Earlier today at the Friedman Conference in Australia, I spoke on the proper design of a tax system.

My goal was to explain the problem of double taxation.

My goal was to explain the problem of double taxation.

I’ve repeatedly shared a flowchart to illustrate the pervasive double taxation in the current system (my example is for the United States, but many other nations make the same mistake).

And to help explain why this is economically misguided, I developed a (hopefully) compelling visual based on how to harvest apples.

But I’ve always wondered if I was presenting the information in an accessible and understandable manner. So for today’s presentation, I decided to experiment with some different visuals.

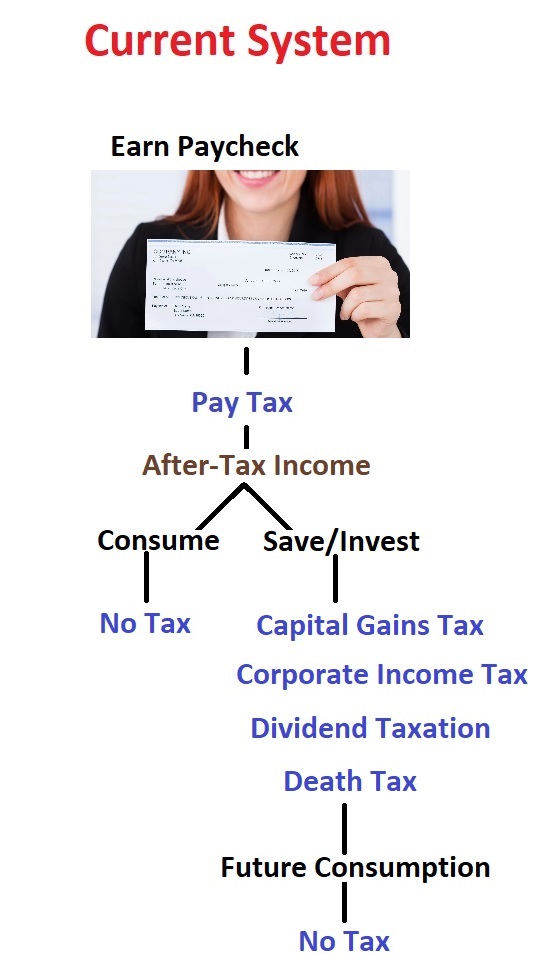

Here’s how I illustrated the current system.

Here’s how I illustrated the current system.

As you can see, there are several additional layers of tax on people who save and invest their after-tax income.

And I explained to the crowd that this is very foolish since every economic theory agrees that saving and investment are key to long-run growth.

Even socialism. Even Marxism. (Socialists and Marxists are foolish to think government can be in charge of allocating capital, but at least they realize that future growth requires saving and investment.)

In other words, you don’t achieve good tax policy solely by having a low tax rate.

Yes, that’

s important, but genuine tax reform also means no bias against saving and investment.

