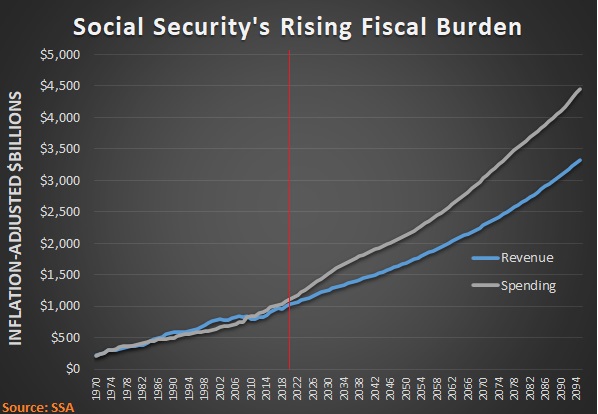

I’m a long-time critic of the Federal Reserve, Fannie Mae, and Freddie Mac, but I had no idea they would produce something as bad as the 2008 financial meltdown. It’s not easy to predict the timing and severity of a crisis.

Unless we’re talking about the ticking time bomb described in this video.

In theory, of course, state politicians and their local counterparts are supposed to set aside enough money to pay the lavish future benefits they promise their bureaucrats.

Far too often, however, that doesn’t happen. And that means the governments (to be more accurate, their taxpayers) have a big “unfunded liability.”

Far too often, however, that doesn’t happen. And that means the governments (to be more accurate, their taxpayers) have a big “unfunded liability.”

This racket is a good deal for the bureaucrats – who get lots of pay now and lots of promised benefits in the future. And it’s a good deal for the state and local politicians who get votes and campaign contributions from the bureaucrats.

But, as explained in a new report from the American Legislative Exchange Council, it is a fiscal disaster that is going to explode at some point in the not-too-distant future.

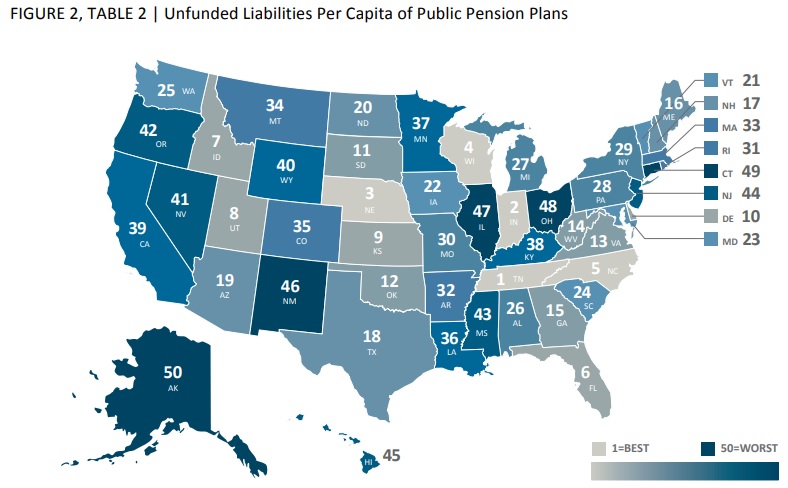

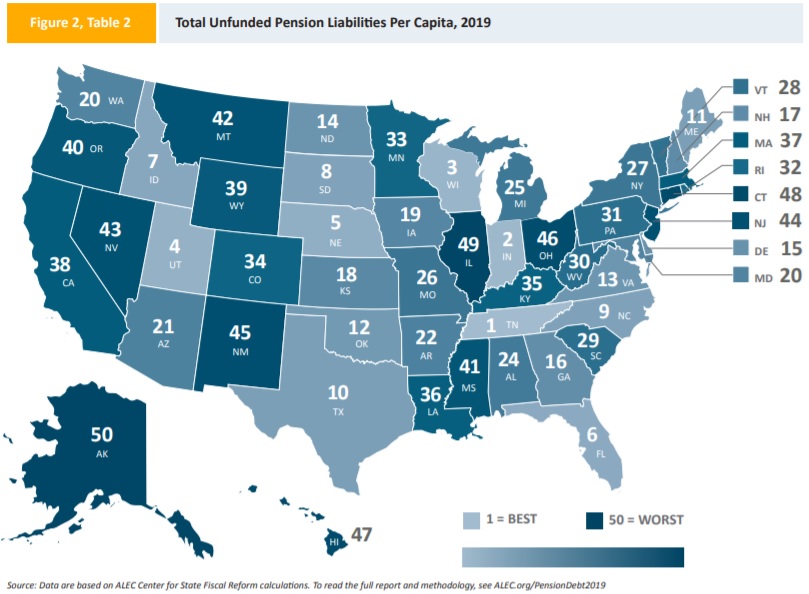

Unfunded state pension liabilities total $4.9 trillion or $15,080 for every man, woman and child in the United States. State governments are often obligated, by contract and state constitutional law, to make these pension payments regardless of economic conditions.

