Sensible regulation requires cost-benefit analysis. In other words, do the positive effects of a government intervention outweigh the negative effects?

For instance, a nationwide, 5-miles-per-hour speed limit definitely would reduce traffic fatalities, but lawmakers fortunately don’t impose that kind of rule because it would be absurdly costly.

And since the scholarly research shows a clear link between health and wealth, it’s possible that some (supposedly) pro-safety regulations may wind up leading to a net loss of life.

Other regulations may not have that deadly effect, but they can still be bad news because they increase costs with no concomitant benefits.

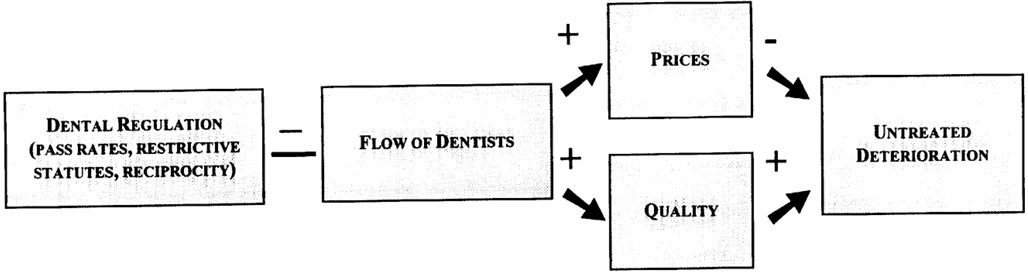

For an example, let’s go back more than 20 years to look at an academic study on dentistry. The authors, Morris M. Kleiner and Robert T. Kudrle, found that red tape was not good news for consumers.

Here are some excerpts.

We have analyzed the impact of stricter occupational licensing requirements on economic outcomes, dental prices, and earnings using dental records of the consumers of these services. …we sketched a model linking regulation to the flow of new dentists as well as to quality and prices. …Alternative multivariate statistical models were used to test the impact of more restrictive licensing provisions, first on dental outcomes and then on the prices of dental service prices and practitioner earnings. …we are able to provide some evidence on how tougher dental regulation reduces the flow of dentists to the states over time. We also show that stricter regulation raises prices, but has no effect on untreated deterioration. …more stringent regulation does not appear to affect some indirect measures of service quality, such as lower malpractice premiums or fewer patient complaints. …Our multivariate estimates show that increased licensing restrictiveness did not improve dental health, but it did raise the prices of basic dental services. Further, using several tests for the robustness of our estimates, we found that the states with more restrictive standards provided no significantly greater benefits in terms of lower cost of untreated dental disease. Our estimates…show that more regulated states have somewhat higher dental prices. …Consequently, moving toward more restrictive policies that limit customer access to these services could reduce the welfare of consumers. …To the extent that states are considering a reduction in the pass rate on dental exams or making it more difficult for out of state practitioners to enter, our analysis suggests that there would be no gains to consumers in terms of overall dental health.

This flowchart from the study illustrates what the authors were trying to measure.

The bottom line is that we have yet another case study (for others, see here, here, here, here, here, here, here, here, here, and here) of red tape being bad news.

P.S. In recent decades, the U.S.A. has had two presidents (here and here) that pushed for less red tape.

I have a three-part series on why price controls are misguided (here, here, and here). In this clip from a recent appearance on Vance Ginn’s Let People Prosper, I look at the specific example of price controls on late fees.

While I think my points are sound, I confess they are not original.

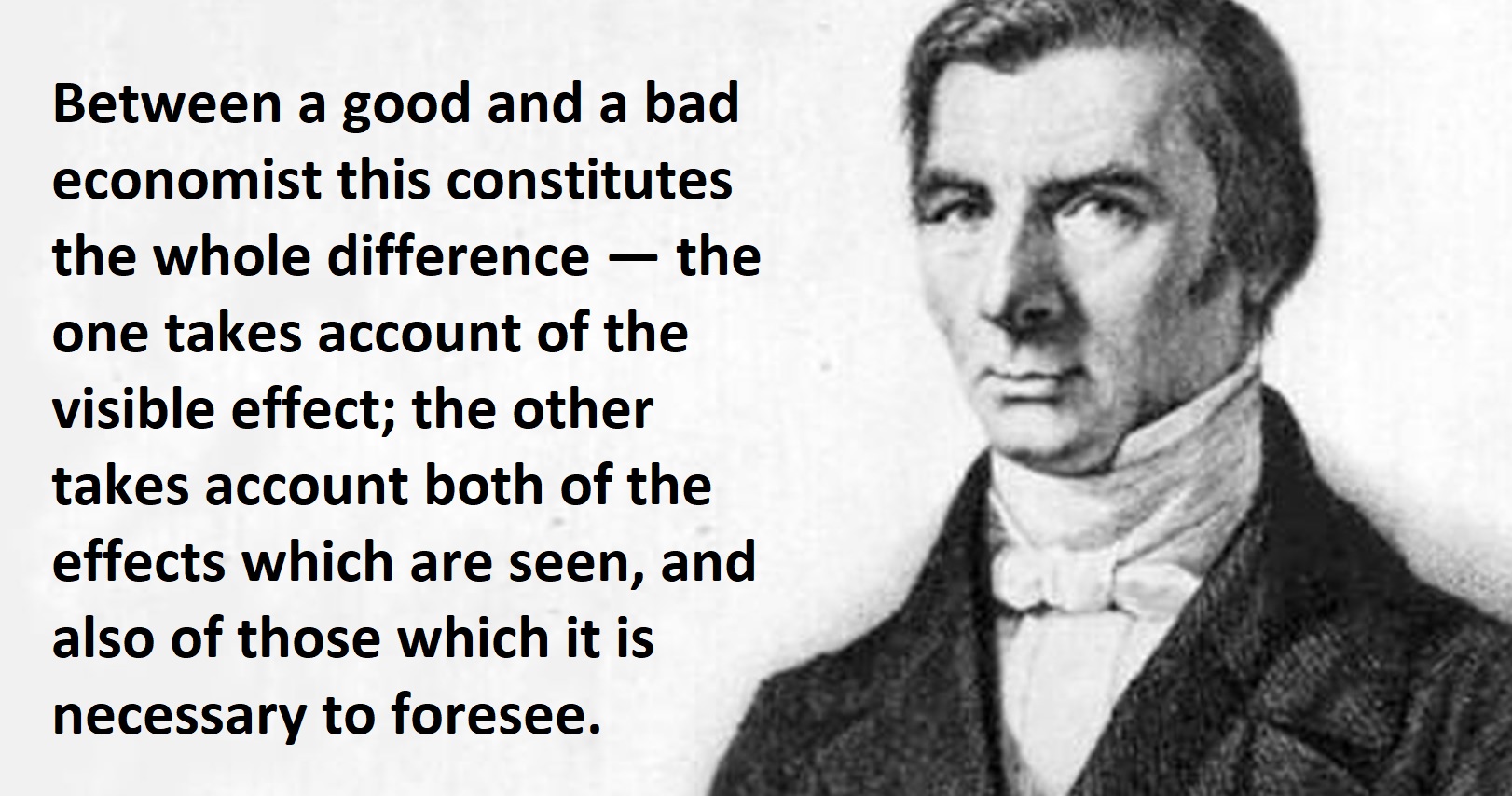

I’m simply recycling the wisdom of Frederic Bastiat, who succinctly and accurately explained way back in the 1800s that you can’t analyze an issue without considering the secondary effects (the “unseen”).

In this case, limiting late fees on credit cards will lead to negative effects in other areas.

I’m not the only one to make this point. The Wall Street Journaleditorialized about this issue a few days ago. Here are some excerpts.

If Americans see their credit costs increase, access to credit decline, or card rewards disappear, blame the Administration’s new price controls. The Consumer Financial Protection Bureau (CFPB) last week finalized a rule effectively capping credit-card late fees at $8… Yet as even the CFPB acknowledges, the lower penalty may cause more borrowers to pay late, and as a result incur higher “interest charges, penalty rates, credit reporting, and the loss of a grace period.” This would make it harder to qualify for an auto loan or mortgage. The agency concedes that credit-card issuers may also raise interest rates, reduce rewards, “increase minimum payment amounts or adjust credit limits to reduce credit risk associated with consumers who make late payments.” Because some states cap credit-card interest rates, “some consumers’ access to credit could fall.” Thanks, Mr. President. By the way, the rule comes as credit-card delinquencies have risen to the highest level in more than a decade. …The Biden Administration is playing up its price controls as an election-year gambit, but it never explains the unseen effects down the road. The forgotten man always pays.

By the way, the editorial includes this bit of bad news caused by a different example of financial intervention.

Consumers are the biggest losers, as we’ve learned from other such price controls. The Durbin Amendment to Dodd-Frank directed the Fed to limit fees charged to retailers for debit-card processing. A 2017 Federal Reserve staff study found that as a result larger banks reduced free checking and raised minimum balance requirements. Small banks not subject to the cap also limited free checking because they faced less competition. Rather than lower prices, retailers pocketed the savings.

And I wrote earlier this year about another example of the Biden crowd imposing red tape on the financial services industry.

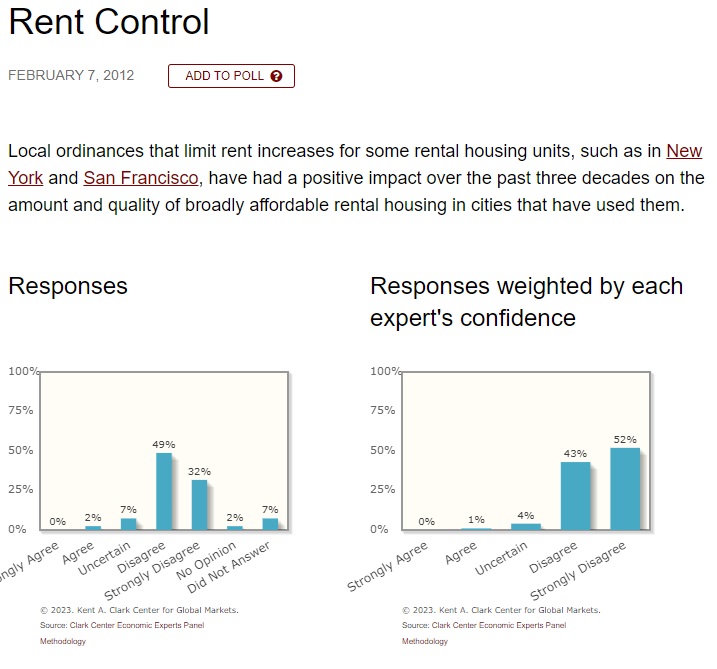

Yet there is near-unanimity in the profession that rent control is a failure. Here’s the data, courtesy of Professor Jeremy Horpedahl.

Yet politicians on the west coast don’t care about economic reality, as explained by David Chen in a report for the New York Times.

…thousands of Washington residents…have converged in recent weeks on Olympia, the state capital, to lobby legislators about one of the most closely watched housing bills in the country: A measure that would cap residential rent increases at 7 percent a year. Deemed a priority by the Democratic leaders who control the State Legislature, the bill has cleared the House of Representatives and is now in the Senate. If it is enacted, Washington would become the third state in the country to adopt statewide rent regulations, after Oregon and California… The state of Washington…would protect tenants throughout the state, including those in towns that may be unable or unwilling to take their own action.

