The Wall Street Journalopined on a crazy proposal from Biden’s team a few days ago. Here are some excerpts.

Income redistribution is an abiding value of the Biden Administration, and now it wants to spread that to mortgage lending. A new rule will raise mortgage fees for borrowers with good credit to subsidize higher-risk borrowers. Under the rule, which goes into effect May 1, home buyers with a good credit score over 680 will pay about $40 more each month on a $400,000 loan, and upward depending on the size of the loan. Those who make down payments of 20% on their homes will pay the highest fees. Those payments will then be used to subsidize higher-risk borrowers through lower fees. This is the socialization of risk, and it flies against every rational economic model, while encouraging housing market dysfunction and putting taxpayers at risk for higher default rates. …selling people houses they can’t afford has never been a good idea. See the subprime loan collapse of 2008. …the Federal Housing Administration…want[s] to punish those who have maintained good credit while rewarding those who haven’t.

The editors of National Review are similarly disgusted by the Biden Administration’s scheme.

The federal government props up the housing market in too many ways to count. The U.S. is unique among rich countries in having the national government insure mortgages, guarantee mortgage securities, and finance mortgages with government-sponsored enterprises. …When government isn’t getting the results it wanted with all of its previous involvement, it tries a little more intervention to “fix” its previous interventions. To help out homebuyers with poor credit scores, the Federal Housing Finance Agency has decided that homebuyers with good credit scores will pay a little more for their mortgages. …FHFA director Sandra Thompson said the new rules…would “increase pricing support for purchase borrowers limited by income or by wealth.” But income and wealth are and should be limiting factors in lending. It’s not good for borrowers to take on loans that may prove beyond their means to pay back. …this policy reduces the incentive to be responsible…and…has the added twist of penalizing people with high credit scores. …That’s one way to get more poor decisions and fewer good ones.

For all intents and purposes, the Biden Administration wants more redistribution.

P.S. Some of my left-wing friends say the 2008 crisis was caused by “Wall Street greed.” I respond by asking them whether there was greed on Wall Street in the 1980s and 1990s, or at other times. They usually have to admit that greed is always present, so I then tell them greed only becomes a big problem when mixed with upside-down government policies.

It was amusing, of course, but also made a serious point about “moral hazard,” which is what happens when government policy rewards bad behavior.

I’m in favor of risk taking, and I certainly don’t object to people earning lots of income when they make astute choices.

But it sends a terrible signal if we bail them out when they make bad choices.

That approach tells others to go overboard with speculation. After all, heads they win, tails the taxpayers lose (as illustrated by this clever cartoon).

And now we can add union pension plans to the list. Here are some excerpts from an editorial in yesterday’s Wall Street Journal.

Democrats sold their $1.9 trillion spending bill in 2021 as Covid “relief,” but it included some $86 billion to shore up more than 200 ailing union multi-employer pension plans. The $36 billion for the Teamsters’ Central States Pension Fund is the largest tranche awarded so far, but Mr. Biden assured his labor friends on Thursday that more is on the way. …Central States last year was only 17% funded and projected to collapse in a few years. …Congress in 2014 acted to prevent this death spiral by passing bipartisan legislation that let sick plans reduce benefits and make other changes to avoid insolvency. Eighteen plans took advantage of the law, but Democrats then had second thoughts and decided to ding taxpayers instead. …Last year’s union, er, Covid relief bill lets the PBGC make lump sum payments to keep some sick 200 multi-employer plans solvent through 2051 and fully restore benefits in the 18 plans that had cuts. Notably, the law prohibits the PBGC from conditioning aid on governance reforms or funding rules. But it doesn’t forbid benefit increases. So the failings that got these plans in trouble will continue and may lead to future bailouts. Government unions with under-funded pensions in New Jersey and Illinois will surely demand one too.

Back in July, Eric Boehm of Reason warned that this was going to happen and that it would be a very bad idea.

The bailout was approved last year as part of the American Rescue Plan, the $1.9 trillion emergency spending bill…the multiemployer pension plan bailout is arguably the least defensible provision in a bill that was full of indefensible spending. …Reps. Virginia Foxx (R–N.C.) and Rick Allen (R–Ga.), respectively the top Republicans on the Education and Labor Committee and the Health, Employment, Labor, and Pensions Subcommittee, in a joint statement…added, “creates perverse incentives for further mismanagement and underfunding and leaves the taxpayer holding the bag.” …this is something of a no-brainer. Biden delivered a major win to his labor union allies, put the cost on the taxpayers’ tab, and took a victory lap for doing it. …And everyone else gets to pay for it.

That same month, Howard Adler and Alex Pollock made similar points in a column for the Wall Street Journal.

Multiemployer plans often promise beneficiaries more benefits than they can afford. Many are governed by a board of trustees with equal representation from unions and employers—a recipe for increasing benefits but not funding them. …Congress and the Biden administration wrote a blank check to political supporters under the guise of Covid relief. …The most egregious aspect of the bailout is that it made no attempt at structural reform. Plans are free to continue the practices that got them into trouble in the first place. …The PBGC’s new projected insolvency date is 2055, four years after the bailout funds end. The pension scheme is set up for failure—or another bailout—in three decades. Bailouts should be conditioned on reforms. In prior bailout legislation…Congress tried to address the causes of the failures that made a bailout necessary. But with multiemployer pension plans, lawmakers made no attempt to fix anything—they merely spent taxpayer money.

What’s most upsetting about this bailout is not the money that’s being squandered today.

But future spending on additional bailouts is just part of the problem. There’s also a macro cost to the economy because the allocation of capital will be distorted.

Investors will take imprudent risks because there is a greater-than-zero chance (in some cases, probably close to 100 percent) that politicians will shift future losses on to the backs of taxpayers.

Today, here are my thoughts on why there should not be a bailout if/when a crisis occurs.

I have moral objections to bailouts, but let’s focus in this column on the practical impact.

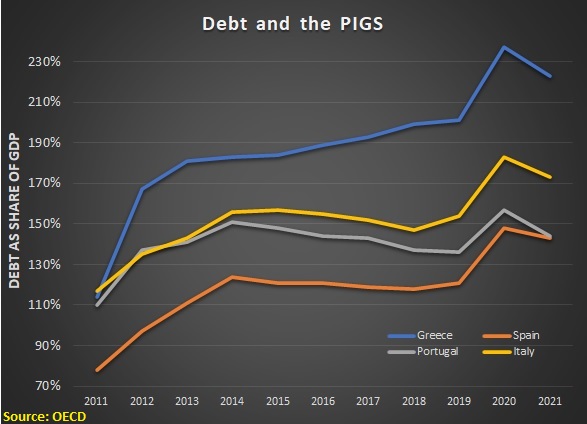

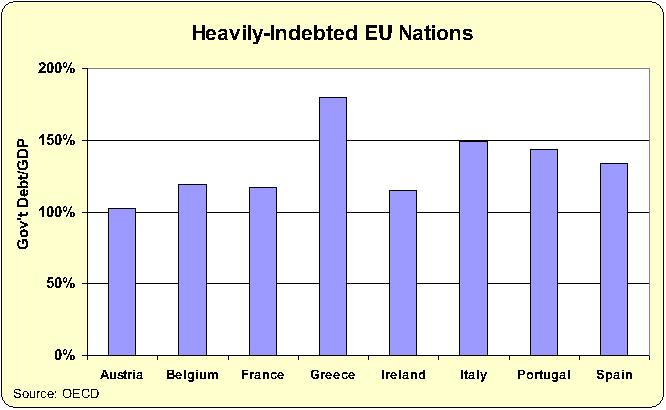

And let’s start with this chart, which shows debt levels in Portugal, Italy, Greece, and Spain (the so-called PIGS) ever since the misguided bailout of Greece about a dozen years ago.

As you can see, OECD data reveals that there’s been no change in these poorly governed nations. They have continued to over-spend and accumulate ever-higher levels of debt.

Defenders of bailouts assert that Greece was forced to engage in “austerity” as a condition of getting a bailout.

I have two problems with that argument.

First, notice how Greece’s debt has continued to go up. If that’s a success, I would hate to see an example of failure.

Second, the main effect of the so-called austerity is a much higher tax burden and a somewhat higher spending burden.

If there’s a bailout of Italy (or any other nation), I suspect we’ll see the same thing happen. Higher taxes, higher spending, and higher debt.

I’ll close by acknowledging that there are costs to my approach. If Italy is not given a bailout, the country may have a “disorderly default,” meaning the government simply stops honoring its commitments to pay bondholders.

That is bad for individual bondholders, but it also could hurt – or even bankrupt – financial institutions that foolishly decided to buy a lot of Italian government bonds.

But there should be consequences for imprudent choices. Especially if the alternative is bailouts that misallocate global capital and encourage further bad behavior.

The bottom line is that the long-run damage of bailouts is much greater than the long-run damage of defaults.

The monetary cost is significant, but I get even more upset that responsible people are forced to finance other people’s irresponsible choices.

It’s such a bad policy that even Bernie Sanders favors reform.