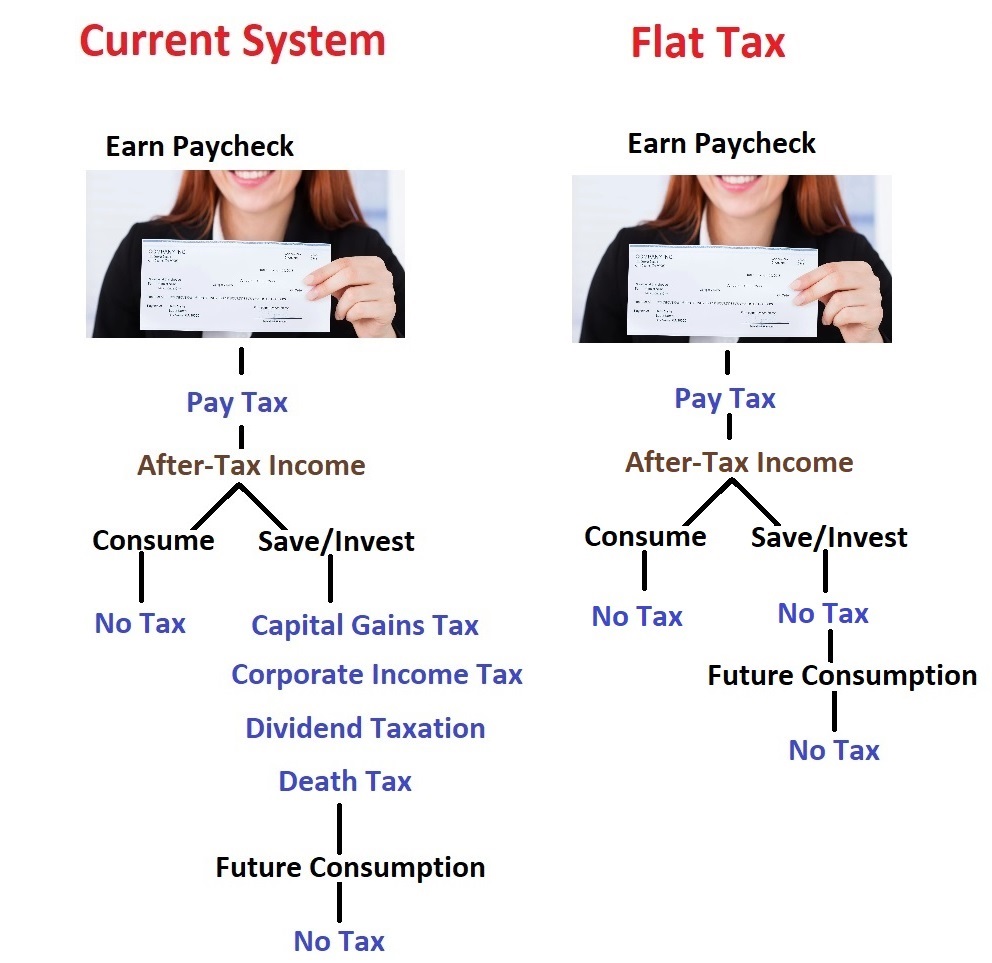

Here’s another visual. This one shows the difference between the current system and the flat tax. As you can see, all the added layers of tax on saving and investment are jettisoned under true tax reform.

By the way, there are some people who prefer a national sales tax over a flat tax.

I question the political viability of that approach, but I’ve always defended the sales tax.

Why? Because it’s conceptually identical to the flat tax.

As you can see from this next visual, the difference between the two systems is that the flat tax grabs a bit of money when income is earned and the sales tax grabs a bit of money when income is spent (either today or in the future).

Remember, the goal is to eliminate the bias against saving and investing.

To economists who specialize in public finance, this is known as shifting to a “consumption base” system.

But I’ve never liked that language. What really happens under true tax reform is that we tax income, but using the right definition.

The current system, by contrast, is known as a “comprehensive income tax” with a “Haig-Simons” tax base. But that simply means a system that taxes some forms of income over and over again.

The current system, by contrast, is known as a “comprehensive income tax” with a “Haig-Simons” tax base. But that simply means a system that taxes some forms of income over and over again.

Time for one final point.

Some people like a value-added tax because it avoids the problem of double taxation.

That’s certainly true.

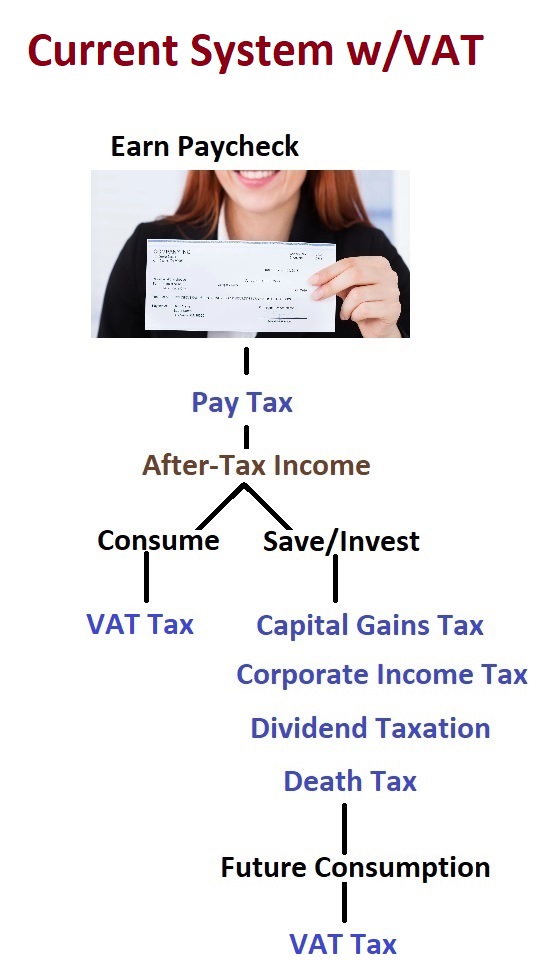

But this final visual shows that adding a VAT to the current system doesn’t solve the problem. All that happens is that politicians have a new source of revenue to expand the welfare state.

If a VAT was used to replace the current tax system, that might be a very worthwhile approach.