Actually, such legislation would not “protect tenants.”

As always happens with price controls, shortages will appear.

Speaking of politicians who ignore reality, here are some excerpts from a Wall Street Journaleditorial last year.

Democrats in Congress are now pressing the President to impose rent control nationwide…a pretext to nationalize local housing policy. Fifty Democrats in Congress…sent a letter urging Mr. Biden “to pursue all possible strategies to end corporate price gouging in the real estate sector and ensure that renters and people experiencing homelessness across this country are stably housed this winter.” …Democrats want the Federal Housing Finance Agency (FHFA), which supervises government-sponsored enterprises Fannie Mae and Freddie Mac, to establish “anti-price gouging protections” and “just cause eviction standards” in rental properties with government-backed mortgages. These are their euphemisms for rent control and eviction bans.

Let’s close with some evidence from a recent rent-control mistake in Germany. Two German scholars, Pekka Sagner and Michael Voigtländer , investigated the impact of a rent freeze in Berlin.

The Berlin rent freeze was an unprecedented market intervention in the German housing market. We analyse how the rent cap part of the legislation which fixed rents at below market levels affected the supply side in the short term. We find rent decreases accompanied by decreases in supply five times as large. …We make use of a rich dataset of real estate advertisements and employ hedonic difference-in-difference and triple-difference estimation strategies.

Maybe it’s just me, but “decreases in supply five times as large” seems like a bad thing.

It’s almost as if Berlin politicians were a bunch of economic illiterates. Or, they knew the likely result but didn’t care because they were focused on short-term political benefits for themselves.

Since economic principles don’t change when you cross national borders, one might expect to see similar patterns in other countries.

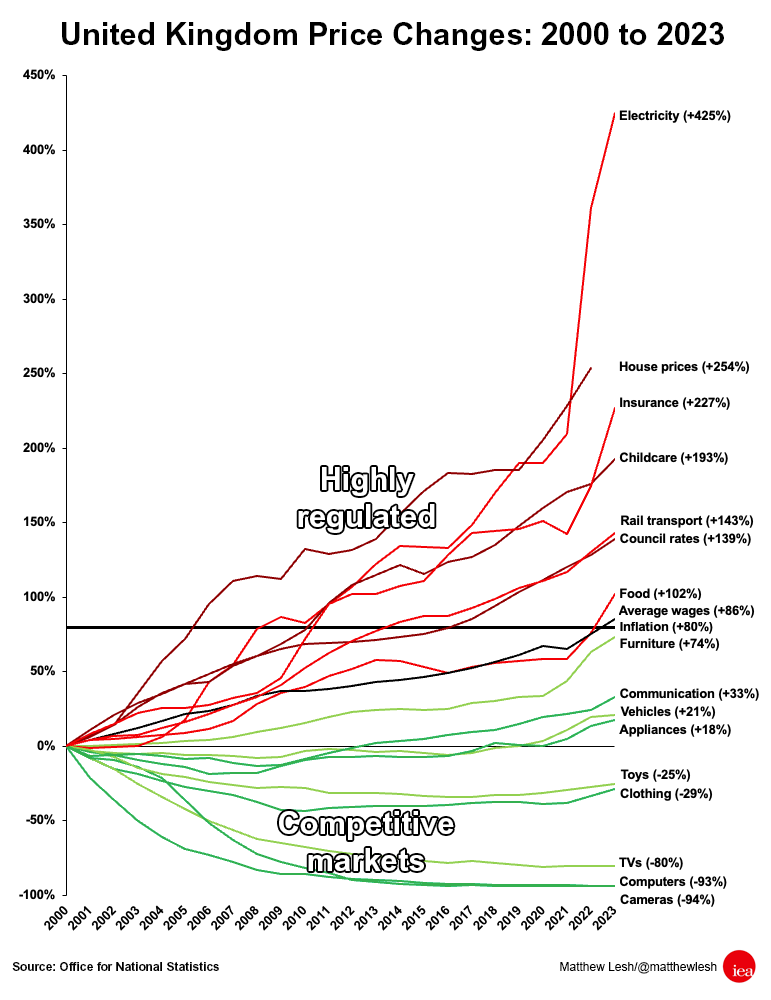

And we do. Here’s a chart from Matthew Lesh of the Institute for Economic Affairs in London. As you can see, overall inflation in the United Kingdom since 2000 has been 80 percent.

But prices have risen much faster in the sectors with lots of government intervention.

And prices have fallen, or risen at a slower-than-average pace, in the sectors where market forces dominate.

Here’s some of what he wrote to accompany the chart.

Prices have risen significantly faster than wages in the United Kingdom over recent years. The result has been a falling quality of life and significant hardship for tens of millions of households. Real household disposable incomes are now expected to be 3.5% lower in 2024-25 than their pre-pandemic levels… A useful starting point is considering which products have, and which have not, risen in price over recent years. …There have also been significant price increases in services and costs the government more directly controls, such as rail transport (+143%) – where the government sets around half the fares and heavily controls the sector – and council rates (+139%). …The products that have gone up most rapidly in cost include electricity (+425%), housing (+254%), and childcare (193%). Notably, these are sectors that have extensive state intervention through regulation and subsidies. …governments can and should change their approach to regulation. Cutting red tape in areas such as housing, energy, and financial services could reduce business costs and increase supply, resulting in lower costs for consumers.

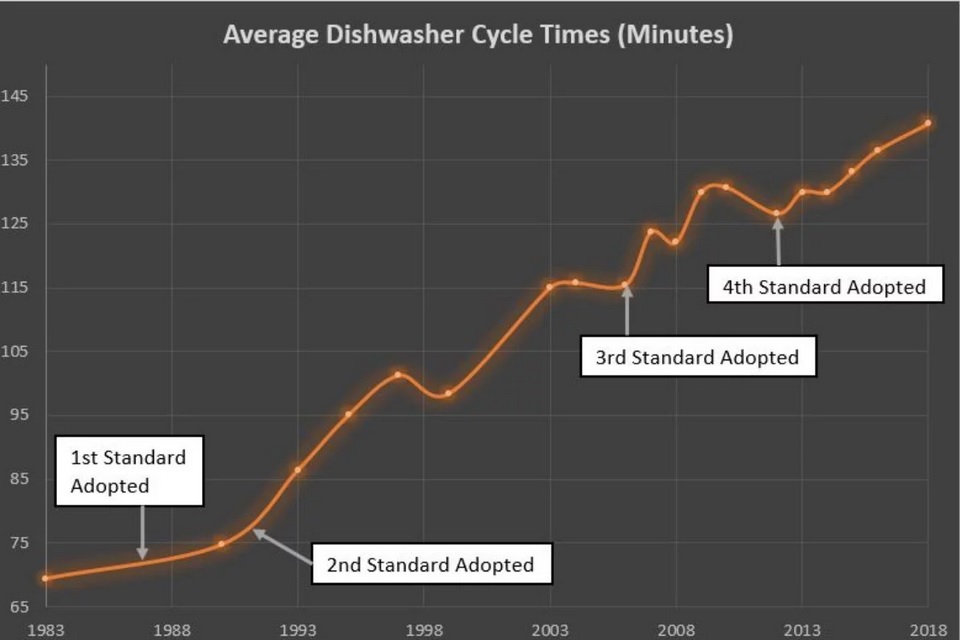

George Will has a new column in the Washington Post about the bureaucracy’s war against dishwashers that…well…actually clean dishes.

The Energy Department’s busy beavers, with their unsleeping search for reasons to boss us around for our own good, decided that dishwashers use too much water and energy… Responding to the Biden administration…, a slew of states sued the Energy Department… This dispute reached the U.S. Court of Appeals for the 5th Circuit, which, in its Jan. 8 ruling,swatted away what it tartly called the department’s “government-always-wins” argument…the court said, not only has the Energy Department acted in excess of statutory authority, but the record also contains “ample evidence” that the department’s new rules reduced efficiency in both energy and water use because “purportedly ‘energy efficient’ appliances do not work.” People “may use more energy and more water to preclean, reclean, or handwash their stuff before, after, or in lieu of using DOE-regulated appliances.” …DOE itself estimated in 2011 that handwashing consumes 350% more water and 140% more energy than machine washing.

The Wall Street Journaleditorialized about this issue last year.

…the Energy Department dropped a sweeping proposal for “efficiency” mandates on dishwashers. Did you enjoy last night’s spaghetti, still crusted on the plate? Now you can taste it twice. …Americans have learned the hard way that stricter efficiency rules on already efficient appliances translate into higher costs, inconvenience, and ultimately waste. The Obama Administration’s dishwasher regulations raised the average price of a machine nearly $100, while producing a new norm of dirty forks and smelly glasses. …Machines can only meet much higher efficiency standards by recirculating water in longer cycles, meaning run times of two or three hours. Yet if the dishes aren’t clean, owners run them again, undermining the argument about conservation. The U.S. Energy Information Administration says that in 2020 nearly 20% of American households that owned a dishwasher never used it. That means they hand washed, which is as inefficient as it comes. The Biden …Energy Department plan gives manufacturers only until 2027 to produce the miracle of costlier washers that do a worse job.

This issue is ridiculous. I’m not sure what’s worse, the fact that bureaucrats are making our lives less pleasant, or that they’re making our lives less pleasant in a way that doesn’t actually save water or energy.

I’ll close on a related note. I was in Mexico City last week and was happily surprised at the quality of the hotel’s shower.

But then I realized that I was enjoying strong water pressure because Mexico presumably does not impose (or does not enforce) the stupid water-flow regulations we have in the United States.

This type of red tape is supposed to save water, but I wonder if that happens since you have to spend twice as long in the shower?

There are plenty of problems, but this image reminds me that there are not necessarily government solutions.

Indeed, it is quite likely that government created the problems in the first place and that additional government intervention will simply make bad situations even worse.

For instance, I’m a frequent flyer, mostly for work but sometimes for more important reasons. So I’m very interested in three things:

Cheap flights

Convenient flights

Comfortable flights

But I’m very skeptical about the ability of government to deliver those goals. Let’s see what two columnists for the Washington Post recently wrote on this topic.

We’ll start with some excerpts from an article by Bina Venkataraman.

…flying is broken. …Little about the experience of modern flying is acceptable. …That’s where Ganesh Sitaraman, a professor at Vanderbilt University Law School…comes in. I cornered him on a recent evening while he was visiting D.C. to ask whether he really thinks there’s a way to end our misery — one that doesn’t just involve paying higher prices. His answer: …Ask more of the country’s airlines. The U.S. airline industry, Sitaraman points out, …is not being required by policymakers to deliver adequate service to the American public. …airlines should be forced to have consistent fares based on distances traveled, not based on when you book your ticket… Sitaraman also advocates disallowing any one airline from dominating a hub such as Dallas, Chicago or Atlanta… airlines should be required to return to the practice of honoring passengers’ tickets from other carriers’ flights when a cancellation or missed connection occurs… I largely agree…that air travel should be treated more as a public utility. …the FAA or Congress could set a minimum size for legroom in economy-class travel.