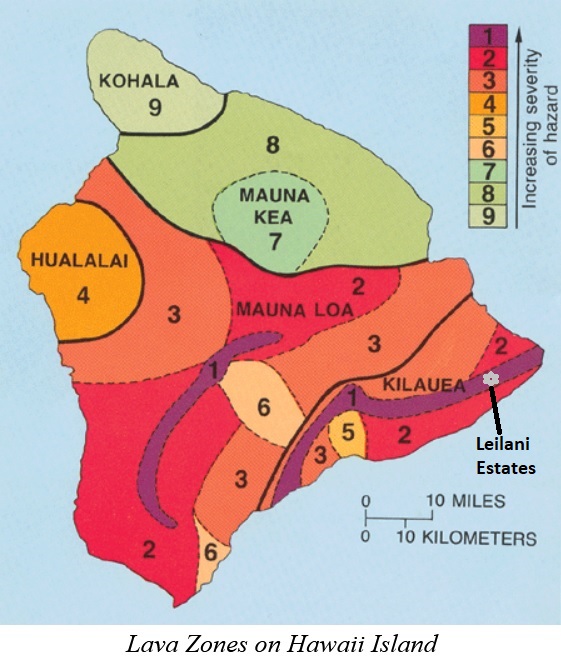

And it’s such a bad policy that politicians in Hawaii decided it is worth copying. But they chose to subsidize building homes that are vulnerable to volcanic eruptions.

I’m not joking. Joe Kent of the Grassroot Institute wrote about this foolish system.

…the state originally encouraged the building of homes in this dangerous area by offering lava insurance where no private company would. …In response to the absence of private insurance, the state Legislature created the Hawaii Property Insurance Association (HPIA), whose job is to provide coverage for homes in areas that private insurance won’t touch. The law requires private insurance companies to pool their money to subsidize the expense of offering insurance in high-risk lava zones. …This resulted in a boom in the housing market below the active Kilauea volcano. …The moral hazard of this new insurance program gave a false sense of security to homebuilders in Leilani Estates.

Given my libertarian sympathies, I think people should have the right to build in dangerous areas.

But I also think that they should bear the risks. Including what happened a few years ago.

…that hazard is very real for families watching their homes be engulfed by magma. What was seen as a “market failure” was really a warning sign to those building in Lava Zones 1 and 2. If the state had stayed out of the situation, probably fewer families would have built in the area, and today there might be less housing destruction.

Why is this unfortunate? Because there are some policy changes that may be costly in the short run, but they are nonetheless very worthwhile because they generate big long-run benefits.

Messy fights over the debt limit create (almost certainly exaggerated) concerns about potential default, but that potential cost would be trivial compared to the long-run benefits of figuring out how to limit the growing burden of federal spending.

I offer the above examples because similar short-run and long-run tradeoffs exist when looking at what happens when the International Monetary Fund provides bailouts for profligate governments.

The Economist has an article that perfectly illustrates the IMF’s pernicious role.

The year was 1958. …Argentina turned to the fund for its first “standby arrangement”, a line of credit accompanied by a plan to stabilise the economy. …Sixty years later, in June 2018, Argentina was back for its 21st arrangement: a $50bn loan, later increased to $57bn, backed by the government’s promises to cut the budget deficit and strengthen the central bank in the hope of quelling inflation and stabilising the peso. The loan was the largest in the imf’s history. …Despite its size, the rescue failed to save Argentina from default and despair. …Foreign capital kept retreating, the peso kept falling and inflation kept rising. The evaluation speculates that the size of the imf’s loan may even have been “self-defeating”, eroding confidence rather than inspiring it.

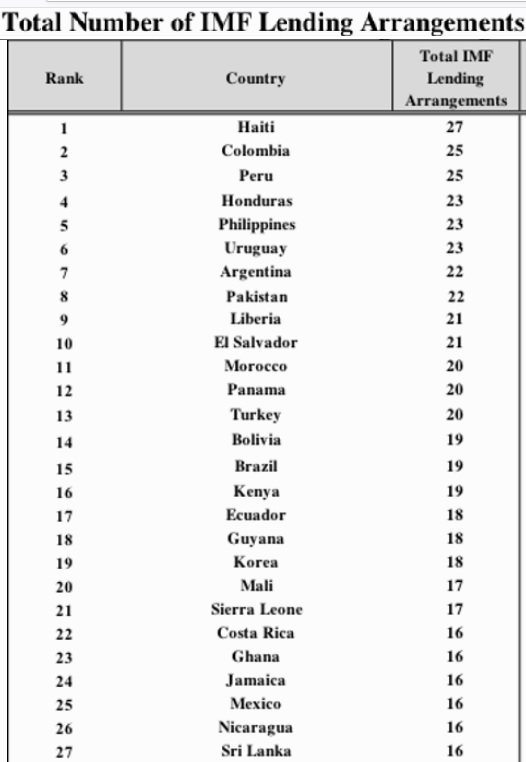

Just in case you missed it, the article mentions that Argentina has received 21 different bailouts since 1958, which works out to be one bailout every three years (Professor Steve Hanke counts 22 bailouts, for what it’s worth).

In probably every case, IMF bureaucrats presumably thought a bailout was a way of minimizing economic pain (and they probably thought the same thing for dozens of bailouts provided to Haiti, Colombia, Peru, Honduras, Philippines, etc).

But what actually has happened is that politicians – in Argentina and elsewhere – have learned that it’s okay to pursue bad policy because there’s always another bailout.

In other words, IMF policy is a glaring example of “moral hazard.” By shielding politicians from the consequences of bad policy, the bureaucracy is actually encouraging those politicians to engage in additional bad policy.

To be blunt, the IMF is the arsonist rather than the firefighter.

The article in the Economist included this observation.

Conservative critics think the fund has been seduced by its dance partner, wasting public money in a futile battle.

My right-leaning friends are correct, but their criticisms are too mild.

It’s not just that the IMF is wasting money. It’s dampening growth by pushing policies that misallocate capital.

Here’s what should have happened to Argentina in 1958 (and what should have happened in 2018, and what should happen when there’s pressure for yet another bailout).

The politicians in Argentina who spend excessively should learn that there’s a tipping point when they can no longer borrow.

The interest groups in Argentina should learn that parasites also suffer when they kill their host animal by being too greedy.

The voters in Argentina should learn that there are serious adverse consequences when you elect “Peronist” politicians.

Sadly, none of these lessons get learned so long as the IMF is standing by to provide never-ending bailouts.

So instead of some short-run pain, which is then offset by better long-run policy, we get bailouts that mask short-run pain and encourage more long-run damage.

P.P.S. To be fair, the IMF recommends tax increases even in the years when bailouts aren’t needed, so at least the bureaucrats have a consistent (albeit nutty) message.

But the biggest problem with the IMF is that it promotes “moral hazard.” More specifically, it provides bailouts for irresponsible governments and for those who foolishly lend to those governments.

All of which explains why some nations (and their foolish lenders) have received dozens of bailouts.

Oh, and let’s not forget that these endless bailouts also lead to a misallocation of capital, thus reducing global growth.

In an article for the New York Times, Patricia Cohen reports on discussions to expand the IMF’s powers.

Once narrowly viewed as a financial watchdog and a first responder to countries in financial crises, the I.M.F. has more recently helped manage two of the biggest risks to the worldwide economy: the extreme inequality and climate change. …long-held beliefs like the single-minded focus on how much an economy grows, without regard to problems like inequality and environmental damage, are widely considered outdated. And the preferred cocktail for helping debt-ridden nations that was popular in the 1990s and early 2000s — austerity, privatization of government services and deregulation — has lost favor in many circles as punitive and often counterproductive.

There’s a lot to dislike about the above excerpts.

Looking at the text, the part about “extreme inequality” is nonsensical, both because the IMF hasn’t done anything to “manage” the issue, other than to advocate for class-warfare taxes.

Moreover, there’s no support for the empty assertion that inequality is a “risk” to the world economy (sensible people point out that the real problem is poverty, not inequality).

Ms. Cohen also asserts that the “preferred cocktail” of pro-market policies (known as the Washington Consensus) has “lost favor,” which certainly is accurate.

But she offers another empty – and inaccurate – assertion by writing that it was “counterproductive.”

Here are some additional excerpts.

The debate about the role of the I.M.F. was bubbling before the appointment of Ms. Georgieva… But she has embraced an expanded role for the agency. …she stepped up her predecessors’ attention to the widening inequality and made climate change a priority, calling for an end to all fossil fuel subsidies, for a tax on carbon and for significant investment in green technology. …Sustainable debt replaced austerity as the catchword. …The I.M.F. opposed the hard line taken by some Wall Street creditors in 2020 toward Argentina, emphasizing instead the need to protect “society’s most vulnerable” and to forgive debt that exceeds a country’s ability to repay.

The last thing the world needs is “an expanded role” for the IMF.

It’s especially troubling to read that the bureaucrats want dodgy governments to have more leeway to spend money(that’s the real meaning of “sustainable debt”).

And if the folks at the IMF are actually concerned about “society’s most vulnerable” in poorly run nations such as Argentina, they would be demanding that the country copy the very successfulpoverty-reducingpolicies in neighboring Chile.

Needless to say, that’s not what’s happening.

The article does acknowledge that not everyone is happy with the IMF’s statist agenda.

Some stakeholders…object to what’s perceived as a progressive tilt. …Ms. Georgieva’s activist climate agenda has…run afoul of Republicans in Congress… So has her advocacy for a minimum global corporate tax.

