Why does the tax code require more than 10,000,000 words and more than 75,000 pages?

There are several reasons and none of them are good. But if you had to pick one cause for all the mess, it would be the fact that politicians have worked with interest groups and lobbyists to create myriad deductions, credits, exclusions, preferences, exemptions, and other loopholes.

to create myriad deductions, credits, exclusions, preferences, exemptions, and other loopholes.

This is a great deal for the lobbyists, who get big fees. It’s a great scam for politicians, who get lots of contributions. And it’s a great outcome for interest groups, who benefit from back-door industrial policy that distorts the economy.

But it’s not great for the American people or the American economy.

Writing for Reason, Veronique de Rugy of the Mercatus Center explains that the net result is a Byzantine tax code that imposes very harsh compliance costs on the productive sector.

According to a 2012 study from the Internal Revenue Service (IRS) and the Treasury Department, …corporations alone spent $104 billion complying with the tax code in 2012. …The cost to individuals may be even higher. According to a 2013 study by Jason Fichtner and Jacob Feldman of the Mercatus Center, Americans face nearly $1 trillion annually in hidden tax-compliance costs. …Why does tax compliance cost so much? The answer is largely that the Internal Revenue Code…is riddled with exclusions, exemptions, deductions, preferential rates, and credits.

And she also points to a solution.

Genuine reform would cut out loopholes that tilt the playing field in favor of those with political connections. It would also aim to provide lower tax rates, fewer tax brackets, and less double taxation of income that is saved and invested. Such measures would be good for growth, but they would also mean taking on the interest groups that benefit from swapping tax preferences for campaign cash.

Since I want to rip up the tax code and replace it with a simple and fair flat tax, this is music to my ears.

Of course, achieving genuine tax reform won’t be easy.

There’s the obvious political obstacle since all the groups that benefit from the current system (politicians, lobbyists, bureaucrats, cronyists, interest groups, and other insiders) will fiercely resist reform.

There’s also a policy obstacle because many people oppose loopholes in theory but they haven’t paid sufficient attention to the nuts-and-bolts details.

With that in mind, let’s set out a set of guiding principles for the elimination of tax loopholes and the creation of a neutral tax system.

1. A loophole exists when income isn’t taxed – In libertarian Nirvana, the central government is so small that there’s no need for an income tax. Until we get to that point, though, we’re stuck with the internal revenue code and the goal should be to collect revenue (hopefully a modest amount) in a way that minimizes the economic damage per dollar collected. And that means a tax code that doesn’t have loopholes, which are best defined as provisions that enable people to avoid any tax based on how they earn income or how they spend income. In a neutral system, all income is taxed one time.

2. The economy performs better without a loophole-riddled tax code – Most people understand that high tax rates are bad for growth because they penalize people for earning income. They also generally understand that double taxation of saving and investment is bad for growth because it creates a bias against capital formation. But there’s not nearly enough appreciation of the fact that loopholes in the code are bad for growth since they are a back-door form of industrial policy that exist for the purpose of incentivizing people to make decisions on the basis of tax rather than on the basis of what makes economic sense. A neutral tax system means less economic damage.

3. It’s not a loophole to protect income from double taxation or to require income to be measured correctly – The bad news is that the current system forces taxpayers to overstate their income and it also imposes multiple layers of tax on income that is saved and invested. The good news is that there are provisions in the tax code – such as IRAs, 401(k)s, deferral, bonus depreciation – that seek to mitigate these biases. These parts of the system oftentimes are needlessly complex and they frequently will alleviate penalties in a discriminatory manner, but they are not loopholes. In a neutral system, all income is taxed only one time.

multiple layers of tax on income that is saved and invested. The good news is that there are provisions in the tax code – such as IRAs, 401(k)s, deferral, bonus depreciation – that seek to mitigate these biases. These parts of the system oftentimes are needlessly complex and they frequently will alleviate penalties in a discriminatory manner, but they are not loopholes. In a neutral system, all income is taxed only one time.

