Why would the economy grow faster if we got fundamental reform such as the flat tax?

In part, because there would be one low tax rate instead of the discriminatory and punitive “progressive” system that exists today. As such, the penalty on productive behavior would be reduced.

In part, because there would be no distorting tax breaks that lure people into making decisions based on tax considerations rather than economic merit.

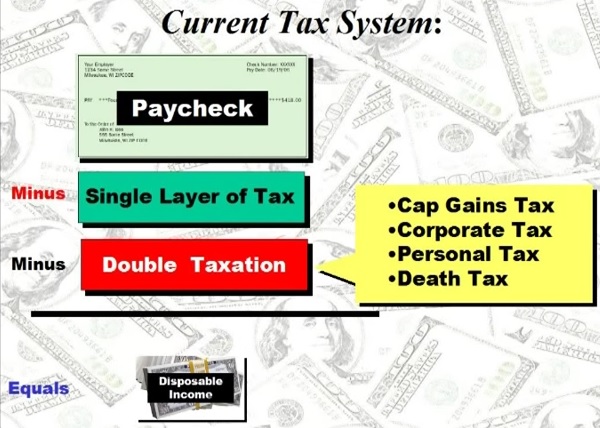

But we’d also enjoy more growth because there would be no more double taxation. Under a flat tax, the death tax is abolished, the capital gains tax is abolished, there’s no double taxation on savings, the second layer of tax on dividends is eliminated, and depreciation is replaced by expensing.

But we’d also enjoy more growth because there would be no more double taxation. Under a flat tax, the death tax is abolished, the capital gains tax is abolished, there’s no double taxation on savings, the second layer of tax on dividends is eliminated, and depreciation is replaced by expensing.

In the wonky jargon of public finance economists, this means we would have a “consumption-based” system, which is just another way of saying that income would be taxed only one time. No longer would the internal revenue code discourage capital formation by imposing a higher effective tax rate on income that is saved and invested (compared to the tax rate on income that is consumed).

Indeed, this is the feature of tax reform that probably generates the most growth. As I explain in this video on capital gains taxation, all economic theories – even Marxism and socialism – agree that capital formation is a key to long-run prosperity.

The good news is that reducing double taxation is a goal of most major tax plans in Washington. Trump’s campaign plan reduced double taxation, and the House Better Way Plan reduces double taxation.

But that doesn’t mean there’s an easy path for reform. The Hill reports on some of the conflicts that may sabotage legislation this year.

The fight over a border-adjustment tax isn’t the only challenge for Republicans in their push for tax reform. …Notably, some business groups have criticized the proposal to do away with the deduction for businesses’ net interest expenses. …the blueprint does not specifically discuss how the carried interest that fund managers receive would be taxed. Under current law, carried interest is taxed as capital gains, rather than at the higher rates for ordinary income. During the presidential race, Trump repeatedly said he wanted to eliminate the carried interest tax break, and Office of Management and Budget Director Mick Mulvaney told CNN on Sunday that Trump still plans to do this. Many Democrats also want carried interest to be taxed as ordinary income.

The border-adjustment tax is probably the biggest threat to tax reform, but the debate over “carried interest” also could be a problem since Trump endorsed a higher tax burden on this type of capital gain during the campaign.

Here are some excerpts from a recent news report.

Donald Trump vowed to stick up for Main Street over Wall Street — that line helped get him elected. But the new president has already hit a roadblock, with fellow Republicans who control Congress balking at Trump’s pledge to close a loophole that allows hedge fund and private equity managers to pay lower taxes on investment management fees. …The White House declined to comment on the status of negotiations between Trump and congressional Republicans over the carried-interest provision. …U.S. Rep. Jim Himes, D-Conn., a House Financial Services Committee member and former Goldman Sachs executive, said there is chaos on the tax reform front. “That’s on the list of dozens of things where there is disagreement between the president and the Republican majority in Congress,” Himes said.

Regarding the specific debate over carried interest, I’ve already explained why I prefer current law over Trump’s proposal.

Today I want to focus on the “story behind the story.” One of my main concerns is that the fight over the tax treatment of carried interest is merely a proxy for a larger campaign to increase the tax burden on all capital gains.

Today I want to focus on the “story behind the story.” One of my main concerns is that the fight over the tax treatment of carried interest is merely a proxy for a larger campaign to increase the tax burden on all capital gains.

For instance, the ranking Democrat on the Senate Finance Committee openly uses the issue of carried interest as a wedge to advocate a huge increase in the overall tax rate on capital gains.

Of course, when you talk about the carried interest loophole, you’re talking about capital gains. And when you talk about capital gains, you’re talking about the biggest tax shelter of all – the one hiding in plain sight. Today the capital gains tax rate is 23.8 percent. …treat[ing] income from wages and wealth the same way. In my view, that’s a formula that ought to be repeated.

The statists at the Organization for Economic Cooperation and Development also advocate higher taxes on carried interest as part of a broader campaign for higher capital gains taxes.

Taxing as ordinary income all remuneration, including fringe benefits, carried interest arrangements, and stock options… Examining ways to tax capital income at the personal level at slightly progressive rates, and align top capital and labour income tax rates.

It would be an overstatement to say that everyone who wants higher taxes on carried interest wants higher taxes on all forms of capital gains. But it is accurate to assert that every advocate of higher taxes on capital gains wants higher taxes on carried interest.