It would be nice, though, if Ms. Cohen had made the article more balanced by quoting some of the critics.

The bottom line, as I wrote last year, is that the world would be better off if the IMF was eliminated.

P.S. The political leadership of the IMF is hopelessly bad, as is the bureaucracy’s policy agenda. That being said, there are many good economists who work at the IMF and they often produce high-quality research (see here, here, here, here, here, here, here, here, here, and here). Sadly, their sensible analyses doesn’t seem to have any impact on the decisions of the organization’s top bureaucrats.

Unless my memory is more faulty than usual, I don’t think I’ve written a single favorable article about any of Joe Biden’s policies. Which isn’t a surprise considering his knee-jerk embrace of higher taxes and bigger government.

But it’s now time to praise the President.

Why?

Because his administration is taking some long-overdue steps to reduce the damaging impact of federal flood insurance.

Darryl Fears and Lori Rozsa explain what’s happening in an article for the Washington Post.

…8 million Americans…moved to counties along the U.S. coast between 2000 and 2017, lured by the sun, the sea and heavily subsidized government flood insurance that made the cost of protecting their homes much less expensive, despite the risk of living in a flood zone near a vast body of water. …the Federal Emergency Management Agency willincorporate climate risk into the cost of flood insurance for the first time, dramatically increasing the price for some new home buyers. Next April, most current policyholders will see their premiums go up and continue to rise by 18 percent per year for the next 20 years. …wealthy customers with high-value homes will see their costs skyrocket by as much as $14,400 for one year. About 3,200 property owners — mostly in Florida, Texas, New Jersey and New York — fall in that category. …Homeowners in inland states such as Iowa, Missouri and Nebraska, where creeks, streams and rivers overflow during heavy rains, will also see price increases in their government-backed flood insurance. …“It is now going to say if you’re in a risky place, you’re going to get charged more for it, and other people aren’t footing the bill,” VinZant said. …As of last year, the National Flood Insurance Program (NFIP) run by FEMA was $20 billion in debt from massive payouts to customers.

And here’s some of what the Wall Street Journal reported, in an article by Arian Campo-Flores.

Chris Dailey and his wife are building a new home in coastal St. Petersburg, Fla., that will sit 7 feet above the flood level expected during a major storm. So he was stunned to learn that under the federal flood insurance program’s revamped pricing, his annual premium is slated to soar to $4,986 from $441. …he plans to go through with the project, which is about a block and a half from a canal that leads to Tampa Bay, but worries about the ability to sell it in the future. The National Flood Insurance Program—the main provider of flood coverage in the U.S., with more than five million policies—is rolling out an overhauled pricing method starting Friday in an effort to reflect more accurately the flood risk that individual properties face. …Under the new system, dubbed “Risk Rating 2.0,” some policyholders in especially vulnerable areas will face big premium increases while others in less-exposed spots will see smaller increases or even decreases. …Developers may rethink where they build, and coastal real-estate markets could take a hit. “There is no greater risk-communication tool than a pricing signal,” said Roy Wright, president of the Insurance Institute for Business and Home Safety… Some members of Congress, mainly from coastal states, are urging a delay in implementing the new rating system. Senators including Chuck Schumer (D., N.Y.) and John Kennedy (R., La.) wrote a letter last week to the FEMA administrator expressing concern about sharp premium increases.

The most important sentence in the above excerpt was Roy Wright’s observation about the role of prices.

In a free market, by contrast, prices force people to internalize costs and benefits.

Indeed, in an article for Reason, Ronald Bailey points out that private insurers use prices to – gasp – reflect actual risk.

“Insurers cherry-pick homes, leave flooded ones for the Feds,” runs a very odd headline over at E&E News. The article goes on to explain, “Taxpayers could be forced to spend billions of dollars to bail out the federal government’s flood program as private-sector insurers begin covering homes with little risk of flooding while clustering peril-prone properties in the indebted public program.” Well, yes. …The E&E News article strangely claims that “an increased number of people with flood coverage could help reduce flood damage by making homeowners more aware of their risk.” Of course that’s right, but not being able to purchase any flood insurance at all would be a much more effective and compelling way to make homeowners aware of their risks. …Instead of decrying private insurers for sensibly refusing to cover houses located in high-risk flood zones, the E&E News article should instead have been arguing for ending the government’s National Flood Insurance Program altogether.

Let’s close by looking at how Canada handles this issue.

In a 2019 article for the New York Times, Christopher Flavelle explains that Canada recognized years ago that it doesn’t make sense to subsidize homeowners who make risky decisions.

Unlike the United States, which will repeatedly help pay for people to rebuild in place, Canada has responded to the escalating costs…by limiting aid after disasters, and even telling people to leave their homes. …In 2015, Canada made it harder for lower levels of government to get federal money after disasters. The next year, British Columbia said flood victims who had chosen not to buy private flood insurance would be ineligible for government aid. This year the federal government went further still, warning that homeowners nationwide would eventually be on their own. If people deliberately rebuild in danger zones, at some point “they are going to have to assume their own responsibility for the cost burden,” Public Security Minister Ralph Goodale told reporters in April. “You can’t repeatedly go back to the taxpayer and say, ‘Oh, it happened again.’” …Quebec also limited disaster aid, and not just inside the special zone. After this spring’s flooding, the province said it would set an upper threshold for assistance at $100,000 over the lifetime of the house. After that, homeowners face a choice: They can sell to the government, which will pay no more than $250,000, regardless of market value. Or they can get money to rebuild one last time — but in doing so, they forfeit any future financial assistance.

Two cheers for the Canadians. They’ve been more rational than policy makers in the United States (the ones at FEMA, at least in the past, have been especially incompetent).

But not three cheers. In a column for the Wall Street Journal, Professor Walter Block explains how our neighbors to the north are still imperfect.

The best policy is…laissez-faire capitalism. Treat people as adults—allow them to take whatever flooding risks they choose, but on their own nickel. They should be free to build wherever they want, and to indemnify themselves against risk by buying insurance on the open market. But they should not receive a dime of taxpayers’ money for rebuilding.

Which, of course, is exactly what happened with the coronavirus.

As is so often the case, Washington responded in an imprudent manner. As part of multi-trillion dollar emergency legislation (the CARES Act), Congress directly funneled hundreds of billions of dollars to state and local governments.

That legislation also gave the nation’s central bank, the Federal Reserve, the authority to steer money to those same governments.

Notwithstanding all this generosity, state and local politicians are now asking for even more money. In part, this is a fight over the provisions of a potential new “stimulus” bill from Congress.

But it’s also a battle over the fate of the Federal Reserve’s ability to interfere with the allocation of capital by directing money to state and local governments.

In a report for the New York Times, Jeanna Smialek and Alan Rappeport explain what’s happening.

A political fight is brewing over whether to extend critical programs that the Federal Reserve rolled out to help keep credit flowing to…municipalities amid the pandemic-induced recession. …Those programs expire on Dec. 31, and it is unclear whether the Trump administration will agree to extend them. The Federal Reserve chair, Jerome H. Powell, and Treasury secretary, Steven Mnuchin, must together decide whether they will continue the programs — including one that buys state and local bonds, another purchasing corporate debt and another that makes loans to small and medium-size businesses. …Mnuchin…has signaled that he would favor ending the one that buys municipal bonds. And he is under growing pressure from Republicans to allow all five of the Treasury-backed programs to sunset. …The financial terms for buying state and local debt…are not generous enough to compete in a market functioning well… Their main purpose has been to reassure investors that the central bank is there as a last-ditch option if conditions worsen.

However, economic conditions have dramatically improved since the coronavirus first hit, so there’s no longer any argument that financial markets are dealing with crisis conditions.

But that doesn’t seem to matter to politicians who want to subsidize bad fiscal policy at the state and local level.

Some Democrats had begun eyeing the municipal program as a backup option in the event that state and local government relief proved hard to pass through Congress. While the program’s terms are unattractive now, they could in theory be sweetened under a Biden administration Treasury Department. …If a coronavirus vaccine is rolled out in the coming weeks, the Treasury Department may be less inclined to extend the programs. Mr. Trump could also block a reauthorization by pressuring Mr. Mnuchin, leaving Mr. Biden with fewer economic stimulus tools at his disposal. …state and local governments are facing budget shortfalls, albeit smaller ones than some had initially projected.

Nick Timiraos reports on the issue for the Wall Street Journal.

Divisions over their future are being amplified by partisan gridlock in Congress over whether to provide more economic stimulus. Democrats, looking ahead to President-elect Joe Biden’s inauguration in January, see the programs as a potential tool to deliver more aid if Congress doesn’t act, while some Republicans are worried about relying on central bank lending powers as a substitute for congressional spending decisions. …A decision not to renew the programs…could also deprive some…governments of access to low-cost credit if market conditions worsen. …If the Trump administration decides not to extend the programs, Mr. Biden’s Treasury Department could determine whether to reactivate them in some fashion after the new administration takes office Jan. 20.

The bottom line is that a Biden Administration likely will be able to give states and localities a bailout, even if Congress doesn’t approve a new “stimulus,” and even if the Trump Administration doesn’t extend the Federal Reserve’s authority. But at least the incoming Biden people would have to jump through a few hoops.

