I’m not an optimist about Europe’s economic future.

Most nations have excessive welfare states and punitive taxes, which is hardly good news. You then have to consider demographic trends such as aging populations  (i.e., more people relying on government) and falling birthrates (i.e., fewer future taxpayers).

(i.e., more people relying on government) and falling birthrates (i.e., fewer future taxpayers).

That’s a very grim combination.

Indeed, this is a big reason why I favored Brexit. Yes, it was largely about escaping an increasingly dirigiste European bureaucracy in Brussels, but it was also about not being chained to a continent with a dismal long-run outlook.

More than one year ago, before there were any concerns about a coronavirus-instigated economic crisis, Vijay Victor, an economist from Szent Istvan University in Hungary, expressed concern about Europe’s fiscal future in a column for the Foundation for Economic Education.

The debt crisis in the Eurozone is getting no better, even in the wake of the new year. The five countries in the Eurozone with the highest debt-to-GDP ratio in the third quarter of 2018 were Greece, Italy, Portugal, Belgium, and Spain.

The total debt of Greece is around 182.2 percent of its GDP and that of Italy is 133 percent… Dawdling economic growth coupled with low-yield investment options are dragging these indebted economies toward insolvency… Unemployment rates, for example, are still very high in most of these highly indebted European economies. Despite the recurrent monetary assistance and policy support, job creation is weak, which might imply that the debt financing is channelized in a nonproductive direction.

By the way, I can’t resist taking this opportunity to remind people that debt is a problem, but it also should be viewed as a symptom of en even-bigger problem, which is an excessive burden of government spending.

A bloated welfare state is a drag on economic performance, whether it’s financed by borrowing or taxes.

Though nations that try to finance big government with red ink eventually spend their way into crisis (as defined by potential default).

And we may be reaching that point.

Desmond Lachman of the American Enterprise has authored a very grim assessment, focusing primarily on Italy, for the National Interest.

Today, with Italy at the epicenter of the world coronavirus epidemic, it would seem to be only a matter of time before the durability of the Euro is again tested by another full-blown Italian sovereign debt crisis. …even before the coronavirus epidemic struck its economy was weak while its public finances and banking system were in a state of poor health.

After having experienced virtually no economic growth over the past decade, the Italian economy again entered into a recession by end-2019. At the same time, at 135 percent its public debt to GDP ratio was higher than it was in 2012 while its banks’ balance sheets remained clogged with non-performing loans and Italian government bonds. …the coronavirus epidemic will seriously damage both Italy’s public finances and its banking system…by throwing the country into its deepest economic recession in the post-war period. That in turn is bound to cause Italy’s budget deficit to balloon and its banking system’s non-performing loans to skyrocket as more of its households and companies file for bankruptcy. …all too likely that the Italian economy will shrink by at least 10 percent in 2020.

All this matters because the people and institutions that purchase government debt may decide that Italy’s outlook is so grim that they will be very reluctant to buy the country’s bonds (i.e., they’ll be very hesitant about lending money to the Italian government because of a concern that they won’t get paid back).

This means that the Italian government will have to pay much higher interest rates in order to compensate lenders for the risk of a potential default.

So what are the implications? Will Italy default, or will there be some sort of bailout?

If the latter, Lachman predicts it will be huge.

One way to gauge the amount of public money that might be needed to prop up Italy is to consider that over the past decade it took around US$300 billion in official support to keep Greece in the Euro. Given that the Italian economy is around ten times the size of that of Greece, this would suggest that Italy might very well need around $3 trillion in official support to keep Italy in the Euro. …Meanwhile, Italy’s US$4 trillion banking system could very well need at least US$1 trillion in official support to counter the capital flight and the spike in non-performing loans that are all too likely to occur in the event of a deep Italian recession.

For what it’s worth, Lachman thinks a bailout would be desirable.

I disagree. Default is a better choice because it will discipline the Italian government (it would mean an overnight balanced budget requirement since nobody will lend money to the government) and also discipline foolish lenders who thought Italian politicians were a good bet.

Simply stated, we should minimize moral hazard.

