs and increase upward mobility so fewer people need Medicaid. Over the first three years, the Rhode Island waiver saved some $100 million in local funds and overall spending fell about $3 billion below the $12 billion cap. The fixed federal spending limit encouraged the state to innovate, such as reducing hospital admissions for chronic diseases or transitioning the frail elderly to community care from nursing homes. The waiver has continued to pay dividends under Democratic Governor Gina Raimondo. …This reform honor roll could continue: the 21 states that have moved more than 75% of all beneficiaries to managed care, Colorado’s pediatric “medical homes” program, Texas’s Medicaid waiver to devolve control to localities from the Austin bureaucracy.

By contrast, the current system is not successful.

Avik Roy explained this perverse result in Forbes back in 2013.

Piles of studies have shown that people on Medicaid have health outcomes that are no better, and often worse, than those with no insurance at all. …authors of the Oregon study published their updated, two-year results, finding that Medicaid “generated no significant improvement in measured physical health outcomes.” The result calls into question the $450 billion a year we spend on Medicaid… And all of that, despite the fact that the study had many biasing factors working in Medicaid’s favor: most notably, the fact that Oregon’s Medicaid program pays doctors better; and also that the Medicaid enrollees were sicker, and therefore more likely to benefit from medical care than the control arm.

In other words, I was understating things when I wrote above that there was “one small problem” with the left’s assertion about Medicaid cuts hurting people.

Yes, the fact that there are no actual cuts is a problem with that argument. But the second problem with the left’s argument is that Medicaid doesn’t seem to have any effect on health outcomes. So if Republicans actually did cut the program, it’s unclear how anybody would suffer (other than the fraudsters who bilk the program).

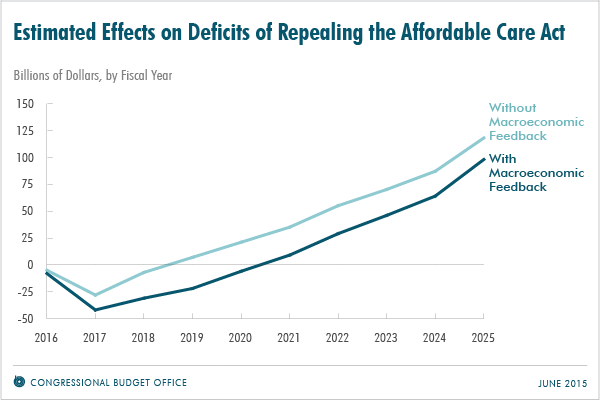

Back in 2015, I basically applauded the Congressional Budget Office for its analysis of what would happen if Obamacare was repealed. The agency’s number crunchers didn’t get it exactly right, but they actually took important steps and produced numbers showing how the law was hurting taxpayers and the economy.

Now we have a new set of Obamacare numbers from CBO based on the partial repeal bill approved by the House of Representatives. The good news is that the bureaucrats show substantial fiscal benefits. There would be a significant reduction in the burden of spending and taxation.

But the CBO did not show very favorable numbers in other areas, most notably when it said that 23 million additional people would be uninsured if the legislation was enacted.

Part of the problem is that Republicans aren’t actually repealing Obamacare. Many of the regulations that drive up the cost of health insurance are left in place.

My colleague at Cato, Michael Cannon, explains why this is a big mistake.

Rather than do what their supporters sent them to Washington to do – repeal ObamaCare and replace it with free-market reforms – House Republicans are pushing a bill that will increase health-insurance premiums, make health insurance worse for the sick… ObamaCare’s core provisions are the “community rating” price controls and other regulations that (supposedly) end discrimination against patients with preexisting conditions. …Community rating is the reason former president Bill Clinton called ObamaCare “the craziest thing in the world” where Americans “wind up with their premiums doubled and their coverage cut in half.” Community rating is why women age 55 to 64 have seen the highest premium increases under ObamaCare. It is the principal reason ObamaCare has caused overall premiums to double in just four years. Community rating literally penalizes quality coverage for the sick… ObamaCare is community rating. The AHCA does not repeal community rating. Therefore, the AHCA does not repeal ObamaCare.

It would be ideal if Republicans fully repealed Obamacare.

But maybe that’s hoping for too much since many Republicans are squeamish about supporting even a watered-down proposal to modify Obamacare.

That being said, there are some reasonable complaints that CBO overstated the impact of the GOP bill.

Doug Badger and Grace Marie Turner, for instance, were not impressed by CBO’s methodology.

The Congressional Budget Office (CBO) launched its latest mistaken Obamacare-related estimate this week, predicting that a House-passed bill to repeal and replace the embattled law would lead to 23 million more uninsured people by 2026. …the agency’s errors are not only massive – one of their predictions of 2016 exchange-based enrollment missed by 140%… Undaunted by failure and unschooled by experience, CBO soldiers on, fearlessly predicting that millions will flock to the exchanges any day now. …CBO measures the House-passed bill against this imaginary baseline and finds it wanting. …One reason CBO gets it so wrong so consistently is its fervent belief that the individual mandate has motivated millions to enroll in coverage. …CBO’s belief in the power of the individual mandate is misplaced. …The IRS reports that in the 2015 tax year, 6.5 million uninsured filers paid the tax penalty, 12.7 million got an exemption and additional 4.2 million people simply ignored the penalty. They left line 61 on their form 1040 blank, refusing to tell the government whether or not they had insurance. …In all, that is a total of 23.4 million uninsured people – out of an estimated 28.8 million uninsured – who either paid, avoided or ignored the penalty. That hardly suggests that the mandate has worked.

The Wall Street Journal also was quite critical of the CBO analysis.

…the budget scorekeepers claim the House bill could degrade the quality of insurance. This editorializing could use some scrutiny. Without government supervision of insurance minutiae and a mandate to buy coverage or pay a penalty, CBO asserts, “a few million” people will turn to insurance that falls short of the “widely accepted definition” of “a comprehensive major medical policy.” They might select certain forms of coverage that Obama Care banned, like “mini-med” plans with low costs and low benefits. Or they might select indemnity plans that pay a fixed-dollar amount per day for illness or hospitalization, or dental-only or vision-only single-service plans. CBO decided to classify these people as “uninsured,” though without identifying who accepts ObamaCare’s definition of standardized health benefits and why they deserve to substitute their judgment for the choices of individual consumers. …But the strangest part of CBO’s preoccupation with “high-cost medical events” is that the analysts never once mention catastrophic coverage—not once. These types of plans didn’t cover routine medical expenses but they did protect consumers against, well, a high-cost medical event like an accident or the diagnosis of a serious illness. Those plans answered what most people want most out of insurance—financial security and a guarantee that they won’t be bankrupted by cancer or a distracted bus driver. …under the House reform Americans won’t have any problem insuring against a bad health event, even if CBO won’t admit it. …CBO has become a fear factory because it prefers having government decide for everybody.