But that’s about as likely as me playing the outfield later this year for the New York Yankees.

P.S. The VAT visual is overly simplified and it sidesteps the logistical issue of whether politicians would go for a credit-invoice VAT or a subtraction-method VAT. But the visual is correct in terms of how a VAT would interact with the current system.

P.P.S. All you need to know about the VAT is that Reagan was against it and Nixon was for it.

[…] tax bias against saving and investment is a major problem in the United States and many other […]

[…] And that means understanding the “tax base.” […]

[…] VAT has the same “tax base” as a flat tax. The structural difference is that a flat tax takes a slice of your income as […]

[…] sounds simple and straightforward, but there is a big controversy over the benchmark (or “tax base“) that gets used when measuring […]

Reblogged this on Utopia, you are standing in it!.

[…] The debate on consumption-base taxation vs. Haig-Simons taxation. […]

[…] So a capital gains tax is a version of triple taxation. […]

[…] So a capital gains tax is a version of triple taxation. […]

[…] But the economic benefits of both plans are identical because the core features of both plans are identical. […]

[…] finance theory teaches us that the capital gains tax should not exist. Such a levy exacerbates the bias against saving and investment, which reduces innovation, hinders economic growth, and lowers worker […]

[…] finance theory teaches us that the capital gains tax should not exist. Such a levy exacerbates the bias against saving and investment, which reduces innovation, hinders economic growth, and lowers worker […]

[…] finance theory teaches us that the capital gains tax should not exist. Such a levy exacerbates the bias against saving and investment, which reduces innovation, hinders economic growth, and lowers worker […]

[…] No tax bias against capital (i.e., saving and investment) […]

[…] tax bias against capital (i.e., saving and […]

[…] No tax bias against capital (i.e., saving and investment) […]

[…] tax bias against capital (i.e., saving and […]

[…] a flowchart I prepared showing the double taxation in the current system compared to what happens with a flat […]

[…] debate on consumption-base taxation vs. Haig-Simons […]

[…] interesting topics (Australian politics and policy, the economics of government spending, the structure of taxation) on my recent trip Down […]

Richard:

We will not get away from progressive effective tax rates. I agree that a true flat tax is best but it has zero chance of getting enacted. Seems that you would rather argue for a “no chance of enactment system” rather than substitute a better system for what we have.

Our tax code is a mess. Our “safety-net” is a mess. Politically the argument to tax the poor at the same effective tax rate, in the current environment, is a loser. Would you rather fix the system, or yell at the sky like those liberals when Trump got elected?

Politicians, regardless of which Party they “identify” with or as have horribly polluted every stream of revenue they’ve had access to. No NEW revenue streams for them to pollute until after the others have been constitutionally closed to them.

If they can use it they will abuse it.

nedlandp,,,

You start off wrong and then get stupider…a flat tax does not assume a standard deduction,,, maybe you want to add it on,,, but a basic flat tax starts at the 1st penny… BTW that’s God’s system,,, he doesn’t have any standard deduction before you start tithing!!!

Also UBI in addition to being a disincentive to work, no matter what the amount is, is not Constitutional… the federal government has no business taking from me and giving it to other people just because they are alive…

It’s time to start taxing the poor and stop subsidizing them..

As my friend Bob says,,, if you want more of something just subsidize it..

Since we’re talking about an ideal tax system:

A “Flat Tax” assumes a standard deduction, so it’s not a “Flat Tax” at all, but rather a two tier tax, zero and the flat rate. Filing is simple, but you must file every year.

Contrast that against a “True Flat Tax” (everybody taxed at the flat rate, including someone making $1). Combine that with a UBI, that is distributed separately, the effective rates are the same as above, but no reason to file annually, as withholding will always be accurate.

For example: At a 25% flat tax, a standard deduction of $20,000 and a UBI of $5,000 are the same thing, for those above $20,000 in income.

I prefer a UBI at $10,000 for adults and $2,000 for citizens below 21, so everyone receives “poverty level” support.

That level will eliminate federal welfare and reduce other “safety-net” programs to the point that they become less of a disincentive (unemployment insurance would be reduced to the point where people would start looking for jobs immediately). It’s true that some in the lower middle class might benefit in increased take-home, but the whole system would be fair. The efficiencies of the system would be great enough that those at the top would see increases in their take-home also, as the economy leaps forward.

No citizen would not be covered, there would be no “welfare queens”, and we could reduce the government payroll by about 1 million bureaucrats.

Since the growth in citizens is only 0.9% annually, we would cap “entitlements” at level below GDP growth.

Diminished Social Security and Medicare costs can finally be addressed to deal with the reality of changing demographics.