I’ve been arguing all year that a substantially lower corporate tax rate is the most vital goal of tax reform for reasons of competitiveness.

And I continued to beat that drum in an interview last week with Fox Business.

The Wall Street Journal agrees that the time has come for a lower corporate rate. Unless, of course, one would prefer the United States to fall even further behind other countries.

President Emmanuel Macron last week pushed a budget featuring substantial tax relief through the National Assembly. The top rate on corporate profits will fall to 28% by 2020 from 33.33% today, and Mr. Macron has promised 25% by 2022. …Critics branded Mr. Macron “the President for the rich” for these overhauls, but the main effect will be to stimulate investment and job creation… The Netherlands also is jumping on the bandwagon. Prime Minister Mark Rutte promises to cut the top corporate rate to 21% from 25% by 2021… Do American politicians really want to have to explain to voters why they let the U.S. trail even France?

For the most part, opponents of tax reform in the United States understand that they have lost the competitiveness argument. So they will pay lip service to the notion that a lower corporate rate is desirable (heck, even Obama notionally agreed), but they will fret about the loss of tax revenue and a supposed windfall for the “rich.”

I agree that tax revenues will decrease, at least in the short run. But there’s some very good research showing the long-run revenue-maximizing corporate rate is somewhere between 15 percent and 25 percent.

And Chris Edwards of the Cato Institute reviewed fifty years of data for industrialized nations and ascertained that lower tax rates are associated with rising revenue.

There’s also good evidence from Canada and the United Kingdom if you want country-specific examples of the relationship between corporate tax rates and corporate tax revenue.

By the way, even left-leaning multilateral bureaucracies such as the International Monetary Fund and the Organization for Economic Cooperation and Development have published research showing the same thing.

And what about the debate over whether the “rich” benefit?

That issue is a red herring. Yes, shareholders of companies, on average, have higher incomes, and they will benefit if the rate is reduced, but I’ve never been motivated by animosity against those with more money (assuming they earned their money rather than mooching off the government).

What does get my juices flowing, however, is growth. And if we can get more dynamism in the economy, that translates into more jobs and higher income.

A new report from the Council of Economic Advisers estimates the potential benefit for ordinary people.

Reducing the statutory federal corporate tax rate from 35 to 20 percent would, the analysis below suggests, increase average household income in the United States by, very conservatively, $4,000 annually. …Moreover, the broad range of results in the literature suggest that over a decade, this effect could be much larger.

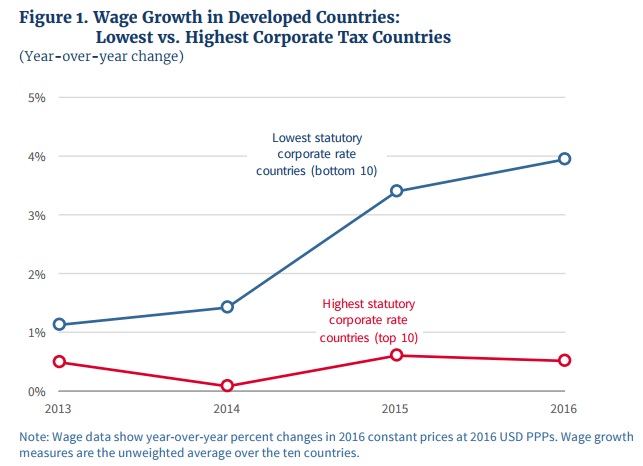

There’s some good cross-country data showing nations with lower corporate tax rates do better.

Between 2012 and 2016, the 10 lowest corporate tax countries of the OECD had corporate tax rates 13.9 percentage points lower than the 10 highest corporate tax countries, about the same scale as the reduction currently under consideration in the U.S. The average wage growth in the low tax countries has been dramatically higher.

Here’s the accompanying chart.

As you can see, there’s a clear divergence between higher-tax and lower-tax nations. Though, given the limited time period in the chart and the fact that many other factors can impact wage growth, I’m actually more persuaded by some of the other empirical research cited in the CEA report.