Drawing on his first-hand knowledge, Dr. Marc Siegel wrote on the issue for Fox News.

…23 million…will lose their health insurance by 2026 if the American Health Care Act, the bill the House passed to replace ObamaCare, is passed in the Senate and signed by President Trump. This number is concerning — until you look at it and the CBO’s handling of the health care bills more closely. …First, the CBO was wildly inaccurate when it came to ObamaCare, predicting that 23 million people would be getting policies via the exchanges by 2016. The actual number ended up being only 10.4 million… Second, many who chose to buy insurance on the exchanges did so only because they wanted to avoid paying the penalty, not because they needed or wanted the insurance. Many didn’t buy insurance until they got sick.

IN the real world, people who don’t have insurance coverage cannot lose it. Yet…the CBO estimates 14 million fewer people will have coverage in 2018 if the House bill is enacted than would be the case if the ACA is left intact, and 23 million fewer by 2026. …In 2016, there were roughly 10 million people obtaining insurance through an Obamacare exchange. The CBO estimated that number would suddenly surge to 18 million by 2018 if the law was left intact, but that far fewer people would be covered if the House reforms became law. Put simply, the CBO estimated that millions of people who don’t have insurance through an exchange today would “lose” coverage they would otherwise obtain next year. That’s doubtful. …At one point, the office estimated 22 million people would receive insurance through an Obamacare exchange by 2016. As already noted, the actual figure was less than half that. One major reason for the CBO being so far off the mark is that federal forecasters believed Obamacare’s individual mandate would cause people to buy insurance, regardless of cost. That hasn’t proven true. …In a nutshell, the CBO predicts reform would cause millions to lose coverage they don’t now have, and that millions more would eagerly reject the coverage they do have because it’s such a bad deal. Those aren’t conclusions that bolster the case for Obamacare.

CBO says 14 million fewer people on net would be insured in 2018 relative to the ObamaCare status quo, rising to 23 million in 2026. The political left has defined this as “losing coverage.” But 14 million would roll off Medicaid as the program shifted to block grants, which is a mere 17% drop in enrollment after the ObamaCare expansion. The safety net would work better if it prioritized the poor and disabled with a somewhat lower number of able-bodied, working-age adults. The balance of beneficiaries “losing coverage” would not enroll in insurance, CBO says, “because the penalty for not having insurance would be eliminated.” In other words, without the threat of government to buy insurance or else pay a penalty, some people will conclude that ObamaCare coverage isn’t worth the price even with subsidies. …CBO’s projections about ObamaCare enrollment…were consistently too high and discredited by reality year after year. CBO is also generally wrong in the opposite direction about market-based reforms, such as the 2003 Medicare drug benefit whose costs the CBO badly overestimated.

Here are excerpts from Seth Chandler’s Forbescolumn.

My complaints about the CBO largely revolve around its dogged refusal to adjust its computations to the ever-more-apparent failings of the Affordable Care Act. When the CBO says that 23 million fewer people will have insurance coverage under the AHCA than under the ACA — a statistic that politics have converted into a mantra — that figure is predicated on an ACA that no longer exists. It is based on the continuing assumption that the ACA will have 18 million people enrolled on its exchanges in 2018 and that this situation will persist until 2026. I know no one on any side of the political spectrum who believes this to be true. The ACA has about 11 million people currently enrolled on its exchanges in 2017 and, with premiums going up, some insurers withdrawing from various markets, and the executive branch fuzzing up whether the individual mandate will actually be enforced. The consensus is that ACA enrollment will stay the same or go down, not increase 60%.

And here’s some of what Drew Gonshorowski wrote for the Daily Signal.

…reducing premium levels by rolling back regulations could actually have the effect of making plans more desirable for individuals looking to pay less. The CBO lacks any real discussion of these positive effects. …The CBO’s score on Medicaid…reflects that it assumes more states would likely have expanded in the future under the Affordable Care Act. Thus, its projection that 14 million fewer people would be insured due to not having Medicaid under the American Health Care Act might be overstated… CBO…assumes the Affordable Care Act will enroll 7 to 8 million more people in the individual market, when in reality it does not appear this will be the case

Last but not least, my former colleague Robert Moffit expressed concerns in a column for USA Today. The part that caught my eye was that CBO has a less-than-stellar track record on Obamacare projections.

The GOP should be skeptical of CBO’s coverage estimates. It has been an abysmal performance. For example, CBO projected initially that 21 million persons would enroll in exchange plans in 2016. The actual enrollment: 11.5 million.

The bottom line is that CBO overstated the benefits of Obamacare, at least as measured by the number of people who would sign up for the program.

The bureaucrats were way off.

Yet CBO continues to use those inaccurate numbers, creating a make-believe baseline that is then used to estimate a large number of uninsured people if the Republican bill is enacted.

P.S. You may be wondering why Republicans don’t fully repeal Obamacare so that they can get credit for falling premiums. Part of the problem is that they are using “reconciliation” legislation that supposedly is limited to fiscal matters. In other words, you can’t repeal red tape and regulation. At least according to some observers. I think that’s silly since such interventions drive up the cost of health care, which obviously has an impact on the budget. Also, Republicans are a bit squeamish about reducing subsidies for various groups, whether explicit (like the Medicaid expansion) or implicit (like community rating). In other words, the Second Theorem of Government applies.

For three decades, I’ve been trying to convince politicians to adopt good policy. I give them theoretical reasons why it’s a good idea to have limited government. I share with them empirical evidence demonstrating the superiority of free markets over statism. And I’m probably annoyingly relentless about disseminating examples of good and bad policy from around the world (my version of “teachable moments”).

But if you want to get a politician to do the right thing, you need more than theory, data, and real-world case studies. You need to convince them – notwithstanding my Second Theorem of Government – that good policy won’t threaten their reelection.

My usual approach is to remind them that Ronald Reagan adopted a bunch of supposedly unpopular policies, yet he got reelected in a landslide because reducing the burden of government allowed the private sector to grow much faster. George H.W. Bush, by contrast, became a one-term blunder because his tax increase and other statist policies undermined the economy’s performance.

I’m hoping this argument will resonate with some of my friends who are now working in the White House. And I don’t rely on vague hints. In this clip from a recent interview, I bluntly point out that good policy is good politics because a faster-growing economy presumably will have a big impact on the 2020 election.

But the Republican plan did not try to fix the government-imposed third-party-payer distortions that cause health care to be so expensive and inefficient. And I pointed out at the end of this clip that Republicans would have been held responsible as the system got even more costly and bureaucratic.

Now let’s shift to fiscal policy.