The big takeaway is that she thinks the market produces bad results and that politicians and bureaucrats would do a better job.

For a different perspective, here are some excerpts from Megan McArdle’s column about airlines.

Every argument about airline customer policy is essentially the same one: “I should be entitled to cheaper and more pleasant flights, and airlines should charge someone else more or make their flight less pleasant to give me what I deserve.” …Politicians are an exception, however. When they weigh in, the argument they’re making is “vote for me.” …Parents understandably…want a guarantee that their kids can sit with them. Unfortunately, the only way to offer such a guarantee would be to toss people without children out of seats they chose in advance, perhaps even paid for… Some might say…passengers shouldn’t have to pay to choose their seats. Fair enough — as long as you understand that the people who pay more for specific seats subsidize the folks who don’t. Stop the practice and the cost of the cheapest tickets will rise. …folks who instinctively feel that the ability to choose your seat or check a bag ought to be included with the price. But if airlines bundled all those things into one standard fare, that fare would be considerably higher than the budget fares the complainers are currently buying. …There is no way to make everyone, or even most people, better off. There is only the Hobbesian scramble for the inherently scarce resources that can be crammed into an aluminum tube flying 35,000 feet above the ground.

Megan also points out that airlines are one of the nation’s least-profitable industries, so it’s absurd to accuse them of successfully pillaging customers.

As explained above, they are simply trying to please consumers, who seem to value low prices over everything else.

The good news is that they are getting low prices thanks to airline deregulation enacted during the Carter Administration.

The bad news is that prices will go back up if Ms. Venkataraman and her allies succeed in pushing through more government control.

The bottom line is that there’s no such thing as a free lunch. There are only tradeoffs. That’s true when looking at the airline market, just like it’s true when looking at everything from the labor market to the nicotine market.

P.S. Ordinary consumers value low prices over conveniences. The main reason is that ordinary consumers are paying out of their own pockets. The people who complain the loudest about airlines are usually the people (such as politicians and journalists) who fly with other people (such as taxpayers and employers) paying for the tickets. For what it’s worth, I’m actually similar to politicians and journalists in that my flight costs rarely come out of my own pocket. But I nonetheless oppose government intervention because I’m not as dumb as Bernie Sanders.

I wrote three columns about occupational licensing in 2017 (here, here, and here), but have since neglected the issue.

It’s time to revisit the issue, and we’ll start with this John Stossel video.

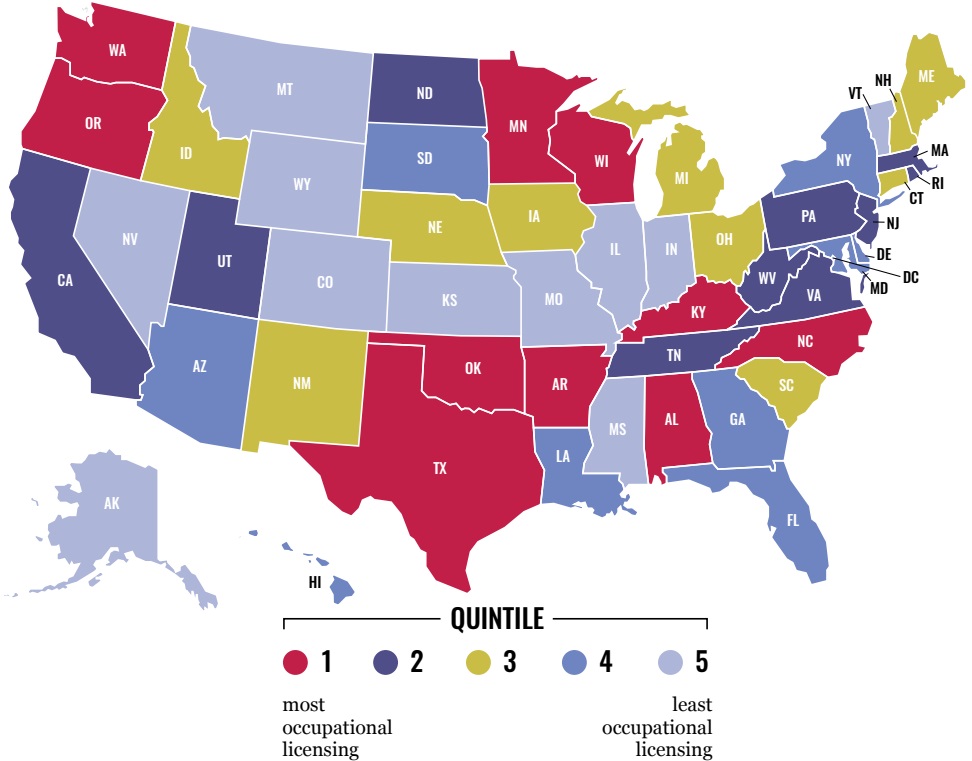

One of the reasons I’m writing about the issue is that the Archbridge Institute issued a report last year that ranked states based on the degree to which they required workers to get permissions slips from government in order to work.

The report was written by Noah Trudeau of Saint Francis University and Edward Timmons of West Virginia University, and it includes a very helpful map. Light blue states are the best and red states are the worst.

Here are some of the findings from their overview.

Occupational licensing affects more than 20 percent of workers in the United States. The extent of occupational licensing greatly differs across states. From both a research and public policy standpoint, it is important to have a comprehensive measure of occupational licensure across states and occupations. The purpose of the State Occupational Licensing Index (SOLI) is to help fill in this gap. The report contains four main sections: an introduction to the index, an overview of our methodology, a comparison to other database rankings, and state profiles for all 50 US states plus DC. …In 2023, the state with the highest occupational licensing burden is Arkansas (#1), followed by Texas (#2), Alabama (#3), Oklahoma (#4), and Washington (#5); the state with the lowest occupational licensing burden is Kansas (#51), preceded by Missouri (#50), Wyoming (#49), Indiana (#48), and Colorado (#47).

Congratulations to Kansas for having the most laissez-faire approach. Arkansas, by contrast, deserves scorn.

Why scorn for Arkansas? Let’s look at some additional analysis.

In 2018, Morris Kleiner and Evgeny Vorotnikov authored a study for the Institute for Justice about occupational licensing. Here are some of their results.

…licensing is frequently wasteful. In preventing people from working in the occupations for which they are best suited, licensing misallocates people’s human capital. In forcing people to fulfill burdensome licensing requirements that do not raise quality, licensing misallocates people’s human capital, money and time. And with its promise of economic returns over and above what can be had absent licensing, licensing encourages occupational practitioners and their occupational associations to invest resources in rent-seeking instead of more productive activity. Taking these misallocated resources into account, we find potential costs to the economy that far exceed those from deadweight losses…we find licensing costs the American economy $183.9 billion in misallocated resources… Assuming the 15 percent national returns, we find licensing costs the American economy $197.3 billion in misallocated resources.

That’s the economic cost to the country.

But don’t forget that hundreds of thousands of Americans lose employment opportunities because of their restrictive regulations.

Let’s close with a bit of good news. Veronique de Rugy wrote a few years ago that there are reform efforts.

The beauty of American federalism is that it allows states to try out different policies and see what works well and what does not. The state of Arizona is putting this flexibility to good use. After implementing a moratorium on occupational-licensing requirements in 2015, the state passed legislation to recognize occupational licenses from other states last year. Going against special-interest groups in various industries whose members would prefer to face as little competition as possible, Arizona is saying that it is open for all business and welcomes competition. As a result, Arizona is effectively launching a healthy competition for workers among the states themselves. …Faced in part with this competition from Arizona, other states are finally getting serious about reforming their own occupational-licensing requirements. …Shoshana Weissmann and Jarrett Dieterle write that many other states are following in Arizona’s footsteps, as evidenced by the fact that in 2020 alone “universal recognition bills are being pursued in Virginia, West Virginia, California, Ohio, Missouri, Georgia, New Hampshire, Indiana, and New Jersey.” …Let’s hope that all the states will follow Arizona’s lead and catch the reform bug so they, too, will free their workers, consumers, and economies from ridiculous licensing requirements.

And other states are catching up, as Veronique hoped.

Marc Joffe has an article about positive developments in Ohio and Nevada.

And here are some excerpts from a Forbes column by Patrick Gleason.

…there is another policy trend emerging that, like income tax relief and greater educational choice, is making states more attractive to workers and employers. That trend is the push by policymakers to remove or mitigate the barriers to employment that state occupational licensing requirements have become. …Universal License Recognition (ULR)…Nearly half of the states now have a ULR law. But four years ago, zero did, underscoring how quickly the ULR movement has grown. Former Governor Doug Ducey (R) made Arizona the first state to enact ULR back in 2019, with positive results observable in the subsequent years. …by also making occupational licensing requirements less taxing for new residents to comply with, both in terms of time and money, reform-minded governors and state lawmakers have honed in on a new way, like with rate-reducing tax reform, to make their states more attractive places to live, work, do business, and support a family.

The great French economist from the 1800s, Frederic Bastiat, famously explained that good economists are aware that government policies have indirect effects (the “unseen”).

Bad economists, by contrast, only consider direct effects (the “seen”).

In modern terms, sensible economists realize that government policies often have indirect effects. These are sometimes called unintended consequences.

Here are a few examples of interventions that have backfired, often hurting intended beneficiaries. Here are a few examples:

By the way, I began every example with “(supposedly)” because our friends on the left tend to have two reasons for pursuing bad policy.

Reason #1, depicted by the cartoon, is a naive do-gooder mentality. They see something that they think is unfair and they reflexively want the government to address the alleged problem. And since they don’t have any (good) economic training, they don’t consider the possibility that their preferred policies will make things worse.

Reason #2 is “public choice,” which is a term that describes how politician, bureaucrats, and voters put self interest above the national interest. Instead of being naive do-gooders, these are people who probably recognize that certain policies will backfire, but they simply don’t care because a policy has certain advantages, such as political popularity.

I didn’t intend to write such a lengthy introduction to today’s column, but you’ll understand my motivation when you read these excerpts from a Washington Poststory by Tony Romm.

The government (supposedly) wants to help bank consumers by limiting overdraft fees.

The U.S. government on Wednesday proposed to limit bank overdraft fees, which companies can charge customers who spend more money than they have available in their accounts… The new draft rules, unveiled by the Consumer Financial Protection Bureau, could cap some of the charges as low as $3… Generally, overdraft payment programs function as a kind of loan: If a customer spends more money than they have, they can elect for the bank to process the transaction anyway. If they do, consumers must pay back the remainder they owe, plus a fee, which averages about $26 per overage nationally… Under the agency’s new draft proposal, banks would be subject to tough credit card-like regulations on their overdraft programs, unless they agree to lower fees on customers.

Reading this story, I don’t doubt that banks want to squeeze as much out of customers as possible (and the same is true for grocery stores, barber shops, and every other kind of business).

But there’s something else I don’t doubt, which is that this policy will backfire in some unintended way.

Why do I think that?

For the simple reason that we’ve seen this happen over and over again. When governments impose costs on the private sector, something bad happens. With lower-income people generally losing the most.

