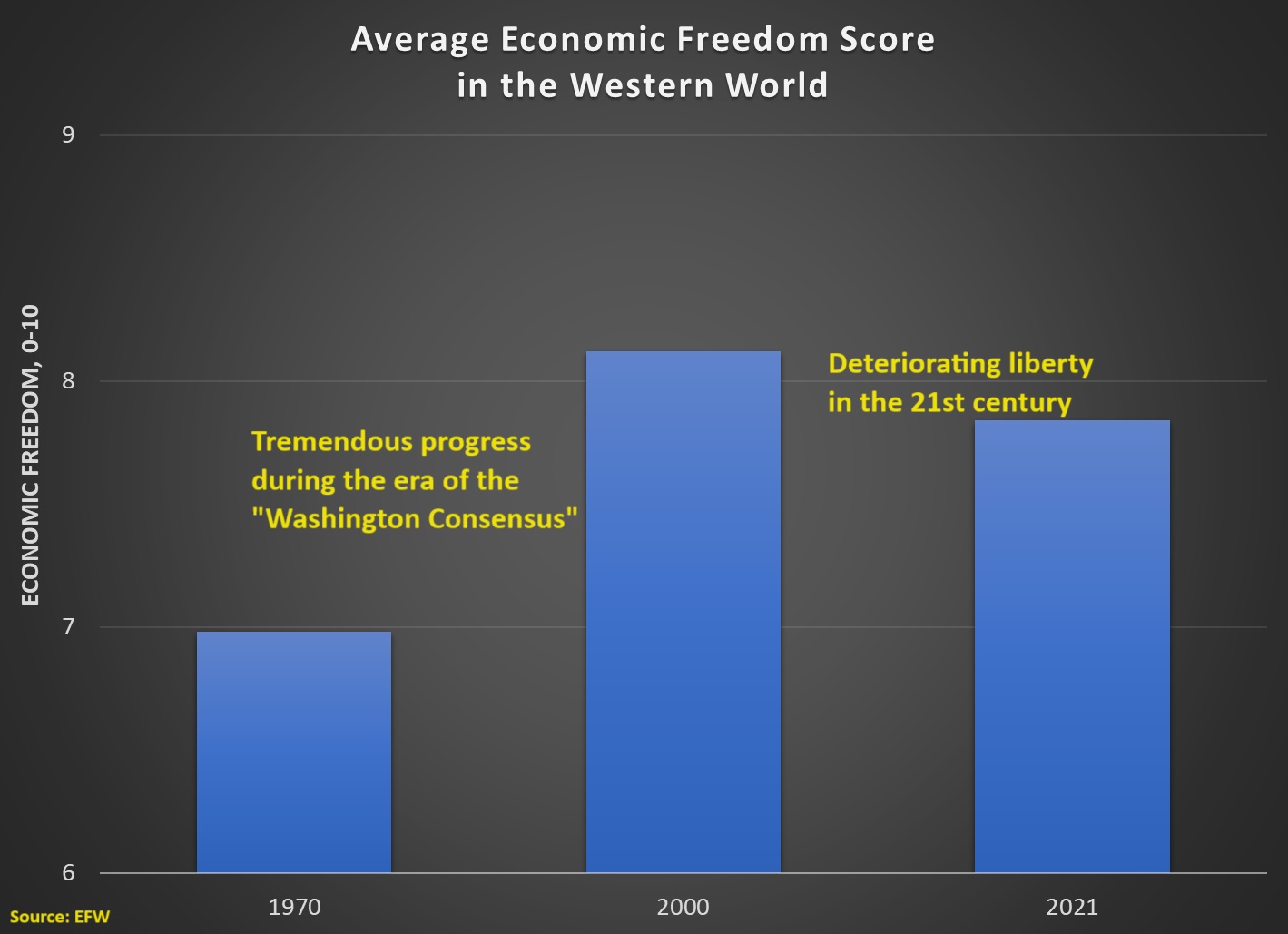

Sadly, here’s a more up-to-date chart showing that the loss of economic freedom is a problem for the entire western world (the advanced nations of North America, Western Europe, and the Pacific Rim).

As you can see, a big increase in economic liberty during the era of the “Washington Consensus” followed by a decline since the turn of the century.

Sadly, only three nations – Israel, South Korea, and Taiwan – improved their economic freedom scores between 2000 and 2021. Every other country declined.

Moreover, it pains me to acknowledge that the United States suffered the biggest decline, dropping from 8.84 to 8.14.

The situation has become so bad that even the New York Times has noticed. Here are some excerpts from a story by Patricia Cohen.

More than 2,500 industrial policies were introduced last year, roughly three times the number in 2019, according to a new study. And most were imposed by the richest, most advanced economies — many of which could previously be counted on to criticize such tactics. …the trend is worrying some international leaders and economists who warn that such top-down economic interventions could end up slowing worldwide growth. …“There are different ways of shooting yourself in the foot,” M. Ayhan Kose, the deputy chief economist of the World Bank, said about the trend of rich countries pursuing industrial policies. “This is one way of doing it.” …The current wave of policies…is a stark contrast to the classic open markets, hands-off government ideology championed by the citadels of capitalism in recent decades. …After years of complaints about China’s subsidies of private and state-owned industries, the United States and Europe have increasingly copied Beijing’s playbook, undertaking multibillion-dollar industrial policies.

It’s rather strange that those mistakes were not mentioned. Or, perhaps not so strange since the reporter was talking to people at the annual meeting of the International Monetary Fund and World Bank. And the IMF this century has been controlled by political types who preach a dirigiste message of bigger government and higher taxes.

I’ll close by citing an additional passage that is very discordant.

…faith in the superiority of free-market policies was deeply shaken in recent years by a string of global jolts — the pandemic, supply chain meltdowns, soaring inflation and interest rates, Russia’s invasion of Ukraine, and rising tensions between the United States and China.

Why on earth did the reporter assert that faith in free enterprise was shaken by things that have nothing to do with capitalism?!?

Then, to add insult to injury, the IMF pushes for higher taxes even when countries don’t need bailouts.

The IMF repeatedly has urged higher taxes in the United States. And now the bureaucrats are pushing for higher taxes in the United Kingdom.

In an article for the BBC, Faisal Islam and Jonathan Josephs describe the IMF’s assertions and the British government’s response.

The International Monetary Fund (IMF) has “advised the UK against further tax cuts”… It said preserving public services and investment implied higher spending than was reflected in the government’s current plans. The IMF suggested the Treasury’s pencilled-in spending cuts from this year were unrealistic. …Commenting on the IMF’s advice, Mr Hunt said: “The IMF expect growth to strengthen over the next few years, supported by our introduction of the biggest capital investment tax reliefs anywhere in the world, alongside National Insurance cuts to improve work incentives. “It is too early to know whether further reductions in tax will be affordable in the Budget, but we continue to believe that smart tax reductions can make a big difference in boosting growth.”

I have two reactions.

First, the United Kingdom is in trouble because of excessive spending and it is (predictably) disappointing that the IMF actually wants an even bigger burden of government financed by even higher taxes.

Second, I have zero sympathy for the U.K.’s supposedly conservative government, which is only contemplating tax cuts as an election-year stunt in hopes voters will forget its track record of bad fiscal policy.

Indeed, a squabble between the IMF and the current British government reminds me of the fight more than 10 years ago between the IMF and the European Commission. The best that can be hoped for is plenty of casualties on both sides.

P.S. I can’t resist sharing one additional excerpt.

…economic forecasters are not always right when it comes to predicting the future. The IMF has previously stated its forecasts for most advanced economies, such as the UK’s, have more often than not been within about 1.5 percentage points of what actually happens.

Unfortunately, the world has plenty of people who are not sensible (or who have a self-interested reason to make senseless arguments). And some of them have congregated at the International Monetary Fund.

That bureaucracy recently published its recipe for economic development and – keeping with long-standing IMF tradition – endorsed massive tax increases for poor nations. Here’s their main recommendation.

You may be wondering why IMF bureaucrats want to make life more difficult for people in developing nations.

Here’s some of what was written by Vitor Gaspar, Mario Mansour, and Charles Vellutini.

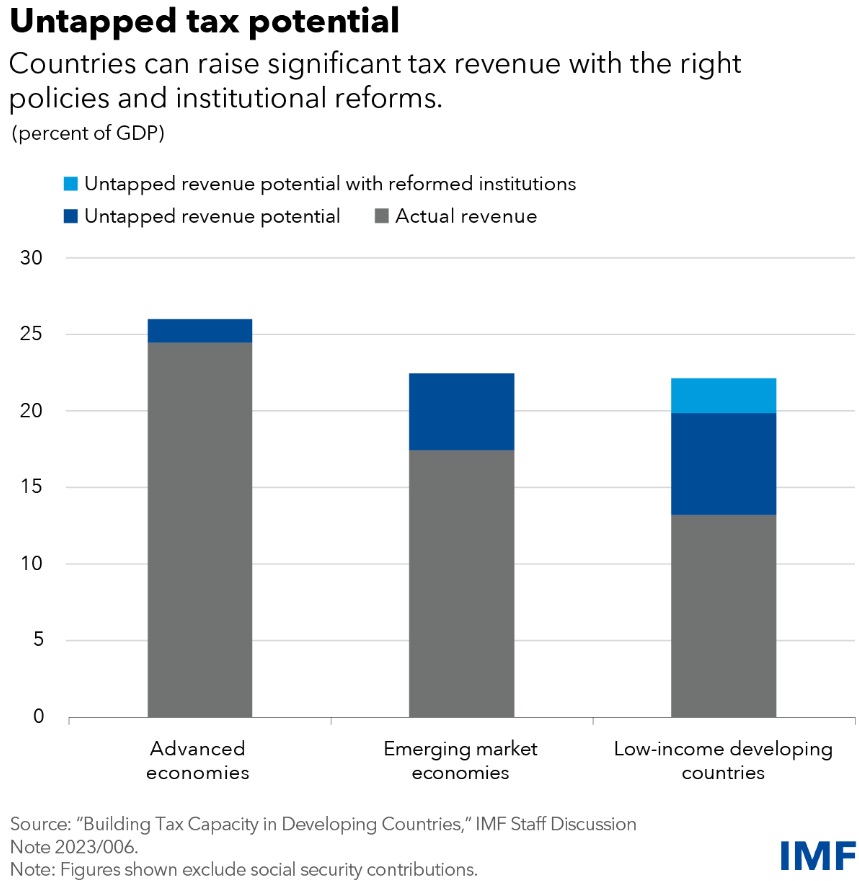

Emerging markets and developing economies need $3 trillion annually through 2030 to finance their development goals … That amounts to about 7 percent of these countries’ combined 2022 gross domestic product and poses a formidable challenge… Our new research finds that many countries have the potential to increase their tax-to-GDP ratios—enabling them to provide critical government services—by as much as 9 percentage points… Countries have considerable room to collect more revenue based on their tax potential… We find that low-income countries could raise their tax-to-GDP ratio by as much as 6.7 percentage points on average. …The total revenue-raising potential, at 9 percentage points of GDP—a staggering two-thirds increase relative to their tax-to-GDP ratio in 2020… Similarly, emerging market economies can raise their tax-to-GDP ratio by 5 percentage points on average.

