I wrote three days ago about the worst-international-bureaucracy contest between the International Monetary Fund and the Organization for Economic Cooperation and Development.

A reader emailed to ask me whether I had a favorite international bureaucracy. I confess I’ve never given that matter any thought. My gut-instinct answer would be the World Trade Organization since its mission is to discourage protectionism.

But I’m also somewhat fond of the European Central Bank, both because the euro has been better than many of the currencies it replaced and because the ECB often publishes good research.

- Two studies (here and here) on the benefits of spending caps.

- Two studies (here and here) showing small government is more efficient.

- Two studies (here and here) on how large public sectors retard growth.

- And also studies on the adverse impact of regulation, bureaucracy, and welfare.

And here’s a study on regulation to add to the collection. The European Central Bank published a working paper that looks at the effect of selected pro-market reforms. Here’s their methodology.

In this paper, we investigate the relationship between a wide range of structural reforms and economic performance over a ten-year time horizon. …we identify 23 episodes of wide-reaching structural reform implementation (so-called “reform waves”).

These are based on a database…which provides detailed information on both real and financial sector reforms in 156 advanced and developing countries over a 40 year period. Indicators considered specifically cover trade-, product market-, agriculture-, and capital-account liberalisation, together with financial and banking sector reform. Then, we track top-reforming countries over the 10 years following adoption and estimate the dynamic impact of reforms.

And here’s an excerpt that describes the theoretical assumptions.

…orthodox economic theory has made a strong case for structural reforms, identified as measures aimed at removing supply-side constraints in an economy. This in turn would favour efficient factor allocation and contribute to medium- to long-term growth. Such measures include, but are not limited to, product and labour market liberalisations, current and capital account openness, and financial liberalisation. For a long time, a collection of these policies has fallen under the name of Washington Consensus.

I agree with this theory, though allow me to elaborate.

The Fraser Institute’s Economic Freedom of the World is the gold standard when looking at overall economic policy. It considers five major factors – fiscal policy, trade policy, regulatory policy, monetary policy, and governance policy (indicators such as rule of law and property rights).

The “Washington Consensus” also is based on good policy, but it undervalues the importance of a small burden of government spending.

But I’m digressing. Let’s return to the ECB study, which basically looks at the impact of trade liberalization and deregulation. Here’s what the authors found.

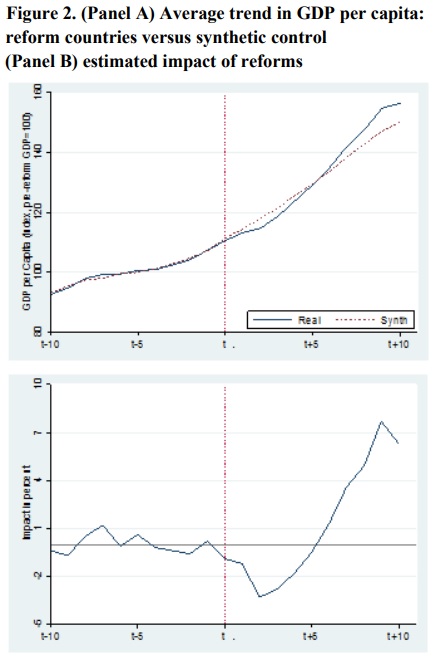

Our main findings are as follows: on average, reforms had a negative but statistically insignificant impact in the short term. This slowdown seems to be connected to the economic cycle, and the tendency to implement reforms during a downturn, rather than an effect of reforms per se. Reforming countries however experienced a growth acceleration in the medium-term. As a result, ten years after the reform wave started, GDP per capita was roughly 6 percentage points higher than the synthetic counterfactual scenario.

Here’s a chart from the study illustrating the positive effect of reform.

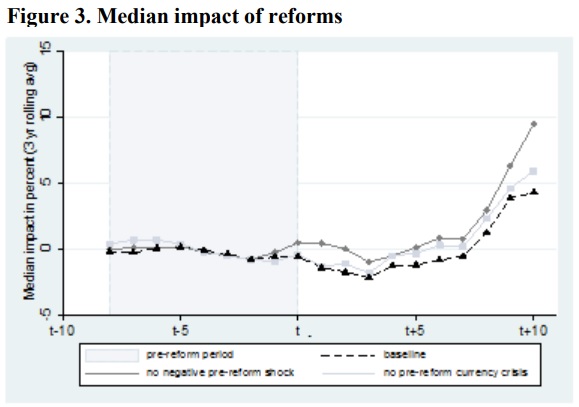

And here’s another chart from the ECB report looking at the results from another perspective.