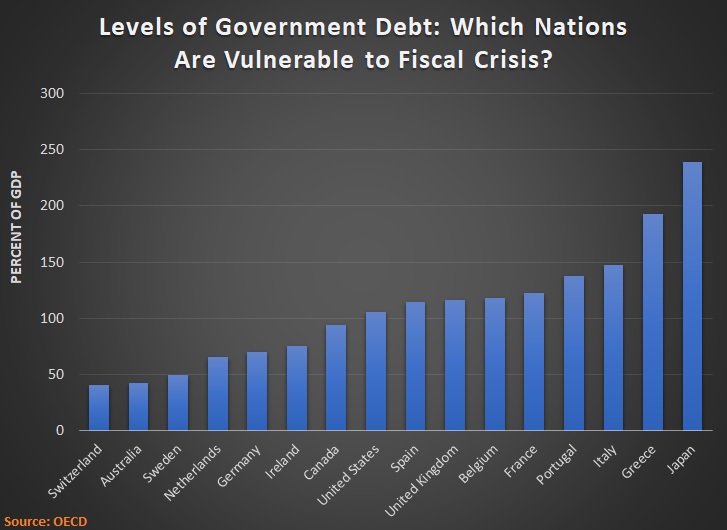

I also think it’s worth noting that Italy isn’t the only government at risk of fiscal crisis. Here’s the OECD data for major nations, including a few non-European examples.

Japan wins the prize for the most red ink, though this doesn’t mean Japan is most vulnerable to a default, at least in the short run.

A fiscal crisis is driven by investor sentiment (i.e., when will people and institutions decide they no longer trust a government to pay back loans). And that depends on a range of factors, including trust.

The bottom line is that investors trust the Japanese government and they don’t trust the Italian government.

That being said, I think all of the PIGS (Portugal, Italy, Greece, and Spain) are very vulnerable.

And politicians in Ireland, Belgium, and France should be nervous as well.

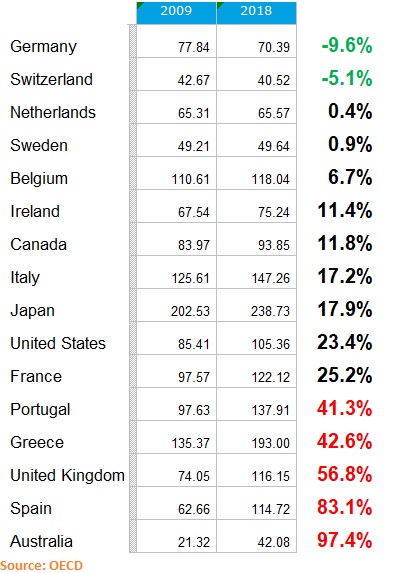

I’ll close by sharing some calculations, based on the aforementioned OECD data, showing which nations used last decade’s economic recovery to improve their balance sheets.

Congratulations to Germany and Switzerland for fiscal responsibility, and mild applause for the Netherlands and Sweden.

I’ve highlighted (in red) the nations that were most reckless.

Though keep in mind that you want to look at both the trend for debt (far-right column) and the existing level of debt (the next-to-far-right column). So I’m not overly worried about Australia. Debt is still comparatively low, even though it almost doubled last decade.

But all of the PIGS are in trouble.

So if economic conditions deteriorate in Europe, the fallout could be significant.

P.S. The United Kingdom, like Japan, benefits from a high level of trust – presumably in part because the country paid off enormous debts from the Napoleonic wars and World War II. That being said, the numbers for the U.K. are worrisome, which hopefully will lead to a renewed commitment to spending restraint by Boris Johnson’s government.