There are two things to address in the above excerpt.

First is it possible that developing nations, with sufficient “tax effort,” can increase their tax burdens by an average of 9 percentage points of GDP? Perhaps.

Second (and far more important), would that be a good idea? For people who care about empirical reality, definitely not.

Allow me to briefly elaborate on this second point. Bureaucrats at the IMF want readers to blindly accept the assertion that $3 trillion of additional tax revenue will help achieve development goals.

Why don’t they offer any evidence? Why have not responded to my repeated requests to provide at least one example of a country that got rich by increasing fiscal burdens?

P.P.S. To give the IMF credit, the bureaucrats don’t discriminate. Yes, they push for bad fiscal policy in relatively poor parts of Africa, Asia, and Latin America, but they also argue for higher taxes and bigger government in relatively rich places, like Japan, Europe, and the United States.

The title of that column was “The Most Economically Illiterate Tweet of 2023?” and you may wonder why I hedged by including a question mark.

I hedged because of a nagging suspicion that I would see an even dumber tweet before the end of the year.

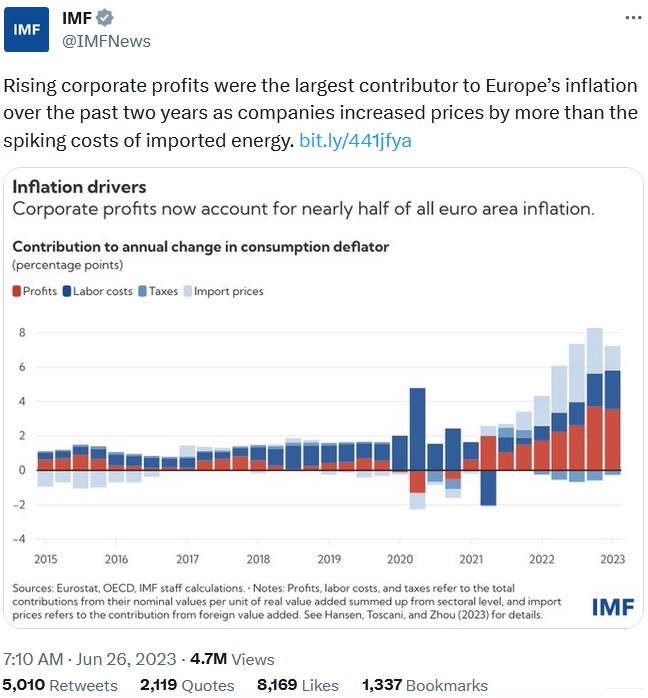

Well, I only need to wait a couple of weeks. The International Monetary Fund issued this tweet and it unquestionably wins the “prize” for economic illiteracy.

The ECB made the same mistake as the Federal Reserve, dramatically increasing the supply of money as a panicked response to the pandemic.

That’s forgivable. But the ECB (like the Fed) kept dumping money into the economy even after it became obvious that the pandemic wasn’t going to cause an economic collapse.

At the risk of understatement, central banks are responsible for inflation. The fact that some of that inflation has shown up as corporate profits is not meaningful.

P.S. The unanswered question is why the IMF would publish such a maliciously misleading and inaccurate tweet. I’m guessing it is because the IMF represents the interests of governments. And since politicians would rather blame corporations for inflation than accept responsibility for their subpar appointees to central banks, the IMF did their bidding. Yet another reason to shut down this bureaucracy. In any event, I feel sorry for the economists at that bureaucracy, most of whom must be embarrassed.

Yesterday’s column reviewed a new report from the International Monetary Fund and criticized that bureaucracy for celebrating how the world’s most-powerful governments are going to take more money from the private sector thanks to a corporate tax cartel.

But that’s not the worst part of the IMF document.

The report also asserts that low-income countries (LICs) can grow faster if they increase their fiscal burdens.

This is not April Fool’s Day. I’m not joking. The bureaucrats at the IMF apparently want readers to believe that higher taxes and more spending are a route to prosperity.

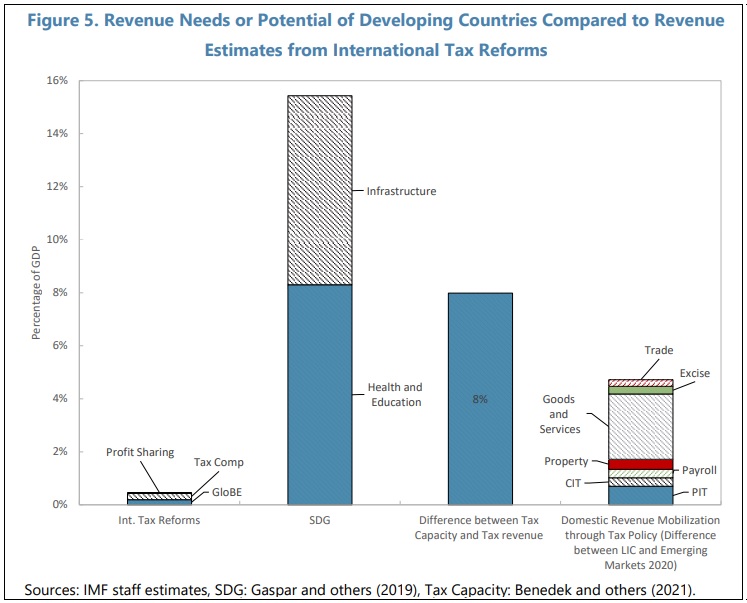

Global revenue from the 2-pillar reform…might rise to around 0.4 percent of GDP in the longer term. If a proportional share of this revenue flows to LICs, this would provide a welcome contribution to their revenue objective. However, the impact is dwarfed by the…expenditure needs in LICs of nearly 16 percent of GDP (and a significant share of this will need to come from taxation)… Estimates…suggest a potential revenue increase in LICs of 8 percent of GDP. …compared with that in emerging market economies as an aspirational level…suggests a revenue potential of around 5 percent of GDP. …Several options present themselves to raise revenues in LICs, both in tax policy and revenue administration. …Some promising avenues in tax policy include: Value-Added Tax (VAT)…specific excises…on select products such as alcohol, tobacco, unhealthy foods, passenger vehicles, fuel, and carbon emissions. …Strengthening the progressive personal income tax… Making greater use of recurrent real property taxes.

Here’s a chart from the study which shows how much bigger the IMF thinks government should be in poor nations (the second column) compared to various potential sources of revenue (columns 1, 3, and 4).

For those not familiar with the jargon, “SDG” is the abbreviation for “sustainable development goals,” as defined by the United Nations.

And the UN now robotically asserts that more taxes are needed to government can boost growth with more spending (other international bureaucracies sing from the same songsheet).

I actually went to the United Nations a few years ago and explained why this “magic beans” theory of government-led economic development is wrong.

Simply stated, there are two parts of the world that have become rich and in both cases prosperity arose when government was far smaller than what the IMF and UN want us to believe is necessary.

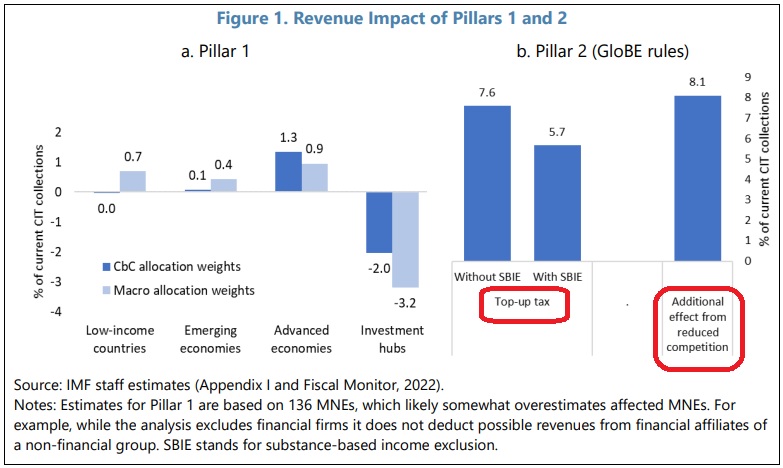

P1 is estimated to reallocate about 2 percent of total profits of MNEs, mainly from low-tax investment hubs to other countries, raising global Corporate Income Tax (CIT) revenue by $12 billion. …P2 would raise global CIT revenues by 5.7 percent, which is before any behavioral responses by firms (Figure 1b). According to staff simulations, 18.5 percent of global profit of MNEs is taxed below 15 percent ($1.47 trillion in 2019). On average, the current tax rate on these profits is 5 percent, so that profits exceeding the substance-based income exclusion would be subjected to a average top-up tax of 10 percent. …An additional positive revenue impact from P2 could come from reduced competition over corporate tax rates, which could boost global CIT revenues by an extra 8.1 percent. …a 1 percentage point increase in the world average CIT rate will, on average, induce a country to raise its own rate by 0.6 percentage points. By putting a floor of 15 percent, the simulations above suggest that 18.5 percent of MNE profit will indeed face a higher CIT burden, implying that countries will feel less pressure to keep their own tax rates low. Using simulations of the tax competition model, we find that the average CIT rate would rise from 22.2 to 24.3 percent due to the global minimum tax. The associated boost in global CIT revenues would be 8.1 percent, exceeding the direct effect on revenue.

By the way P1 is Pillar 1, which is the proposal to give powerful nations a bigger claim on the taxable income of big companies. By contrast, P2 is Pillar 2, which is the proposal for a mandatory minimum tax of at least 15 percent on corporate income.

Second, we should all be outraged that IMF bureaucrats (including the authors of the paper cited above) receive tax-free salaries while pushing for higher taxes on the rest of us.

But I am vaguely hopeful that things may get better. More specifically, Argentina almost surely will suffer a major collapse at some point in the future.

When that happens, the only option will be liberalization. Simply stated, politicians no longer will have any ability to pillage the private sector (sort of like the Soviet Union and Eastern Europe when communism collapsed).

Naomi Klein views this scenario as “disaster capitalism,” but it’s the only hope for Argentina.

But there’s a catch. Politicians in Buenos Aires will only be forced to reform if they don’t get another bailout from the International Monetary Fund.

Unfortunately, there are (according to Professor Steve Hanke) 22 reasons to expect the IMF to do the wrong thing.

The bureaucrats at that international bureaucracy have a terrible track record of rewarding Argentina when it gets in fiscal trouble.

I wrote just last month that Italy is getting closer and closer to a fiscal crisis and I warned that the IMF may intervene to prop up that country’s bad policy. And when other European countries get in trouble, IMF bureaucrats will probably try to make a bad situation even worse with further bailouts.

It graphically illustrates why politicians are wrong if they think you can double tax revenue by doubling tax rates (or that revenues will drop by 50 percent if tax rates are cut in half).

In cases where taxpayers have a lot of control over the timing, level, and composition of their income, changes in tax rates may cause big changes in taxable income (or “tax base” in the jargon of economists).

Today, we are going to see that the pro-tax International Monetary Fund also admits there is a Laffer Curve.