4. Loopholes should be eliminated as part of a plan to lower tax rates, not in order to give politicians more money – If loopholes are a corrupt and distorting dark cloud, the silver lining to that cloud is that all the special favors in the tax code deprive the government of tax revenue. Even the most egregious of loopholes, such as ethanol, have this redeeming feature. This is why loopholes should only be eliminated as part of an overall tax reform plan that also lowers tax rates and reduces double taxation. A neutral tax system shouldn’t enable bigger government.

There are some important implications that follow from these four guiding principles.

As a practical matter, we can now identify provisions in the tax code that are clearly loopholes, such as the healthcare exclusion, the municipal bond exemption, and the state and local tax deduction (the mortgage interest deduction is misguided, but isn’t technically a loophole since one of the goals of tax reform is to give business investment the same tax-income-only-one-time treatment now reserved for residential real estate).

We also know that the capital gains tax rate isn’t a “preferential” loophole, but instead is the mitigation of a penalty that shouldn’t exist. Similarly, it’s not a loophole when companies deduct expenses when calculating income. And you’re not getting some sort of handout simply because Uncle Sam isn’t imposing double taxation on your retirement account. At the risk of repeating myself, all income should be taxed in a neutral system, but only one time.

Let’s close by looking at a few secondary – but still important – implications of a neutral tax code.

First, getting rid of loopholes won’t put a burden on poor and middle-income taxpayers for the simple reason that an overwhelming share of the benefits of these provisions go to high-income taxpayers.

First, getting rid of loopholes won’t put a burden on poor and middle-income taxpayers for the simple reason that an overwhelming share of the benefits of these provisions go to high-income taxpayers.

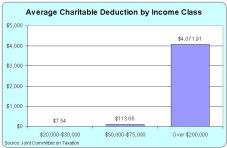

I’ve already shown how the vast majority of charitable deductions are taken by those making more than $200,000 per year.

The same is true for the state and local tax deduction and the healthcare exclusion.

And the Washington Post just editorialized that the home mortgage interest deduction is a boon for rich taxpayers as well.

The mortgage interest deduction is also a significant cause of after-tax income inequality: The top 20 percent of earners get 75 percent of the benefits; the top 1 percent get 15 percent, according to the Congressional Budget Office. …Specifically, 10 metropolitan “hot spot” counties (among them Los Angeles in California and Fairfax in Virginia) with the greatest number of mortgages larger than $500,000 accounted for 45.1 percent of all such mortgages nationally. Just eight California urban and suburban counties accounted for 40 percent of the national total. Outside of such tony coastal precincts, the only big-mortgage hot spots were resort destinations such as Martha’s Vineyard, Mass., and Vail, Colo. — where many homes are vacation places, not primary residences.

To be sure, the Post is misguided in that it wants to restrict tax preferences in order to finance a larger burden of government spending.

So I’m not expecting the editors to join a coalition for pro-growth tax reform.

The second implication is that a neutral tax system means less corruption.

To cite one example, consider the oleaginous way that politicians deal with so-called tax extenders. Marc Short and Andy Koenig explain in a column they wrote for the New York Times.

Congress will soon take up the so-called tax extenders package, which has more than 50 tax breaks affecting a variety of industries and issues. …this bill mostly helps the wealthy and the well connected.

The fact that rich insiders benefit is no surprise, but what makes “tax extenders” so odious is that what began in 1988 as a supposedly one-time fix now has become a regular part of the process, a scam that gives lobbyists and politicians a way of generating fees and contributions.

The first tax-extender package…opened a door that lobbyists and lawmakers were all too willing to run through. …A 2014 analysis by Americans for Tax Fairness found that more than one out of every 10 lobbyists in Washington focused specifically on the extenders package. Given that this bill comes up about every year or two, special interests constantly have the opportunity to demand new handouts.

By the way, some of the extenders actually are good policy. They’re in the mitigation-of-penalties category I discussed above.

But those good provisions should be made permanent and the bad provisions should be jettisoned.

Unfortunately, that’s not in the interests of the politicians and lobbyists who benefit from an annual extender package, so the problem doubtlessly will fester.

Last but not least, let’s consider the moral component.

For those of us who believe in justice, it is ethically offensive that some rich and powerful taxpayer get better treatment simply because they know how to manipulate the political process.