Here’s a clip from an interview about Trump’s budget. I’m happy about some of the specific reductions (see here, here, and here), but I grouse that there’s no attempt to fix entitlements and I’m also unhappy that the reductions in domestic discretionary spending are used to benefit the Pentagon rather than taxpayers.

The latter half of the above interview is about the corruption that defines the Washington swamp. Yes, it’s possible that Trump could use the “bully pulpit” to push Congress in the right direction, but I wish I had more time to emphasize that shrinking the overall size of government is the only way to really “drain the swamp.”

And since we’re talking about good policy and good politics, here’s a clip from another interview.

Back when the stock market was climbing, I suggested it was a rather risky move for Trump to say higher stock values were a referendum on the benefits of his policies. After all, what goes up can go down.

The hosts acknowledge that the stock market may decline in the short run, but they seem optimistic in the long run based on what happened during the Reagan years.

In other words, there was a direct connection between good policy, good economy, and good political results. Indeed, let’s enshrine this relationship in a “Fourth Theorem of Government.”

For what it’s worth, Reagan also demonstrated leadership, enacting all those pro-growth reforms over the vociferous opposition of various interest groups.

Will Trump’s reform be that bold and that brave? His proposed 15-percent corporate tax rate deserves praise, and he seems serious about restraining the regulatory state, but he will need to do a lot more if he wants to be the second coming of Ronald Reagan. Not only will he need more good policies, but he’ll also need to ditch some of the bad policies (childcare subsidies, infrastructure pork, carried-interest capital gains tax hike, etc) that would increase the burden of government.

The jury is still out, but I’m a bit pessimistic on the final verdict.

I’m flabbergasted when people assert that America’s costly and inefficient healthcare system is proof that free markets don’t work.

In hopes of helping them understand what’s really going on, I try to explain to them that an unfettered market involves consumers and producers directly interacting with their own money in an open and competitive environment.

I then explain why that’s not a description of the U.S. system. Not even close. As I noted in Part I, consumers directly finance only 10.5 percent of their healthcare expenses. Everything else involves a third-party payer thanks to government interventions such as Medicare, Medicaid, the healthcare exclusion, the Veterans Administration, etc.

Obamacare then added another layer of intervention to the existing mess. By my rough calculations, that costly boondoggle took the country from having a system that was 68-percent controlled and dictated by government to a system where government dictates and controls 79 percent of the system.

This is very relevant because Republicans in Washington are now trying to “repeal and replace” Obamacare, but they’re confronting a very unpleasant reality. Undoing that legislation won’t create a stable, market-driven healthcare system. Instead, we’d only be back to where we were in 2010 – a system where government would still be the dominant player and market forces would be almost totally emasculated.

The only difference is that Republicans would then get blamed for everything that goes wrong in the world of healthcare rather than Obama and the Democrats (and you better believe that’s a big part of the decision-making process on Capitol Hill).

Yes, the GOP plan would save some money, which is laudable, but presumably the main goal is to have a sensible and sustainable healthcare system. And that’s not going to happen unless there’s some effort to somehow unravel the overall mess that’s been created by all the misguided government policies that have accumulated over many decades.

This isn’t a new or brilliant observation. Milton Friedman wrote about how government-controlled healthcare leads to higher costs and lower quality back in 1977, but I can’t find an online version of that article, so let’s look at what he said in a 1978 speech to the Mayo Institute.

I realize that many people won’t have 45 minutes of spare time to watch the entire video, so I’ll also provide some excerpts from a column Friedman wrote back in the early 1990s that makes the same points. He started by observing that bureaucratic systems have ever-rising costs combined with ever-declining output.

…a study by Max Gammon…comparing input and output in the British socialized hospital system…found that input had increased sharply, while output had actually fallen. He was led to enunciate what he called “the theory of bureaucratic displacement.” In his words, in “a bureaucratic system . . . increase in expenditure will be matched by fall in production. . . . Such systems will act rather like `black holes,’ in the economic universe, simultaneously sucking in resources, and shrinking in terms of `emitted production.'” …concern about the rising cost of medical care, and of proposals to do something about it — most involving a further move toward the complete socialization of medicine — reminded me of the Gammon study and led me to investigate whether his law applied to U.S. health care.

Friedman then noted how this bureaucratic rule operated in the United States after the healthcare exclusion was adopted during World War II.

Even a casual glance at figures on input and output in U.S. hospitals indicates that Gammon’s law has been in full operation for U.S. hospitals since the end of World War II… Before 1940, input and output both rose, input somewhat more than output, presumably because of the introduction of more sophisticated and expensive treatment. The cost of hospital care per resident of the U.S., adjusted for inflation, rose from 1929 to 1940 at the rate of 5% per year; the number of occupied beds, at 2.4% a year. Cost per patient day, adjusted for inflation, rose only modestly. The situation was very different after the war. From 1946 to 1989, the number of beds per 1,000 population fell by more than one-half; the occupancy rate, by one-eighth. In sharp contrast, input skyrocketed. Hospital personnel per occupied bed multiplied nearly seven-fold and cost per patient day, adjusted for inflation, an astounding 26-fold.

Friedman then explained that the adoption of Medicare and Medicaid hastened the erosion of market forces.

One major engine of these changes was the enactment of Medicare and Medicaid in 1965. A mild rise in input was turned into a meteoric rise; a mild fall in output, into a rapid decline. …The federal government’s assumption of responsibility for hospital and medical care for the elderly and the poor provided a fresh pool of money, and there was no shortage of takers. Personnel per occupied bed, which had already doubled from 1946 to 1965, more than tripled from that level after 1965. Cost per patient day, which had already more than tripled from 1946 to 1965, multiplied a further eight-fold after 1965. Growing costs, in turn, led to more regulation of hospitals, further increasing administrative expense.

Remember, Friedman wrote this article back in 1991. And the underlying problems have gotten worse since that time.

So what’s the bottom line? Friedman pointed out that the problem is too much government.

The U.S. medical system has become in large part a socialist enterprise. Why should we be any better at socialism than the Soviets?

And he explained that there’s only one genuine solution.

The inefficiency, high cost and inequitable character of our medical system can be fundamentally remedied in only one way: by moving in the other direction, toward re-privatizing medical care.

Some readers may be skeptical. Even though he cited lots of historical evidence, perhaps you’re thinking Friedman’s position is impractical.

So let’s fast forward to 2017 and look at some very concrete data assembled by Mark Perry of the American Enterprise Institute. He looks at medical costs over the past 18 years and compares what’s happened with prices for things that are covered by third-party payer (either government or government-distorted private insurance) and prices for cosmetic procedures that are financed directly by consumers.

As you can see, the relative price of health care generally declines when people are spending their own money and operating in a genuine free market. But when there’s third-party payer, relative prices rise.