Indeed, a new study authored by David Amaglobeli, Valerio Crispolti, and Xuguang Simon Sheng openly states that politicians should be very cognizant of the fact that some tax policy changes can have a big effect on the “tax base.”

This paper investigates the potential revenue impact of different tax policy changes using the Tax Policy Reform Database (TPRD)… Revenue responses to tax policy changes depend on many factors… However, one of most important factors is the nature of the tax policy change itself. For example, while a tax rate cut will directly lower revenue intake, it could also encourage more economic activity, hence expand the tax base. Estimating the revenue response to a tax policy change, therefore, requires granular information on the nature of this change, including on the tax instrument used (e.g., VAT or personal income tax), the type of change adopted (e.g., tax base, tax rate), and its timing and size.

Here are some of the findings.

We assess the impact of tax policy changes on tax revenues using Jordà (2005)’s local projections method. Our baseline results are based on tax shocks identified in the year when a tax change is announced. Our main empirical findings suggest that the revenue yield of tax policy changes varies significantly across taxes and types of changes, with tax rate changes generally having a more transitory revenue impact than tax base changes for most taxes. Specifically, base broadening changes in PIT, CIT, EXE, and PRO have on average a more significant and long-lasting impact on tax collection than rate changes. At the same time, rate hikes have relatively more significant effects on taxes in the case of VAT and SSC measures.

Gechert and Groß (2019) conclude that measures to broaden the tax base are less harmful to economic growth than tax hikes. Dabla-Norris and Lima (2018) find that during fiscal consolidations, tax base-broadening measures lead to smaller output and employment declines compared to measures to increase tax rates.

And we learn that it is very foolish to raise corporate tax rates.

Mertens and Ravn (2013) find that…increases in CIT are approximately revenue neutral for the United States. …Announcements of CIT increases are associated with a somewhat transitory rise in tax collection, suggesting that companies have quickly adapted their business to reduce the tax burden.

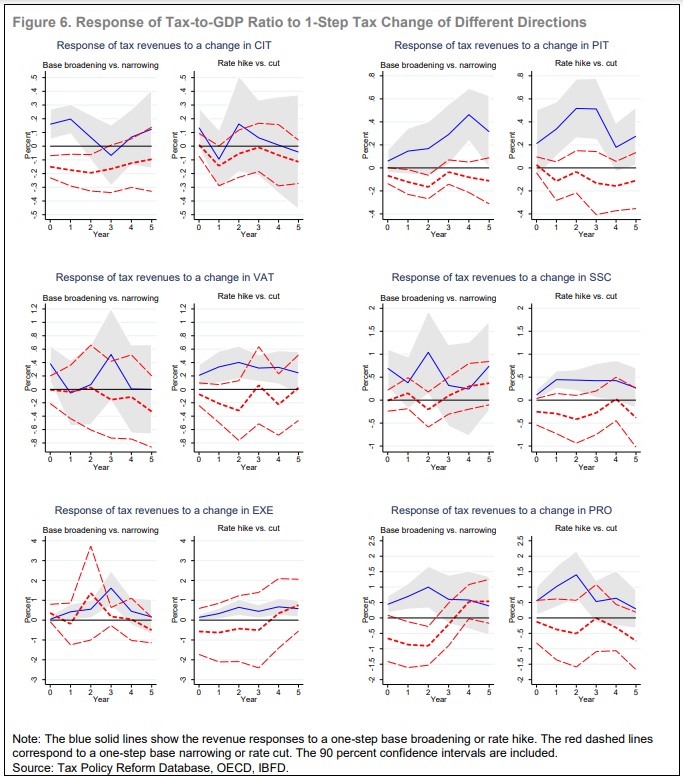

For wonky readers, here’s a chart from the study. Note how, in many cases, there’s not much difference in revenue between tax increases (blue line) and tax cuts (red lines).

P.S. One big takeaway is that there is not a single Laffer Curve. There are multiple Laffer Curves depending on the tax that’s being changed and the ability of taxpayers to change their behavior.

P.P.S. A less-obvious takeaway is that class-warfare taxes cause the most economic damage, meaning the most harm to ordinary people.

P.P.P.S. You can call it the “Khaldun Curve” if you prefer.

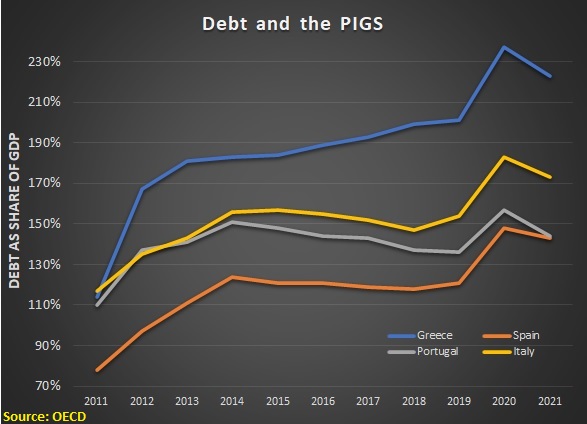

Today, here are my thoughts on why there should not be a bailout if/when a crisis occurs.

I have moral objections to bailouts, but let’s focus in this column on the practical impact.

And let’s start with this chart, which shows debt levels in Portugal, Italy, Greece, and Spain (the so-called PIGS) ever since the misguided bailout of Greece about a dozen years ago.

As you can see, OECD data reveals that there’s been no change in these poorly governed nations. They have continued to over-spend and accumulate ever-higher levels of debt.

Defenders of bailouts assert that Greece was forced to engage in “austerity” as a condition of getting a bailout.

I have two problems with that argument.

First, notice how Greece’s debt has continued to go up. If that’s a success, I would hate to see an example of failure.

Second, the main effect of the so-called austerity is a much higher tax burden and a somewhat higher spending burden.

If there’s a bailout of Italy (or any other nation), I suspect we’ll see the same thing happen. Higher taxes, higher spending, and higher debt.

I’ll close by acknowledging that there are costs to my approach. If Italy is not given a bailout, the country may have a “disorderly default,” meaning the government simply stops honoring its commitments to pay bondholders.

That is bad for individual bondholders, but it also could hurt – or even bankrupt – financial institutions that foolishly decided to buy a lot of Italian government bonds.

But there should be consequences for imprudent choices. Especially if the alternative is bailouts that misallocate global capital and encourage further bad behavior.

The bottom line is that the long-run damage of bailouts is much greater than the long-run damage of defaults.

The latest example of IMF misbehavior revolves around the bureaucracy’s criticism of recently announced tax cuts in the United Kingdom.

A BBCreport by Natalie Sherman and Tom Espiner summarizes the controversy.

The International Monetary Fund has openly criticised the UK government over its plan for tax cuts…In an unusually outspoken statement, the IMF said the proposal was likely to increase inequality and add to pressures pushing up prices. …Chancellor Kwasi Kwarteng unveiled the country’s biggest tax package in 50 years on Friday. But the £45bn cut has sparked fears that government borrowing could surge along with interest rates. …Lord Frost, the former Brexit minister and close ally of Prime Minister Liz Truss, criticised the IMF’s statement. …”The IMF has consistently advocated highly conventional economic policies. It is following this approach that has produced years of slow growth and weak productivity. The only way forward for Britain is lower taxes, spending restraint, and significant economic reform.” …Moody’s credit rating agency said on Wednesday that the UK’s plan for “large unfunded tax cuts” was “credit negative” and would lead to higher, persistent deficits “amid rising borrowing costs [and] a weaker growth outlook”. Moody’s did not change the UK’s credit rating.

So what should be done about the IMF’s misguided interference?

Writing for the Spectator in the U.K., Kate Andrews has some observations about the underlying philosophical and ideological conflict..

…the International Monetary Fund has weighed in on the UK’s mini-Budget, offering a direct rebuke of Liz Truss and Kwasi Kwarteng’s tax cuts. …its spokesperson said…‘Given elevated inflation pressures in many countries, including the UK, we do not recommend large and untargeted fiscal packages at this juncture’… But this rebuke from the IMF is the kind of battle the Truss camp might be happy to have. …The IMF takes a political stance on inequality, viewing its reduction as a good thing in itself. Truss and Kwarteng reject this premise – summed up in the Chancellor’s statement last Friday when he called for the end of redistribution politics – and think it’s far more important to focus on ‘growing the size of the pie.’ The IMF’s ‘intervention’ is likely to become an example of the ‘Treasury orthodoxy’ that Truss was so vocal about during the leadership campaign: her belief that a left-wing economic consensus will not tolerate any meaningful shake-up of the tax code or supply-side reform.

Truss and Kwarteng are correct to reject the IMF’s foolish – and immoral – fixation on inequality.

All you really need to know is that the IMF publishes research implying it is okay to hurt poor people if rich people are hurt by a greater amount.

Let’s close by addressing whether tax cuts are bad for Britain’s currency and financial markets

Paul Marshall explained the interaction (and non-interaction) of fiscal and monetary policy in a column for the U.K.-based Financial Times.

Since 2010, the G7 policy framework has been one of tight fiscal and loose monetary policy. …This combination of fiscal austerity and monetary largesse has not been a success. Austerity has not prevented government debt ratios steadily climbing to historic highs. …Meanwhile quantitative easing has fuelled asset inflation for the super-rich and has more or less abolished risk pricing in financial markets. And…it has produced inflation which is still out of control. But now the global policy consensus is in the process of pivoting… A distinctive feature of the UK’s fiscal pivot is the emphasis on reducing the burden of tax on work and business. This is sensible. …the bigger problem for Liz Truss’s government is the Bank of England. It seems that the governor, Andrew Bailey, did not get the memo. Our central bank has been behind the curve since inflation first started to rise sharply in 2021. …The Bank of England effectively lost control of the UK bond market last Thursday when it raised interest rates by 50 basis points, instead of the 75bp that the US Federal Reserve and the European Central Bank raised by. Its timidity is now having an impact on both the gilt market and sterling. That is the essential context for the market reaction to the mini-Budget. Once you lose market confidence, it is doubly hard to win it back. …a more muscular stance from the BoE to underpin financial market confidence in the UK, even at the expense of some short-term pain.

He is right.

The Bank of England should be focused on trying to unwind its mistaken monetary policy that produced rising prices. That’s the approach that will strengthen the currency.

And Truss and Kwarteng should continue their efforts for better tax policy so the economy can grow faster.

Even though they ostensibly exist to promote economic growth, the International Monetary Fund (IMF) and Organization for Economic Cooperation and Development (OECD) have an unfortunate track record of promoting higher taxes and bigger government.

Not that we should be surprised. IMF and OECD officials get very comfortable (and tax-free!) salaries, so they have a “public choice” incentive to reflect the wishes of the politicians who control their purse strings.

But understanding the incentives of international bureaucrats definitely does not mean we should give them a free pass when they push bad policy.

And that’s exactly what the IMF and OECD are doing in Latin America.

Consider, for instance, the new IMF report on “Tax Policy for Inclusive Growth in Latin America and the Caribbean.” The authors (Santiago Acosta-Ormaechea, Samuel Pienknagura, and Carlo Pizzinelli) apparently think those struggling nations will grow faster if there is a bigger burden of government.