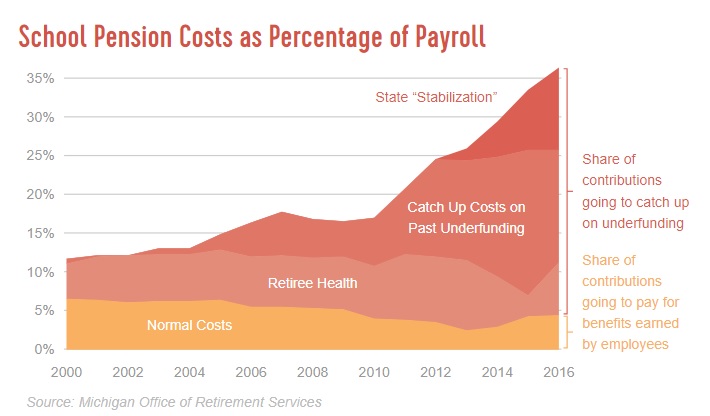

As these pension payments continue to grow, revenue that would have gone to essential services like public safety and education, or tax relief, goes to paying off these liabilities instead. …Most state pension plans are structured as defined-benefit plans. Under a defined-benefit plan, an employee receives a fixed payout at retirement based on the employee’s final average salary, the number of years worked and a benefit multiplier.

There are several ways to measure the degree to which a state has dug a big hole by promising big goodies to bureaucrats.

Figure 2 shows per-capita unfunded liabilities on a state-by-state basis. Tennessee is in the best shape, followed by Indiana and Wisconsin (thanks in part to former Governor Scott Walker). Alaska has the biggest fiscal hole, along with Illinois (no surprise) and Connecticut (no surprise).

It’s important to recognize, though, that some states have more income than others.

So in addition to a per-capita estimate of pension liabilities, here’s a map showing the burden as a share of each state’s economic output. Once again, Tennessee, Indiana (the #22 is a misprint), and Wisconsin rank the highest. Alaska stays at the bottom, joined by Mississippi and New Mexico.

Let’s also give credit and blame to states that are the top 10 and bottom 10 on each map.

In addition to Tennessee, Indiana, and Wisconsin, good states include Utah, Nebraska, South Dakota and Texas (honorable mention to Florida, which just missed).

Bad states are led by Alaska, with Nevada, New Mexico, Mississippi, Illinois, and Ohio also being governed by particularly short-sighted politicians.

So what’s the solution for the bad states? The ALEC report gives the answer.

Ultimately, one of the best ways to solve the pension crisis is to change the way pension plans are structured. Changing from the current defined-benefit system toward a defined-contribution system for new employees will improve the health of state pension plans by giving employees full control over their retirement savings.

By the way, it’s worth noting that blue states may have a bigger problem than red states, but this is a bipartisan mess.

In a recent column in the Wall Street Journal, Steve Malanga says there is plenty of blame to share.

The crisis in state pension systems is a result of decades of fiscal mismanagement. The problem, however, goes well beyond deeply indebted Illinois and New Jersey. Many state and municipal retirement funds have been on an unrelenting downward trajectory…

This fiscal nightmare stems in part from politicians’ habit of increasing employee benefits while markets are booming, thereby squandering fund surpluses. …Politicians have consistently neglected to contribute to these systems even during good budgetary times, preferring to fund more popular programs. …Meanwhile, elected officials and pension administrators have endorsed overly optimistic economic assumptions that made their systems look affordable.