Perry explains the issue very succinctly.

Cosmetic procedures, unlike most medical services, are not usually covered by insurance. Patients paying 100% out-of-pocket for elective cosmetic procedures are cost-conscious, and have strong incentives to shop around and compare prices at the dozens of competing providers in any large city. Providers operate in a very competitive market with transparent pricing and therefore have incentives to provide cosmetic procedures at competitive prices. Those providers are also less burdened and encumbered by the bureaucratic paperwork that is typically involved with the provision of most standard medical care with third-party payments. Because of the price transparency and market competition that characterizes the market for cosmetic procedures, the prices of most cosmetic procedures have fallen in real terms since 1998, and some non-surgical procedures have even fallen in nominal dollars before adjusting for price changes. In all cases, cosmetic procedures have increased in price by far less than the 100.5% increase in the price of medical care services between 1998 and 2016 and the 176.6% increase in hospital services.

In other words, a free market can work in healthcare. And it gives us falling prices and transparency rather than bureaucracy and inefficiency. Maybe when they’ve exhausted all other options, Republicans will decide to give freedom a try.

P.S. If you want to get a flavor for how competition and markets generate better results, watch this Reason TV video and read these stories from Maine and North Carolina.

And as Milton Friedman wisely observed, that approach (known as “third-party payer”) undermines normal market incentives for lower costs. Indeed, it’s a green light for ever-higher costs, which is exactly what we see in the parts of the healthcare system where government programs or insurance companies pick up most of the tab.

For what it’s worth, I’m not overflowing with confidence that the new Obamacare-replacement proposal from Republicans will have much impact on the third-party payer crisis. And it probably doesn’t solve some of the Obamacare-specific warts in the system. If you want to get depressed about those issues, read what Michael Cannon, Philip Klein, and Christopher Jacobs have written about the new GOP plan.

But healthcare in America is also a fiscal issue. And if we’re just looking at the impact of the American Health Care Act on the burden of government spending and taxes, I’m a bit more cheerful.

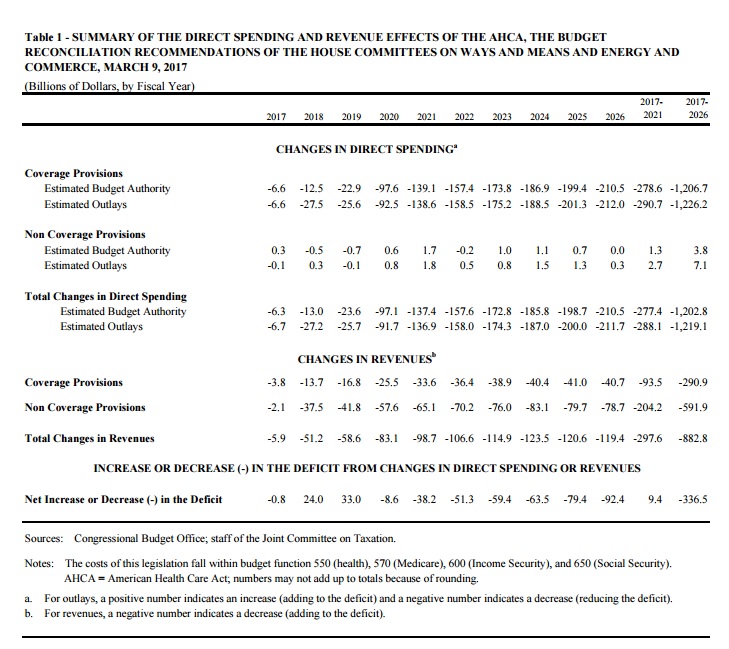

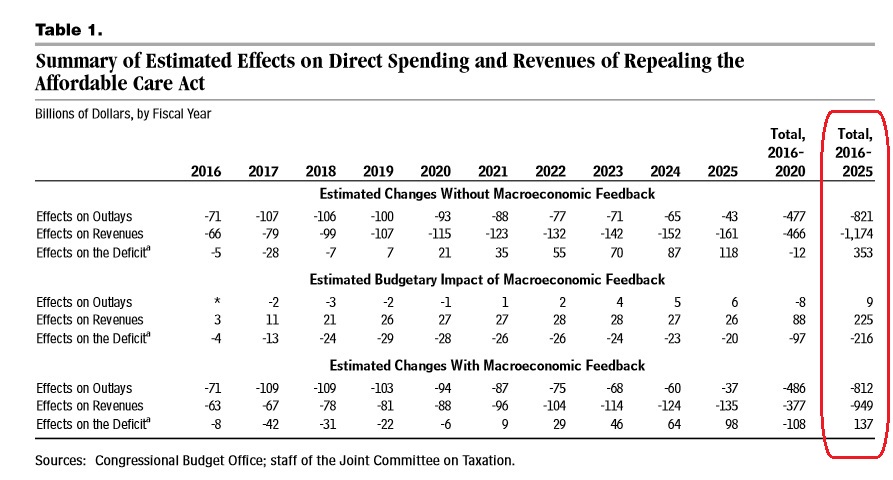

The Congressional Budget Office released its official score on the impact of the legislation. Here’s the excerpt that warmed my heart.

Outlays would be reduced by $1.2 trillion over the period, and revenues would be reduced by $0.9 trillion. The largest savings would come from reductions in outlays for Medicaid and from the elimination of the Affordable Care Act’s (ACA’s) subsidies for nongroup health insurance. … parts of the legislation would repeal or delay many of the changes the ACA made to the Internal Revenue Code… Those with the largest budgetary effects include: • Repealing the surtax on certain high-income taxpayers’ net investment income; • Repealing the increase in the Hospital Insurance payroll tax rate for certain high-income taxpayers; • Repealing the annual fee on health insurance providers; and • Delaying when the excise tax imposed on some health insurance plans with high premiums would go into effect.

And fellow wonks will be interested in this table.

By the way, the “two cheers” in the title may be a bit too generous. After all, there should be full reform of Medicare and Medicaid. Though I suppose some of that can happen (at least Medicaid, hopefully) as part of the regular budget process.

It’s also unfortunate that Republicans are creating a new refundable tax credit (and when you see the term “refundable tax credit,” that generally is a sneaky euphemism for more government spending that is laundered through the tax code, sort of like the EITC) to replace some of the Obamacare subsidies that are being repealed.

So it’s far from ideal.

For those who want to see the glass as being half-full rather than half-empty, however, Ryan Ellis has a very upbeat assessment in a column for Forbes.

It’s a net spending cut of over $1.2 trillion and a net tax cut of nearly $900 billion over the next decade. …the score shows that the AHCA would be a large and permanent tax cut for families and employers….This should lower the tax revenue baseline considerably, perhaps even by half a percentage point of the economy.