Which is very unfortunate since it will reward the jurisdictions that behaved recklessly. A classic example of “moral hazard.”

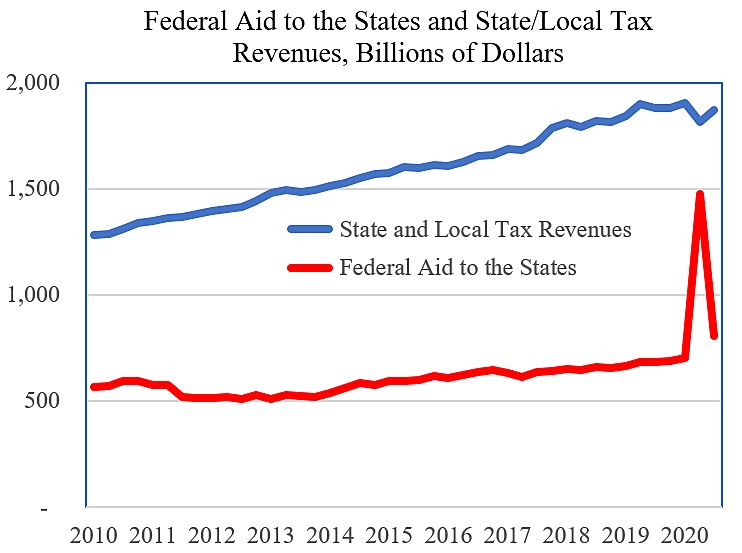

I’ll close with this critical bit of data from Chris Edwards. As you can see, state and local governments actually have profited from the coronavirus since they got far more money from the CARES Act than they lost because of diminished tax revenue.

P.S. For what it’s worth, the Federal Reserve has always had the ability to steer money to state and local governments, both as part of normal monetary policy operation and because of its vast emergency powers. The good news is that it has not gone down that path.

And the best way to make sure it doesn’t go down that path in the future is to eliminate or restrict such powers. Private markets, which reflect the preferences of consumers, should determine the allocation of capital. We don’t want to copy the mistakes of China and have government making those choices.

But the silver lining to that dark cloud is that Fannie and Freddie were placed in “conservatorship,” which basically has curtailed their actions over the past 10 years.

Indeed, some people even hoped that the Trump Administration would take advantage of their weakened status to unwind Fannie and Freddie and allow the free market to determine the future of housing finance.

Those hopes have been dashed.

Cronyists in the Treasury Department unveiled a plan earlier this year that will resuscitate Fannie and Freddie and recreate the bad incentives that led to the mess last decade.

This proposal may be even further to the left than proposals from the Obama Administration. And, as Peter Wallison and Edward Pinto of the American Enterprise Institute explained in the Wall Street Journal earlier this year, this won’t end well.

…the president’s Memorandum on Housing Finance Reform…is a major disappointment. It will keep taxpayers on the hook for more than $7 trillion in mortgage debt. And it is likely to induce another housing-market bust, for which President Trump will take the blame.The memo directs the Treasury to produce a government housing-finance system that roughly replicates what existed before 2008: government backing for the obligations of the government-sponsored enterprises Fannie Mae and Freddie Mac , and affordable-housing mandates requiring the GSEs to encourage and engage in risky mortgage lending. …Most of the U.S. economy is open to the innovation and competition of the private sector. Yet for no discernible reason, the housing market—one-sixth of the U.S. economy—is and has been controlled by the government to a far greater extent than in any other developed country. …The resulting policies produced a highly volatile U.S. housing market, subject to enormous booms and busts. Its culmination was the 2008 financial crisis, in which a massive housing-price boom—driven by the credit leverage associated with low down payments—led to millions of mortgage defaults when housing prices regressed to the long-term mean.

Wallison also authored an article that was published this past week by National Review.

He warns again that the Trump Administration is making a grave mistake by choosing government over free enterprise.

Treasury’s plan for releasing Fannie Mae and Freddie Mac from their conservatorships is missing only one thing: a good reason for doing it. The dangers the two companies will create for the U.S. economy will far outweigh whatever benefits Treasury sees. Under the plan, Fannie and Freddie will be fully recapitalized… The Treasury says the purpose of their recapitalization is to protect the taxpayers in the event that the two firms fail again. But that makes little sense. The taxpayers would not have to be protected if the companies were adequately capitalized and operated without government backing. Indeed, it should have been clear by now that government backing for private profit-seeking firms is a clear and present danger to the stability of the U.S. financial system. Government support enables companies to raise virtually unlimited debt while taking financial risks that the market would routinely deny to firms that operate without it. …their government support will allow them to earn significant profits in a different way — by taking on the risks of subprime and other high-cost mortgage loans. That business would make effective use of their government backing and — at least for a while — earn the profits that their shareholders will demand. …This is an open invitation to create another financial crisis. If we learned anything from the 2008 mortgage market collapse, it is that once a government-backed entity begins to accept mortgages with low down payments and high debt-to-income ratios, the entire market begins to shift in that direction. …why is the Treasury proposing this plan? There is no obvious need for a government-backed profit-making firm in today’s housing finance market. FHA could assume the important role of helping low- and moderate-income families buy their first home. …Why this hasn’t already happened in a conservative administration remains an enduring mystery.

I’ll conclude by sharing some academic research that debunks the notion that housing would suffer in the absence of Fannie and Freddie.

A working paper by two economists at the Federal Reserve finds that Fannie and Freddie have not increased homeownership.

The U.S. government guarantees a majority of mortgages, which is often justified as a means to promote homeownership. In this paper, we estimate the effect by using a difference-in-differences design, with detailed property-level data, that exploits changes of the conforming loan limits (CLLs) along county borders. We find a sizable effect of CLLs on government guarantees but no robust effect on homeownership. Thus, government guarantees could be considerably reduced,with very modest effects on the homeownership rate. Our finding is particularly relevant for recent housing finance reform plans that propose to gradually reduce the government’s involvement in the mortgage market by reducing the CLLs.

For those who care about the wonky details, here’s the most relevant set of charts, which led the Fed economists to conclude that, “There appears to be no positive effect of the CLL increases in 2008 and no negative effect of the CLL reductions in 2011.”

And let’s not forget that other academic research has shown that government favoritism for the housing sector harms overall economic growth by diverting capital from business investment.

The bottom line is that Fannie and Freddie are cronyist institutions that hurt the economy and create financial instability, while providing no benefit except to a handful of insiders.

There are many reasons to oppose the various bailouts of the Greek government. Here are my two main reasons.

I don’t like rewarding investors who make imprudent decisions, and it really galls me to bail out the (mostly) rich people who bought Greek bonds.

I don’t like rewarding politicians who make imprudent decisions, and it really galls me since bailouts encourage additional imprudent behavior.

Let’s focus today on the second point.

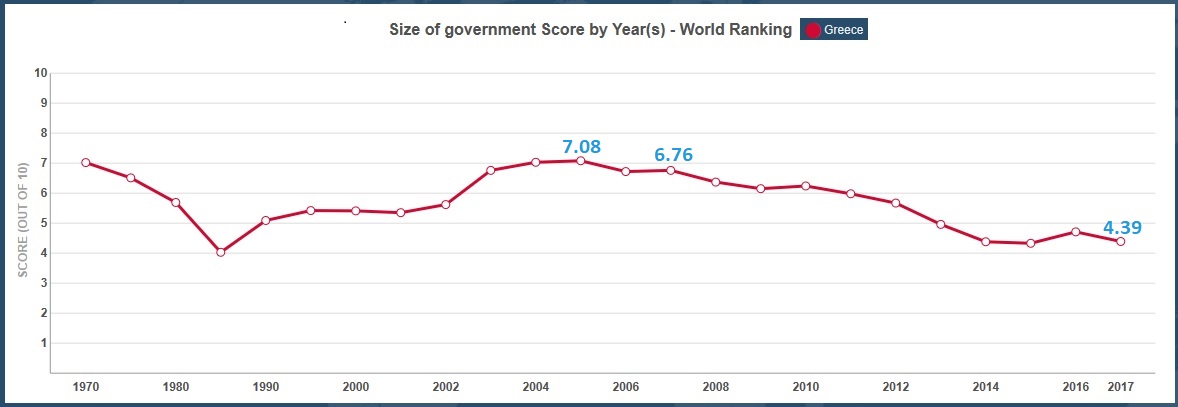

Here’s Greece’s score for the “Size of Government” component from Economic Freedom of the World. As you can see, bailouts have actually subsidized a decline in fiscal responsibility.

And it’s worth pointing out that Greek politicians have been doing a bad job in other areas.

The burden of red tape has been, and remains, stifling.