Here are just three examples from the financial services industry.

If politicians dictate that people can’t be employed unless they receive, say, $15 per hour, then workers who are worth less than than amount (because of low skills, no experience, etc) won’t get hired.

And if a worker is worth $17 per hour and a government now says that worker must get $20 per hour, that’s a recipe for getting laid off.

Which is exactly what is happening in California. Here are some excerpts from a Wall Street Journaleditorial.

California’s $20 an hour minimum wage for fast-food workers doesn’t take effect until April, but the casualties are already piling up. Pizza Hut franchises this week told more than 1,200 delivery drivers that they’ll lose their jobs before the higher wage kicks in. …it defies economics and common sense to think that businesses won’t adapt by laying off workers. Some may try to pass on their higher labor costs to customers. McDonald’s and Chipotle Mexican Grill have said that they plan to raise prices. But how many people will pay $8 for a Big Mac? Restaurants will probably deploy more automation to the extent they can, but fewer workers will mean longer waits in the drive-through. Pizza Huts are shaving their costs by out-sourcing delivery service to apps like DoorDash and GrubHub—ironic given how unions have fought against gig work. …Employment in California has fallen by 77,700 in the last year. Yet Democrats continue to impose higher costs and other burdens on business, oblivious to the lost jobs and services.

Why do politicians impose bad laws?

The simple answer is that they are kowtowing to unions.

So you may then ask why unions support bad laws?

I’ve previously noted that unions are willing to screw workers so long as the union benefits. And now we have more evidence for that view.

By the way, here’s some new research showing that minimum wages are bad for workers and the economy.

"Do minimum wages deliver what they promise? Effects of minimum wage on employment, output, and income inequality from occupational choice theory" https://t.co/IltyZHpG1o "the effects are mainly negative… and quantitatively large for high minimum-to-average wage ratios" pic.twitter.com/pIZhHvs4ll

To elaborate, if you give government a little bit of power, we fear it will just be a matter of timebefore politicians and bureaucrats figure out how to expand and abuse that authority.

Today, let’s look at a new power being sought by the crowd in Washington.

They want a “kill switch” for our cars.

I’m not joking, Here’s some of what Jon Miltimore wrote for the American Institute for Economic Research.

Like most Americans, I had never heard of this alleged “kill switch” until a few days ago when Representative Thomas Massie, a libertarian-leaning Republican, proposed to strip the mandate’s funding. …The claim that the feds would mandate that every new motor vehicle include technology that could disable the vehicle seemed ludicrous. So I started Googling. To my relief, I saw several fact-checkers at legacy institutions had determined the “kill switch” mandate was not true. …Unfortunately, my relief evaporated once I looked at the bill itself. Sec. 24220 of the law explicitly states: “[T]o ensure the prevention of alcohol-impaired driving fatalities, advanced drunk and impaired driving prevention technology must be standard equipment in all new passenger motor vehicles.” The legislation then goes on to define the technology as a computer system that can “passively monitor the performance of a driver of a motor vehicle” and can “prevent or limit motor vehicle operation if an impairment is detected” …the law’s language could not be more clear: New motor vehicles must have a computer system to “monitor” drivers, and the system must be able to prevent vehicle operation if it detects impairment.

Clyde Wayne Crews of the Competitive Enterprise Institute analyzed the proposal and specifically warned that a power granted for a good reason (fighting drunk driving) inevitably would be used for other reasons.

The ability to remotely disable a vehicle is not new, of course. Long used in theft prevention, you can buy disabling gear on Amazon yourself. The question is over who performs a remote shutoff of a car, and when it happens. The new vehicle kill switch accelerates government regulation down a sorry new road, with bureaucrats and authorities soon capable of clicking and swiping from afar to strand you. The rationale this time—there’s always a rationale for regulatory overreach—is to combat drunk driving. …To believe newly enabled kill-switch technology will be confined to combatting drunk driving is to pay no sober attention to the proclivities of modern helicopter government. Since no one stopped the kill switch, various agencies can be expected to readily involve themselves in remote enforcement of speed restrictions, no drive zones, emissions monitoring, vehicle sidelining when emergency vehicles pass, preventing startup if the seatbelt isn’t clicked, and the like. …What might an EPA drunk on Green New Deal absinthe do with rooftop-mounted carbon-footprint monitors, or a capability to override commercial building water and energy usage and thermostat settings? Would tomorrow’s EPA have interest in remotely countermanding people’s smart home preferences? You know the answer.

Yes, indeed, we know the answer.

Giving government more power is a very dangerous proposition if you care about economic growth and personal freedom.

Kudos to Congressman Massie for working to block this pernicious idea.

And shame on the 19 Republicans in the House of Representatives who voted to kill his amendment (and shame on the Republicans Senators and Representatives who voted for Biden’s pork-filled Transportation bill in the first place).

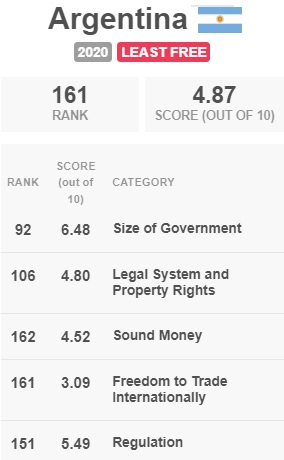

Last month, a plurality of Argentinians voted for a libertarian in their nation’s presidential primary. This shocking result may be an sign that voters have sobered up and realized that they have “run out of other people’s money.”

For what it’s worth, The Economist is not a libertarian-friendly publication. So it is especially remarkable and noteworthy that the video clearly explains that Argentina’s problems are the result of statism (the country has the world’s fifth-lowest score for economic liberty).

Argentina’s economic misery is not a surprise to anyone who has paid attention, as I explained in Part I of this series.

The situation is tragic. Argentina used to be one of the world’s richest nations. Unfortunately, it has suffered from varying degrees of Peronism since World War II (occasional right-of-center governments often are just as bad as the Peronists).

As a result, Argentina has suffered a massive decline in relative living standards.

One reason for decades of bad policy is that the bureaucrats at the International Monetary Fund have a terrible track record of rewarding Argentina when it gets in fiscal trouble (22 bailouts so far!).

So what’s the main lesson to be learned? In part, it will be good if Argentinian voters reject Peronism later this year in their presidential election. But I worry that won’t be enough if international bureaucracies like the IMF continue to play a malignant role.

But let’s not forget that Europe has foolish agriculture subsidies (as does the United States), and this is leading the wine-loving French to actually destroy wine.

Here are some excerpts from a Washington Postreport by Caroline Anders.

France is about to destroy enough wine to fill more than 100 Olympic-size swimming pools. And it’s going to cost the nation about $216 million. Ruining so much wine may sound ludicrous, but there’s a straightforward economic reason this is happening…people are drinking less of it. That has left some producers with a surplus that they cannot price high enough to make a profit. …In June, the European Union initially gave France about $172 million to destroy nearly 80 million gallons of wine, and the French government announced additional funds this week. …Costs are so high and demand is so low that some producers cannot turn a profit. While this year’s subsidy is getting a lot of attention, French government intervention is not a new phenomenon… The nation has long regulated the wine market intensely, in some cases telling producershow many vines they can grow and how far apart they have to be, in an effort to prevent the market from being flooded.

I can’t resist complaining about a bit of that wording.

There is not “a straightforward economic reason” for destroying the wine. After all, the free market does not lead people to do crazy things or make inefficient choices.

The article should be changes to say that there’s “a straightforward political reason” for destroying the wine.

Industrial policy is when politicians use subsidies, mandates, protectionism, and other forms of intervention to provide unearned benefits to a specific companies and/or specific industries.

The politicians claim that the free enterprise system somehow is too inefficient or too short-sighted to produce the ideal outcome, so they have to intervene.

Some of them may even believe those words (based on my decades in Washington, I think the truth is that they like industrial policy because it’s a great way of swapping favors for campaign cash).

For purposes of today’s column, their motives don’t matter. Our goal is simply to show that industrial policy does not work.

China’s economic model—which has leaned strongly into industrial policy and top-down investments directed from Beijing—”is broken” and has left the country “drowning in debt and running out of things to build,” Lingling Wei and Stella Yifan Xie explain… As in the U.S., bridges to nowhere and useless high-speed rail projects are a sign of infrastructure policies driven by politics rather than economics. …government is scaling up another round of industrial policy focused on semiconductors, artificial intelligence, and direct government spending on cultural items such as sporting events. …the bill eventually comes due in the form of higher debt and wasted resources. …More attention should be paid to the weaknesses in China’s economic model, which are becoming more difficult to ignore on both sides of the Pacific. China’s leaders have bet heavily on the misguided notion that government-directed investment is the key to greater economic growth.

Boehm is correct. More attention should be paid to the failures of industrial policy.

Unfortunately, there’s a problem with Joe Biden’s attention span, as noted in a Wall Street Journaleditorial on August 25.

Bidenomics is fast becoming a study in the contortions of industrial policy. Consider the Commerce Department’s decision late last week to slap tariffs on solar imports from Southeast Asia, raising the costs of U.S. solar-energy projects that the White House says are the vital future of U.S. energy. …the Inflation Reduction Act (IRA) provides hefty handouts for U.S. solar-panel manufacturers. First Solar expects to pocket as much as $710 million this year in tax credits—nearly 90% of forecast operating profit. …The solar follies reveal the contradictions of the Biden Administration’s industrial policy. Its labor, climate and anti-China agendas conflict in their combination of subsidies, mandates, bans and taxes. Subsidies lead to tariffs, which lead to more subsidies as government becomes the allocator of capital and decides which companies win or lose. The biggest losers, as usual, will be American taxpayers.

The Wall Street Journal also opined on the issue on August 21.

It’s ironic, to say the least, that the U.S. is seeking to imitate China’s economic model at the moment that its industrial policy fractures. Look no further than its collapsing electric-vehicle bubble, which is a lesson in how industries built by government often also fail because of government. …About 400 Chinese electric-car makers have failed in the past several years as Beijing reduced industry subsidies while ramping up production mandates. Scrap-yards around China are littered with EVs whose technology has become outdated, redolent of its unoccupied housing developments created by government-driven investment. …Now comes the destruction that invariably follows the government creation, which may be a harbinger for the U.S. as the Biden Administration emulates China’s EV industrial policy. …Business failures are inevitable in a dynamic economy, but government will be mainly responsible for the destruction that results from its force-fed EV transition—and the damage may only just be starting.

But Biden isn’t the only politicians with a problem. Donald Trump suffered from attention deficit disorder during his years in the White House.

The Washington Post has a report by Jeanne Whalen about Foxconn, which Trump gushed about during his time in the White House.

A 30-minute drive from…Milwaukee stands a mysterious glass globe that has come to symbolize the failure of one of Republican front-runner and former president Donald Trump’s big promises. …The orb and the three partially used buildings nearby are nothing like the giant manufacturing campus with 13,000 high-tech jobs that Trump and Foxconn promised five years ago, when Trump — wielding a golden shovel for the groundbreaking — called the project the “Eighth Wonder of the World.” Instead, the orb is the butt of local jokes. …It might be funny, …except that local and state governments spent roughly $500 million to buy land, bulldoze houses and build infrastructure for an unfulfilled manufacturing megasite that was supposed to include dozens of futuristic buildings and a factory… The ill-fated project, backed by heavy state and municipal spending, comes as the federal government is pouring tens of billions of dollars into subsidizing domestic manufacturing, hoping that the funds will help spur projects that might otherwise not happen.