I like starving the beast, so I agree this is a good thing.

And I also agree with Ryan that the resulting lower tax burden on dividends and capital gains is very positive. After all, double taxation is probably the most pernicious feature of the internal revenue code.

The most pro-growth tax cut in the bill is the elimination of the so-called “NIIT” or “net investment income tax.” It adds on a 3.8 percentage point surtax on savers and investors. By eliminating NIIT, the bill cuts the capital gains and dividends tax from 23.8 percent in 2017 to 20 percent in 2018 and beyond. …The contribution limit to HSAs is doubled, from nearly $7000 for families today to $14,000 starting in 2018.

But I’ll close with some sad news. If the legislation is approved, that probably means no more Obamacare-related humor. If this makes you sad, you can easily spend about 30 minutes enjoying Obamacare cartoons, videos, and jokes by clicking here, here, here, here, here, here, here, here, here, here, here, here, here, here, here, here, here, here, here, and here.

I call it the “First Theorem of Government,” and I think it accurately reflects the real purpose and operation of government. Except I probably should have added lobbyists and contractors. And it goes without saying (though I probably should have said it anyhow) that politicians are the main beneficiaries of this odious racket.

I think this theorem has stood the test of time. It works just as well when Republicans are in charge as it does when Democrats are in charge.

But it doesn’t describe everything.

For instance, Republicans have won landslide elections in recent years by promising that they will repeal Obamacare the moment they’re in charge. Well, now they control both Congress and the White House and their muscular rhetoric has magically transformed into anemic legislation.

This is very disappointing and perhaps I’ll share some of Michael Cannon’s work in future columns about the policy details, but today I want to focus on why GOP toughness has turned into mush.

In part, this is simply a reflection of the fact the rhetoric of politicians is always bolder than their legislation (I didn’t agree with 98 percent of what was said by Mario Cuomo, the former Governor of New York, but he was correct that “You campaign in poetry. You govern in prose.”)

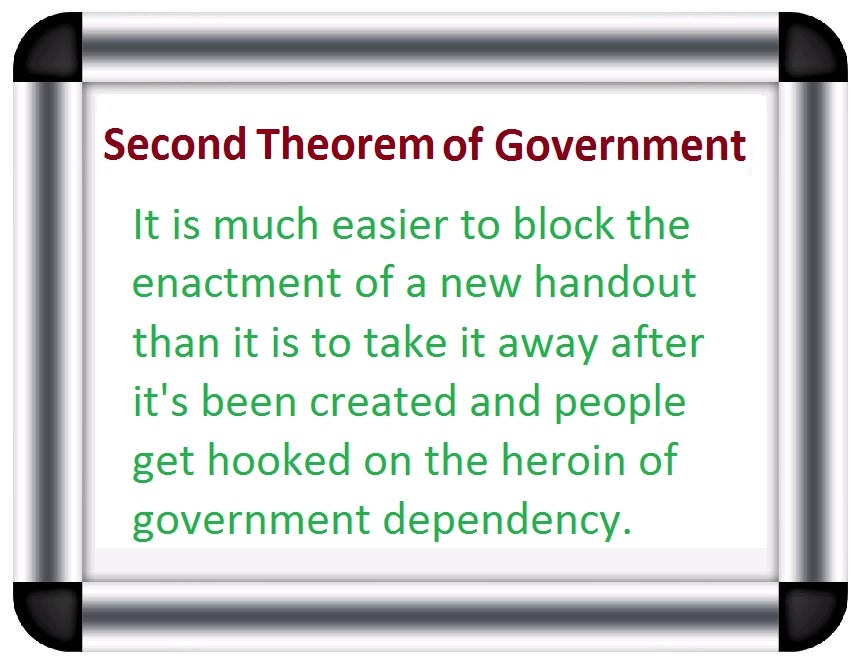

But that’s just a small part of the problem. The real issue is that it’s relatively easy for GOP politicians to battle against proposed handouts and it’s very difficult to battle against existing handouts. That’s because government goodies are like a drug. Recipients quickly get hooked and they will fight much harder to preserve handouts than they will to get them in the first place.

And that’s the basic insight of the “Second Theorem of Government.”

Here’s a recent interview on FBN. The topic is the Republican reluctance to fully repeal Obamacare. I only got two soundbites, and they both occur in the first half of the discussion, but you can see why I was motivated to put forth the new theorem.

Simply stated, I’m disappointed, but I’m more resigned than agitated because this development was so sadly predictable.

And here are a couple of follow-up observations. I guess we’ll call them corollaries to the theorem.

You break it, you buy it – Government intervention had screwed up the system well before Obamacare was enacted, but people now blame the 2010 law (and the Democrats who voted for it) for everything that goes wrong with healthcare. Republicans fear that all the blame will shift to them if their “Repeal and Replace” legislation is adopted.

Follow the money – What’s partly driving GOP timidity is their desire not to anger many of the interest groups – such as state governments, hospitals, doctors, insurance companies, etc – who benefit from various Obamacare handouts. That’s what is motivating criticism for politicians such as Ohio’s John Kasich and Alaska’s Lisa Murkowski.

Don’t throw the baby out with the bathwater – The “Cadillac Tax” is the one part of Obamacare that’s worth preserving because it will slowly cut back on the distorting tax preferences that lead to over-insurance and third-party payer. For what it’s worth, the GOP plan retains that provision, albeit postponed until 2025.

For these reasons (as well as other corollaries to my theorem), I’m not brimming with optimism that we’ll get real Obamacare repeal this year. Or even substantive Obamacare reform.

P.S. Now you know what I speculated many years ago that Obamacare would be a long-run victory for the left even though Democrats lost many elections because of it. I sometimes hate when I’m right.

And if you want to be even more specific, the fastest-growing entitlement program is Medicaid, which was originally supposed to be a very small program to subsidize health care for poor people but has now metastasized into a budget-gobbling fiscal disaster. Arguably, it’s the entitlement program most in need of reform.

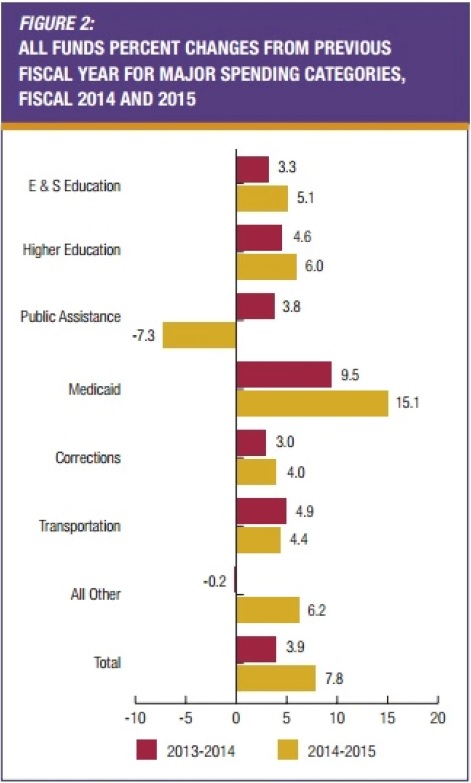

So how big is the problem? Enormous if you look at the numbers from the National Association of State Budget Officers.