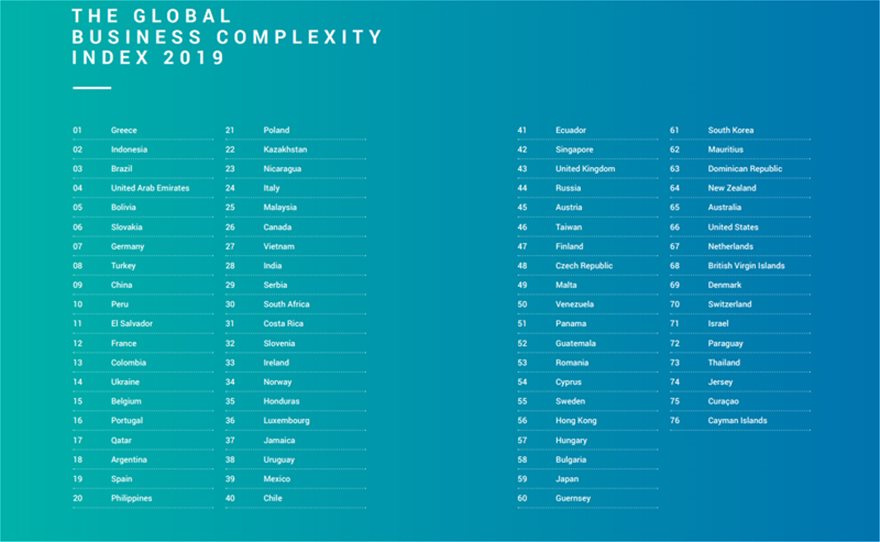

Greece ranks at the top in difficulty in setting up and running a business among 75 countries, according to the Global Business Complexity Index for 2019. The difficulty in starting an enterprise in Greece is mainly due to a labyrinth bureaucracy, frequent changes in legislation, differences in taxation and VAT rates in regions and unpredictable treatment of businesses by authorities. Indonesia, Brazil, the United Arab Emirates, Bolivia, and Slovakia follow Greece in the first six places. The easiest state to start and run a business is in the Cayman Islands.

Here are the rankings. Keep in mind that “01” is the worst score and “76” is the best score (kudos to the Cayman Islands for being the most entrepreneur-friendly).

Interestingly, voters ousted a left-wing government earlier this year.

And Bloomberg reports that Greece’s new right-of-center government intends to reduce the burden of government.

Mitsotakis presented his four-year economic agenda in his first plenary speech to parliament since winning national elections on July 7. …The premier’s priority is a reform of Greece’s complex tax system to create a more pro-business environment, necessary for attracting investment to boost the economy’s recovery. Mitsotakis wants to make good on election pledges to alleviate the tax burden for crisis-weary Greeks, specifically for the middle classes who were targeted the most by the previous administration. …Mitsotakis said he will introduce legislation…to reduce the so-called Enfia property tax by as much as 30%, according to the value of properties. …The government plans to reduce the corporate tax rate to 20% in two phases. The first step, in September, will cut the rate to 24% from 28% in 2019 and to 20% in 2020. The tax on dividend payments will be slashed by half to 5%… Also planned is the privatization of Hellenic Petroleum SA and the sale of a 30% stake in Athens Airport.

Indeed, a columnist for the New York Timesfrets that the new government is hard right.

New Democracy…seems to be a right-wing party… And Mr. Mitsotakis, who promised to unite the country, is following divisive and polarizing policies. …You don’t have to search far for evidence. …Three crucial regulatory agencies — protecting the country’s finances, work force and environment — have been effectively dissolved as part of a bill, recently passed by Parliament, to restructure government. …Domna Michailidou, the vice minister of labor, personifies the cabinet’s ideological agenda. In 2017, she openly praised cuts in wages as “necessary” for the sake of competitiveness. …Greece finished its third and last bailout program last August, but remains shellshocked after nearly a decade of austerity. Official unemployment is at 18 percent; youth unemployment scores a staggering 40 percent. …None of New Democracy’s vaunted policies — to cut corporation taxes and privatize industry in an effort to stimulate economic growth and create “new jobs” — are likely to address the country’s problems. They may well do the opposite.

Some of this sounds good, but I’ll have to see concrete results before I become a believer.

Most supposed right-of-center governments are either very inconsistent (think Trump) or generally bad (think Macri or Sarkozy).

I just focus on results.

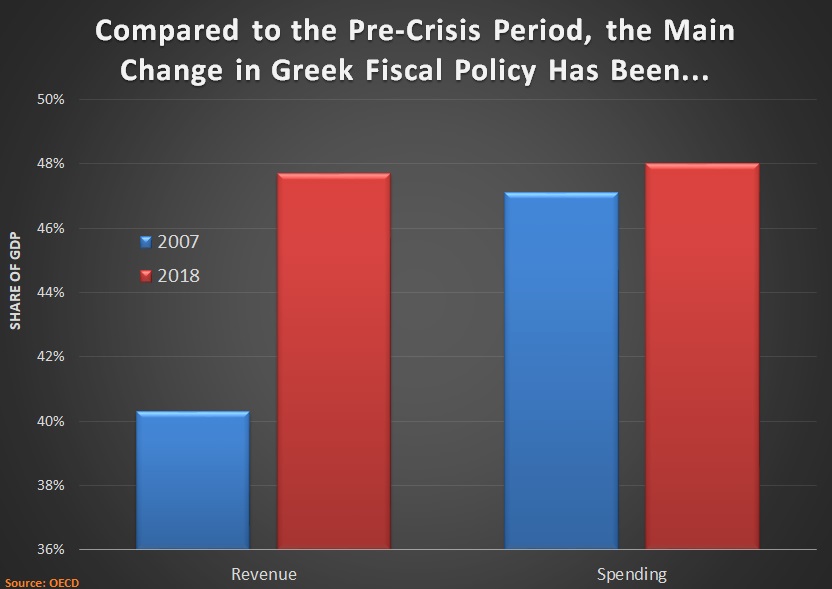

Speaking of which this chart, based on the OECD’s fiscal database, shows what happened to revenue (left side) and spending (right side) between 2007 and 2018.

As you can see on the right side, the burden of spending has actually increased. That’s not my idea of austerity.

The big change that stands out over the past 10 years, though, is that the burden of taxation has jumped. A lot.

In other words taxpayers have been forced to tighten their belts but politicians haven’t tightened government’s belt.

The moral of the story is that tax increases always make a bad fiscal situation worse. Greece has proved that over and over and over again.

Shocking, but true. The Vermont socialist actually understands that it makes no sense to subsidize new homes in flood-prone areas.

"If people want to rebuild in an area which will be devastated by the next storm, they're certainly not going to get federal assistance from my administration." -Sen. Sanders on changing FEMA rules to spur a retreat from properties suffering repeated losses. #ClimateTownHallpic.twitter.com/BC47QBZupm

I’ll probably never again have a chance to write this next sentence, so it deserves an exclamation point. Bernie is completely correct!

Flood insurance encourages people to take on excessive risk (i.e., it creates moral hazard). And the subsidies often benefit rich people with beachfront homes (which may explain why Senator Sanders is on the right side)

If nothing else, politicians are very clever about doing the wrong thing in multiple ways.

So we’re not merely talking about luring people into flood-prone areas with subsidized insurance.

Sometimes government uses rental subsidies to put people in flood-prone areas.

Here are some excerpts from a story in the New York Times.

When a deadly rainstorm unloaded on Houston in 2016, Sharobin White’s apartment complex flooded in up to six feet of water. She sent her toddler and 6-year-old to safety on an air mattress, but her family lost nearly everything, including their car. When Hurricane Harvey hit the next year, it happened all over again: Families rushed to evacuate, and Ms. White’s car, a used Chevrolet she bought after the last flood, was destroyed. …But Ms. White and many of her neighbors cannot afford to leave. They are among hundreds of thousands of Americans — from New York to Miami to Phoenix — who live in government-subsidized housing that is at serious risk of flooding… But the Department of Housing and Urban Development, which oversees some of the at-risk properties, does not currently have a universal policy against paying for housing in a designated flood zone. …Nationwide, about 450,000 government-subsidized households — about 8 to 9 percent — are in flood plains…

While FEMA and government-subsidized flood insurance wouldn’t even exist in my libertarian fantasy world, I’m willing to acknowledge that government sometimes does things that aren’t completely foolish.

For instances, it’s better to subsidize people to move out of flood-prone areas instead of subsidizing them to rebuild in those areas.

Nashville is trying to move people…away from flood-prone areas. The voluntary program uses a combination of federal, state and local funds to offer market value for their homes. If the owners accept the offer, they move out, the city razes the house and prohibits future development. The acquired land becomes an absorbent creekside buffer, much of it serving as parks with playgrounds and walking paths. …While a number of cities around the country have similar relocation projects to address increased flooding, disaster mitigation experts consider Nashville’s a model that other communities would be wise to learn from: The United States spends far more on helping people rebuild after disasters than preventing problems. …research shows that a dollar spent on mitigation before a disaster strikes results in at least six dollars in savings. There are many reasons more people end up rebuilding in place than moving away. Reimbursement is relatively quick, while FEMA’s buyout programs tend to be slow and difficult to navigate.

While it’s encouraging to see a better approach, we wouldn’t need to worry about the issue if government got out of the business of subsidizing flood insurance.

Which helps to explain why the Wall Street Journalexpressed disappointment last year when Republicans blew a golden opportunity to fix the program.

