Every year, the Social Security Administration issues a “Trustees Report” that summarizes the program’s financing. So every year (see 2018, 2017, 2016, 2015, etc) I cut through all the verbiage and focus the numbers that really matter.

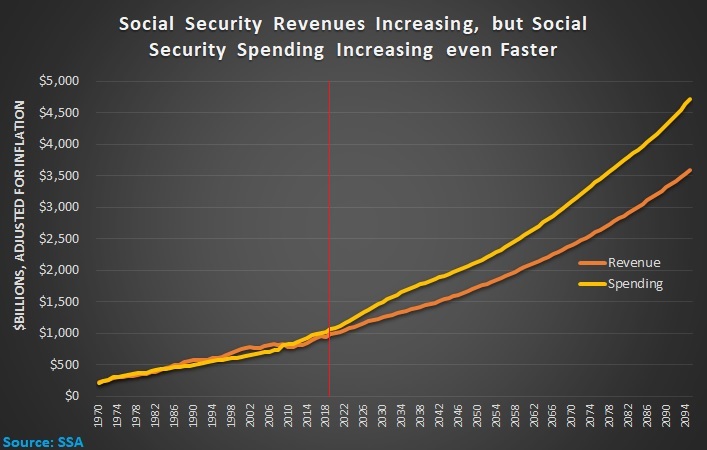

First, here’s the data from Table VI.G9 showing annual spending and annual revenue, and the numbers are adjusted for inflation. Everything to the left of the vertical red line is historical data. Everything to the right is an estimate based on “intermediate” economic and demographic projections.

The bad news is that there’s a never-ending increase in the program’s fiscal burden.

The only good news is that country presumably will be much richer in the future, so we’ll have more income to pay all those taxes and finance all that spending.

That being said, the fiscal burden is projected to increase faster than our income, so the economic burden of Social Security will increase over time.

But there’s also a wild card to consider. Simply stated, we have more data from Table VI.G9 that shows the program has a giant, ever-expanding deficit.

Here are the grim numbers (though not quite as grim as last year when the cumulative shortfall was $43.7 trillion). Once again, everything to the left of the line is historical data and everything to the right is a projection.

The obvious takeaway is that the program is bankrupt.

Indeed, a private pension fund with these numbers would have been shut down a long time ago. And its executives would be in prison for running a Ponzi Scheme.

Politicians won’t put themselves in prison, of course, but they eventually will be forced to address Social Security’s huge shortfall. If nothing else, the so-called Trust Fund (which isn’t a real Trust Fund since it is filled with IOUs) runs out of money in 2035.

The interesting question is what sort of “solution” they choose when the crisis occurs.

Sadly, many politicians are gravitating to a plan to impose ever-higher taxes to prop up the system.

A far better approach is personal retirement accounts. I’ve written favorably about the Australian system, the Chilean system, the Hong Kong system, the Swiss system, the Dutch system, the Swedish system. Heck, I even like the system in the Faroe Islands.

The bottom line is that there’s been a worldwide revolution in favor of private savings and the United States is falling behind.

P.S. If you have some statist friends and family who get confused by numbers, here’s a set of cartoons that shows the need for Social Security reform.

P.P.S. As I explain in this video, reform does not mean reducing benefits for current retirees, or even older workers.

[…] problem seems to worsen. The 75-year shortfall was $44.7 trillion according to the 2020 report and $42.1 trillion according to the 2019 […]

[…] problem seems to worsen. The 75-year shortfall was $44.7 trillion according to the 2020 report and $42.1 trillion according to the 2019 […]

[…] problem seems to worsen. The 75-year shortfall was $44.7 trillion according to the 2020 report and $42.1 trillion according to the 2019 […]

[…] problem seems to worsen. The 75-year shortfall was $44.7 trillion according to the 2020 report and $42.1 trillion according to the 2019 […]

[…] problem seems to worsen. The 75-year shortfall was $44.7 trillion according to the 2020 report and $42.1 trillion according to the 2019 […]

[…] problem seems to worsen. The 75-year shortfall was $44.7 trillion according to the 2020 report and $42.1 trillion according to the 2019 […]

[…] problem seems to worsen. The 75-year shortfall was $44.7 trillion according to the 2020 report and $42.1 trillion according to the 2019 […]

[…] Sadly, the United States isn’t part of that conversation since we’re still stuck with our actuarially bankrupt Social Security scheme. […]

[…] They have voted themselves generous pensions, so they they don’t have to worry about a bankrupt Social Security system. […]

[…] Good News from Dan our Man in DC. The social security system is only $42.1 Trillion in the hole. […]

[…] bad news is that Bloomberg never supported the right policies that would address both Social Security’s gigantic fiscal shortfall and the fact that the program is a really bad deal for younger workers. Instead, he supported plans […]

[…] Security is projected to consume an ever-larger share of America’s national income, mostly thanks to an aging […]

[…] Security is projected to consume an ever-larger share of America’s national income, mostly thanks to an aging […]

[…] Security is projected to consume an ever-larger share of America’s national income, mostly thanks to an aging […]

[…] not a big fan of the current tax system. I’m also not supportive of America’s bankrupt Social Security […]

[…] but Australia’s system of private retirement accounts is vastly superior to America’s bankrupt tax-and-transfer Social Security […]

Simple solution… Social Security (and Medicare and medicaid) are all UnConstitutional. So government should stop spending money on them,, not tomorrow,,, but right now,, today.

Also government has no authority to force people to save money, (or buy health insurance) so talking about forced private savings is a non starter…

Social Security is a vestige of the failed New Deal, and ought to be done away with. The current obligation could be met by selling government properties – which the government anyway has no right to own.

When Bismarck offered the first Social Security-like system, back in the 1870’s, benefits were paid out to those over 70. Life span for those that survived childbirth was only 48.

Obviously, with retirement at 66 and people living until almost 80, something must be done.

More money is not the answer. Less money is not the answer. The only appropriate answer under the current system is to raise retirement age, to reflect changing demographics.

The problem with a gradual increase in retirement age is that life span might increase faster.

We must get new entrants to the system out of this system, and give those with many years to go the option of bailing out, for reduced government benefits in the future.

This leaves us with quite an unfunded “nut” that tax payers will need to face, but better to face it now, rather than kick the can any further.

Our system supports government spending.

In private systems investment supports private enterprises.

Obviously, we want to expand private rather than public, BUT we do not want the government guiding us as to which investments.

Right now it is the upper classes that invest heavily in the private sector, and as a result returns are skewed toward the upper classes. If Social Security was invested privately, “inequality” would not be such a big deal, since all would participate. Sadly, the returns would diminish from current levels, but they would still be a better bet than investing in government bonds.

While your chart may have been picked from other sources, it is somewhat disingenuous, in that it ends in 2094, which means that it includes about 9 years of population that has not yet reached 21.

Our system is atrocious as it is. There is no reason to include people who have not yet joined the workforce.