This violates the important principle that the law should treat everyone alike. Yet another reason to have a simple and fair flat tax.

P.S. At the risk of being a nit-picker about my own writing, I should confess that a flat tax is not a purely neutral tax system. There will still be a penalty on earning income. But the penalty presumably will be modest if there is a low rate and that penalty won’t be exacerbated by penalties and loopholes that distort how people earn income and spend income.

P.P.S. Here, in one image, is all you really need to know about the economics of taxation.

[…] asked about tax loopholes, my first reaction is to determine whether something is an actual tax preference or merely a […]

[…] by contrast, discourage productive behavior while also giving people a bigger incentive to find loopholes and other ways of avoiding […]

[…] Elimination of unfair and corrupt loopholes. […]

[…] instance, even though I don’t like itemized deductions for things like charitable contributions and home mortgage interest, I am glad when taxpayers are […]

[…] start with a definition. A tax expenditure is basically a loophole in the tax code. And these loopholes are called tax expenditures because they are seen as being equivalent to a […]

[…] There are no loopholes. […]

[…] For those unfamiliar with the term, tax expenditures are special preferences in the tax code. In other words, tax loopholes. […]

[…] income is exempt from tax, other than a family-based […]

[…] income is exempt from tax, other than a family-based […]

[…] it is true that some provisions of the tax code create distortions and should be eliminated as part of tax […]

[…] Grotesque unfairness […]

[…] As an economist, however, I don’t like when people are lured into make inefficient choices simply because of a convoluted tax system. […]

[…] As an economist, however, I don’t like when people are lured into make inefficient choices simply because of a convoluted tax system. […]

[…] We got lower rates and moved closer to neutrality. […]

[…] Corrupt, complex, and inefficient loopholes. […]

[…] Corrupt, complex, and inefficient loopholes. […]

[…] by contrast, discourage productive behavior while also giving people a bigger incentive to find loopholes and other ways of avoiding […]

[…] No more corrupt, complex, and inefficient loopholes. […]

[…] by contrast, discourage productive behavior while also giving people a bigger incentive to find loopholes and other ways of avoiding […]

[…] by contrast, discourage productive behavior while also giving people a bigger incentive to find loopholes and other ways of avoiding […]

[…] Distortionary loopholes that reward inefficiency and promote corruption. […]

[…] Tax cuts are not a “cost” to government, they’re a “savings” to taxpayers. This is why provisions in the tax code that allow taxpayers to keep more of their money should not be referred to as “tax expenditures.” Even if they are bad policy. […]

[…] So Louisiana voters opted for a win-win situation of lower rates and getting rid of a loophole. […]

[…] So Louisiana voters opted for a win-win situation of lower rates and getting rid of a loophole. […]

[…] money honestly), I generally want lower taxes for upper-income taxpayers. But I don’t want special tax breaks for rich people. Instead, I want to cut their taxes in ways that promote greater national […]

[…] money honestly), I generally want lower taxes for upper-income taxpayers. But I don’t want special tax breaks for rich people. Instead, I want to cut their taxes in ways that promote greater national […]

[…] No tax preferences that distort the economy […]

[…] tax preferences that distort the […]

[…] No tax preferences that distort the economy […]

[…] tax preferences that distort the […]

[…] No corrupt preferences that distort economic choices. […]

[…] No complicating preferences and loopholes that encourage inefficient economic choices. […]

[…] Loopholes to encourage inefficiency. […]

[…] No complicating preferences and loopholes that encourage inefficient economic choices. […]

[…] of cronyism in the United States (ethanol handouts, the Export-Import Bank, protectionism, tax favoritism, bailouts, subsidies, and green energy are just a few examples of how the friends of politicians […]

[…] No preferences and loopholes that encourage inefficient economic choices. […]

[…] No preferences and loopholes that encourage inefficient economic choices. […]

[…] other loopholes, it should be repealed. But not so politicians get more […]

[…] that’s true, it would be morally and economically appropriate to remove that […]

[…] it’s a good idea to treat all businesses the […]

[…] to say, there are many loopholes to exploit in a 75,000-page tax […]