States increased their spending in fiscal year 2015 by the biggest margin in more than 20 years, but most of the increase was thanks to huge leaps in Medicaid spending under the first full year of the Affordable Care Act (ACA). Spending increased last fiscal year, which ended on June 30 for most states, by 7.8 percent, according to new estimates from the National Association of State Budget Officers (NASBO). It’s the biggest boost since 1992 and was thanks to a 15.1 percent increase in Medicaid spending, much of that paid for via federal Medicaid funds. Illinois, Michigan, Kentucky, Nevada and Oregon saw more than 30 percent increases in federal funding because they expanded Medicaid under the ACA. But 2015 was also a year where states were putting up more of their own money again.

Here’s the chart showing which outlay categories grew the fastest.

The article points out that spending is outpacing revenue.

On average, state revenues aren’t keeping pace with spending; NASBO estimates General Fund revenues will increase by just 3.8 percent.

Though the real problem is that spending is expanding faster than the private sector, which is the opposite of what is called for by my Golden Rule.

One of the reasons Medicaid grows so fast is that the program is split between Washington and the states, which both picking up a share of the cost. This may sound reasonable, but it creates a very perverse incentive structure since politicians at both levels can vote to expand the spending burden while only having to provide part of the cost.

The National Center for Policy Analysis explains how this system produces bad decisions.

Medicaid has a horrible financing mechanism: Federal transfers to states are not based on the number of poor people, or any other reasonable calculation. Instead, they depend on the amount of its own taxpayers’ money a state spends. Traditionally, when California spent $1 on Medi-Cal, the federal government kicked in $1. …So, state politicians hike taxes and spending on their own citizens in order to get as much funding as possible from people in other states (via the feds). Hospitals and Medicaid MCOs maximize this by agreeing to a state tax on themselves, which the state uses to ratchet up the federal funding. After multiplication, the money goes right back to these providers. …Stopping this wild spending growth requires fundamental reform to Medicaid’s financing. Congressional Republicans have proposed “block grants,” whereby states would get federal Medicaid transfers based on their population of poor residents, not how much they gouge out of their own people.

But unless that kind of reform happens, the program will continue to grow and become an ever-larger fiscal burden.

Heritage Action has more details on the perverse incentives of the current system.

…the federal government promises to reimburse states for a majority of their Medicaid spending, most of which involves reimbursements to health care providers. Therefore, states collude with health care providers in the following manner: they tell providers that they will tax them (so-called “provider taxes”), bringing in more revenue to the state. The state then promises to filter that money back to those same providers in the form of higher Medicaid reimbursements. States then bill the federal government for this added cost. Because the federal government provides more than 50% of total Medicaid funding, both state governments and Medicaid providers are made better off by the arrangement, while the federal government is stuck footing a larger bill it had no part in creating.

Though I partially disagree with the assertion that the feds are blameless. After all, it was politicians in Washington who created this wretched system, including the reimbursement rules that states manipulate.

The net result of all this is a nightmare for federal taxpayers, but states also are losing out when you consider the long-run consequences. And that’s even true with the Medicaid expansions contained in Obamacare, which supposedly were going to be financed almost entirely by Uncle Sam. The Wall Street Journalreports.

…the Affordable Care Act was designed to essentially bribe states to expand their Medicaid programs: The feds offered to pay 100% of additional costs through 2016, dropping to 90% by 2020. This “free money” prompted 30 states and the District of Columbia to take the deal. Democratic activists have joined with state hospital lobbies to pressure lawmakers in the remaining 20 state capitals to follow.

But free money can be very expensive.

Consider the experience of the states that did expand Medicaid. “At least 14 states have seen new enrollments exceed their original projections, causing at least seven to increase their cost estimates for 2017,” the Associated Press reported in July. The AP says that California expected 800,000 new enrollees after the state’s 2013 Medicaid expansion, but wound up with 2.3 million. Enrollment outstripped estimates in New Mexico by 44%, Oregon by 73%, and Washington state by more than 100%. This has blown holes in state budgets. Illinois once projected that its Medicaid expansion would cost the state $573 million for 2017 through 2020. Yet 200,000 more people have enrolled than were expected, and the state has increased its estimated cost for covering each. The new price tag? About $2 billion… Enrollment overruns in Kentucky forced officials to more than double the anticipated cost of the state’s Medicaid expansion for 2017, the AP reports, to $74 million from $33 million. That figure could rise to $363 million a year by 2021. In Rhode Island, where one-quarter of the state’s population is now on Medicaid, the program consumes roughly 30% of all state spending, the Providence Journal reports. To plug this growing hole, Rhode Island has levied a 3.5% tax on insurance policies sold through the state’s ObamaCare exchange.

Interestingly, Obamacare is causing pro-big government states to dig even deeper fiscal holes.

The National Center for Policy Analysis has some remarkable data on this development.

States that expanded Medicaid tend to have per capita state spending that’s about 17 percent higher than non-expansion states. …In 2004, expansion states had median per capita tax collections (both state and local) of 19 percent more than non-expansion states. By 2012, this gap had widened with expansion states collecting 28 percent more taxes per capita than non-expansion states. Moreover, since 2008 expansion states have moved to increase taxes, while non-expansion states have reduced taxes slightly.

Unsurprisingly, the states that are making government bigger are experiencing slower growth.

In 2001 expansion states had real median income that was nearly 13 percent higher than non-expansion states. However, by 2013 this gap had narrowed to just over 9 percent. Expansion states have historically had slightly lower poverty rates, but the difference was only 1 percentage point by 2012 (12.9 percent vs. 13.9 percent). Non-expansion states, although slightly poorer, have lower unemployment than expansion states (6.7 percent versus 7.2 percent).

Another point worth mentioning is that the program isn’t even a good deal for the poor according to Scott Atlas at the Hoover Institution. Here’s some of what he wrote for the Wall Street Journal.

Americans should be more worried than ever about Medicaid… The cost of the $500 billion program is expected to rise to $890 billion by 2024… Yet more spending doesn’t necessarily mean better care for beneficiaries… The expansion of Medicaid is one of the most misguided parts of ObamaCare… Some 55% of doctors in major metropolitan areas refuse to take new Medicaid patients… Medicaid enrollees who manage to see a doctor typically experience outcomes worse than those under private insurance. That means more in-hospital deaths, more complications from surgery, worse posttreatment survival rates, and longer hospital stays than similar patients with private insurance. A randomized study by the Oregon Health Study Group showed that having Medicaid did not significantly improve patients’ physical health compared with those without insurance.