…fiscal policy…is not progressive enough… This paper presents a detailed assessment of tax structures in LAC and outlines reform options to improve collection… Specific tax design features are then assessed, inspecting how the taxation of capital and labor can be improved…to both increase revenue and provide a more equitable tax structure… Evidence for LA7 countries shows that better PIT design could bring significant gains in collection and equity. … Potentially adverse growth impacts could be mitigated by providing well-targeted incentives to labor force participation of low-wage earners through an earned income tax credit… Increasing the tax burden on certain non-labor income sources (e.g., capital gains) would also raise PIT revenue and improve equity… Other untapped revenue sources should be considered more forcefully, including the taxation of immovable property, inheritance taxes, and environmental taxes.

As illustrated by Figure 1 from the report, one of the clear messages is that Latin American countries should be more like high-tax countries in Western Europe.

What the authors overlook, however, is that the (relatively) rich countries in Western Europe became rich when the burden of government was very small.

The LEO 2021 provides tailored policy messages to help stakeholders take action and build forward better. …it highlights the need to learn from the pandemic and mainstream some of the social policy innovations adopted throughout the crisis to strengthen social protection systems and improve quality and accessibility of public services. …a set of tax policy options could increase revenues… there needs to be greater resource mobilisation…in most LAC countries, which in turn implies greater progressivity of the taxation system… the average tax-to-GDP ratio in the LAC region was 22.9% in 2019, considerably below the OECD average of 33.8%… Countries may need to consider additional ways of raising revenues… PIT is the principal factor behind the tax gap between LAC and the OECD, limiting not only potential revenues but also the redistributive power of the tax system… taxation of immovable property…and of individuals’ capital gains, should contribute to increasing revenues to finance the recovery and improve the progressivity of the taxation system. Other measures include wealth and inheritance taxes.

Table 1 from the report summarizes the “new social contract” that the OECD is advocating.

All you need to understand is that “strengthening social protection systems and public services” is bureaucrat-speak for more government spending and “developing fairer and stronger tax systems” is bureaucrat-speak for higher taxes and class warfare.

I’ll close by calling your attention to this video explaining the ideal fiscal policy for nations in the developing world.

But remember that fiscal policy is just one piece of the puzzle, so I also recommend this video and this video if you want a full understanding of the policies that are needed to create broadly shared prosperity.

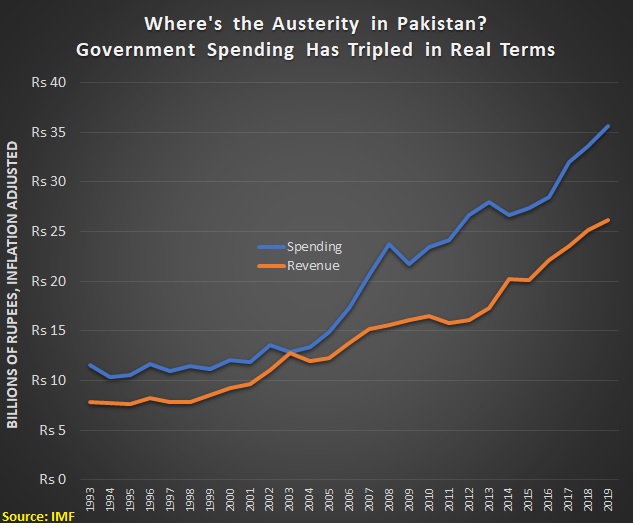

I realize few readers are interested in small, faraway countries. But I periodically write about nations such as Jordan, Cyprus, Latvia, Vanuatu, Panama, and Pakistan because they offer important lessons – mostly negative, but sometimes positive – about fiscal policy.

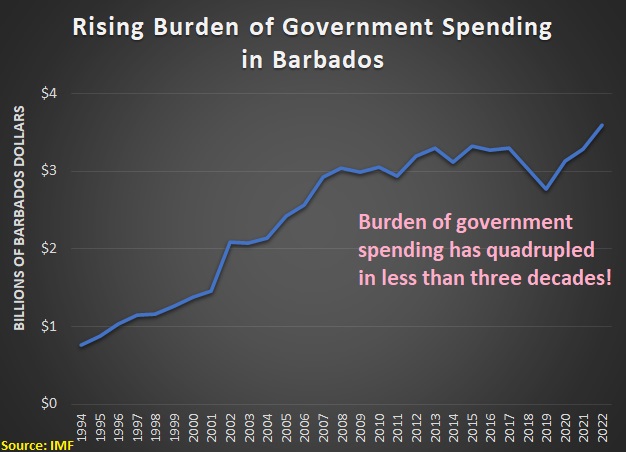

Today, let’s see what we can learn from Barbados.

That island nation in the Caribbean wound up in fiscal trouble a few years ago and Abrahm Lustgarten of the New York Times wrote a lengthy article last week about that experience.

Here’s the situation as of 2018.

Barbados was out of money. It was so broke that it was taking out new loans just to pay the interest on the old ones, even as its infrastructure was coming undone. Soon the nation would have no choice but to declare itself insolvent, instigating a battle with the dozens of banks and creditors that held its $8 billion in debt and triggering austerity measures that would spiral the island into further poverty. …Mottley, the first woman to lead Barbados, had been working…to develop a plan that would restructure the country’s soaring debts in a way that would free up money to invest in Barbados’s economy.

While the preceding excerpts are mostly to illustrate what was happening, I can’t resist two editorial comments.

Second, government spending rarelyacts as productive investment.

Now let’s get back to the story.

Prime Minister Mottley’s plan involved going to the International Monetary Fund, then headed by Christine Lagarde, for a bailout.

Mottley knew that banks and investors would work with her only if Barbados were participating in a formal I.M.F. program… Mottley wanted Lagarde to endorse an economic program that would still allow her to raise salaries of civil servants, build schools and improve piping and wiring for water and power. …No one was sure how Lagarde would respond. Would she trust Mottley to spend on Barbados first? …the director’s surprising reply: She was extremely supportive of what Mottley was proposing.

Needless to say, I don’t like bailouts. And a bailout that enables more government spending seems especially foolish.

But I like to check the numbers before making sweeping pronouncements.

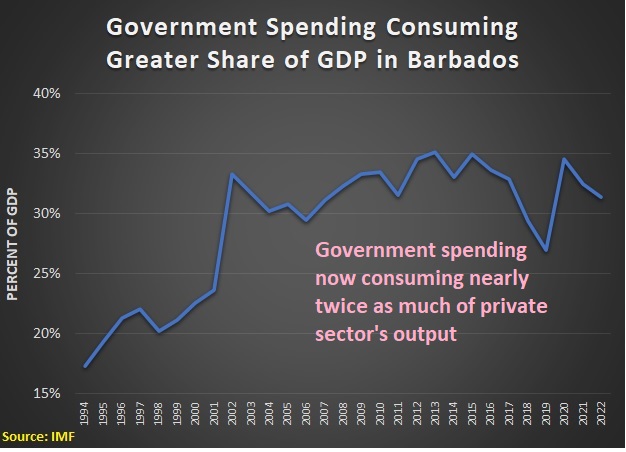

So let’s see whether Barbados somehow was being hurt by inadequate levels of government spending.

But it turns out that total government spending today is more than four times greater than it was in 1994.

And if we look at government spending as a share of gross domestic product, we can see that government has nearly doubled in size.

To be fair to Ms. Mottley, the politicians in office from 1994-2008 were the most profligate.

But none of that changes the fact that government is far bigger today than it was in the recent past. So the notion that Barbados needs a bigger government budget is nonsense.

Sadly, the reporter did not bother to share any of these numbers. Indeed, in a story that ran more than 10,000 words, there were only 50 words that even hinted at the real problem.

…a mixture of poor management and corruption had eroded the country’s economy. …the country had developed a “dysfunctional” fiscal culture in which government agencies and departments took loans and negotiated deals without consulting the central bank, accumulating sprawling debt… The country’s response was to print more money and borrow more.

I’ll close by observing that Barbados never would have gotten into trouble if it had a Swiss-stylespending cap. If government spending had been allowed to grow only 3 percent each year starting in 1994, Barbados would be enjoyed a huge budget surplus today.

P.S. Ironically, economists at the IMF have written in favor of spending caps on multiple occasions. Too bad the political hacks in charge of the bureaucracy don’t pay attention to that research.

To be fair, there are some good fiscal economists at the IMF (even with regards to tax policy), but the political types who run the bureaucracy almost always ignore their research.

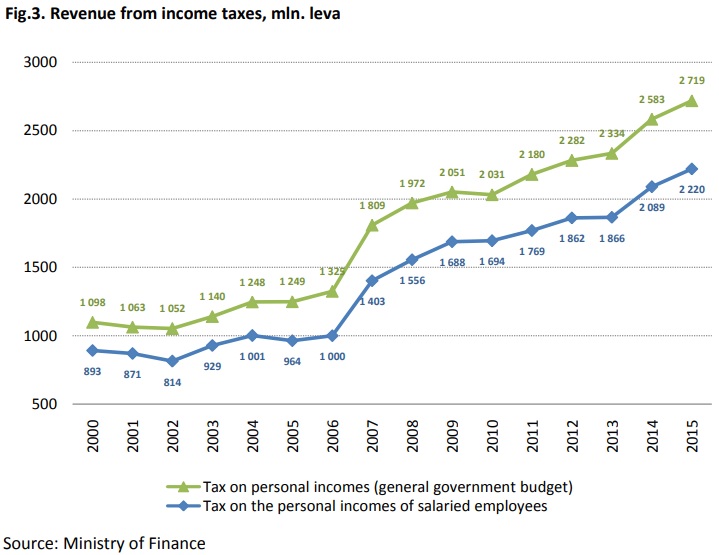

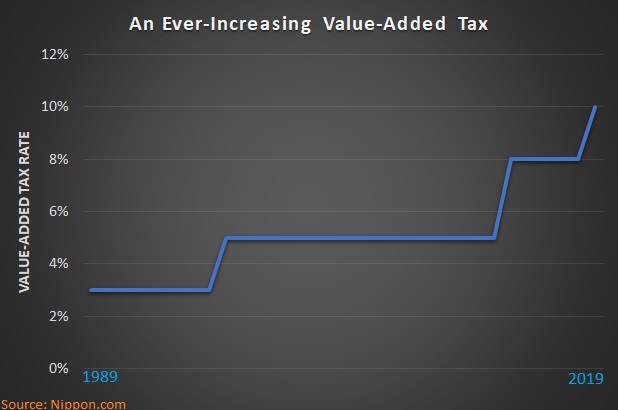

The latest example if that the IMF is pressuring Bulgaria to replace its flat tax with a system based on discriminatory rates.

Fiscal policy needs to be flexible given the large uncertainty, but some changes are already advisable in the mid-year budget revision. …Room to address long-term social and investment needs could be significantly increased by…Reviewing the tax system to increase revenue and redistribution . A reform of the low flat personal income tax rate could help create fiscal space and reduce inequalities.

By the way, just in case it’s not obvious, “social and investment needs” is bureaucrat-speak for more redistribution spending.