[…] they basically exist to lure people into making decisions that otherwise aren’t economically […]

[…] es el término para cuando los políticos recaudan más ingresos al revocar o limitar las deducciones, exenciones, exclusiones, créditos y otras preferencias fiscales (“reforma fiscal” es el término para cuando los políticos revocan o limitan las […]

[…] broadening” is the term for when politicians collect more revenue by repealing or limiting deductions, exemptions, exclusions, credits, and other tax preferences (“tax reform” is the term for when politicians repeal or limit preferences and use the […]

[…] broadening” is the term for when politicians collect more revenue by repealing or limiting deductions, exemptions, exclusions, credits, and other tax preferences (“tax reform” is the term for when politicians repeal or limit preferences and use the […]

[…] companies. The purpose of policies such as ethanol handouts, the Export-Import Bank, protectionism, tax favoritism, bailouts, subsidies, and green energy is to provide unearned wealth to the friends of […]

[…] policy. So I have to direct people to various columns about marginal tax rates, double taxation, tax favoritism, tax reform, corporate taxation, and tax […]

[…] I actually agree with both of his arguments. Giving states extraterritorial tax powers isn’t an attack on the Internet. And I also agree that tax policy shouldn’t provide special preferences. […]

[…] Fewer loopholes […]

[…] looking at the key principles of good tax reform (reducing tax rates, reducing double taxation, and reducing distortionary preferences). Final grade […]

[…] are big areas of overlap. We both like spending restraint. We both favor getting rid of loopholes (though I fear she may favor the Haig-Simons definition of loopholes rather than […]

[…] are big areas of overlap. We both like spending restraint. We both favor getting rid of loopholes (though I fear she may favor the Haig-Simons definition of loopholes rather than the […]

[…] Yes, but it’s more than that. Are subsidies cronyism? Yes, but it’s more than that. Are favors in the tax code cronyism? Yes, but it’s more than that. Are trade barriers cronyism? Yes, but it’s more […]

[…] End distorting preferences in order to reduce economically irrational decisions. […]

[…] are weak on spending, will they achieve deficit neutrality (necessary for permanent reform) by eliminating loopholes? That’s a good idea, but interest groups will […]

[…] be permanent. But that means coming up with tax increases to offset tax cuts. That’s okay if undesirable tax preferences are being eliminated to produce more revenue, but defenders of those loopholes will then lobby against the […]

[…] damage is not only the result of high tax rates and pervasive double taxation, but also because of loopholes that exist to bribe people into making economically unwise […]

[…] damage is not only the result of high tax rates and pervasive double taxation, but also because of loopholes that exist to bribe people into making economically unwise […]

[…] distorting preferences in order to reduce economically irrational […]

[…] decisions based on what makes economic sense rather than because they’re taking advantage of some bizarre quirk in the tax […]

[…] The bottom line is that there are big divisions. There is (thankfully) a lot of opposition to the border-adjustable tax, and there’s also no agreement on whether the tax plan should be a pure tax cut or whether it should be a revenue-neutral package that finances lower tax rates by eliminating or curtailing undesirable preferences. […]

[…] is good the end distorting preferences in order to reduce economically irrational […]

[…] part, because there would be no distorting tax breaks that lure people into making decisions based on tax considerations rather than economic […]

[…] are discouraged from investing and producing in America. Firms also have an incentive to seek out deductions, credits, exemptions, and other preferences when rates are high. And multinational companies understandably will seek to minimize the amount of […]

[…] are discouraged from investing and producing in America. Firms also have an incentive to seek out deductions, credits, exemptions, and other preferences when rates are high. And multinational companies understandably will seek to minimize the amount of […]

[…] the border-adjustable provision and focus on lowering tax rates, reducing double taxation, and cutting back on loopholes. Such ideas are economically sounder and politically […]

[…] the border-adjustable provision and focus on lowering tax rates, reducing double taxation, and cutting back on loopholes. Such ideas are economically sounder and politically […]

[…] the border-adjustable provision and focus on lowering tax rates, reducing double taxation, and cutting back on loopholes. Such ideas are economically sounder and politically […]