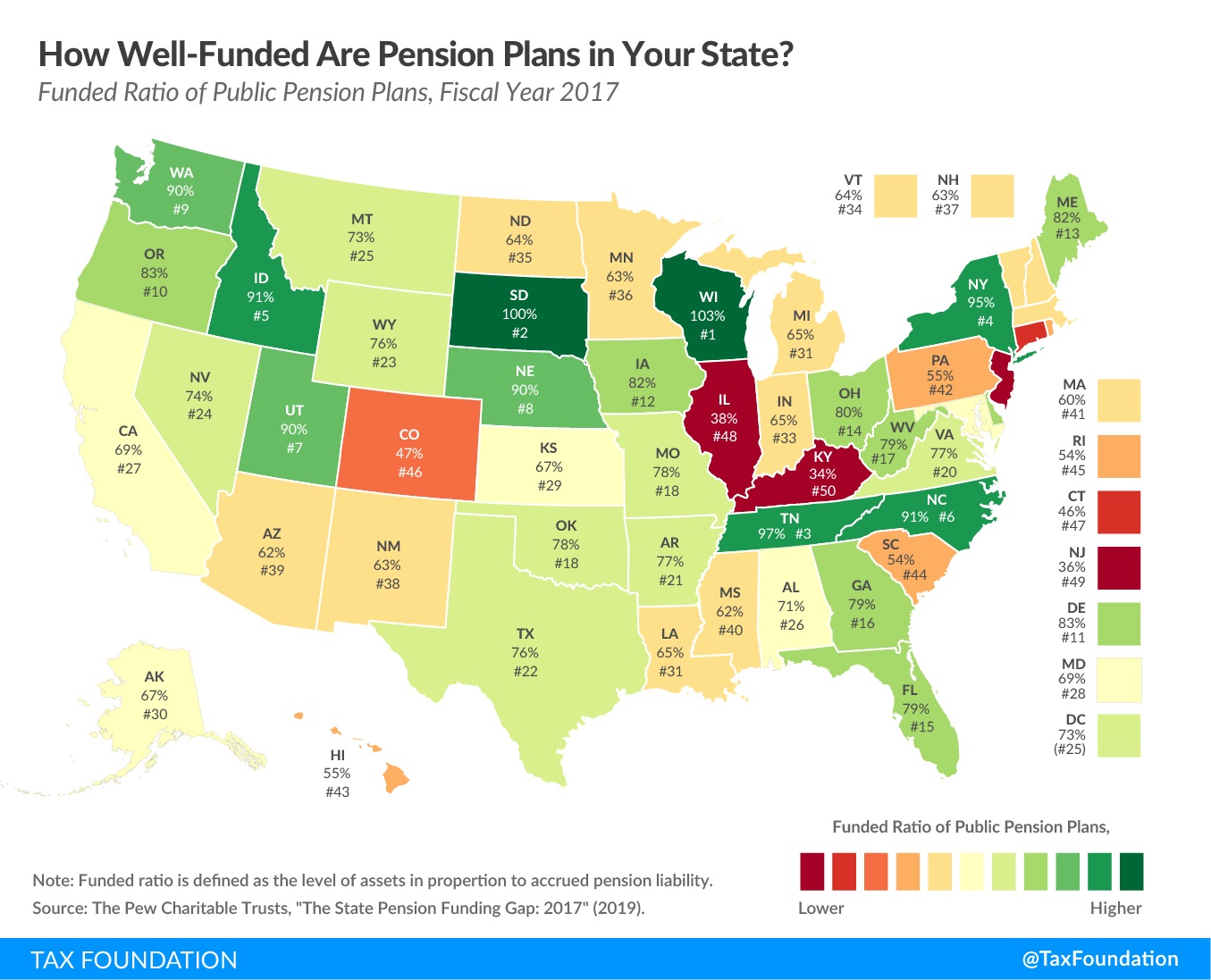

Let’s close today’s grim column with another way of measuring the problem.

Here’s a map from the Tax Foundation that shows how much money is set aside in pension programs compared to the level of benefits that bureaucrats are promised.

Looking at the data from this angle, Kentucky has the biggest hole, followed by New Jersey, Illinois (the only state to be in the bottom 10 on all three maps), and Connecticut, while the good states are led by Wisconsin, South Dakota, and Tennessee.

The bottom line is that some states have a very grim future, which is why even Warren Buffett is advising investors and entrepreneurs to steer clear of doing business in those places.

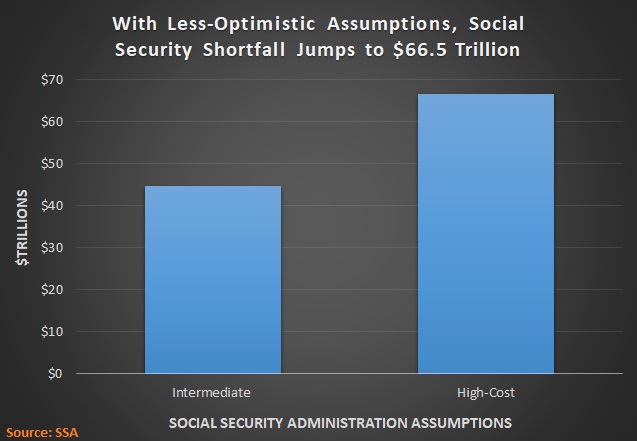

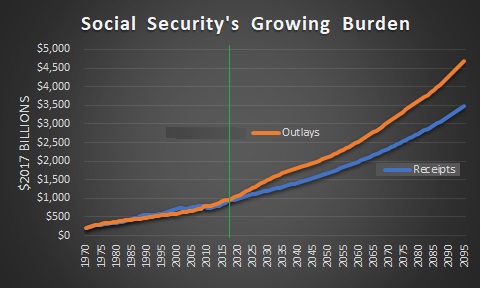

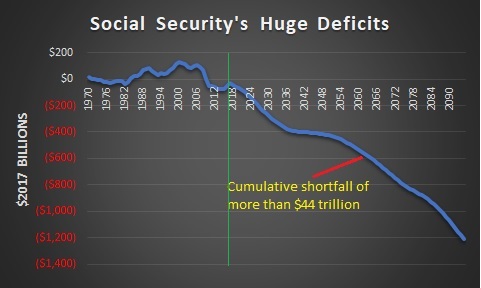

P.S. Unfortunately, you can’t avoid the massive unfunded liabilities of Social Security, Medicare, and Medicaid by moving across state lines.