Some of you may be wondering whether a new system is needed because the flat tax caused a big drop in revenue.

But as you can see from this chart, income tax revenues continued to grow after the flat tax was approved in 2008.

I’ll close by noting that Bulgaria is ranked #36 in the latest edition of Economic Freedom of the World, which is a good but not great score.

But it gets its lowest score for “size of government,” which is the measure for fiscal policy. The flat income tax is a positive, of course, but that policy is offset by low scores for other features of fiscal policy (payroll tax, redistribution, etc).

So the bottom line is that the IMF wants to get rid of the good part of Bulgaria’s fiscal policy and drive its overall score even lower.

Why is this unfortunate? Because there are some policy changes that may be costly in the short run, but they are nonetheless very worthwhile because they generate big long-run benefits.

Messy fights over the debt limit create (almost certainly exaggerated) concerns about potential default, but that potential cost would be trivial compared to the long-run benefits of figuring out how to limit the growing burden of federal spending.

I offer the above examples because similar short-run and long-run tradeoffs exist when looking at what happens when the International Monetary Fund provides bailouts for profligate governments.

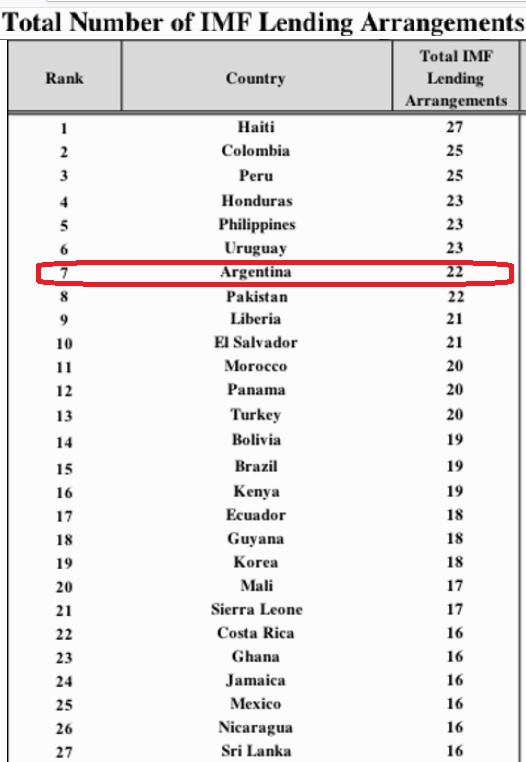

The Economist has an article that perfectly illustrates the IMF’s pernicious role.

The year was 1958. …Argentina turned to the fund for its first “standby arrangement”, a line of credit accompanied by a plan to stabilise the economy. …Sixty years later, in June 2018, Argentina was back for its 21st arrangement: a $50bn loan, later increased to $57bn, backed by the government’s promises to cut the budget deficit and strengthen the central bank in the hope of quelling inflation and stabilising the peso. The loan was the largest in the imf’s history. …Despite its size, the rescue failed to save Argentina from default and despair. …Foreign capital kept retreating, the peso kept falling and inflation kept rising. The evaluation speculates that the size of the imf’s loan may even have been “self-defeating”, eroding confidence rather than inspiring it.

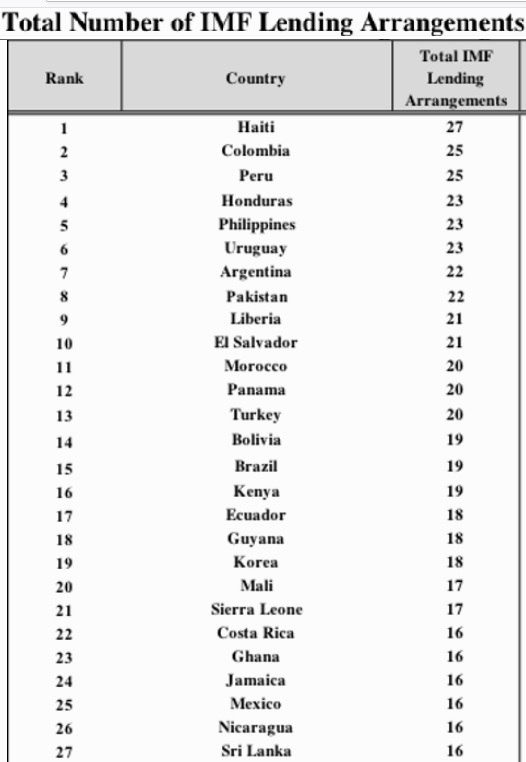

Just in case you missed it, the article mentions that Argentina has received 21 different bailouts since 1958, which works out to be one bailout every three years (Professor Steve Hanke counts 22 bailouts, for what it’s worth).

In probably every case, IMF bureaucrats presumably thought a bailout was a way of minimizing economic pain (and they probably thought the same thing for dozens of bailouts provided to Haiti, Colombia, Peru, Honduras, Philippines, etc).

But what actually has happened is that politicians – in Argentina and elsewhere – have learned that it’s okay to pursue bad policy because there’s always another bailout.

In other words, IMF policy is a glaring example of “moral hazard.” By shielding politicians from the consequences of bad policy, the bureaucracy is actually encouraging those politicians to engage in additional bad policy.

To be blunt, the IMF is the arsonist rather than the firefighter.

The article in the Economist included this observation.

Conservative critics think the fund has been seduced by its dance partner, wasting public money in a futile battle.

My right-leaning friends are correct, but their criticisms are too mild.

It’s not just that the IMF is wasting money. It’s dampening growth by pushing policies that misallocate capital.

Here’s what should have happened to Argentina in 1958 (and what should have happened in 2018, and what should happen when there’s pressure for yet another bailout).

The politicians in Argentina who spend excessively should learn that there’s a tipping point when they can no longer borrow.

The interest groups in Argentina should learn that parasites also suffer when they kill their host animal by being too greedy.

The voters in Argentina should learn that there are serious adverse consequences when you elect “Peronist” politicians.

Sadly, none of these lessons get learned so long as the IMF is standing by to provide never-ending bailouts.

So instead of some short-run pain, which is then offset by better long-run policy, we get bailouts that mask short-run pain and encourage more long-run damage.

P.P.S. To be fair, the IMF recommends tax increases even in the years when bailouts aren’t needed, so at least the bureaucrats have a consistent (albeit nutty) message.

Needless to say, that approach doesn’t work. The best evidence is that many governments wind up in a never-ending cycle of tax-spend-debt-crisis-bailout, followed by further rounds of tax-spend-debt-crisis-bailout.

Moreover, the net effect of these policies is to divert capital from the economy’s productive sector. So it’s the economic equivalent of a lose-lose policy.

When criticizing the IMF, I usually focus on how the bureaucrats relentlessly urge higher taxes. Indeed, I often complain about how the bailouts are provided only if countries agree to raise taxes (another lose-lose situation).

Today, though, I want to write about another bad IMF policy. Earlier this year, the bureaucrats (with support from the Biden Administration) allocated $650 billion of new Special Drawing Rights (SDRs) – sort of a version of IMF-created money.

You can learn about SDRs by clicking here and here, so I won’t bore people with a description of how they work.

For purposes of our discussion, what matters is that the IMF uses SDRs to enable more government spending.

And that’s not a recipe for prosperity, either for national economies or the global economy.

Earlier this year, Mary Anastasia O’Grady of the Wall Street Journalhighlighted how SDRs are rewarding very dodgy governments in Latin America.

Nicaraguan dictator Daniel Ortega is jailing, killing and disappearing his political opponents. …At the International Monetary Fund, he’s a valued member. So too are the governments of socialist, deadbeat Argentina and of El Salvador, which every day slips further into arbitrary, authoritarian rule. These are some of the bad actors in the Western Hemisphere who received more “special drawing rights” from the IMF on Aug. 23 as part of a new $650 billion general allocation. …SDRs are created out of thin air but can be converted, on demand, into hard currency. …Treasury Secretary Janet Yellen, who led the charge for this new round of SDRs, claims the transaction is cost-free… In fact, the conversion of SDRs to dollars is a subsidized, perpetual loan. For poor countries the subsidy is above 90% of the loan value. …There was a time when large multilateral handouts were conditioned on attempts at good governance. Those days are gone.

In a column last month for the Wall Street Journal, D.J. Nordquist and Dan Katz also analyzed the impact of the IMF’s policy.

…the International Monetary Fund announced in August a new general allocation of special drawing rights equivalent to $650 billion. …All IMF members, even rogue nations, receive them, so Iran got some $5 billion and Belarus $1 billion. …The allocation added more than $17 billion to Russia’s record-high reserves…the IMF and other proponents justified the SDR allocation on grounds that its benefits outweighed the harms… But because of the IMF shareholding formula… Only 3% of the general allocation flowed to low-income countries. …the IMF publicly indicated it would collaborate with the World Bank and other international financial institutions to ensure that SDRs were put to productive uses… Unfortunately, the IMF appears to have fallen into a classic trap of international organizations: acting based on aspirations rather than binding agreements. …Public confidence in international financial institutions has been understandably shaken as a result of corruption investigations into the IMF’s emergency pandemic-relief loans, theft of World Bank assistance by elite government officials, and serious questions regarding inappropriate Chinese influence at the World Bank, the World Health Organization, and elsewhere.

I’ll close by noting that SDRs are a great deal for politicians and bureaucrats. They get more spending, all of which seems free. And since almost nobody understands how this racket works, there’s near-zero democratic accountability.

P.S. Shifting gears, here’s are some excerpts from an article on the IMF’s website. It has nothing to do with the SDR issue, but it is a window into the the IMF’s statist mindset. The bureaucracy is lauding an economist, Mariana Mazzucato, who argues for industrial policy.

Mazzucato has been stirring the pot in economics and public policy for nearly a decade. Her main message is that governments around the world need to seize their power to lead innovation for the betterment of humanity. …Government is for setting big goals, defining the missions necessary for achieving them, encouraging and investing in innovation, and governing the process so that the public benefits. …She made the case for rethinking the role of government in her 2013 book, The Entrepreneurial State: Debunking Public vs. Private Sector Myths. …“State capacity has really been hollowed out because of the narrow way that we think about the state,” she says. …That’s particularly evident in the United Kingdom and the United States, where political leaders defunded public health and devalued government itself, eroding public trust and government’s capacity to respond to crises, she says. …Mazzucato urged “citizens’ dividends” and government equity stakes in businesses linked to government funding.

P.P.S. There are many good economists who work at the IMF and they often produce high-quality research (see here, here, here, here, here, here, here, here, here, and here). Sadly, their sensible analyses doesn’t seem to have any impact on the policy decisions of the organization’s top bureaucrats.

My reason for revisiting this topic is a story in the Economist about the possibility of an “grossly uneven” recovery, as illustrated by this chart.

My knee-jerk reaction to this chart is that nobody should pay attention to economic forecasters for the simple reason that they have a terrible track record.

Or it may simply reflect the fact that it’s basically impossible to make such predictions (if any economists actually had that ability, they would be billionaires).

Instead, I want to focus on this issue of whether rich countries should be blamed for being richer than poor countries.

