In an ideal world, Americans would have personal retirement accounts, just like workers in Australia, Sweden, Chile, Hong Kong, Israel, Switzerland, and a few dozen other nations.

But we’re not in that ideal world. We are forced to participate in a Ponzi Scheme known as Social Security.

But we’re not in that ideal world. We are forced to participate in a Ponzi Scheme known as Social Security.

By the way, that’s not necessarily a disparaging description. A Ponzi Scheme can work if there are always enough new people in the system to pay off the old people.

But because of demographic changes (increasing lifespans and decreasing birthrates), that’s not what we have in the United States.

And this is why Social Security faces serious long-run problems.

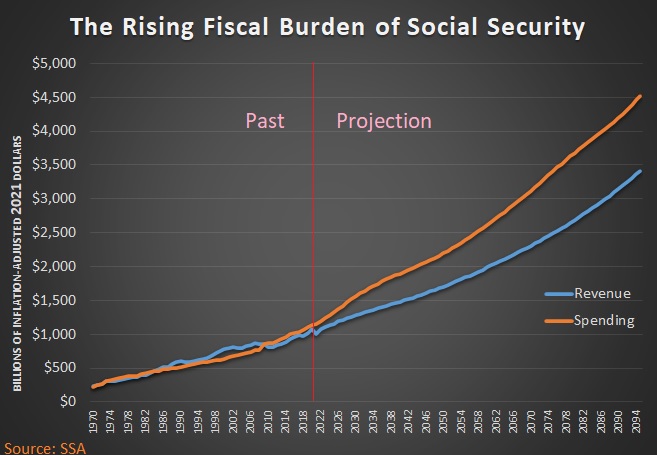

How serious? The Social Security Administration finally released the annual Trustees Report. This document has a wealth of data on the program’s financial condition, and Table VI.G9 is where the rubber meets the road.

As you can see from this chart, there will be an ever-increasing burden of Social Security taxes and spending over the next 75 years. And these numbers are adjusted for inflation!

The good news (relatively speaking) is that the economy also will be growing over the next 75 years, both in nominal terms and inflation-adjusted terms.

The bad news is that spending on Social Security will grow at a faster rate, so the program will consume a larger share of the economy’s output.

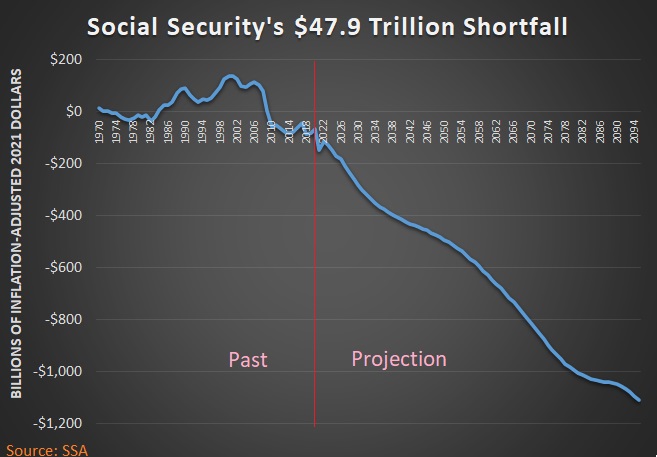

And because Social Security spending is growing faster than the economy (and also faster than tax revenue), this next chart shows there is going to be more and more red ink in the future. Once again, you’re looking at inflation-adjusted data.

As indicated by the chart’s title, the cumulative shortfall over the next 75 years is nearly $48 trillion. That’s a lot of money, even by Washington standards.

And with each passing year, the problem seems to worsen. The 75-year shortfall was $44.7 trillion according to the 2020 report and $42.1 trillion according to the 2019 report.

I’ll conclude by observing that today’s column focuses on the big-picture fiscal problems with Social Security.

I’ll conclude by observing that today’s column focuses on the big-picture fiscal problems with Social Security.

But let’s not forget the program’s second crisis, which is the fact that Americans are deprived of the ability to enjoy much higher levels of retirement income.

Certain groups are particularly harmed by this aspect of the current program, including minorities, women, older workers, and low-income workers.

P.S. Our friends on the left argue that the program’s fiscal problems (the first crisis) can be solved with tax increases. Perhaps that is true, but it will mean a weaker economy and it will exacerbate the second crisis by forcing workers to pay more to get less.

P.P.S. I once made a $16 trillion dollar mistake on national TV when discussing Social Security’s shaky finances.