One disappointment you can count on is a GOP failure to fix one of the worst programs in government: taxpayer subsidized flood insurance. …The Federal Emergency Management Agency’s flood insurance program was set to expire on Nov. 30, and Congress rammed through a temporary extension to buy more time. Congress was supposed to deal with the program as part of the end-of-the-year rush. The program runs a $1.4 billion annual deficit, which comes from insurance priced too low to compensate for the risk of building homes near water. Congress last year forgave $16 billion of the program’s $24 billion debt to Treasury, not that anyone learned anything. The program then borrowed another $6 billion. …If Republicans can’t fix this example of failed government because it might upset parochial interests, they deserve some time in the political wilderness.

In other words, Bernie Sanders is better on this issue than last year’s GOP Congress.

I’ve criticized Republicans on many occasions, but this must rank as the most damning comparison.

But let’s set aside politics and partisanship.

What matters is that the federal government is operating an insanely foolish program that puts people at risk, soaks taxpayers, and destroys wealth.

But that’s not what worries me most about the IMF.

To be sure, higher fiscal burdens undermine economic vitality, and I regularly warn that such policies will reduce an economy’s potential long-run growth rate.

That being said, tax increases generally don’t threaten macroeconomic stability.

If we’re looking at policies that can trigger short-run crises, I’m more concerned about the IMF’s bailout policies. For all intents and purposes, the IMF subsidizes “moral hazard” by reducing the perceived cost (to financial institutions) of lending money to dodgy governments and reducing the perceived costs (to governments) of incurring more debt.

Why not take more risk, after all, if you think the IMF will step in to socialize any losses? In other words, when the IMF engages in a few bailouts today, it increases the likelihood of more bailouts in the future.

That’s the bad news. The worse news is that the bureaucrats want a bigger figurative checkbook to enable even bigger future bailouts.

The good news is that the U.S. government can say no.

But will it? The U.K.-based FinancialTimes reported a few days ago that the United States might support an expansion of the IMF’s bailout capacity.

The Trump administration has left the door open for a US funding boost to the IMF, calling for a “careful evaluation” of the global lender’s finances to make sure it has enough money to rescue struggling economies. …The IMF — led by Christine Lagarde, a former French finance minister — is hoping to get its members to increase the fund’s permanent reserves… This year, the Trump administration has been among the most enthusiastic supporters of the IMF’s $57bn loan package to Argentina— its largest in history.

The IMF is set to embark on a major fundraising drive…the success of Ms Lagarde’s campaign is highly uncertain, with potentially profound consequences not only for the fund but for the global economy. …supporters of the fund say there are many possible scenarios in which it would be essential. If a recession and financial crisis were to hit in the coming years,central bankers may well struggle to find monetary remedies… a US Treasury spokesman left the door open to new possible contributions from America to the IMF. …Optimists point to a surprise decision by the Trump administration in April to support a $13bn boost to World Bank resources… there is still scepticism of the IMF among his top lieutenants at the Treasury department, including David Malpass, the undersecretary for international affairs. …Even if they were on board, economic and national security hawks at the White House who disdain multilateralism as a loss of sovereignty could be an additional obstacle, not to mention Republican lawmakers on Capitol Hill. The previous IMF quota increase, pushed by the Obama administration — which raised America’s permanent commitment to the fund to about $115bn — finally scraped through Congress in 2016, after a half-decade delay.

I was very saddened a couple of years ago when the GOP Congress agreed to expand the IMF’s bailout authority, especially since a similar effort was blocked in 2014 when Democrats still controlled the Senate.

The issue today is whether the Trump Administration will repeat that mistake.

Back in 2012, I stated that the IMF issue was a “minimum test” for Republicans. Well, the issues haven’t changed. Everything I wrote then still applies today.

I hope Trump does the right thing and rejects expanded bailout authority for the IMF for the sensible reason that it’s foolish to subsidize more borrowing by badly governed nations.

But I’m not picky. I’ll also be happy if Trump says no simply because he’s miffed that the IMF attacked him (accurately but unfairly) during the 2016 campaign and dissed his tax plan earlier this year.

There are just two principles you need to understand.

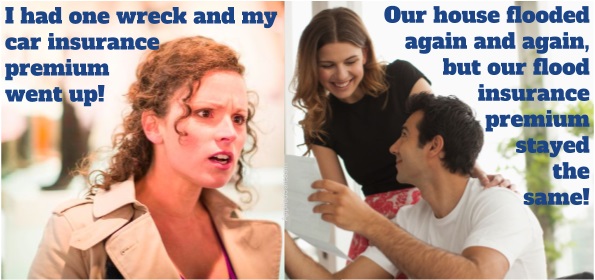

When Washington subsidizes something, you get more of it, and the federal government subsidizes building – and living – in risky areas.

When Washington provides bailouts, you incentivize risky behavior in the private sector and “learned helplessness” from state and local governments.

If I wanted to be lazy (or to be merciful and spare readers from a lengthy column), this satirical image is probably all that’s necessary to explain the first point. The federal government’s flood insurance program gives people – often the very rich, which galls me – an incentive to build where the risk of flooding and hurricanes is very high.

But let’s look at additional information and analysis.

We’ll start with this excellent primer on the issue from Professor William Shughart.

Disaster relief arguably is, in short, something of a public good that would be undersupplied if responsibility for providing it were left in the hands of the private sector. If this line of reasoning is sound, the activity of the Federal Emergency Management Agency (FEMA) or something like it is a proper function of the national government. …even if disaster relief is thought of as a public good—a form of “social insurance” against fire, flood, earthquake, and other natural catastrophes—it does not follow that government provision is the only or necessarily the best option. …both economic theory and the historical record point to the conclusion that the public sector predictably fails to supply disaster relief in socially optimal quantities. Moreover, because it facilitates corruption, creates incentives for populating disaster-prone areas, and crowds out self-help and other local means of coping with disaster, government provision of assistance to disaster’s victims actually threatens to make matters worse. …Government agencies are created by legislation, overseen by elected officials, and operated by huge bureaucracies. Public employees’ fear of being blamed for doing something wrong (or failing to do something right) produces risk aversion…the people who set priorities and make decisions are often separated by multiple layers of management from those on the ground who know what really needs to be done.

FEMA has been shown to be responsive more to the political interests of the White House than to the needs of disaster victims on the ground. …federal emergency relief funds tend to be allocated disproportionately to electoral-vote-rich states that are important to the sitting president’s reelection strategy. …The term moral hazard refers to the reduction in the cost of carelessness… The prospect of receiving federal and state reconstruction assistance after the next hurricane creates an incentive for others to relocate their homes and businesses from inland areas of comparative safety to vulnerable coastal areas. …The expectation of receiving publicly financed disaster relief may explain why 69 percent of the residents of Mississippi’s Gulf Coast did not have federal flood insurance when Katrina hit. …the immediate reactions of for-profit businesses, nongovernmental organizations large and small, and countless individual volunteers amply demonstrate that the private sector can and will supply disaster relief in adequate and perhaps socially optimal quantities

Barry Brownstein has a sober assessment of the underlying problem.

…federal flood insurance was amplifying the impact of storms by encouraging Americans to build and rebuild in areas prone to flooding. …the case against subsidized flood insurance is not a case against growth; it is a case against distorted growth. Federally supported insurance overrides the risk-reducing incentives that insurance premiums provide and results in building in vulnerable areas. …In a free market, insurance premiums on cars, for instance, tend to settle toward an “actuarially fair price.” …If you have a history of drunk driving, that increases the chances you’ll make an insurance claim on your car – so your premiums will be higher, and that encourages you not to drive in the future (or to drive sober in the first place). …Getting the government out of the flood insurance business and having insurance companies determine actuarially sound premiums is the only way for homeowners, businesses, and builders to know the real risk they are assuming.

And here are excerpts from a column by David Conrad and Larry Larson.

…the Great Flood of 1993 in the upper Midwest. After that disaster, the Clinton administration directed an experienced federal interagency task force to report on the flood and its causes. That report…made more than 100 recommendations for policy and program changes… The government found that many policies were encouraging — rather than discouraging — people to build homes and businesses in places with increasingly high risks of flooding… That often compounded the costs and problems caused by floods. …Experts and policymakers have known for a long time that we need to change the way we approach flood mitigation and prevention, but that hasn’t stopped the nation from making the same mistakes over and over. …substantial benefits for property owners and taxpayers could be gleaned by simply removing damaged buildings, rather than repairing them only to see them flooded out again. …many flood insurance policies were heavily subsidized and underestimated risk, leading to premiums that were far too low. …Americans facing some new devastation in the future will be looking back at Harvey and wondering why we didn’t act now.

National Flood Insurance Program…an…increasingly dysfunctional program. Enacted 50 years ago…, the program made a certain sense in theory…in return for appropriate local land-use and other measures to prevent development in low-lying areas and for actuarially sound premiums. Politics being what they are, the program gradually fell prey to pressure from developers and homeowners in the nation’s coastal areas. Arguably, the existence of flood insurance encouraged development in flood zones that would not have occurred otherwise. …Ideally, more of the costs of flood insurance would be shouldered by the people and places who benefit most from it; modern technology and financial tools should enable the private sector to handle more of the business, too. Such radical reform is not on Congress’s agenda, of course.