Here’s some of what the Economist wrote.

Over the longer term, the economic recovery is projected to remain grossly uneven. That, the fund argues, reflects…variations in fiscal largesse. In 2020 rich and poor countries alike loosened the purse-strings to protect households and businesses from the impact of lockdowns. This year fiscal support in the rich world is projected to remain broadly as generous as it was last year, allowing time for the private sector to get back on its feet (and, some economists would argue, even leading to some overheating in America). Emerging markets, by contrast, have shrunk their budget deficits (adjusted for the economic cycle, and before interest payments). The result will be a two-speed global economy. Output in the rich world is expected to return to its pre-pandemic trend by next year, and then to rise slightly above it. For the rest of the world, however, gdp is expected to remain well below trend at least until 2025.

As you can see from the excerpt, the IMF is wedded to the Keynesian view that government spending supposedly is good for growth – notwithstanding all the real-world evidence to the contrary.

But I’m more interested in the two points that aren’t mentioned, both of which revolve around the strong link between economic liberty and national prosperity.

First, rich countries tend to be rich because they have (or had) good economic policy.

Second, poor countries fail to converge because they tend to have bad economic policy.

The bottom line is that the global economy is not a fixed pie. If there are “grossly uneven” growth rates in the world, the reason is that some nations don’t follow the prudent recipe for prosperity.

But the biggest problem with the IMF is that it promotes “moral hazard.” More specifically, it provides bailouts for irresponsible governments and for those who foolishly lend to those governments.

All of which explains why some nations (and their foolish lenders) have received dozens of bailouts.

Oh, and let’s not forget that these endless bailouts also lead to a misallocation of capital, thus reducing global growth.

In an article for the New York Times, Patricia Cohen reports on discussions to expand the IMF’s powers.

Once narrowly viewed as a financial watchdog and a first responder to countries in financial crises, the I.M.F. has more recently helped manage two of the biggest risks to the worldwide economy: the extreme inequality and climate change. …long-held beliefs like the single-minded focus on how much an economy grows, without regard to problems like inequality and environmental damage, are widely considered outdated. And the preferred cocktail for helping debt-ridden nations that was popular in the 1990s and early 2000s — austerity, privatization of government services and deregulation — has lost favor in many circles as punitive and often counterproductive.

There’s a lot to dislike about the above excerpts.

Looking at the text, the part about “extreme inequality” is nonsensical, both because the IMF hasn’t done anything to “manage” the issue, other than to advocate for class-warfare taxes.

Moreover, there’s no support for the empty assertion that inequality is a “risk” to the world economy (sensible people point out that the real problem is poverty, not inequality).

Ms. Cohen also asserts that the “preferred cocktail” of pro-market policies (known as the Washington Consensus) has “lost favor,” which certainly is accurate.

But she offers another empty – and inaccurate – assertion by writing that it was “counterproductive.”

Here are some additional excerpts.

The debate about the role of the I.M.F. was bubbling before the appointment of Ms. Georgieva… But she has embraced an expanded role for the agency. …she stepped up her predecessors’ attention to the widening inequality and made climate change a priority, calling for an end to all fossil fuel subsidies, for a tax on carbon and for significant investment in green technology. …Sustainable debt replaced austerity as the catchword. …The I.M.F. opposed the hard line taken by some Wall Street creditors in 2020 toward Argentina, emphasizing instead the need to protect “society’s most vulnerable” and to forgive debt that exceeds a country’s ability to repay.

The last thing the world needs is “an expanded role” for the IMF.

It’s especially troubling to read that the bureaucrats want dodgy governments to have more leeway to spend money(that’s the real meaning of “sustainable debt”).

And if the folks at the IMF are actually concerned about “society’s most vulnerable” in poorly run nations such as Argentina, they would be demanding that the country copy the very successfulpoverty-reducingpolicies in neighboring Chile.

Needless to say, that’s not what’s happening.

The article does acknowledge that not everyone is happy with the IMF’s statist agenda.

Some stakeholders…object to what’s perceived as a progressive tilt. …Ms. Georgieva’s activist climate agenda has…run afoul of Republicans in Congress… So has her advocacy for a minimum global corporate tax.

It would be nice, though, if Ms. Cohen had made the article more balanced by quoting some of the critics.

The bottom line, as I wrote last year, is that the world would be better off if the IMF was eliminated.

P.S. The political leadership of the IMF is hopelessly bad, as is the bureaucracy’s policy agenda. That being said, there are many good economists who work at the IMF and they often produce high-quality research (see here, here, here, here, here, here, here, here, here, and here). Sadly, their sensible analyses doesn’t seem to have any impact on the decisions of the organization’s top bureaucrats.

Call me crazy, but I’m baffled that the IMF seems to think nations will grow faster and be more prosperous if politicians seize more money from the economy’s productive sector.

Unfortunately, the IMF has been especially active in recent months..

In a column for the U.K.-based Guardian, Larry Elliott writes about the IMF using the pandemic as an excuse to push for higher taxes.

…the IMF called for domestic and international tax changes that would boost the money available to expand public services, make welfare states more generous… “To help meet pandemic-related financing needs, policymakers could consider a temporary Covid-19 recovery contribution, levied on high incomes or wealth,” the fiscal monitor said. …Paolo Mauro, the deputy director of the IMF’s fiscal affairs department, said there had been an “erosion” of the taxes paid by those at the top of the income scale, with the pandemic offering a chance to claw some of the money back. “Governments could consider higher taxes on property, capital gains and inheritance,” he said. “One specific option would be a Covid-19 recovery contribution – a surcharge on personal tax or corporate income tax.”

Mr. Mauro, like most IMF bureaucrats, is at “the top of the income scale,” but he doesn’t have to worry that he’ll be adversely impact if politicians seek to “claw some of the money back.”

Writing for the IMF’s blog, Mr. Mauro is joined by David Amaglobeli and Vitor Gaspar in supporting higher taxes on other people.

Breaking the cycle of inequality requires both predistributive and redistributive policies. …The COVID-19 crisis has demonstrated the vital importance of a good social safety net that can be quickly activated to provide lifelines to struggling families. …Enhancing access to basic public services will require additional resources, which can be mobilized, depending on country circumstances, by strengthening overall tax capacity. Many countries could rely more on property and inheritance taxes. Countries could also raise tax progressivity as some governments have room to increase top marginal personal income tax rates… Moreover, governments could consider levying temporary COVID-19 recovery contributions as supplements to personal income taxes for high-income households.

Needless to say, the IMF is way off base in fixating on inequality instead of trying to reduce poverty.

The International Monetary Fund (IMF) says it backs a U.S. proposal for a global minimum corporate tax. IMF Chief Economist Gita Gopinath said that the fund has been calling for international cooperation on tax policy “for a long time,” adding that different corporate tax rates around the world have fueled tax shifting and avoidance. “That reduces the revenues that governments collect to do the needed social and economic spending,” Gopinath told Yahoo Finance Tuesday. “We’re very much in support of having this kind of global minimum corporate tax.” …Gopinath also backed Yellen’s push forward on an aggressive infrastructure bill… As the IMF continues to encourage countries with fiscal room to continue spending through the recovery, its chief economist said investment into infrastructure is one way to boost economic activity.

Based on the above stories we can put together a list of the tax increases embraced by the IMF, all justified by what I call “fairy dust” economics.

All supported by bureaucrats who are exempt from paying tax on their own very-comfortable salaries.

P.S. I feel sorry for two groups of people. First, I have great sympathy for taxpayers in nations that follow the IMF’s poisonous advice. Second, I feel sorry for the economists and other professionals at the IMF (whooftenproducehigh–qualityresearch). They must wince with embarrassment every time garbage recommendations are issued by the political types in charge of the bureaucracy.

And since it’s comparatively easy to control the timing, level, and composition of that income, class-warfare taxes generally backfire.

Heck, well-to-do taxpayers can simply shift all their investments into tax-free municipal bonds (that’s bad for the rest of us, by the way, since it’s better for growth if they invest in private businesses rather than buying bonds from state and local governments).

Or, they can simply buy growth stocks rather than dividend stocks because politicians (thankfully) haven’t figured out how to tax unrealized capital gains.

Some of my left-leaning readers probably think that my analysis can be ignored or dismissed because I’m a curmudgeonly libertarian.

But I’m simply recycling conventional economic thinking on these issues.

And to confirm that point, let’s review a study on taxes and growth that the International Monetary Fund published last December. Written by Khaled Abdel-Kader and Ruud de Mooij, there are passages that sound like they could have been written by yours truly.

Such as the observation that taxes hinder prosperity by reducing economic output (what economist refer to as deadweight loss).

…public finance…theories teach us some important lessons about efficient tax design. By transferring resources from the private to the public sector, taxes inescapably impose a loss on society that goes beyond the revenue generated. …deadweight loss (or excess burden) is what determines a tax distortion. Efficient tax design aims to minimize the total deadweight loss of taxes. The size of this loss depends on two main factors. First, losses are bigger the more responsive the tax base is to taxation. Second, the loss increases more than proportionately with the tax rate: adding a distortion to an already high tax rate is more harmful than adding it to a low tax rate. Two prescriptions for efficient tax policy follow: (i) it is efficient to impose taxes at a higher rate if things are in inelastic demand or supply; and (ii) it is best to tax as many things as possible to keep rates low. …empirical studies on the growth impact of taxes…generally find that income taxes are more distortive for economic growth than taxes on consumption.

There are several parts of the above passage that deserve extra attention, such as the observation about elasticity (similar to the point I made in the video about why higher tax rates on upper-income taxpayers are so destructive).

But the most important thing to understand is what the authors wrote about how “the [deadweight] loss increases more than proportionately with the tax rate.”

In other words, it’s more damaging to increase top tax rates.

This observation, which is almost certainly universally recognized in the economics profession, tells us why class-warfare taxes do the most economic damage, on a per-dollar-collected basis.

The IMF study also has worthwhile observations on different types of taxes, such as why it’s a good idea to have low income tax rates on people.

Optimal tax theory emphasizes the trade-off between equity and efficiency. …This requires balancing the revenue gain from a higher marginal top PIT rate at the initial base against the revenue loss induced by behavioral responses that a higher tax rate would induce—such as reduced labor effort, avoidance or evasion—measured by the elasticity of taxable income. …high marginal rates cause other adverse economic effects, e.g. on innovation and entrepreneurship, and thus create larger economic costs than is sometimes assumed.

Capital income—interest, dividends and capital gains—is used for future consumption so that taxes on it correspond to a differentiated consumption tax on present versus future consumption—one that compounds if the time horizon expands. Prudent people who prefer to postpone consumption to later in life (or transfer it to their heirs) will thus be taxed more than those who do not, even though they have the same life-time earnings. This violates horizontal equity principles. Moreover, it causes a distortion by encouraging individuals to substitute future with current consumption, i.e. they reduce savings. The tax is therefore also inefficient. A classical result, formalized by Chamley (1986) and Judd (1985), is that the optimal tax on capital is zero.

Indeed, the study even asks whether there should be a corporate income tax when the same income already is subject to dividend taxation when distributed to shareholders.