Since I live in Virginia, I’m relieved that Wisconsin taxpayers were pillaged for that boondoggle.

Unfortunately, that’s the exception rather than the rule.

Remember, by the way, that the indirect costs of industrial policy (misallocated resources, foregone growth) almost surely are greater than the direct cost on taxpayers.

But he also was a big proponent of industrial policy, and that the topic of today’s column.

In a column for the Wall Street Journal, Professor Jason Taylor explains the failure of President Franklin Roosevelt’s so-called National Industrial Recovery Act.

In June 1933 Roosevelt signed the National Industrial Recovery Act (NIRA), which required firms to meet with competitors and construct a “code of fair competition.” Over two years, 557 codes were implemented in industries ranging from steel to fishing tackle. …Businesses that were found violating the codes—say, charging a price below the code-specified one—could face hefty fines and imprisonment. …Predictably, the NIRA was a disaster. Companies responded to forced wage increases by scaling back employment. And colluding firms did what cartels generally do—they restricted output and raised prices. …manufacturing output rose an unprecedented 78% between March and July 1933, it fell sharply after the Blue Eagle’s arrival. By November two-thirds of the recovery gains were lost. …While it’s impossible to say exactly how the U.S. economy would have fared without the NIRA’s enactment, we do know one thing: The Great Depression would’ve been a lot less depressing. As he signed the NIRA, FDR said it was “the most important and far-reaching legislation ever enacted.” It was important, far-reaching and disastrous.

The moral of the story is that bad government policies caused the Great Depression, and FDR made a bad situation far worse.

P.S. FDR also wanted an “Economic Bill of Rights” that would have created far-reaching entitlements to other people’s money.

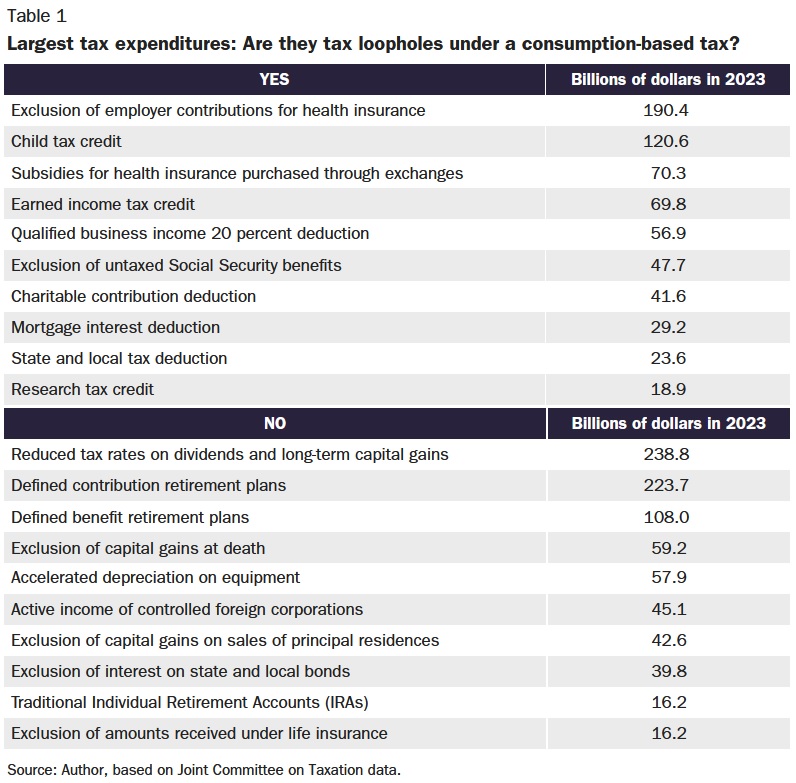

At the start of the year, I wrote that so-called tax expenditures were a “boring but important issue.”

Well, it’s time to once again put readers to sleep.

Let’s start with a definition. A tax expenditure is basically a loophole in the tax code. And these loopholes are called tax expenditures because they are seen as being equivalent to a spending program.

For instance, the crowd in Washington could pass a $100 billion spending program to benefit an interest group, or it could create a special preference in the tax code that is worth $100 billion to the same interest group.

Libertarians don’t view these things as morally equivalent. A spending program takes money from other people and gives those funds to an interest group, whereas a tax loophole simply lets people keep their own money.

But that does not mean tax loopholes are good policy. They are a form of industrial policy in the tax code.

This sounds simple and straightforward, but there is a big controversy over the benchmark (or “tax base“) that gets used when measuring loopholes.

Is is the Haig-Simons tax base, which assumes that there should be double taxation of income that is saved and invested (in effect, taxing income plus changes in net worth)?

Is is the consumption tax base, which assumes that income should be taxed only one time (thus creating neutrality between current consumption and future consumption)?

Official Washington (primarily the Treasury Department and the Joint Committee on Taxation, but also CBO, GAO, ) uses the Haig-Simons tax base.

For those who want to finance genuine tax reform, there are genuine loopholes that could be eliminated or curtailed, most notably the fringe benefits exclusion and the muni-bond exemption.

P.S. The fringe benefits exclusion is such bad policy (contributing to third-party payer) that I even wrote something nice about Obamacare.

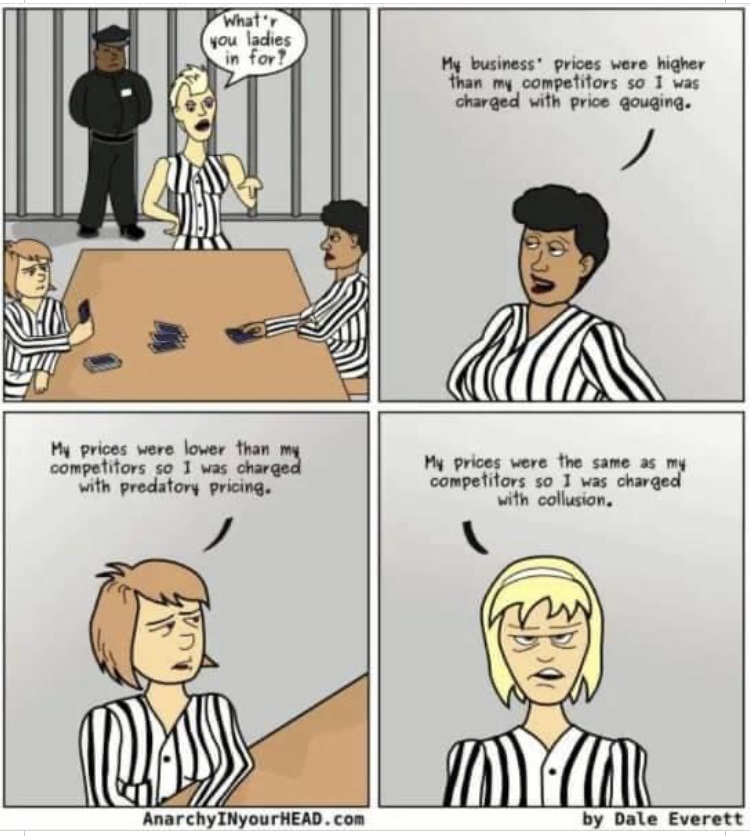

Especially when politicians have created a Catch-22 situation with antitrust laws.

Companies can be accused of improper behavior regardless of what they do.

If they charge more than their competitors, that’s supposedly evidence of monopoly power.

If they charge the same as their competitors, that’s supposedly evidence of collusion.

If they charge less than their competitors, that’s supposedly evidence of predatory pricing.

Just like the poem from The Incredible Bread Machine.

For today, let’s focus on the specific issue of “consumer welfare,” which has limited the folly of antitrust policy by creating a presumption that mergers are okay if prices go down.

In a column for the Wall Street Journal last year, former Senator Phil Gramm and Mike Solon elaborated on this issue.

…over the past half-century, a bipartisan consensus has existed that antitrust law and enforcement should be anchored in consumer welfare. This consensus, beginning in the 1970s, was founded on a bipartisan rejection of Progressive-era regulatory frameworks that harmed consumers, competitiveness and economic growth. …The modern progressives who dominate the Biden administration..see the world through the lens of class warfare, as a zero-sum game. Like Progressives before them, they view the rule of law not as a cornerstone of liberty and democracy, but as an impediment to equality… Unlike most Americans, progressives view low prices as a problem, not a benefit. …With the consumer-welfare standard uprooted, antitrust would become a license to control the American economy, capriciously rewarding favored businesses and punishing disfavored ones.

Professor Brian Albrecht explained in National Review why politicians and bureaucrats should not abandon the consumer welfare standard.

U.S. courts and antitrust-enforcement agencies…, beginning in the 1970s, …turned toward economic reasoning to develop a consistent framework for determining antitrust violations. The result has been the elevation of consumer welfare as antitrust regulation’s fundamental concern. Based on this criterion, economic analysis is applied to business conduct alleged to be anticompetitive to determine the likely impact on consumers. Higher prices for goods or services, lower quality, or less output are the characteristic harms to be avoided. Unfortunately, the Federal Trade Commission (FTC) under chairwoman Lina Khan wants to rewind the clock. …the commission will decide what is “unfair” based on whether the conduct might harm “competition, workers, or other market participants.” If that sounds extremely vague, it’s because it is.

Back in 2021, John McGinnis wrote about antitrust and consumer welfare for Law and Liberty.

The Biden Administration wants to transform antitrust law. In doing so, it would dispense with a four-decade-old consensus that the welfare of consumers should be the object of competition policy. This principle would be replaced with a mixture of untested economic ideas combined with a view that antitrust law should somehow advance democracy. …Not only will this vision harm economic efficiency, it will also make it easier for government officials to reward friendly companies and punish those who do not do the administration’s bidding even on matters unrelated to competition. …the Biden administration’s blunderbuss approach to antitrust law is not limited to tech, but represents a potentially new mechanism of government control over the commanding heights of the economy.

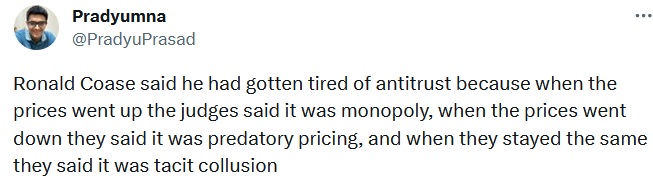

Here’s a tweet from Pradyumna Prasad about antitrust laws.

It’s akin to the above cartoon since it points out that government policies are so convoluted that a company can be guilty regardless of the prices it charges.

I mentioned in the interview that antitrust bureaucrats have a dismal and embarrassing track record. Jessica Melugin of the Competitive Enterprise Institute summarized some of the most famous mistakes back in 2021.