The National Flood Insurance Program, created in 1968 under LBJ on the theory that the private insurance market couldn’t handle flood damage, presumed that Washington could. Like many of his Great Society initiatives, it has turned out to be an expensive tutorial on the perils of government intervention. …A house outside of Baton Rouge, La., assessed at $56,000, has soaked up 40 floods and over $428,000 in insurance payouts. One in North Wildwood, New Jersey has been rebuilt 32 times. Nationally, some 30,000 buildings classified as “severe repetitive loss properties” have been covered despite having been swamped an average of five times each. Homes in this category make up about one percent of the buildings covered by the flood insurance program—but 30 percent of the claims. Their premiums don’t cover the expected losses. But as National Resources Defense Council analyst Rob Moore told The Washington Post, “No congressman ever got unelected by providing cheap flood insurance.” …The root of the problem is a familiar one: the people responsible for these decisions are not spending their own money. They find it easier to indulge the relative handful of flood victims than to attend to the interests of millions of taxpayers in general.

Now let’s look at some of the perverse consequences of federal intervention.

Brian Harmon had just finished spending over $300,000 to fix his home in Kingwood, Texas, when Hurricane Harvey sent floodwaters “completely over the roof.” The six-bedroom house, which has an indoor swimming pool, sits along the San Jacinto River. It has flooded 22 times since 1979, making it one of the most flood-damaged properties in the country. Between 1979 and 2015, government records show the federal flood insurance program paid out more than $1.8 million to rebuild the house—a property that Mr. Harmon figured was worth $600,000 to $800,000 before Harvey hit late last month. …Homes and other properties with repetitive flood losses account for just 2% of the roughly 1.5 million properties that currently have flood insurance, according to government estimates. But such properties have accounted for about 30% of flood claims paid over the program’s history. …Nearly half of frequently flooded properties in the U.S. have received more in total damage payments than the flood program’s estimate of what the homes are worth, according to the group’s calculations.

Disaster legislation, Rachel Bovard explained, is often an excuse for unrelated pork-barrel spending.

In 2012, President Obama requested a $60.4 billion supplemental funding bill from Congress, ostensibly to fund reconstruction efforts in the parts of the country most impacted by Hurricane Sandy. However, that’s not what Congress gave him, or what he signed. Instead, the bill was loaded up with earmarks and pork barrel spending, so much so that only around half of the bill ended up actually being for Sandy relief. Consider just a handful of the goodies contained in the final legislation…$150 million for Alaska fisheries (Hurricane Sandy was on the east coast of the US; Alaska is the country’s western most tip)…$8 million to buy cars and equipment for the Homeland Security and Justice departments (at the time of the Sandy supplemental, these agencies already had 620,000 cars between them)…$821 million for the Army Corps of Engineers to dredge waterways with no relation to Hurricane Sandy (the Corps never likes to waste a disaster)…$118 million for AMTRAK ($86 million to be used on non-Sandy related Northeast corridor upgrades). …the Sandy supplemental represented the worst of special interest directed, unaccountable, pork-barrel spending in Washington.

And as seems to always be the case with government, Jeffrey Tucker explains that disaster relief subsidizes corrupt favors for campaign contributors.

Look closely enough and you find corruption at every level. I recall living in a town hit by a hurricane many years ago. The town mayor instructed people not to clean up yet because FEMA was coming to town. To get the maximum cash infusion, the inspectors needed to see terrible things. When the money finally arrived, it went to the largest real estate developers, who promptly used it to clear cut land for new housing developments. …It does seem highly strange that this desktop operation in Montana would be awarded a $300 million contract to rebuild the electrical grid in Puerto Rico. That sounds outrageous. But guess what? …Zinke claims that he had “absolutely nothing to do” with selecting the company that got the contract, even though the company is in his hometown and his own son worked there. And yet there is more. The Daily Beast discovered that the company that is financing Whitefish’s expansions, HBC Investments, was founded by its current general partner Joe Colonnetta. He and his wife were larger donors to Trump campaign, in every form permissible by law and at maximum amounts. …FEMA has long been used as a pipeline to cronies.

The ideal solution is to somehow curtail the role of the federal government.

Which is what Holman Jenkins suggests in this column for the Wall Street Journal, even though he is pessimistic because rich property owners capture many of the subsidies.

What’s really missing in all such places is…proper risk pricing through insurance. …Now we wonder if it can even be ameliorated. …our most influential citizens all have one thing in common: a house in Florida. An unfortunate truth is that the value of their Florida coastal property would plummet if they were made to bear the cost of their life-style choices. A lot of ritzy communities would shrink drastically. Sun and fun would still attract visitors, but property owners and businesses would face a new set of incentives. Either build a lot sturdier and higher up. Or build cheap and disposable, and expect to shoulder the cost of totally rebuilding every decade or two. Faced with skyrocketing insurance rates, entire communities would have to dissolve themselves or tax their residents heavily to invest in damage-mitigation measures. …With government assuming the risk, why would businesses and homesteaders ever think twice about building in the path of future hurricanes?

Katherine Mangu-Ward of Reason offered some very sensible suggestions after Hurricane Harvey.

Many of the folks who take on the risk of heading into an unstable area do so because they are driven by the twin motivations of fellow-feeling and greed. These people are often the fastest and most effective at getting supplies where they are most needed, because that’s also where they can get the best price. This is just as true for Walmart as it is for the guy who fills his pickup with Poland Spring and batteries. Don’t use the bully pulpit to vilify disaster entrepreneurs, small or large. …by trying to control who gets into a storm zone to help, governments can wind up blockading good people who could do good while waiting for approval from Washington in a situation where communications are often bad. Ordinary people see and know things about what their friends and neighbors need and want that FEMA simply can’t be expected to figure out. …Emergency workers and law enforcement shouldn’t waste post-storm effort rooting around in people’s homes for firearms. Law-abiding gun owners do not, by and large, turn into characters from Grand Theft Auto when they get wet.

Amen to her point about so-called price gouging. The politicians who demagogue against price spikes either don’t understand supply-and-demand, or they don’t care whether people suffer. Probably both.

Sadly, FEMA, federal flood insurance, and other forms of intervention now play a dominant role when disasters occur.

That being said, let’s wrap up today’s column with some examples of how the private sector still manages to play a very effective role. We’ll start with this article from the Daily Caller.

Faith-based relief groups are responsible for providing nearly 80 percent of the aid delivered thus far to communities with homes devastated by the recent hurricanes… The United Methodist Committee on Relief, which has 20,000 volunteers trained to serve in disaster response teams, not only helps clean up the mess and repair the damage inflicted on homes by disasters, but also helps families… The Seventh Day Adventists help state governments with warehousing various goods and necessities to aid communities in the aftermath of a disaster. …Non-denominational Christian relief organization Convoy of Hope helps to provide meals to victims of natural disasters by setting up feeding stations in affected communities.

And I strongly recommend this video by Professor Steve Horwitz, my buddy from grad school.

The famous “Cajun Navy” is another example, as noted by the Baton Rouge Advocate.

The Pelican State managed Sunday to avoid most of Harvey’s fury. But around Baton Rouge, Lafayette and other parts of the state, members of the Cajun Navy sprung into action… Many who spent last August wading around south Louisiana’s floodwaters in boats packed them up Sunday and headed west to help rescue Texans caught in the floods. …”I can’t look at somebody knowing that I have a perfect boat in my driveway to be doing this and to just sit at home,” said Jordy Bloodsworth, a Baton Rouge member of the Cajun Navy who flooded after Hurricane Katrina when he lived in Chalmette. “I have every resource within 100 feet of me to help.” Bloodsworth was heading overnight on Sunday to Texas to help with search and rescue. …Others arrived in Texas earlier on Sunday. Toney Wade had more than a dozen friends…in tow as he battled rain and high water to get to Dickinson, Texas. Wade is the commander of an all-volunteer group of mostly former law enforcement officers and former firefighters called Cajun Coast Search and Rescue, based in Jeanerette. They brought boats and high-water rescue vehicles with them, along with food, tents and other supplies.

Here’s another good example of how the private sector – when it’s allowed to play a role – acts to reduce damage.

Increasingly, insurance carriers are finding wildfires, such as those in California, are an opportunity to provide protection beyond what most people get through publicly funded fire fighting. Some insurers say they typically get new customers when homeowners see the special treatment received by neighbors during big fires. “The enrollment has taken off dramatically over the years as people have seen us save homes,” Paul Krump, a senior executive at Chubb, said of the insurer’s Wildfire Defense Services. …Tens of thousands of people benefit from the programs. …The private-sector activity calls to mind the early days of fire insurance in the U.S., in the 18th and 19th centuries before municipal fire services became common. Back then, metal-plaque “fire marks” were affixed to the front of insured buildings as a guide for insurers’ own fire brigades.

It’s also important to realize that armed private citizens are the ones who help maintain order following a disaster, as illustrated by this video of a great American (warning: some strong language).

I imagine that guy would get along very well with the folks in the image at the bottom of this column.

Last but not least, here’s some analysis for history buffs of what happened after the fire that leveled much of Chicago in the 1800s.