…capital income taxes can be levied directly on the people that ultimately receive that income, i.e. shareholders and creditors. So: why is there a need for a CIT? It is hard to justify a CIT on efficiency grounds. As explained before, the incidence of the CIT in a small open economy falls largely on workers, not on the firm or its shareholders. Since it is more efficient to tax labor directly than indirectly, the optimal CIT is found to be zero. …CIT systems…in most countries…create two major economic distortions. First, by raising the cost of capital on equity they distort investment decisions. This hurts economic growth and adversely affects efficiency. Second, by differentiating between debt and equity, they induce a bias toward debt finance. This not only creates an additional direct welfare loss, but also threatens financial stability. Both distortions can be eliminated by…cash-flow taxes, which allow for full expensing of investment instead of deductions for tax depreciation

And I like the fact that the study makes very sensible points about why there should not be a pro-debt bias in tax codes and why there should be “expensing” of business investment costs.

I’ll close by noting that the IMF study is not a libertarian document.

The authors are simply describing the economic costs of taxation and acknowledging the tradeoffs that exist when politicians impose various types of taxes (and the rates at which those taxes are imposed).

But that doesn’t mean the IMF is arguing for low taxes.

There are plenty of sections that make the (awful) argument that it’s okay to impose higher tax rates and sacrifice growth in order to achieve more equality.

And there are also sections that regurgitate the IMF’s anti-empirical argument that higher taxes can be good for growth if politicians wisely allocate the money so it is spent on genuine public goods.

Politicians doing what’s best for their countries rather than what’s best for themselves? Yeah, good luckwith that.

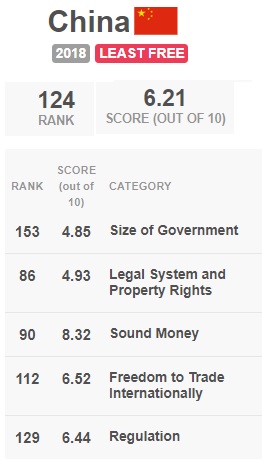

During the 1950s, 1960s, and 1970s, China was horrifically impoverished because of socialist policies. According to the Maddison database, the country was actually poorer under communism than it was 1,000 years ago.

But there was then a bit of economic liberalization starting in 1979. As a result, there’s been a significant increase in living standards and a huge reduction in poverty.

That’s the good news. And I sometimes use China’s post-1979 growth as an example of how even a modest bit of pro-market reform can generate positive results.

According to the most-recent edition of the Fraser Institute’s Economic Freedom of the World, China is in the bottom quartile, ranked #124 out of 162 nations.

If you look at the the details of China’s score, you’ll notice that it does poorly in all areas. But the nation’s lowest score is for fiscal policy (“size of government”).

So if the goal is to help China converge, the obvious place to start is by shrinking the size and scope of government.

But not according to the bureaucrats at the International Monetary Fund.

In a recent report, the IMF actually advised China to move fiscal policy even further to the left.

I’m not joking. Here are the relevant excerpts.

A combination of a permanent strengthening of the social safety net with reforms to broaden the tax base and increase progressivity would provide effective household support. This would include: Expanding significantly the coverage of unemployment insurance… These efforts would be more effective if complemented with hiring subsidies and programs. …there remains ample scope to further increase transfers… Tax reforms could help improve the progressivity of the tax system as well as meet additional financing needs to permanently expand the social safety net.

This is so misguided, I’m at a loss for words.

But fortunately, I don’t need to be locquacious because Mihai Macovei already wrote an excellent article, critiquing the IMF’s statist approach, for the Mises Institute.

The IMF argues…that a “reliable and effective social safety system” and a “reduction of the high household savings rate” would rebalance and make “resilient” China’s growth model. But why would high saving and low consumption impede sustainable growth? Both sound economic theory and historic experience refute the mainstream’s claim that China needs a big welfare state like those of modern Western economies in order to get richer. …China’s social safety nets are much less generous than in advanced economies, in particular in terms of unemployment benefits and pension income… The fact that China has not built a highly redistributive welfare system like in most advanced economies is illustrated primarily by the very limited role played by the personal income tax (PIT) in income redistribution. …Only people in the top income quintile are effectively paying an income tax… As a result, the Chinese budget collects only 1.2 percent of GDP from PIT, compared to more than 10 percent of GDP in the US. …All this prompts the IMF…to call China’s taxation system “regressive” and to call for more progressive income taxation and redistribution. …In reality, China’s lighter taxation system reduces less people’s incentives to work and save compared to other economies. At the same time, less welfare redistribution ensures higher workforce participation and less waste relative to the oversized and increasingly unsustainable social safety nets in modern advanced economies. …the mainstream criticism of China’s high savings propensity, lean welfare system, and reduced progressivity of taxation seems utterly misplaced.

Mihai is obviously very polite. I would use all sorts of bad words to describe the IMF’s recommendations, but he simply observes that the bureaucracy’s approach is “utterly misplaced.”

Though at least you can give the IMF credit for consistency. The bureaucrats also pushed for higher taxes and bigger government in China in 2015 and 2018.

Bernie Sanders was considered a hard-core leftist because his platform was based on higher taxes and higher spending.

Elizabeth Warren also was considered a hard-core leftist because she advocated a similar agenda of higher taxes and higher spending.

And Joe Biden, even though he is considered to be a moderate, is currently running on a platform of higher taxes and higher spending.

Want to know who else is climbing on the economically suicidal bandwagon of higher taxes and higher spending? You probably won’t be surprised to learn that the pro-tax International Monetary Fund just published its World Economic Outlook and parts of it read like the Democratic Party’s platform.

Investments in health, education, and high-return infrastructure projects that also help move the economy to lower carbon dependence… Moreover, safeguarding critical social spending can ensure that the most vulnerable are protected while also supporting near-term activity, given that the outlays will go to groups with a higher propensity to spend their disposable income… Some fiscal resources…should be redeployed to public investment—including in renewable energy, improving the efficiency of power transmission, and retrofitting buildings to reduce their carbon footprint. …social spending should be expanded to protect the most vulnerable where gaps exist in the safety net. In those cases, authorities could enhance paid family and sick leave, expand eligibility for unemployment insurance, and strengthen health care benefit coverage…social spending measures…strengthening social assistance (for example, conditional cash transfers, food stamps and in-kind nutrition, medical payments for low-income households), expanding social insurance (relaxing eligibility criteria for unemployment insurance…), and investments in retraining and reskilling programs.

And here’s a partial list of the various class-warfare taxes that the IMF is promoting.

Although adopting new revenue measures during the crisis will be difficult, governments may need to consider raising progressive taxes on more affluent individuals and those relatively less affected by the crisis (including increasing tax rates on higher income brackets, high-end property, capital gains, and wealth) as well as changes to corporate taxation that ensure firms pay taxes commensurate with profitability. …Efforts to expand the tax base can include reducing corporate tax breaks, applying tighter caps on personal income tax deductions, instituting value-added taxes.

Where fiscal rules may constrain action, their temporary suspension would be warranted

Needless to say, any time politicians have a chance to expand their power, temporary becomes permanent.

When I discuss IMF malfeasance in my speeches, I’m frequently asked why the bureaucrats propose policies that don’t work – especially when the organization’s supposed purpose is to promote growth and stability.

The answer is “public choice.” Top IMF officials are selected by politicians and are given very generous salaries, and they know that the best way to stay on the gravy train is to support policies that will please those politicians.

P.S. I wish there was a reporter smart enough and brave enough to ask the head of the IMF to identify a single nation – at any point in history – that became rich by expanding the size and cost of government.

P.P.S. There are plenty of good economists who work for the IMF and they often write papers pointing out the economic benefits of lower taxes and smaller government (and spending caps as well!). But the senior people at the bureaucracy (the ones selected by politicians) make all the important decisions.

Do you want to understand the International Monetary Fund’s (IMF) pernicious role in the global economy?

Here’s a simple analogy that will tell you everything you need to know. Let’s say you have two friends.

Friend A, who continuously gets in financial trouble because of compulsive gambling and alcoholism.

Friend B, who continuously gets in financial trouble because he loses money by giving loans to Friend A.

Assuming you’re a good person, you will scold both your friends for irresponsible and imprudent behavior. And you certainly won’t aid and abet their recklessness.

But if that’s your attitude, you’ll never get a lucrative (and tax-free!) job at the IMF.

That’s because the role of the IMF is enabling bad fiscal policy by governments (i.e., Friend A) and then providing bailouts so that the institution that lend money to those governments (i.e., Friend B) are insulated from their foolish choices.

To make matters worse, the IMF usually imposes “conditionality” on bailouts so that governments – for all intents and purposes – are bribed or extorted to impose higher taxes. Sort of akin to giving Friend A (the alcoholic gambler) access to more cash.

All of which explains why we see a lather-rinse-repeat cycle of nations making the same mistakes over and over again.

It’s so predictably destructive that I was only half joking when I told an audience in El Salvador that they should ban all flights containing IMF bureaucrats.

In an article for National Review, Professor Steve Hanke explains why the IMF should be shuttered. But what makes his column especially interesting is that he digs into the history of the bureaucracy.

We learn, for instance, that the IMF supposedly existed to help countries abide by the post-WWII system of fixed exchange rates. So when that system disappeared in the early 1970s, the IMF should have gone away as well.

Established as part of the 1944 Bretton Woods agreement, the IMF was designed to be primarily responsible for extending short‐term, subsidized credits to countries experiencing balance‐of‐payments problems under the post-war, international, pegged‐exchange-rate system. In 1971, however, Richard Nixon, then U.S. president, closed the gold window, triggering the 1973 collapse of the Bretton Woods agreement and, logically, the demise of the IMF. It was then that the IMF should have been mothballed.

Like any self-interested bureaucracy, the IMF figured out new reasons to exist.

And new reasons to expand.

The oil crises of the 1970s were the first to allow the IMF to reinvent itself. Those shocks were deemed to “require” more IMF lending to facilitate, yes, balance‐of‐payments adjustments. …with the onset of the Mexican debt crisis, more IMF lending was “required” to contain the crisis and prevent U.S. bank failures. …Then came the collapse of the Soviet Union. What a “jobs for the boys” bonanza that was! And, the list goes on and on with every crisis providing yet another opportunity for the ineffective IMF to pump out more credit… Today, things have become so politicized that even an international organization, like the IMF, has been able to grant itself a license to meddle in what used to be none of its business… While the IMF’s protean attributes are truly breathtaking, its most recent meddling gives yet another reason to put an end to it.

Steve is right.

But let’s conclude by contemplating the biggest reason to support his conclusion.

Should we abolish the IMF because it’s repugnant that big banks and other lenders are the main beneficiaries of the bailouts?

Should we abolish the IMF because it’s disgusting that corrupt politicians in poor nations get more opportunities to impose bad policy?

Should we abolish the IMF because it’s tragic that the bureaucracy lowers global growth by enabling the misallocation of capital?