Arulpalapam et al (2012) find that workers pay nearly 50 percent of the tax, while Desai et al (2007) estimate a worker share of 45 to 75 percent. Gravelle and Smetters (2006) generate a rate of 21 percent when the rate of capital mobility across countries is moderate and 73 percent when capital can flow freely, evidence that the labor incidence is likely both dynamic and positively correlated with the rate of international capital transfers. A Congressional Budget Office (CBO) study (Randolph, 2006) finds that workers bear 70 percent of the corporate income tax burden in the baseline and 59 to 91 percent in alternative specifications. In a summary study, Jensen and Mathur (2011) argue for an assumption of greater than 50 percent. …A cross-country study by Hassett and Mathur (2006) based on 65 countries and 25 years of data finds that the elasticity of worker wages in manufacturing after five years with respect to the highest marginal tax rate in a country is as low as -1.0 in some specifications, although other sets of control variables increase the elasticity to -0.3. Expanded analysis by Felix (2007) follows the Hassett and Mathur strategy, but incorporates additional control variables, including worker education levels. Felix settles on an elasticity of worker wages with respect to corporate income taxes of -0.4, at the high end of the Hassett and Mathur range. …Felix (2009) estimates an elasticity of worker wages with respect to corporate income tax rates based on variation in the marginal tax rate across U.S. states. In this case, the elasticity is substantially lower; a 1 percentage point increase in the top marginal state corporate rate reduces gross wages by 0.14 to 0.36 percent over the entire period (1977-2005) and by up to 0.45 percent for the most recent period in her data (2000-2005). …Desai et al (2007)…measure both the changes in worker wages and changes in capital income associated with corporate income tax changes. The estimated labor burden of the corporate tax rate varies from 45 to 75 percent under various specifications in the paper.

That’s a lot of jargon, so I suspect that many readers will find data from Germany and Australia to be more useful when considering how workers benefit from lower corporate rates.

P.S. While I think a lower corporate tax rate may result in more revenue over time, that’s definitely not my goal.

P.P.S. The biggest obstacle to good tax policy is the unwillingness of Republicans to impose even a modest amount of spending restraint.

[…] will be once again mired at the bottom. And this bad policy will lead to unfortunate results for American workers and American […]

[…] was good for workers since a lower rate means more investment, which translates to increased productivity and higher […]

[…] was good for workers since a lower rate means more investment, which translates to increased productivity and higher […]

[…] will be once again mired at the bottom. And this bad policy will lead to unfortunate results for American workers and American […]

[…] For more information on corporate taxation and wages, click here, here, here, here, and […]

[…] corporate taxes mean a bigger capital stock which means new jobs, higher wages, and more goods and services. That is why Ireland’s low corporate taxes have not just been good […]

[…] corporate taxes mean a bigger capital stock which means new jobs, higher wages, and more goods and services. That is why Ireland’s low corporate taxes have not just been good […]

[…] corporate taxes mean a bigger capital stock which means new jobs, higher wages, and more goods and services. That is why Ireland’s low corporate taxes have not just been good […]

[…] this bad policy will lead to unfortunate results for American workers and American […]

[…] will be once again mired at the bottom. And this bad policy will lead to unfortunate results for American workers and American […]

[…] will be once again mired at the bottom. And this bad policy will lead to unfortunate results for American workers and American […]

[…] a look at how much faster wages have grown in countries with low corporate tax rates compared to nations with high corporate tax […]

[…] a look at how much faster wages have grown in countries with low corporate tax rates compared to nations with high corporate tax […]

[…] a look at how much faster wages have grown in countries with low corporate tax rates compared to nations with high corporate tax […]

[…] bottom line is that it’s not a good idea to raise the corporate tax burden and it’s not a good idea to worsen the payroll tax […]

[…] few years ago, the United States had a much higher burden of double taxation because the corporate tax rate was so high. Indeed, the combined tax rate on dividends was the fourth-highest in the developed […]

[…] happened in 2017. I’ve written many times about why it was a very good idea to reduce the tax rate on corporate income. And I’ve also lauded the 2017 law’s […]

[…] I offered to China. Respond to Americans tax cuts by doing the right thing for your citizens. Boost growth and wages with lower tax […]

[…] is why it is in the best interest of workers to get rid of capital gains taxes, lower the corporate tax rate, eliminate the death tax. The more investment we have, the more productivity goes up, and the more […]

[…] the 21 percent corporate tax rate was the unquestioned crown jewel of the Tax Cut and Jobs Act. The U.S. system had become extremely anti-competitive thanks to a 35 […]

[…] instrumental in moving the ball forward on tax reform. I very much doubt we would have achieved a lower corporate tax rate or scaled back the state and local tax deduction without all the work he did during his time at the […]

[…] the reason this fills me with joy is two-fold. First, we get more growth, more jobs, and higher wages when corporate rates […]

[…] let’s not forget that the tax reform legislation – particularly the lower corporate rate – also will make America more attractive to foreign investors. And that also will lead to a […]