The proverbial icing on this foul-tasting cake is the way the program enables staggering amounts of fraud and theft.

I’ve written about this before (including how foreigners are bilking the system). But here are some fresh details from the Wall Street Journal.

…one of our favorite political euphemisms is “improper payments.” That’s how Washington airbrushes away the taxpayer money that flows each year to someone who is not eligible, or to the right beneficiary in the wrong amount, or that disappears to fraud or federal accounting ineptitude. Now thanks to ObamaCare, improper payments are soaring. Last week the Health and Human Services Department published an “alert” warning that the improper payment rate for Medicaid in 2016 will likely hit 11.5%. That’s nearly double the 5.8% rate as recently as 2013… The 11.5% for 2016 is likely an underestimate given that HHS’s goal last year was 6.7% and instead scored 9.8%, which amounts to $29.1 billion. The dollar amount of improper payments in Medicaid was bound to rise because ObamaCare vastly opened eligibility. In 2015 enrollment climbed by 13.8% and one of five Americans are now covered by the program. …In recent audits of Medicaid in Arizona, Florida, Michigan and New Jersey, the GAO uncovered 50 dead people who recouped at least $9.6 million in benefits after they died; 47 providers who registered foreign addresses as their location of service in places such as Saudi Arabia; and $448 million bestowed on 199,000 beneficiaries with fake Social Security numbers—12,500 of which had never been issued by the Social Security Administration.

But as bad as all this sounds, it can get worse.

If HHS tries hard enough, maybe the department can match the failure rate for school lunches (15.7%) or the Earned Income Tax Credit (23.8%).

And Kevin Williamson of National Reviewadds some acidic observations.

…the criminal — and I do not use the word figuratively — administration of Medicaid by the Obama administration. …improper payments under Medicaid have become so common that they will account this year for almost 12 percent of total Medicaid spending — just shy of $140 billion. …That rate has doubled in only a few years…12 percent in improper payments isn’t an error rate — it’s a malfeasance rate. …If improper and illegal federal payments were an economy of their own, that economy would be bigger than Hungary’s… The Obama administration is not lifting a pinky to do anything about this, even though analysts such as John Hood have — for years — been arguing that it is necessary and possible to reform this mess. As the Wall Street Journal has reported, we don’t even verify that doctors billing Medicaid for services rendered are actually doctors. In many cases, we do not do much to verify that their patients actually, you know, exist. We’ve paid untold billions of dollars to “clinics” that turn out to be little more — or nothing more — than post-office boxes and prepaid cell phones. And as bad as that 12 percent rate is, some policy scholars believe that it is in fact probably worse.

Kevin observes that this system is good for the Poverty Pimps.

…the real problem with the welfare state is not the poor people receiving checks — it’s everybody in the middle, the vast array of government employees, their union allies, contractors, and third parties who earn six-, seven-, eight-, or nine-figure paydays taking their cuts of money we think we’re spending on the poor. This is an enormous criminal conspiracy against the American people and the public fisc.

You might think that fixing this fraud would be an area for bipartisan cooperation.

But the sad reality is that fraud is a feature, not a bug. Politicians like the fact that scam artists in their states and district are stealing healthcare money from taxpayers. After all, recipients of the loot can be registered voters and campaign contributors.

So what’s the best way of fixing this mess?

Will big tax hikes solve the problems? If the problem is that America isn’t enough like France, then the answer is yes.

But if the problem is that government already is too much of a burden and that it would be a good idea to at least slow down the rate at which America becomes France, then the answer is genuine entitlement reform.

P.S. For all intents and purposes, block granting Medicaid is a partial repeal of Obamacare. Just in case you wanted an additional reason to support reform.

Based on what’s been happening, those of us who have been warning about the fiscal burden of Medicaid, Medicare, and Obamacare could rest on our laurels and say “we told you so.” But it’s a Pyrrhic victory because being right means bad news for the country.

Earlier this year, The Hillreported some very sobering news about the ever-growing burden of health entitlements.

Spending on federal healthcare programs outpaced spending on Social Security for the first time in 2015, according to an expansive report from the congressional budget scorekeeper released Monday. The government spent $936 billion last year on health programs including Medicare, Medicaid and subsidies related to the Affordable Care Act, a jump of 13 percent from 2014, according to the Congressional Budget Office. Spending on Social Security, in contrast, totaled $882 billion, the Congressional Budget Office (CBO) reported.

Let’s look at just one example of why the fiscal burden of health entitlements keeps growing so rapidly.

According to new data, the portion of Obamacare that expanded Medicaid is generating a torrent of new spending.