The obvious good news from this research is that we have new evidence about the benefits of pro-market reforms. Boosting economic output by an extra 6.3 percent is nothing to sneeze at. And it reinforces my oft-made point that even small improvements in growth – if sustained over time – can lead to dramatic improvements in living standards.

What might be most noteworthy in this study, however, is the finding that pro-market reforms are associated with a short-run dip in economic performance. The authors suggested that it might be a statistical quirk related to the fact that governments have a “tendency to implement reforms during a downturn”.

That’s certainly plausible, but I’m also open to the notion that good reforms sometimes may have short-run costs. Simply stated, if bad policy has produced a misallocation of labor and capital, then pro-growth reforms are going to cause some temporary disruption.

But unless you’re planning on dying very soon and also don’t care about your heirs, that’s not an argument against reform. For example, I think the housing lobby’s opposition to the flat tax is misguided since every sector will enjoy long-run benefits from faster growth, but it’s certainly possible that residential real estate will endure some short-run weakness as some resources shift to business investment.

Unfortunately, politicians tend to have very short time horizons (i.e., the next election), so they fixate on short-run costs and under-value long-run benefits.

But I’m digressing again. Let’s look at one final passage from the ECB study. For those interested in additional research, there’s a section citing some of the other literature on liberalization and growth.

Post-Soviet countries moving towards a market economy have received considerable attention in this respect. Fischer et al. (1996) looked at 26 transition economies over the period 1989-1994. They conclude that structural reforms played a vital role in reviving economic growth. This finding for transition economies was echoed by de Melo et al. (1996), and more recently by Havrylyshyn and van Rooden (2003) and Eicher and Schreiber (2010). Focussing more broadly on countries implementing wide reform packages covering domestic finance, trade, and the capital account, Christiansen et al. (2013) find a strong impact of the former two on growth in middle-income countries. Moreover, they show how well-developed property rights are a precondition in order to reap fully the benefits of structural reforms. The importance of institutions in explaining cross-country heterogeneity is further remarked by Prati et al. (2013), who illustrate how the positive relationship between structural reforms and growth depends on a country’s constraints on the authority of the executive power. Distance from the technological frontier seems also to play a role.

If you’re not familiar with technological jargon, “distance from the technological frontier” is basically a way of saying that nations with lots of bad policy – and thus lots of misallocated and/or underutilized labor and capital – probably have more ability to enjoy fast growth. Sort of a version of convergence theory.

I also like the reference to “constraints on the authority of the executive power,” which presumably a recognition of the importance of the rule of law.

The bottom line is that the ECB study reconfirms that free enterprise is the answer if the goal is reducing poverty and increasing prosperity.

[…] article also cites research from two European Central Bank economists, which I wrote about back in […]

[…] not to overstate the importance of short-run data. And I also fully agree that there’s often a time lag between the adoption of good policy and the evidence of good […]

[…] not to overstate the importance of short-run data. And I also fully agree that there’s often a time lag between the adoption of good policy and the evidence of good […]

[…] bottom line is that even trivial pro-growth reforms are worth the effort. Even if it takes a few years for the growth to materialize or if the growth only lasts for a limited period of […]

[…] bottom line is that even trivial pro-growth reforms are worth the effort. Even if it takes a few years for the growth to materialize or if the growth only lasts for a limited period of […]

[…] It takes time for investment to increase, so the resulting improvements in productivity and wages don’t occur immediately. […]

[…] of labour and capital in eight macro-sectors,” and also found that reform could boost national income by more than six […]

If you’re going to give the EU/ECB credit for their so-called safeguards, you should at least look at whether those safeguards worked.

When the Euro was created (administratively) in 1997, it came with a “stability pact” that purported to cap both the deficits each country could run (at 2% of GDP) and the national debt each could have (50% of GDP). Both limits were backed by the threat of expulsion from using the Euro. They also made it expressly illegal, by treaty, for any member country to bail out another in the event of default.

In practice, all the Euro members except Germany had to fudge the numbers even to say they were in compliance with the limits on opening day, and have been fudging them more and more ever since. And the no-bailout rule has been replaced by mandatory bailouts. Why have no heads rolled over these betrayals? Because the EU is designed to keep its decision makers unaccountable. All its power resides in unelected bureaucrats who answer to no one but themselves.

I believe that the EU’s largest member countries are already faking election results to prevent their voters from taking them out of the union, and that soon it will become impossible to continue hiding the fraud. Good. It’s about time.