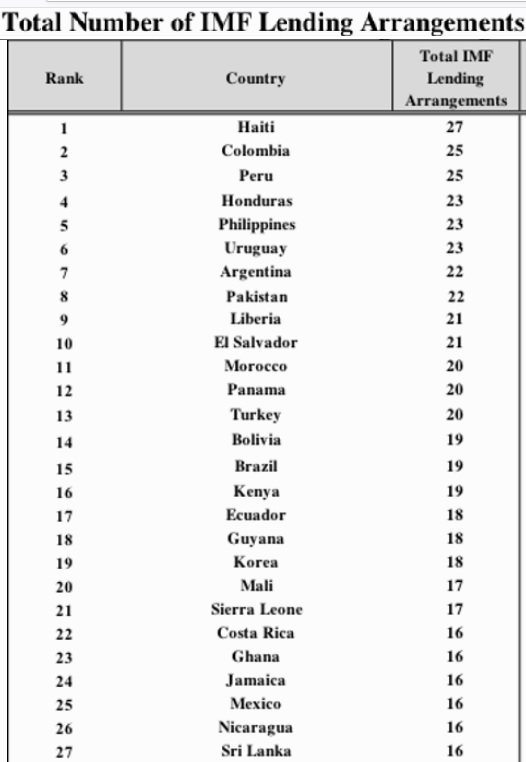

Those are all good reasons, but I think the strongest argument for abolishing the IMF is that the bureaucracy perpetuates poverty. Look at this table, also prepared by Professor Hanke, which shows the nations that have received the most bailouts.

Are any of these nations economic success stories?

Hardly.

Instead, this is primarily a list of nations that have been mired in a sad cycle of poverty thanks in part to wasteful and corrupt governments that were aided and abetted by the IMF.

The bottom line is that the people of the United States should no longer be underwriting this awful organization.

P.S. The IMF is an equal-opportunity dispenser of bad advice. Relying on incredibly shoddy analysis and zero-sum thinking, the bureaucrats are encouraging higher taxes in developed nations as well.

The IMF also is infamous for encouraging higher tax burdens, which is especially outrageous since its cossetted employees are exempt from paying tax on their lavish salaries.

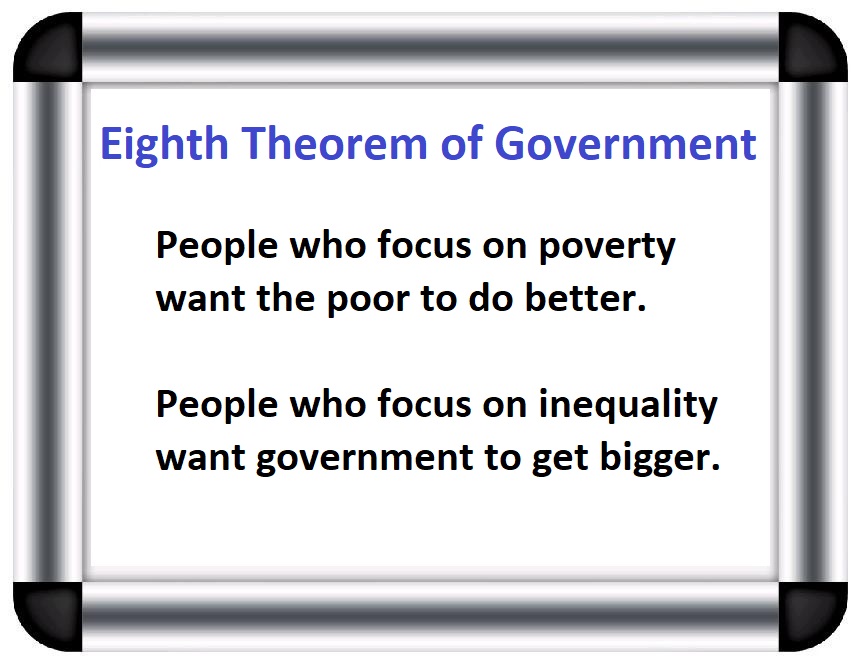

In recent years, the IMF has been using inequality as a justification for statist policies. Most recently, the lead bureaucrat at the IMF, Kristalina Georgieva, cited that issue as a reason for governments to impose higher taxes to fund bigger welfare states.

…inequality has become one of the most complex and vexing challenges in the global economy. Inequality of opportunity. Inequality across generations. Inequality between women and men. And, of course, inequality of income and wealth. …The good news is we have tools to address these issues… Progressive taxation is a key component of effective fiscal policy. At the top of the income distribution, our research shows that marginal tax rates can be raised without sacrificing economic growth. …Gender budgeting is another valuable fiscal tool in the fight to reduce inequality…. The ability to scale up social spending is also essential… A cornerstone of our approach to issues of economic inclusion is our social spending strategy.

What’s especially remarkable is that the IMF has claimed that the punitive policies actually will lead to more growth, in stark contrast to honest people on the left who have always acknowledged the equity-efficiency tradeoff.

The economics editor at the left-leaning Guardian, Larry Elliott, is predictably delighted with the IMF’s embrace of Greek-style fiscal policy.

Raising income tax on the wealthy will help close the growing gap between rich and poor and can be done without harming growth, the head of the International Monetary Fund has said. Kristalina Georgieva, the IMF’s managing director, said higher marginal tax rates for the better off were needed as part of a policy rethink to tackle inequality. …The IMF managing director, who succeeded Christine Lagarde last year, said higher taxes on the better off…would help fund government spending to expand opportunities for those “communities and individuals that have been falling behind.” …Georgieva said the IMF recognised that social spending policies are increasingly relevant in tackling inequality. …She added that many less well-off countries needed to scale up social spending.

Ironically, the IMF actually has admitted that this approach is bad for prosperity.

It has produced research on something called “equally distributed equivalent income” to justify lower levels of income so long as economic misery is broadly shared.

I’m not joking. You can click here to see another example of the IMF embracing poverty if it means the rich disproportionately suffer.

In other words, negative-sum economics. Though Margaret Thatcher was more eloquent in her description of this awful ideology.

At first, this column was going to be a run-of-the-mill anti-IMF diatribe.

But as I contemplated how the people fixated on inequality are willing to treat the poor like sacrificial lambs, it occurred to me that this is a perfect opportunity to unveil my Eighth Theorem of Government.

P.S. Here are my other theorems of government.

The “First Theorem” explains how Washington really operates.

The “Second Theorem” explains why it is so important to block the creation of new programs.

The “Third Theorem” explains why centralized programs inevitably waste money.

The “Fourth Theorem” explains that good policy can be good politics.

The “Fifth Theorem” explains how good ideas on paper become bad ideas in reality.

The “Sixth Theorem” explains an under-appreciated benefit of a flat tax.

The “Seventh Theorem” explains how bigger governments are less competent.

Today, let’s consider the economic consequences of excessive bureaucracy.

And what will make this column particularly interesting is that I’ll be citing some research from economists at the International Monetary Fund (a bureaucracy which is definitely not an outpost of libertarian thinking).

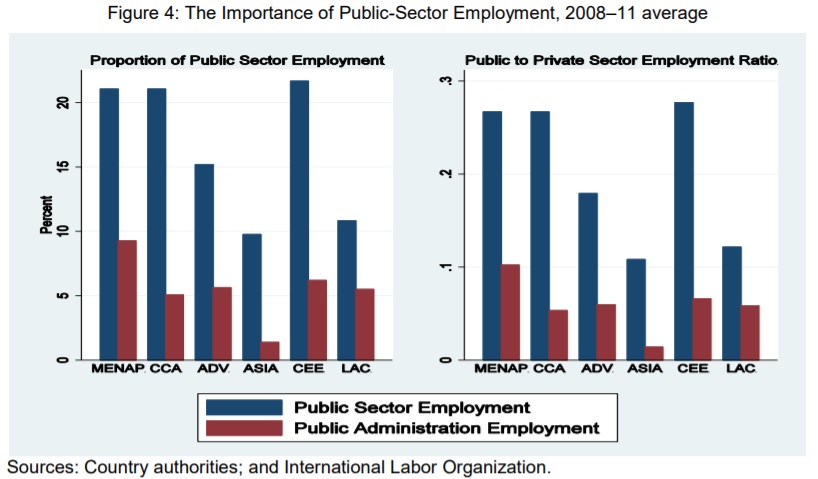

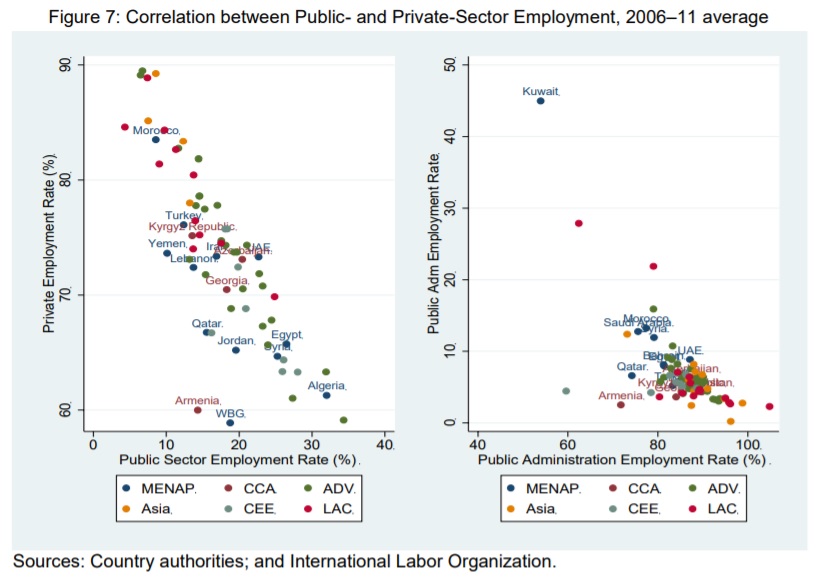

The two authors, Alberto Behar and Junghwan Mok, investigated whether nations lowered unemployment rates by employing more bureaucrats.

The contribution of this paper is to investigate the effects of public hiring of workers on labor market outcomes, specifically unemployment and private employment. In particular, does public hiring increase (“crowd in”) private employment or decrease (“crowd out”) private employment? …It is arguably the case that a private-sector job is more desirable than a public-sector job from a public policy point of view…there is evidence that a large government share in economic activity can be negative for long-term growth because of the distortionary effects of taxation, inefficient government spending due in part to rent-seeking or lower worker productivity, and the crowding out of private investment. …Crowding out could occur through a number of channels. Derived labor demand can be affected through crowding out of the product market, possibly via higher taxes, higher interest rates, and competition from state-owned enterprises. It can occur through the labor market, where higher wages, more job security, or a higher probability of finding a public-sector job can make an individual more likely to seek or wait for public-sector employment rather than search for or accept a job in the private sector… Finally, it can occur in the education market, where individuals seek qualifications appropriate for entering the public sector rather than skills needed for productive employment

As you can see, the authors sensibly consider both the direct and indirect effects of public employment.

Yes, hiring someone to be a bureaucrat obviously means that person is employed, but it also means that resources are being diverted to government.

And that imposes costs on the economy’s productive sector.

So the real question is the net impact.

In their study for the IMF, the authors cite other academic research suggesting that government employment crowds out (i.e., reduces) private employment.