[…] for fundamental reform is driven by my desire for a low rate, for no double taxation, and for the elimination of loopholes. Those are the economic reasons for […]

[…] argue for the flat tax, I tend to focus on the economic benefits (low rate, no double taxation, and no loopholes) and the moral benefits (less corruption, more fairness, and better […]

[…] idea, period. Cronyism is also bad in agriculture. It’s bad in finance. It’s bad in the tax code. It’s bad in energy. It’s bad […]

[…] Yes, but it’s more than that. Are subsidies cronyism? Yes, but it’s more than that. Are favors in the tax code cronyism? Yes, but it’s more than that. Are trade barriers cronyism? Yes, but it’s more […]

[…] Yes, but it’s more than that. Are subsidies cronyism? Yes, but it’s more than that. Are favors in the tax code cronyism? Yes, but it’s more than that. Are trade barriers cronyism? Yes, but it’s more than […]

[…] Yes, but it’s more than that. Are subsidies cronyism? Yes, but it’s more than that. Are favors in the tax code cronyism? Yes, but it’s more than that. Are trade barriers cronyism? Yes, but it’s more […]

[…] this also can be a win-win situation since there are many distortionary preferences in the tax code that lure people into making economically inefficient decisions solely because of […]

[…] doesn’t necessarily mean we’re necessarily talking about good policy since there are plenty of preferential tax laws that should be wiped out as part of a shift to a simple and fair flat […]

[…] income is shielded from taxation, either based on how it is earned or how it is spent, that creates an incentive for taxpayers to […]

[…] is it the loss of economic output caused by high tax rates, distorting preferences, and pervasive double taxation (i.e., policies that reduce our pre-tax […]

[…] loopholes or special preferences – The tax code shouldn’t be riddled with corrupt deductions, exemptions, exclusions, credits, and other […]

[…] the worst loophole (properly defined) in the cluttered internal revenue […]

[…] the worst loophole (properly defined) in the cluttered internal revenue […]

[…] the worst loophole (properly defined) in the cluttered internal revenue […]

[…] Ubiquitous loopholes that lure people into inefficient choices. […]

[…] Ubiquitous loopholes that lure people into inefficient choices. […]

[…] There’s a reason for the fixation on tax avoidance, of course. Politicians realize that they need to demonize legal tax if they want to impose big tax hikes by shutting down loopholes (both the real ones and the fake ones). […]

[…] I confess that my anti-tax resolve sometimes gets a bit wobbly when I think about unsavory tax breaks such as the ethanol credit, the state and local tax deduction, and the healthcare exclusion. I have […]

[…] “everything” they need to know about a topic. I’ve used that tactic when writing about tax loopholes, entitlements, fiscal policy, bureaucracy(twice), tax evasion, France, Greece, corporate […]

[…] they need to know about a topic. I’ve used that tactic when writing about tax loopholes, entitlements, fiscal policy, bureaucracy (twice), tax evasion, France, Greece, corporate […]

[…] is about the desire for a fair system that neither punishes people for being productive nor rewards them for being politically powerful. As is etched above the entrance to the Supreme Court, the law should treat everyone […]

[…] no distorting preferences for charity or housing. And no double taxation of any form, along with expensing instead of […]

[…] no distorting preferences for charity or housing. And no double taxation of any form, along with expensing instead of […]

[…] But since most of my fantasies won’t happen (at least in the near future), my intermediate goal is to junk the current tax system and replace it with a simple and fair flat tax, which would mean a low tax rate, no double taxation, and no corrupt and distorting tax preferences. […]

[…] businesses are focused on harvesting favors from Washington (such as bailouts, export subsidies, special tax preferences, etc), that is a very depressing indication of a cronyist economy rather than a capitalist economy. […]

5 ways to earn money with instagrams http://ow.ly/Vj9ZB

The largest crony industry in the nation is “lawyers”. The second largest is “government” staffed by legal craftpersons(?) created by lawyers. The third is welfare recipients that support politicians who make the laws that constructed the command economy leaching off the working rich, middle class, and yes, the poor as well. In its perfected state, it will achieve a no growth economy of adolescent, sophomoric decadence.