*Standard Oil Co. of New Jersey v. United States had a defendant that was cutting prices while increasing output. The case also lacked evidence of either predatory pricing or consumer harm. *U.S. v. American Telegraph and Telephone Company (AT&T) broke up a monopoly that was created by government, not the market. The case illustrates how regulatory capture—regulated entities’ influence over the regulatory process—works to create and maintain monopolies. *The U.S. v. International Business Machines (IBM) case lasted for 13 years before the Department of Justice (DOJ), which brought the suit, deemed it “without merit” and dropped it. The multi-million-dollar litigation inadvertently raised prices for IBM customers. *Finally, U.S. v. Microsoft illustrates how technological innovation moves faster than litigators.

In a column for the American Institute for Economic Research, Professor Don Boudreaux explains that antitrust laws were enacted because established firms were upset about bigger (and more efficient) rivals charging lower prices..

The post–Civil War transcontinental expansion of railways and telegraphy, along with other technological developments such as the refrigerated railroad car, markedly increased the scale on which many goods could be profitably produced and supplied. Entrepreneurial firms that took advantage of these economies of scale expanded outputs and lowered prices to unprecedented levels. While as a result consumers reaped massive benefits, many established producers suffered. Older, smaller, and less entrepreneurial firms could not match the low prices offered by their large-scale rivals. The demise of many familiar, small-scale producers along with the rise of unprecedentedly huge firms — and equally unprecedented personal fortunes — created the mirage of monopolization. This mirage was opportunistically exploited by some producers who could not match the lower prices of newer and larger rivals. …This animus, in the late 19th century, of smaller-scale producers against their upstart, large-scale, and more efficient rivals supplied the fuel for antitrust legislation, first at the state level and soon afterward at the national level.

In other words, antitrust laws are a product of “public choice” incentives. Politicians always come up with excuses to grab more power.

P.S. You won’t be surprised to learn that Robert Reich does not understand antitrust.

P.P.S. There’s been massive turnover among Fortune 500 companies in the post-WWII era.

That being said, you can sometimes find displays of common sense and sound thinking. Even from places that almost always support bigger government and more intervention., such as the editorial page of the Washington Post.

Here are some excerpts from the Post‘s recent analysis of how to avoid another shortage of infant formula.

…the infant formula shortage that struck American families in 2022 has mostly abated… Yet…the main lesson of last year’s crisis: Ill-conceived or excessive government rules and regulations were themselves among its causes. Unless and until those are fundamentally reformed, the infant formula supply chain will remain vulnerable to another devastating rupture. …The best proof that this market is over-regulated came from the measures government took to alleviate the crisis, almost all of which involved, well, deregulation. Congress suspended tariffs, allowing imports to come in from Europe and elsewhere; the Agriculture Department, which administers WIC, allowed states to offer a wider variety of formula brands and packages than their current contracts covered. …A better policy would open the United States to appropriately regulated imports, make it easier for new domestic producers to enter the market and let all qualified suppliers sell in all states, counting on competition to temper prices.

Usually with regard to government-run health care, folks on the left commonly criticize the United States for being the “only country” that does not provide this or that handout from the government.

That should not be a persuasive argument without first looking at whether the United States is doing better or worse than other nations.

And based on comparative living standards, the United States is far ahead.

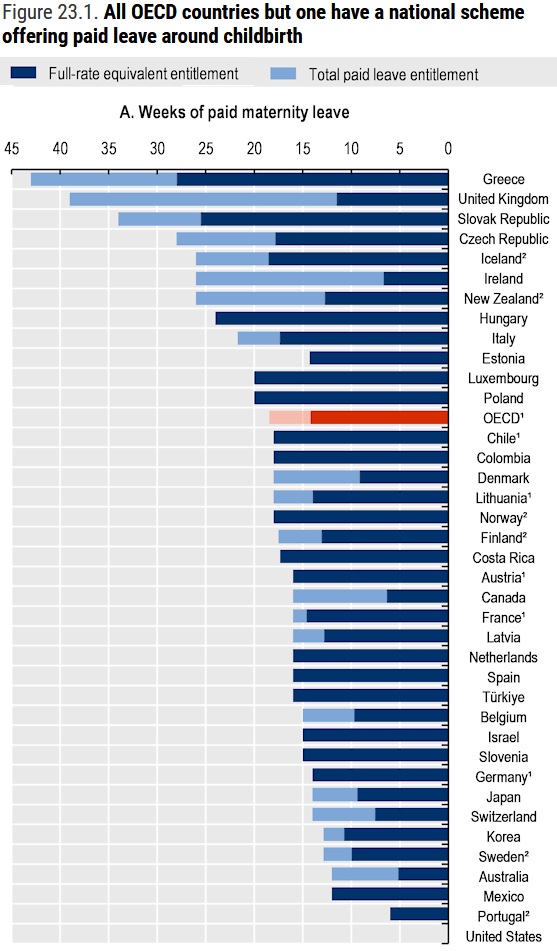

Here are some excerpts from an OECD publication about paid parental leave, authored by Jason Fluchtmann.

Except for the United States, all OECD countries have national statutory rights that entitle mothers to (de facto) paid maternity leave around childbirth. …these entitlements are designed to protect infants and mothers around childbirth, to give both parents the necessary time to provide childcare during the early stages of life of a new-born, and ensure that fathers and mothers are financially supported during their time on leave… Across the OECD, statutory rights to paid maternity leave are provided with an average length of 18.5 weeks as of April 2022…, ranging from 43 weeks in Greece (the longest entitlement) to none in the United States – the only OECD member with no national provision of paid maternity leave.

Here is an accompanying chart showing the United States compared to other OECD nations (needless to say, the article never addresses the issue of whether Greece should be a role model).

To hammer home the point, the OECD article concludes with advice for governments.

One thing you may notice is that the OECD report, for all intents and purposes, only looks at supposed benefits and ignores very real costs.

…calls are intensifying for the federal government to implement paid leave, which may unwittingly hurt those whom the program claims to help. …women would like to get paid to stay home after the birth of their children, yet that’s no more evidence of a market failure than is my not driving a Tesla, even though I’d like to drive one if it were free. This isn’t a reason for government to mandate paid leave (or Teslas) for all workers. …Because paid leave is costly, when firms provide this benefit, they change the composition of their employees’ total compensation by reducing the value of workers’ take-home pay to offset the cost of providing paid leave. While some workers prefer this mix in their pay packages, others don’t. In particular, mandated leave would be a hard trade-off for many lower-paid women who would prefer as much of their income as possible in the form of take-home pay. In fact, polls show that when women learn of the trade-offs inherent in any government-mandated paid-leave policy, their support for such a policy collapses.

As is always the case, Veronique is right. Paid parental leave is not a freebie. If politicians force employers to incur certain costs, workers will bear the burden.

P.S. Parental leave was one of many issues where Trump was in favor of big government rather than economic liberty.

For purposes of today’s column, though, let’s consider how it is a recipe for reducing competition.

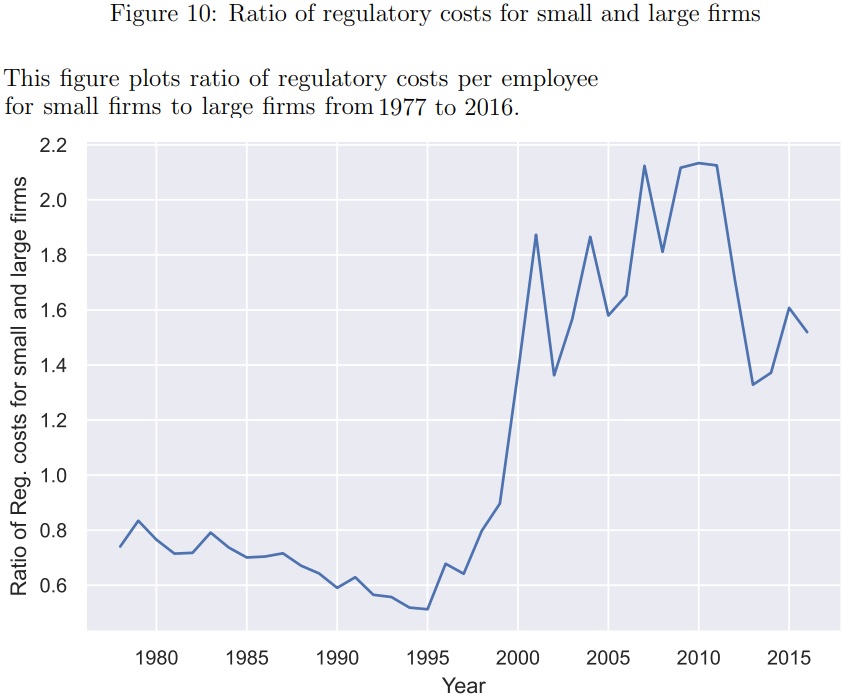

We can now quantify the damage, thanks to some new research by Professor Shikhar Singla, published by Goethe University in Frankfurt.

…the total economy-wide cost of regulations since 1970 has increased by almost 1 trillion dollars, which is roughly 5% of US GDP in 2018. …there has been a massive increase in regulation since the late 1990s. …an average small firm faces an average of $9,093 per employee in our sample period compared to $5,246 for a large firm. …We find that a 100% increase in regulatory costs leads to a 1.2%, 1.4% and 1.9% increase in the number of establishments, employees and wages, respectively, for large firms, whereas it leads to 1.4%, 1.5% and 1.6% decrease in the number of establishments, employees and wages, respectively for small firms… Results on employees and wages provide evidence that an increase in regulatory costs creates a competitive advantage for large firms. Large firms get larger and small firms get smaller. …The smaller the firm, the more competitively disadvantaged it gets… Fixed costs create a competitive disadvantage for small firms. …We find that large firms oppose regulations in general. But, they push for regulations which have an adverse impact on small firms. Hence, they are willing to incur a cost that creates a competitive advantage for them.

How much of a competitive advantage?

It’s become very significant this century, as shown by Figure 10 from the study.

Policy obviously veered in the wrong direction at the end of the Clinton Administration and then (unsurprisingly) stayed bad during the Bush, Obama, and Trump years.

And policy is staying bad during the Biden years.

The Wall Street Journaleditorialized on this topic in 2021. Here are some excerpts.

…what’s really going on: Old-fashioned self-interest. …Take Amazon CEO Jeff Bezos’s endorsement of a higher corporate tax rate. …Mr. Bezos knows a higher rate would hurt Amazon much less than it would other companies. …Mr. Bezos can buy some political goodwill by providing cover to Democrats on taxes, while his company will benefit on the tax subsidy side of the ledger. Big businesses also know they can afford the higher costs of new regulation that smaller competitors cannot. That helps explain Big Oil’s embrace of methane emission rules in the Obama years that hurt independent frackers, as well as putting a price on carbon now. …Or consider the rush by Big Finance to endorse environmental, social and governance investing, or ESG. …BlackRock CEO Larry Fink is an enthusiast, and guess who will benefit if Biden Administration regulators set new requirements for ESG disclosure or investing? ESG lets BlackRock charge higher investment fees than it can charge for index funds that buy the entire market. …corporations look out first and foremost for their own interests, and that often means collaborating with government for narrow purposes that aren’t always in the public interest.

This is disgusting. And it’s not the first time Bezos and Amazon have tried to hurt small businesses.