[…] But what about the United States? Or Japan? And how’s the outlook for Europe’s welfare states? […]

[…] Once again, I’ll add an editorial comment. It’s not that budget crises will “possibly” happen. They will happen. […]

[…] Once again, I’ll add an editorial comment. It’s not that budget crises will “possibly” happen. They will happen. […]

[…] But what about the United States? Or Japan? And how’s the outlook for Europe’s welfare states? […]

[…] But what about the United States? Or Japan? And how’s the outlook for Europe’s welfare states? […]

[…] But what about the United States? Or Japan? And how’s the outlook for Europe’s welfare states? […]

[…] But what about the United States? Or Japan? And how’s the outlook for Europe’s welfare states? […]

[…] But what about the United States? Or Japan? And how’s the outlook for Europe’s welfare states? […]

[…] But what about the United States? Or Japan? And how’s the outlook for Europe’s welfare states? […]

[…] But what about the United States? Or Japan? And how’s the outlook for Europe’s welfare states? […]

[…] crisis and I warned that the IMF may intervene to prop up that country’s bad policy. And when other European countries get in trouble, IMF bureaucrats will probably try to make a bad situation even worse with further […]

[…] crisis and I warned that the IMF may intervene to prop up that country’s bad policy. And when other European countries get in trouble, IMF bureaucrats will probably try to make a bad situation even worse with further […]

[…] “Fiscal conservatism has dominated policy.” To be blunt, that’s wildly wrong. […]

[…] be more specific, the combination of demographic decline and fiscal decay means the bureaucrats and politicians in Brussels eventually will obtain the power to impose taxes […]

[…] be more specific, the combination of demographic decline and fiscal decay means the bureaucrats and politicians in Brussels eventually will obtain the power to impose taxes […]

[…] But what about the United States? Or Japan? And how’s the outlook for Europe’s welfare states? […]

[…] showed which European nations were in the unfortunate position of facing big future spending increases (the vertical axis) combined with already-high […]

[…] showed which European nations were in the unfortunate position of facing big future spending increases (the vertical axis)combined with already-high levels of […]

[…] showed which European nations were in the unfortunate position of facing big future spending increases (the vertical axis) combined with already-high levels of […]

[…] of Europe’s welfare states already are on the verge of crisis. And as demographics change over time (findings replicated in the European Commission’s Ageing […]

[…] of Europe’s welfare states already are on the verge of crisis. And as demographics change over time (findings replicated in the European Commission’s […]

[…] First, many European countries are at risk because politicians, year after year, have spent too much money (Italy is just the tip of the iceberg). […]

[…] I’ve periodically warned the European nations such as France, Italy, Greece, and Spain almost surely are doomed to suffer a fiscal crisis. […]

[…] But what about the United States? Or Japan? And how’s the outlook for Europe’s welfare states? […]

[…] that data doesn’t even include all the additional red ink accumulated in recent […]

[…] don’t think it’s “a hard argument to make”. I’ve pointed out – over and over again – that Europe’s reasonably good policies in some areas are more than […]

[…] But what about the United States? Or Japan? And how’s the outlook for Europe’s welfare states? […]

[…] But what about the United States? Or Japan? And how’s the outlook for Europe’s welfare states? […]

[…] But what about the United States? Or Japan? And how’s the outlook for Europe’s welfare states? […]

[…] But what about the United States? Or Japan? And how’s the outlook for Europe’s welfare states? […]

[…] For what it’s worth, it’s a mistake to provide bailouts, especially if there are no strings attached to force recipients to fix bad policies. […]

[…] Her wise words also could be applied to what happened about a decade ago in Greece. And what’s about to happen in Italy. […]

[…] 1) https://danieljmitchell.wordpress.com/2020/03/26/european-fiscal-crisis-round-2/ […]

[…] warned that the budgetary impact of the coronavirus may trigger another fiscal crisis in […]

[…] remarks focused on the severity of the downturn, the likelihood of a new fiscal crisis in Europe, and how to balance the costs and benefits of re-opening the […]

[…] Either bankruptcy or default would be a much better choice, and I lean in the direction of default (the same view I have when contemplating Europe’s failing welfare states). […]

[…] I wrote last month, the coronavirus-triggered economic mess is wreaking havoc with the finances of EU nations, […]

Reblogged this on Boudica2015.

the answer to the debt crisis is more EU, we need debt equity swaps with EIB to relief Member States and manage 16 Trillion of state assets better at EIB