[…] the bad news. The good news is that the Trump tax cuts did produce a lower corporate rate. So in the version below, I’ve added my back-of-the-envelope calculation of where the U.S. […]

[…] now I’m actually somewhat hopeful that we’ll get a lower corporate rate and repeal of the pernicious deduction for state and local income […]

[…] was a big fan of the lower corporate tax rate in last year’s tax bill, largely because I want a better […]

[…] was a big fan of the lower corporate tax rate in last year’s tax bill, largely because I want a better […]

[…] strongly applauded the tax reform plan that was enacted in December, especially the lower corporate tax rate and the limit on the deduction for state and local […]

[…] amount of attention various provisions produced, last year’s fight over tax reform was about reducing the corporate tax rate and limiting the deduction for state and local […]

[…] of the ledger, he pushed for and ultimately signed a better-than-expected tax bill featuring an impressive reduction in the corporate tax rate and some much-needed limits on the deductibility of state and local taxes. On the spending side of […]

[…] tax rate – Dropping the federal corporate tax rate from 35 percent to 21 percent will boost investment, wages, and competitiveness, while also pressuring other nations to drop their corporate rates in a virtuous cycle of tax […]

[…] are several provisions of the tax bill that will boost the economy, most notably dropping the federal corporate tax rate from 35 percent to 21 percent. Slightly lower individual tax rates will also help growth, as will […]

[…] That proposal was not warmly received by his GOP colleagues since the 20-percent corporate rate was perceived as their biggest achievement. […]

[…] A lower corporate tax rate. […]

[…] I offered to China. Respond to Americans tax cuts by doing the right thing for your citizens. Boost growth and wages with lower tax […]

[…] study underscores why that reform will boost investment. And remember, when investment increases, that translates into higher wages for […]

[…] makes me happy since any agreement presumably will include a lower corporate tax rate and the elimination of the deduction for state and local income […]

[…] been saying for months that tax reform will be a worthwhile success if it leads to a significantly lower corporate tax rate and the elimination of the deduction for state and local income […]

[…] I don’t want to lose sight of two very important goals: Lowering the corporate rate and getting rid of the deduction for state and local income taxes (and I’m still fantasizing […]

[…] Lower corporate tax rate. […]

[…] America’s high corporate tax rate is probably the most self-destructive feature of the current system. If the rate is permanently reduced from 35 percent to 20 percent, that will be a huge boost to competitiveness. […]

[…] « Cut the Corporate Tax Rate to Boost Wages and Help Workers […]

and what is a UBI

здесь

купить тренболон энантат Верхотурье

The primary beneficiary of investment tax elimination will be job creating startups. The primary beneficiaries of a corporate tax reduction would be existing companies with revenues.

Note that the “painless tax” is a political expedient. This tax would collect +5x normal investment taxes and would therefore be a huge tax on the rich.

Class warriors will scream bloody-murder, but not as much as if the investment taxes were eliminated without the tax.

While cutting the corporate tax rate is the hot topic, the flip side, elimination of capital gains, dividends, gift, and death taxes is being ignored.

Both can be accomplished, through means of a “painless tax”. If you eliminate the above “investment” taxes the value of securities will jump, creating a windfall. However, the day before this goes into effect, you could have a one-time “painless tax” [a 20% ransom to release investment value] on all accumulated gains. In all cases, the windfall increase would be more than the tax, making it painless. In addition, you could allow the tax to be paid by applying future Social Security benefits. If you also apply this to non-Roth pensions funds, tax collected plus future Social Security reductions would be between $1T-$2T.

The most frequently discussed method of resolving the coming Entitlement crisis is to means-test benefits. While I believe that to be unethical, since promises from government to the people would be reneged, taxing the wealth and applying benefits for payment accomplishes the same thing in an ethical way.

Note that investments would be narrowly defined as investments that stimulate job creation and growth. Short term trading, derivatives, and collectibles would be re-categorized as business income. Real estate would continue to be taxed as current.

Elimination of investment taxes opens the door to a flat tax (with either a large standard deduction, or my preference, a UBI [which repairs the safety-net]) and the elimination of all “tax expenditures”. It also allows for lower corporate and individual tax rates, since the Entitlement burden will have been reduced.

The elimination of “tax expenditures” is another reason for a UBI, since the goal is to shift healthcare and pensions from corporate expenditures to individual accounts. A UBI moves tax benefits from employers to individuals, providing for a fluid 21st century workforce.

While taxes are the hot issue, government spending should be the primary focus, but neither party wants cuts.

Dan:

Congrats on your Georgia Bulldogs! — Love the tie.