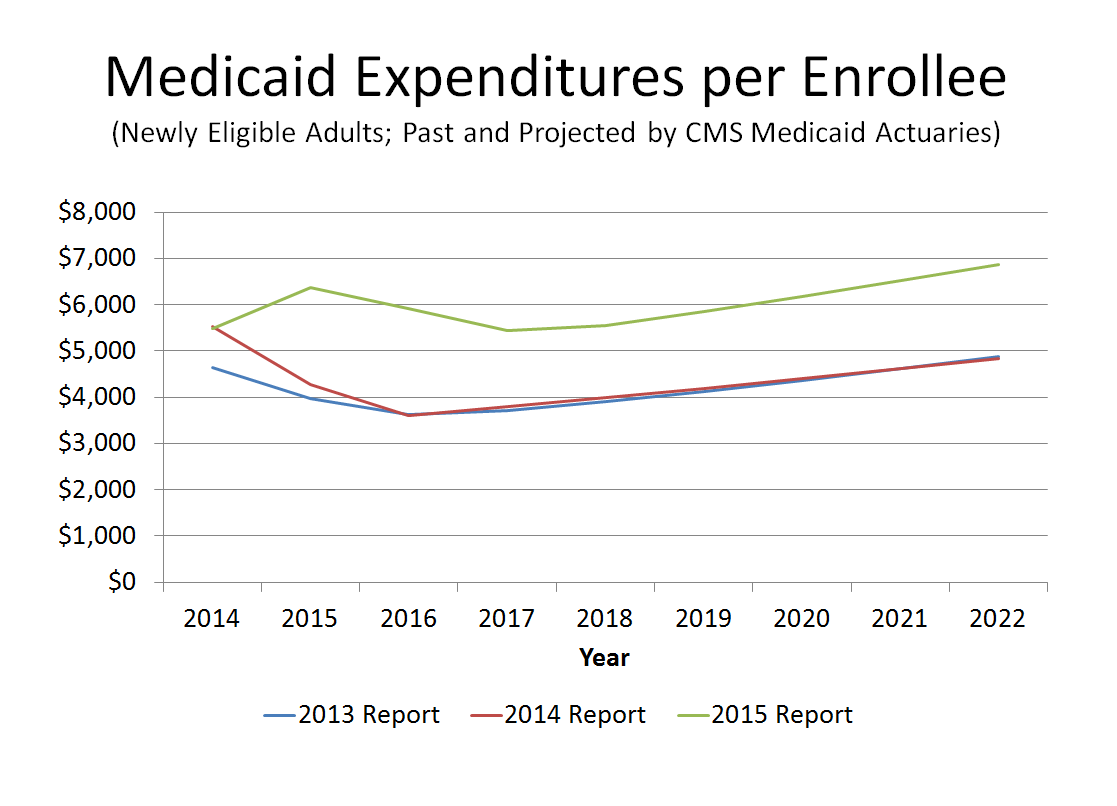

Charles Blahous is a former Trustee for Social Security and Medicare Given his inside-the-belly-of-the-beast familiarity with entitlement programs, what he’s written should be especially alarming.

The implementation of major legislation such as the Affordable Care Act (ACA) often results in fiscal outcomes that differ significantly from prior projections. …Recall that the ACA considerably expanded Medicaid eligibility… It turns out that the 2015 per-capita cost of this Medicaid expansion is a whopping 49% higher than projections made just one year before. This disclosure can be found on page 27 of the 2015 Actuarial Report for Medicaid, released this July.

Here’s the chart showing how much higher per-recipient spending will be according to the new numbers.

Blahous goes through a lot of technical information to explain why the previous forecasts were so inaccurate.

But here’s the part that I think is most important to understand. Obamacare created a free lunch for states, at least in the short run. So we shouldn’t be surprised that many states have been seduced into participating and that they’re now spending money like drunken sailors.

Basically states established far higher expenditure requirements for the expansion population than the federal government expected, by positing that beneficiaries would be in need of more health services. Why did this happen? Remember, the ACA established an initial 100% federal matching payment for state Medicaid expansion costs, contrasting with historical federal match rates that averaged 57%. Even when the feds paid 57% of the bill there was a longstanding concern that states were insufficiently accountable for their cost-expanding decisions, with much of that cost being shifted to federal taxpayers. But the ACA’s current 100% match means that states make the decisions about expanding Medicaid while the federal government picks up all the costs. Even after the ACA is fully phased in, the feds will still pay for 90%. Under such arrangements, cost overruns are predictable.

So what’s the obvious conclusion?

Having federal taxpayers pick up between 90-100% of the cost of state Medicaid expansions was one of many questionable policy decisions made in the ACA. It’s also proving to be much more expensive than the federal government expected.

Brian Blase of the Mercatus Center also has a grim assessment on the numbers.

The Department of Health and Human Services’ (HHS) annual report on Medicaid’s finances contains a stunning update: the average cost of the Affordable Care Act’s Medicaid expansion enrollees was nearly 50% higher in fiscal year (FY) 2015 than HHS had projected just one year prior. Specifically, HHS found that the ACA’s Medicaid expansion enrollees cost an average of $6,366 in FY 2015—49% higher than the $4,281 amount that the agency projected in last year’s report. The government’s chief financial experts appear not to have anticipated how states would respond to the federal government’s 100% financing of the cost of people made eligible for Medicaid by the ACA. It appears that the enhanced federal funding for the ACA expansion population has led states to set outrageously high capitation rates—the amount government pays insurers—for the ACA Medicaid expansion population.

Blase points out that this goes beyond the traditional failure of bureaucrats to accurately anticipate behavioral changes when politicians give away other people’s money.

There’s also some sleazy maneuvers to funnel money to special interest groups.

…the amounts…suggest that states are inappropriately funneling federal taxpayer money to insurers, hospitals, and other health care interests through the ACA Medicaid expansion. …The health care interest groups within the states, particularly hospitals and insurers, benefit from the higher rates while federal taxpayers are left footing the bill. …Moreover, the elevated federal reimbursement rate removes the incentives for states to make sure that insurers are not overspending on providers since overpayments come at the expense of federal, not state, taxpayers.

And most of the new spending does wind up in the pockets of the interest groups.

Recent evidence that new Medicaid enrollees only receive about 20 to 40 cents of benefit for each dollar of spending on their behalf.

But even the small fraction that goes to consumers doesn’t seem to have much positive impact on their health according to one major new study.

Medicaid expansion in Oregon was not related to significant health improvements.

So what does all this mean?

Obamacare has been a disaster. This column has been a look at how just one provision has backfired on taxpayers.

And just as bureaucrats are grossly incompetent at estimating the revenue impact of changes in tax law, they’re also grossly incompetent at predicting behavioral changes when expanding entitlement programs.

Some of us, for what it’s worth, warned about this as Obamacare was being debated.

P.S. Since I don’t want to be a naive rube, allow me to acknowledge there’s an alternative explanation for consistently inaccurate fiscal forecasts from the government.

But for ordinary people, what probably matters most is household income. And if you look at the median household income numbers for the United States, Obamanomics is a failure. According to the Census Bureau’s latest numbers, the average family today has less income (after adjusting for inflation) than when Obama took office.

In an amazing feat of chutzpah, however, the President is actually arguing that he’s done a good job with the economy. His main talking point is that the unemployment rate is down to 4.7 percent.

Yet as discussed in this Blaze TV interview, sometimes the unemployment rate falls for less-than-ideal reasons.

But he can be blamed for the fact that the numbers haven’t recovered, as would normally happen as an economy pulls out of a recession. This is a rather damning indictment of Obamanomics.

By the way, I can’t resist commenting on what Obama said in the soundbite that preceded my interview. He asserted that “we cut unemployment in half years before a lot of economists thought we could.”

In effect, the President airbrushed history and then tried to take credit for something that happened, at least in part, because of policies he opposed.

Wow.

One final point. I was asked in the interview which policy deserves the lion’s share of the blame for the economy’s tepid performance and weak job numbers.

I wasn’t expecting that question, so I fumbled around a bit before choosing Obamacare.

It’s even been bad for some of the special interest groups that backed the legislation. The big insurance companies supported the law, for instance, because they thought it would be good to have the government force people to buy their products.

And these corrupt firms even got a provision in the law promising bailouts from taxpayers if the Obamacare system didn’t work.

But the companies mistakenly assumed their sleazy pact with Obama, Pelosi, and Reid was permanent. Fortunately, their Faustian bargain appears to be backfiring.

Senator Marco Rubio has led the fight to stop bailouts for the big insurance companies.

Here are some excerpts from his recent column in the Wall Street Journal.