…does the current emphasis on top-down disaster relief favored in the US and beyond represent the best strategy? Emily Skarbek, a professor at Brown University, approached this question by studying one of the most famous catastrophes of the 19th century, the Chicago fire of 1871. …scholars and laypeople alike are convinced that there is no substitute for the resources and direction that centralized governments can provide in the wake of a disaster. …This maxim was apparently inconsistent with the Chicago fire, however, as the Midwestern city was reconstructed in a remarkably short period of time, and without the supervision of an overbearing central government. …in 1871 there was no analogue to the present-day, Federal Emergency Management Agency (FEMA), meaning that relief efforts had to be decentralized. Moreover, there was no institutionalized source of government financial aid…it was up to Chicago’s residents to develop solutions to the calamity that they faced. …The Chicago Relief and Aid Society was founded, and set about coordinating the funds and efforts, including sophisticated bylaws regarding who merited support, and at what level. …the society exhibited the flexibility and adaptability necessary for it to expand dramatically immediately after the fire…and to subsequently contract once the needs for its services fell. This latter feature distinguishes Chicago’s relief efforts from those of 21st century government agencies.

Since I started with an image that summarizes the foolishness of government-subsidized risk, let’s end with another visual showing the impact of government.

Sadly, I predict that politicians will ignore these logical conclusions and immediately clamor after Hurricane Florence for another wasteful package of emergency spending, most of which will have nothing to do with saving lives and have everything to do with buying votes. Trump, being a big spender, will be cheering them on.

Which will then encourage more damage and risk more lives in the future. Lather, rinse, repeat.

This is one of the reasons I’m not a fan of a balanced budget amendment, Based on the experiences of American states and European countries, I fear politicians in Washington would use any deficit-limiting requirement as an excuse to raise taxes.

I much prefer spending caps, such as those found in Hong Kong, Switzerland, and Colorado. If you cure the disease of excessive government, you automatically ameliorate the symptom of too much borrowing.

That being said, the fiscal chaos plaguing European welfare states is proof that there is a point when a spending problem can also become a debt problem. Simply stated, the people and institutions that buy government bonds at some point will decide that they no longer trust a government’s ability to repay because the public sector is too big and the economy is too weak.

And even though the European fiscal crisis no longer is dominating the headlines, I fear this is just the calm before the storm.

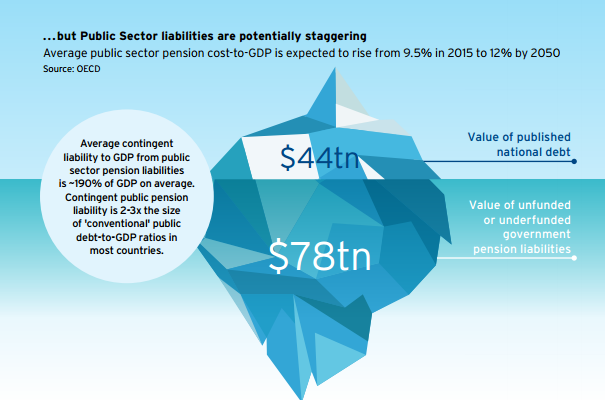

For instance, the data in a report from Citi about the looming Social Security-style crisis are downright scary.

…the total value of unfunded or underfunded government pension liabilities for twenty OECD countries is a staggering $78 trillion, or almost double the $44 trillion published national debt number.

And the accompanying chart is rather appropriate since it portrays this giant pile of future spending promises as an iceberg.

But it’s also important to realize that government policies also can encourage excessive debt in the private sector.

Before digging into the issue, let’s first make clear that debt is not necessarily bad. Households often borrow to buy big-ticket items like homes, cars, and education. And businesses borrow all the time to finance expansion and job creation.

But if there’s too much borrowing, particularly when encouraged by misguided government policies, then households and businesses are very vulnerable if there’s some sort of economic disruption and they no longer have enough income to finance debt payments. This is when debt becomes excessive.

Yet this is what the crowd in Washington is encouraging.

Writing for the Wall Street Journal, George Melloan warns that misguided “stimulus” and “QE” policies have created a debt bubble.

…while Mr. Bernanke and Ms. Yellen were trying to prevent deflation, the federal government was engineering its cause, excessive debt. And the Fed abetted the process by purchasing trillions of dollars of government paper, aka quantitative easing. Near-zero interest rates also have encouraged consumers and business to releverage. Cars are now financed with low or no-interest five-year loans. With the 2008 housing debacle forgotten, easier mortgage terms have made a comeback. Corporations also couldn’t let cheap money go to waste, so they have piled up debts to buy back their own stock. Such “investment” produces no economic growth, but it has to be paid back nonetheless. Amid the Great Recession, many worried that the entire economy of the U.S., or even the world, would be “deleveraged.” Instead, we have a new world-wide debt bubble.

The numbers he shares are sobering.

Global debt of all types grew by $57 trillion from 2007 to 2014 to a total of $199 trillion, the McKinsey Global Institute reported in February last year. That’s 286% of global GDP compared with 269% in 2007. The current ratio is above 300%.

Professor Noah Smith writes in Bloomberg about research showing that debt-fueled bubbles are especially worrisome.

…since debt bubbles damage the financial system, they endanger the economy more than equity bubbles, which transmit their losses directly to households. Financial institutions lend people money, and if people can’t pay it back — because the value of their house has gone down — it could cause bank failures. …Economists Oscar Jorda, Moritz Schularick, and Alan Taylor recently did a historical study of asset price crashes, and they found that, in fact, debt seems to matter a lot. …To make a long story short, they look at what happened to the economy of each country after each large drop in asset prices. …bubbles make recessions longer, and credit worsens the effect. …the message is clear: Bubbles and debt are a dangerous combination.

To elaborate, equity and bubbles aren’t a good combination, but there’s far less damage when an equity bubble pops because the only person who is directly hurt is the person who owns the asset (such as shares of a stock). But when a debt bubble pops, the person who owes the money is hurt, along with the person (or institution) to whom the money is owed.

Desmond Lachman of the American Enterprise Institute adds his two cents to the issue.

…the world is presently drowning in debt. Indeed, as a result of the world’s major central banks for many years having encouraged markets to take on more risk by expanding their own balance sheets in an unprecedented manner, the level of overall public and private sector indebtedness in the global economy is very much higher today than it was in 2008 at the start of the Great Economic Recession. Particularly troublesome is the very high level of corporate debt in the emerging market economies and the still very high public sector debt levels in the European economic periphery. …the Federal Reserve’s past policies of aggressive quantitative easing have set up the stage for considerable global financial market turbulence. They have done so by artificially boosting asset prices and by encouraging borrowing at artificially low interest rates that do not reflect the likelihood of the borrower eventually defaulting on the loan.

In other words, artificially low interest rates are distorting economic decisions by making something (debt) seem cheaper than it really is. Sort of financial market version of the government-caused third-party payer problem in health care and higher education.

And Holman Jenkins of the Wall Street Journal makes the very important point that debt is encouraged by bailouts and subsidies.

Big banks aren’t automatically bad or badly managed because they are big, but it’s hard to believe big banks would exist without an explicit and implicit government safety net underneath them. …None of this has changed since Dodd-Frank, none of it is likely to change. …we know where the crisis will come from and how it will be transmitted to the financial system. The Richmond Fed’s “bailout barometer” shows that, since the 2008 crisis, 61% of all liabilities in the U.S. financial system are now implicitly or explicitly guaranteed by government, up from 45% in 1999. …Six years after a crisis caused by excessive borrowing, McKinsey estimates that even visible global debt has increased by $57 trillion, while in the U.S., Europe, Japan and China growth to pay back these liabilities has been slowing or absent.

The bottom line is that government spending programs directly cause debt, but we should be just as worried about the private debt that is being encouraged and subsidized by other misguided government policies.

And surely we shouldn’t forget to include the pernicious role of the tax code, which further tilts the playing field in favor or debt.

P.S. Let’s briefly divert to another issue. I wrote last Christmas that President Obama may have given the American people a present.

But the Washington Examinerreports that gift has turned into a lump of coal.

The Department of Justice announced this week that it is resuming its Equitable Sharing program…that allows state and local police to get around tough state laws that limit how much property can be taken from citizens without being charged with wrongdoing, let alone convicted of a crime. …money-hungry police departments can exploit these lax federal rules about confiscating people’s property. The feds like this because they get a cut of the loot. …there is no presumption of innocence. …civil forfeitures by the feds amounted to $4.5 billion in 2014, which is more than the $3.9 billion that all of America’s burglars stole that year. It’s hard to imagine more compelling evidence of gross wrong.

Wow, so the government steals more money than burglars. I guess I’m not surprised.

But if you really want to get upset, check out real-world examples of asset forfeiture by clicking here, here, here, here, and here.

Thankfully, some states are seeking to curtail this evil practice.

Well, it’s becoming an issue in the 2016 presidential race, with some folks criticizing Donald Trump for siding with Bush and Obama on the issue.

I suppose I could make a snide observation about the absurdity of Trump being perceived as an anti-establishment candidate when he supported a policy that had unanimous support from political insiders.

But I would much rather focus on the policy implications. So when Neil Cavuto asked me to comment on Chris Christie’s rejection of bailouts, I took the opportunity to stress (once again) that it wasn’t a TARP-or-nothing choice and that there was a sensible, non-corrupt, way of dealing with failing financial firms. Simply stated, only bail out depositors and let bondholders and shareholders take the hit.

For the geeks who are reading this, you’ll recognize that the policy I’m advocating is often called the FDIC-resolution approach.