In the real world, I’ll be happy if we can simply block the left’s ESG agenda so that big companies will be forced to earn money in the market rather than steal money via politics.

Most people instinctively support anti-money laundering laws, but I wonder whether they would change their minds if they understood two very important facts.

As shown in a major study from the World Bank, these laws can deprive poor people of access to banking services.

Regarding the second point, let’s look at some excerpts from a recent report in the New York Times by Tara Siegel Bernard and Ron Lieber.

There are many anecdotes about consumers losing access to banking services, but let’s look at some macro issues.

…financial institutions are obligated to alert regulators and law enforcement through a Suspicious Activity Report if there’s irregular behavior that they cannot easily explain. …if banks fail to report suspicious activity and regulators discover problematic transactions later, banks and their compliance employees are potentially on the hook for all manner of penalties. “So all their incentives are toward closing accounts,” according to an explanation of SARs on the website of the Bank Policy Institute… a median of just 4 percent of 640,000 suspicious activity reports from a sample of large banks warranted a follow-up from law enforcement, according to the research, which examined 16 million alerts.

By the way, some people may think AML laws are worthwhile because 4 percent of reports generate follow up, but that has to be balanced against the estimated $180 billion cost imposed on the private economy.

Money laundering became a federal crime only in 1986… Because the law is so vague and has been subject to so much prosecutorial abuse, including its weaponization for political purposes, there have been calls for its repeal. …The real purpose of many payments between individuals and other individuals, government, or business entities is difficult to prove, which is why so few “stand-alone” money laundering convictions are made. …There is no evidence that the government’s crusade against money laundering has had any appreciable impact on drug dealing, terrorism, or government corruption. …By any objective standard and given the massive cost per conviction in contrast to the few stand-alone convictions, the war on money laundering has been a colossal failure. It has hurt the taxpayers, financial institutions, and, most importantly, Americans’ civil liberties.

Amen. Richard is right. These laws never should have been enacted.

Sadly, many politicians want to expand AML laws by abolishing cash.

P.S. I’m batting .500 in my career as a global money launderer.

That’s true in the United States, and it’s true everywhere else in the world.

And now we have even more evidence thanks to a new National Bureau of Economic Research study by Shang-Jin Wei, Jianhuan Xu, Ge Yin and Xiaobo Zhang. Here’s a description of their methodology.

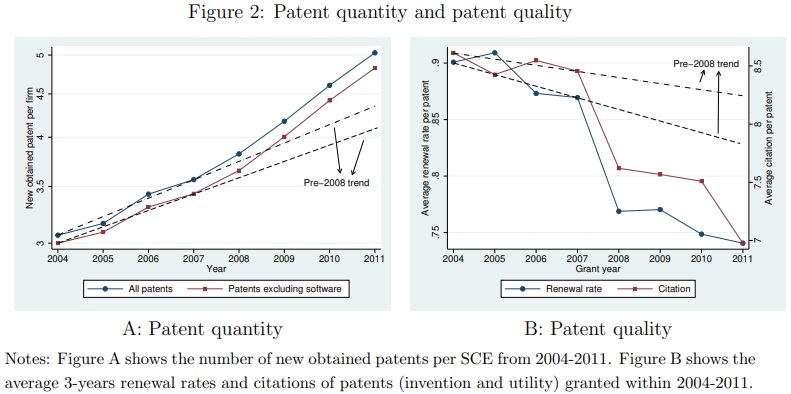

In this paper, we study the consequence of a relatively mild form of government failure – bureaucrats simply being average and not omniscient – on the success or failure of an industrial policy. For example, when a firm applying for a subsidy presents a set of recent patents as proof of its innovation ability to a government committee that reviews the application, the bureaucrats in the committee can count the patents but may not be able to differentiate their quality. …We study these questions in the context of China’s largest pro-innovation industrial policy. The program is known as InnoCom and offers a large subsidy – a 10 percentage points reduction in the corporate income tax rate to successful applicant firms. A major policy change in 2008 expanded the scale of the program greatly… the 2008 policy shock has induced the initially less innovative firms – those with fewer than six patents – in the targeted industries to rush to achieve the desired level of patents for subsidy applications. In addition, a rising share of the new patents owned by them appears to be of low quality. …we study how the patent trade has changed following the 2008 policy shock. In particular, the share of patents sold to initially less innovative firms in the targeted industries exhibits the fastest growth after 2008. This is especially true for patents sold by either the firms outside the targeted industries, which are not eligible for a subsidy anyway, or by the firms in the targeted industries that already had more than six patents before the policy shock and hence do not need more to compete for a subsidy.

What did they find?

As shown in Figure 2, firms responded by having more patents, but those patents had much less value.

Indeed, 98 percent of the patents were low quality.

Even more important, the overall program has destroyed wealth, as measured by a negative net social return.

After calibrating the model to the data, we find that although the subsidy leads to an increase in the patent count by 33%, 98% of the increase is of low quality. This implies a notable decline in the average quality of the new patents. …By comparing the welfare levels in the model with and without the subsidy program, we estimate the net social return to the subsidy to be -19.7%. That is, the society would be better off without this subsidy program. …the thought experiment serves to confirm that the presence of even a mild government failure could convert an…industrial policy from success to failure.

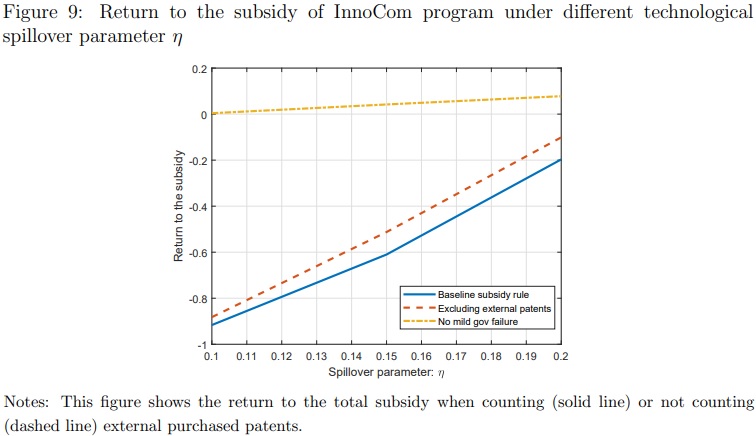

Here’s another visual, this one showing negative rates of return regardless of assumptions of technological spillovers.

One final point that’s worth sharing.

The authors note that industrial policy also causes damage because taxes produce deadweight loss.

…because public funding is financed through distortionary taxation, it costs the society more than 1 RMB to fund 1 RMB worth of subsidy.

Some fans of industrial policy claim that China is an example of successful industrial policy, but that’s nonsense. Total nonsense. Utter nonsense. Unless there are sweeping pro-market reforms, China will continue to lag way behind the United States.

Sometimes, though, politicians don’t even wait for bad results before coming up with new excuses for bigger government.

Last year, a handful of clueless Republicans in the Senate sided with Democrats to enact Joe Biden’s scheme for industrial policy (the so-called CHIPS Act).

But it also should have been opposed because it opened the door for additional forms of government intervention.

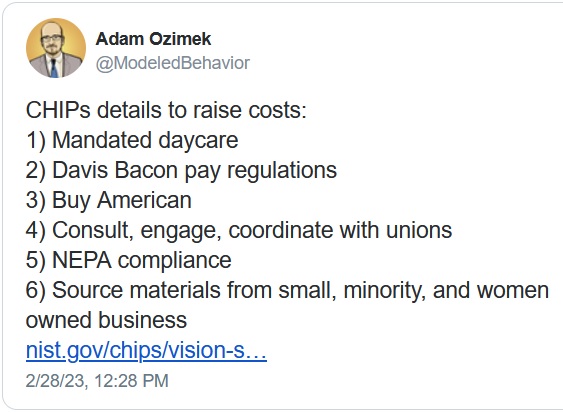

Here’s a tweet from Adam Ozimek that summarizes some of the ways that the Biden Administration is using subsidies as a lure to impose a dirigiste agenda.

Here’s what has happened. Politicians have driven a lot of manufacturing away from the United States because of red tape, mandates, and taxes.

So then politicians figured they could bring production back to American with a big package of subsidies for high-tech companies.

Yet those same politicians are now attaching lots of strings to those subsidies. Companies can only get the handouts if they accept red tape, mandates, and taxes.

Here’s some of the Wall Street Journal‘s editorial on the topic.

Government subsidies are never free, and now we are learning the price U.S. semiconductor firms and others will pay for signing on to President Biden’s industrial policy. They will become the indentured servants of progressive social policy. …the Administration is using the semiconductor subsidies to impose much of the social policy that was in the failed Build Back Better bill. …Start with child care, which chip makers applying for more than $150 million in federal aid will be required to provide to their employees and construction workers. …Chip makers will also have to pay construction workers prevailing wages set by unions and will be “strongly encouraged”—i.e., required—to use project labor agreements (PLAs), which let unions dictate pay, benefits and work rules for all workers. …chip makers will have to describe their “wraparound services to support individuals from underserved and economically disadvantaged communities,” such “as adult care, transportation assistance, or housing assistance.” The Administration is imposing a cradle-to-grave welfare system via corporate subsidies.

The editorial concludes with some very sensible observations about the willful stupidity of the self-styled national conservatives who were cheerleaders for this expansion of government power.

The irony is rich because chip makers have shifted manufacturing to Asia to reduce costs. Producing chips in the U.S. is 40% more expensive than overseas. One reason is the U.S. permitting thicket. But chip makers that receive federal largesse will still have to comply with more regulation under the National Environmental Policy Act. …What a wonderful life if you’re a politician. First, pile on regulation that increase business costs. Then dangle subsidies to drive your social policy… We took a lot of grief from the big-government right for opposing the Chips Act, but these conservatives look like chumps for voting for an industrial policy that is now an engine for progressive policy. And one subsidy is never enough. …Welcome to French industrial policy.

The bottom line is that Biden got a victory, but the American economy suffered a defeat.

Politicians and bureaucrats now have a new tool that they can use to make government a bigger burden on the economy’s productive sector.

At the risk of understatement, that’s not a recipe for economic vitality and competitiveness.