P.P.P.S. Much of the news coverage about the Trustees Report has focused on the year the Social Security Trust Fund supposedly runs out of money. But this is sloppy journalism since the Trust Fund has nothing but IOUs (as illustrated by this joke).

[…] the yearly forecast of the program’s long-run finances. Jut like I did in 2023, 2022, 2021, 2020, etc, it’s time to see what to expect in the […]

[…] 2023 Social Security Trustees Report was released yesterday, and just like I did last year (and the year before, and the year before that, etc), let’s look at the fiscal status of the retirement […]

[…] 2023 Social Security Trustees Report was released yesterday, and just like I did last year (and the year before, and the year before that, etc), let’s look at the fiscal status of the retirement […]

[…] 2023 Social Security Trustees Report was released yesterday, and just like I did last year (and the year before, and the year before that, etc), let’s look at the fiscal status of the retirement […]

[…] 2023 Social Security Trustees Report was released yesterday, and just like I did last year (and the year before, and the year before that, etc), let’s look at the fiscal status of the retirement […]

[…] 2023 Social Security Trustees Report was released yesterday, and just like I did last year (and the year before, and the year before that, etc), let’s look at the fiscal status of the retirement […]

[…] 2023 Social Security Trustees Report was released yesterday, and just like I did last year (and the year before, and the year before that, etc), let’s look at the fiscal status of the retirement […]

[…] the make-believe country of Libertaria, there is no such thing as Social Security or any other type of government-mandated retirement […]

[…] The Real (and Growing) Problem with Social Security […]

[…] Shifting to a system of personal retirement accounts means trillions of dollars of near-term “transition costs” in order to protect current retirees and older workers, but reform will solve the program’s long-term $40 trillion-plus unfunded liability. […]

[…] The Real (and Growing) Problem with Social Security […]

[…] And that’s much better than “pay-as-you-go” systems, like we have in the United States. […]

[…] The Real (and Growing) Problem with Social Security […]

[…] The Real (and Growing) Problem with Social Security […]

[…] The Real (and Growing) Problem with Social Security […]

[…] This raises all sorts of challenging questions, such as what’s the value of a life saved compared to the value of lives that might have existed (a philosopher might have a different answer than an actuary at the Social Security Administration!). […]

[…] The Real (and Growing) Problem with Social Security […]

I agree with you: (1) things are not good; (2) the members of Congress were elected to serve the people, not their own bank account; (3) as A. Lincoln once said, “You can fool all the people some of the time, and you can fool some of the people ALL the time, but you CAN’T fool all the people all the time”, so we (the public) must wake them up. It’s our job to force our politicians to fix this problem in a REAL way, not just with ‘smoke ‘n’ mirrors, as has been done many times in the past. Oh, and another quote comes to mind, this one by Karl Marx — one of the fathers of communism — “Kill all the lawyers!”).

For you old codgers, like me, chances are pretty certain that we will be dead by the time 2094 comes around. (I hold out some small chance that medical science – through DNA research and development – may find a way to prolong a healthy life – for those who want it and can afford it.) Nevertheless, if we are still voting, we need to change this situation for the good –> what’s ‘for the good’? The program needs to be made solvent.

So, what’s my long-lasting and fair solution? Require that all the Congresses ‘retirement money’ be put into the Soc. Sec. Fund; require that Congress pay the same Soc. Sec. contributions that the public must pay (including their staff members); require that their monthly retirement distribution checks from their ‘working’ years (including their work(?!) in Congress) be paid to them at the same rate as is paid to other members of Soc. Sec.; require that they pay Income Tax on Soc. Sec. as do all the rest of us, etc.

In short, abolish the existing retirement ‘perks’ and separate retire fund(s) that they have, collectively, created for themselves, and make them subject to all the laws to which the rest of the public are subject. Let’s move to eliminate the ‘elitist club’ they’ve created by beginning with changes to the Social Security program.

This arithmetic is always worrisome, but it obscures the “real” issues we have to deal with. It’s a societal decision to determine what slice of the overall pie (yearly gdp) granny and grandpa (that’s you and me) get and, to some extent, from what source. Tax (“contribution”) rates and benefits levels are always subject to adjustment to provide the degree of pie sharing society chooses. Also, there are other tweaks available like cutting off all SS benefits to professors who have cushy private retirement funds built up.

[…] https://danieljmitchell.wordpress.com/2021/09/01/the-real-and-growing-problem-with-social-security/ […]

Is part of the downfall of social security retirement due to its expansion to include disability?