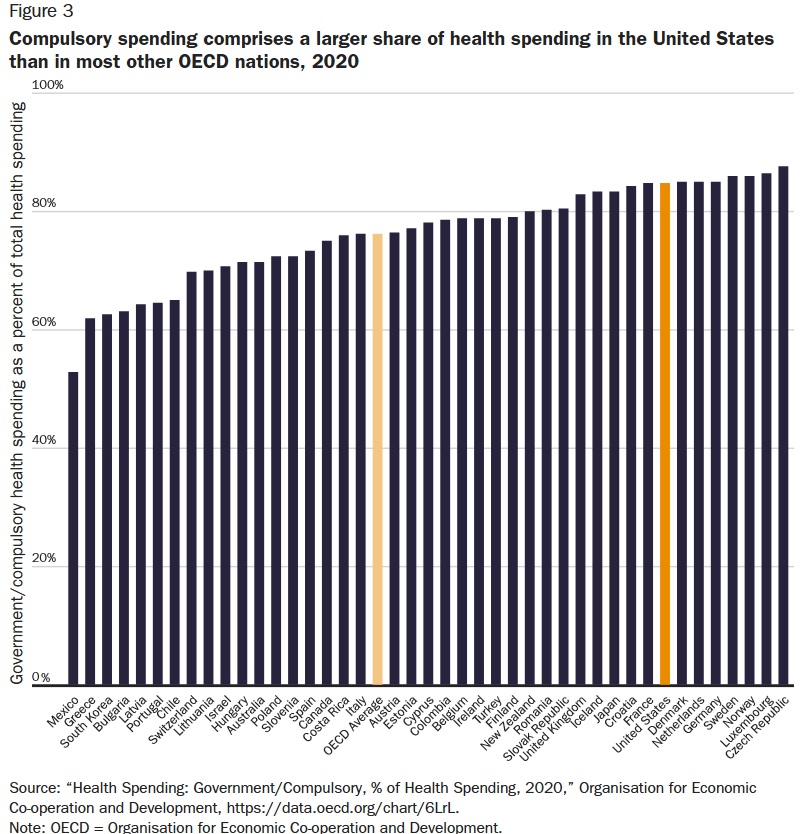

Because of Medicare, Medicaid, and other government programs, taxpayers directly finance about 50 percent of overall health expenditures. Does that mean we have a 50-percent socialist system?

Once again, there’s no easy answer.

On one hand, Uncle Sam does not operate the hospitals and employ the doctors and nurses (like we see – often with horrifying consequences – in the United Kingdom).

If you want words rather than numbers, we have an incoherent and inefficient system that is part socialist, part interventionist, and part market.

That being said, is the US system more market oriented than other nations?

That’s also a hard question to answer. But let’s look at a couple of charts that suggest the answer is more negative than positive.

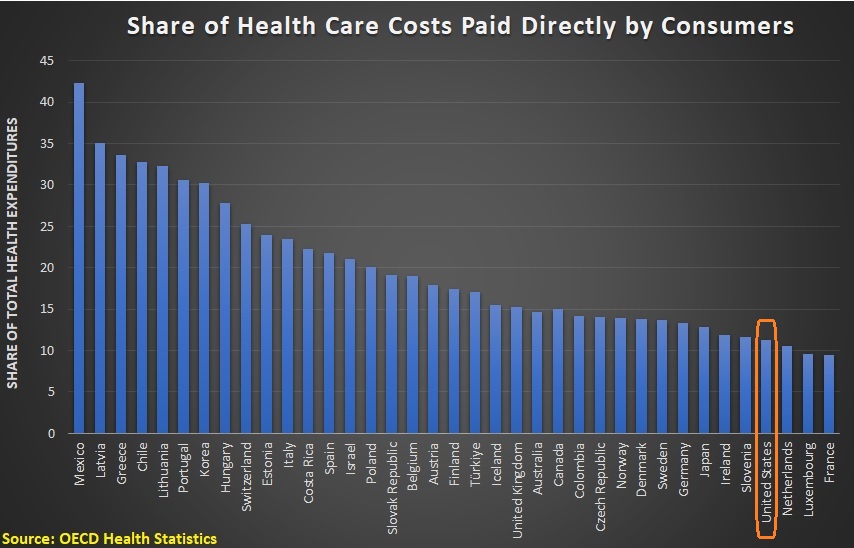

First we have a chart from Michael Cannon’s recent analysis of the tax treatment of healthcare. As you can see, the United States has a much-higher-than-average amount of health spending dictated by government.

In the United States, government has a huge footprint in the health sector.

For our next chart, Andrew Biggs of the American Enterprise Institute shared a chart last year showing which nations have the most third-party payment (i.e., someone other than the consumer paying the cost of healthcare).

It showed that the United States had a much-lower-than-average share of expenses financed by consumers.

But his chart relied on 2016 data and we now have data from 2019. So here’s the latest look at how the United States is not market-oriented, at least when compared to other developed nations.

Basically the same look as the chart from Andrew Biggs, but I didn’t want anyone to think the data may have changed.

I’ll conclude by noting that America’s healthcare system is a mess. But as I explain in this video, it’s a mess because government plays a big role. Even bigger than some of the nations that have “socialist” health systems.

I’ve expressed opposition numerous times to so-called industrial policy because I don’t want politicians and bureaucrats to provide special favors to certain businesses or industries at the expense of everyone else.

That’s a practice known as cronyism, and it is absurd to think that selfish, election-focused politicians somehow correctly identify and subsidize the technologies of tomorrow.

But there are still people who think government should try to steer the economy – including some supposed conservatives.

Let’s remind ourselves why this is a bad idea. Samuel Gregg of the American Institute for Economic Research has a new article about the topic for National Review.

…several polling outfits have indicated an uptick in the number of Americans who say they are disillusioned with capitalism and willing to consider socialism as an alternative. This, however, isn’t the most immediate threat to American capitalism. …It is best labeled “corporatism.” …Examples of full-blown corporatism include distinctly authoritarian regimes such as Mussolini’s Italy, Dollfuss’s Austria, and Franco’s Spain until the mid 1950s. …Following World War II, corporatism took on milder expressions. …whatever the form, corporatism creates serious political and economic problems. Even soft versions of corporatism provide established companies with political mechanisms to advance their interests over those of consumers, taxpayers, and new entrepreneurs… This undermines the ability of businesses to make necessary but often difficult changes. The chances of a business’s becoming complacent and disappearing, along with the jobs it provides, thus multiply. …The expansive versions of stakeholder capitalism favored by progressives and woke capitalists are almost indistinguishable from corporatism. …World Economic Forum chairman Klaus Schwab, for instance, wants a trinity of governments, businesses, and NGOs working together to pursue political goals that are always of the progressive variety. …Not every corporatist is a fascist, but every fascist is a corporatist. Authoritarian economics isn’t just economically foolish. It is also an affront to human liberty and dignity.

Writing in August for Reason, Michael Farren documented the failure of industrial policy.

The once-beleaguered CHIPS Act…reflect a cross-party shift toward embracing industrial policy—the idea that the government should jump into the economy with both feet and have fun getting wet. Facetiousness aside, the neoliberal era from the late 1970s through the 1990s—when economic thinking carried more political sway and resulted in massive deregulation of airlines, railroads, and interstate trucking and the privatization of the internet—is far behind us. …Whether it’s encouragement via subsidies or constraint via regulation, using the government to guide the economy is akin to thinking that just a little bit of cyanide won’t hurt. …Compounding the problem is that people, not some agnostic supercomputer, determine which industries and companies are considered worthy of a boost. Humans are subject to influence and pressure, turning industrial policy into a contest of who can secure the most government favoritism… Lastly, industrial policy motivates “unproductive entrepreneurship.” Some of the best and brightest minds inevitably withdraw from productive activities premised on voluntary exchange, and instead use their skills to find autocratic mechanisms to extract political payoffs… The crystal balls policy makers peer into are easily clouded by charlatans, and we all lose when they win.

For those who want real-world evidence, the unhappy experience of Japan is very enlightening. Adam Thierer wrote last year about the failure of industrial policy in that nation.

American pundits and policymakers are today raising a litany of complaints about Chinese industrial policies, trade practices, industrial espionage and military expansion. …In each case, however, it is easy to find identical fears that were raised about Japan a generation ago. …In 1949, the Japanese government created the Ministry of International Trade and Industry (MITI) to work with other government bodies (especially the Bank of Japan) to devise plans for industrial sectors in which they hoped to make advances. …By the late 1970s, however, U.S. officials and market analysts came to view MITI with a combination of reverence and revulsion, believing that it had concocted an industrial policy cocktail that was fueling Japan’s success at the expense of American companies and interests. …Just as Japan phobia was reaching its zenith in the early 1990s, Japan’s fortunes began taking a turn for the worse. The Japanese stock market crashed… The Nikkei Index peaked at 38,915.87 on Dec. 29, 1989, then began a dramatic fall. It has never reached that level since. …Japan suffered a brutal economic downturn that became known as the Lost Decade, which really lasted almost two decades. Microeconomic planning failures—including many missteps by MITI—were also becoming evident during this time. MITI had made a variety of industrial policy bets that were originally feared by U.S. pundits, only to become embarrassing failures a few years after inception. …by the late 1990s many scholars came to view most Japanese industrial policy initiatives as a costly bust. Marcus Noland of the Peterson Institute for International Economics noted in a 2007 study of Japanese industrial policy efforts, “Attempts to formally model past industrial policy interventions uniformly uncover little, if any, positive impact on productivity, growth, or welfare. …Perhaps most notable in this regard was the Japanese government’s own admission that the MITI model had not worked as well as planned. A 2000 report by the Policy Research Institute within Japan’s Ministry of Finance concluded that “the Japanese model was not the source of Japanese competitiveness but the cause of our failure.”

Writing for Forbes, Stuart Anderson also debunks the notion that industrial policy helped Japan.

…it appears each generation must relearn the lessons of the past as today governments in China, Europe and the United States support industrial policy. Policymakers are convinced that government planning will make national economies better than market forces. “Industrial policy in Japan was not responsible for the country’s economic achievements in the post-war era or the international performance of leading sectors, including autos and electrical machinery,” according to a new study by economist Richard Beason for the National Foundation for American Policy. …He found Japanese industrial policy from 1955 to 1990 did not improve growth rates by sector, provide greater efficiency through economies of scale or result in improved productivity growth or “competitiveness.” …To conduct the research, Beason examined four measures of industrial policy used by the Japanese government during the 1955-1990 period: 1) subsidized government loans to industry, 2) subsidies, 3) tariff protection and 4) tax relief. …“Industrial policy tools generally also had no positive and significant impact on productivity growth (“competitiveness”) for the various sub-periods from 1955 to 1990. …Beason notes that policymakers in Japan abandoned industrial policy, viewing the policies costly, unsuccessful.

Fortunately not. Today’s industrial policy is cronyism, not full-fledged central planning. But it is nonetheless a bad idea to move in the wrong direction.

Way back in 2009, in the early days of writing this column, I shared an image that aptly summarizes the bad things that happen when politicians interfere with economic liberty.

The simple message is that more government is almost always the wrong answer.

Today, we’re going to look at an example of how government spending is the wrong answer.

Here are some excerpts from a story in the Washington Post, but the headline tells you everything you need to know.

The offer to military veterans left unemployed by the coronavirus pandemic was tantalizing: A year of online courses courtesy of the federal government. Graduates would be set up for good jobs in high-demand fields… Schedules were disorganized and courses did not follow a set syllabus. School-provided laptops couldn’t run critical software. And during long stretches of scheduled class time, students were left without instruction… The disarray…is the most painful example of broader problems with the $386 million Veteran Rapid Retraining Assistance Program, or VRRAP. …nearly 90 schools have had their approvals yanked, according to VA officials, including several that were actively serving about 100 veterans. …only about 6,800 veterans had enrolled in the program, far fewer than the 17,250 Congress created it to serve, the agency said; just 397 had landed new jobs.

Some of you may be tempted to conclude that the program was a success since it did result in 397 jobs.

Others will conclude it was a failure since the budget was $386 million, implying each job cost taxpayers nearly $1 million.