If they succeed, that would be a very bad result for American workers and for American competitiveness.

For those wanting more information, here’s the Center for Freedom and Prosperity’s video on carried interest.

Last but not least, wonky readers may be interested in learning that carried interest partnerships can be traced all the way back to medieval Venice.

Start-up merchants needed investors, and investors needed some incentive to finance the merchants. For the investor, there was the risk of their investment literally sailing out of the harbor never to be seen again. The Venetian government solved this problem by creating one of the first examples of a joint stock company, the “colleganza.” The colleganza was a contract between the investor and the merchant willing to do the travel. The investor put up the money to buy the goods and hire the ship, and the merchant made the trip to sell the goods and then buy new foreign goods that could then be brought back and sold to Venetians. Profits were then split between the merchant and investor according to the agreements in the contract.

Fortunately for the merchants and investors of that era, neither income taxes nor capital gains taxes existed.

P.S. Italy didn’t have any sort of permanent income tax until 1864. Indeed, most modern nations didn’t impose these punitive levies until the late 1800s and early 1900s. The United States managed to hold out until that awful dreary day in 1913. It’s worth noting that the U.S. and other nations managed to become rich and prosperous prior to the adoption of those income taxes. And it’s also worth noting that the rapid growth of the 18th century occurred when the burden of government spending was very modest and there was almost no redistribution spending.

P.S. Italy didn’t have any sort of permanent income tax until 1864. Indeed, most modern nations didn’t impose these punitive levies until the late 1800s and early 1900s. The United States managed to hold out until that awful dreary day in 1913. It’s worth noting that the U.S. and other nations managed to become rich and prosperous prior to the adoption of those income taxes. And it’s also worth noting that the rapid growth of the 18th century occurred when the burden of government spending was very modest and there was almost no redistribution spending.

P.P.S. Now that we have income taxes (and the bigger governments enabled by those levies), the only silver lining is that governments have compensated for bad fiscal policy with better policy in other areas.

[…] gains, a more punitive death tax, and a higher tax rate on capital gains that are part of “carried interest” (even though that becomes irrelevant if the regular capital gains rate is being […]

[…] I sympathize with Mr. Fink’s policy objective (especially since higher taxes on carried interest would be the precursor for higher taxes on other forms of capital gains), but I very much disagree with his […]

[…] with Mr. Fink’s policy objective (especially since higher taxes on carried interest would be the precursor for higher taxes on other forms of capital gains), but I very much disagree with his […]

[…] Many people don’t realize that income taxes only began to plague the world about 100 years ago. […]

On the issue of the capital gains tax, I favor its elimination. But if we must have it at all, I say tax labor and investment at the same rate. Maybe 10%. No loopholes, all deductions scrapped with the exception of the deduction for charitable donations.

I’m a huge supporter of capital gain, etc. elimination, to stimulate growth, but let’s look at the practical impact of eliminating the capital gains tax:

1. With elimination there would be a one-time windfall gain for stockholders. Why? Rather than receiving 80% of the return, they would receive 100% and stocks would increase by 25% (20%/80%). This run-up would occur prior to the abolishment date. Future purchasers would have to pay a higher price, so their returns should be the same as current after-tax returns on lower priced stock.

2. Growing companies issuing new stock would benefit, since to raise the same money they would only have to issue 80% of the stock that would have been required previously.

3. Elimination is one of the sticking points in moving to a flat or sales tax, because of the wealth benefits.

To pass political hurdles, we should pass a “Painless Tax” that would occur in conjunction with abolishment. This would be a one-time tax on all accumulated gains at 20%. How could it be painless?

1. Gains on the stock from elimination will always exceed the amount of the tax, since the tax is only on accumulated gains, not the full value of the stock.

2. Taxes could be paid by individuals using future Social Security payments, so for most there would be no out-of-pocket payments. One of the possible methods of addressing the coming Entitlement crisis would be to means-test, so future Social Security for those with substantial assets are at risk anyhow.

3. If capital gains is not eliminated, they would have to have paid this tax at some point in the future.

Carried interest has been a hot topic for years, with lawmakers promising to “fix” this enormous injustice upon the US tax system being perpetrated by those Wall Street criminals! Is that so?

Let’s first discuss what carried interest means. At its simplest, it means that one party to a consensual transaction gets more out of the transaction proportionally than the amount of cash he or she put into it. A simple example would be two partners getting together to form a business to mow lawns. Partner Worker Bee (Worker to his friends) puts up $100 and Partner Money Bags (Money to her friends) puts up $9,900. Money has a full time job, so she cannot be active in the business, but is available to help deal with the big issues. As a result, they agree to split the profits 50/50. (In tax parlance, this is what is called a special allocation. We need not get into the details of that to understand carried interest.) They buy a $10,000 lawn mower, and as they say, the rest is history!

Another more complicated scenario would be what happens when Worker and Money take the millions they have reaped from selling their lawn mowing business ten years down the road. At that point, Worker invests $1,000,000 in a new venture (Real Estate LLC), Money invests $9,000,000 in Real Estate LLC, and they borrow $40,000,000 from the bank to buy an undervalued office building. They agree to split the profits 10/90 initially. But Money, wanting to incentivize Worker to maximize return in the long run, agrees to split profits 50/50 after Money has received a certain return on her investment. They agree that the required return will be a 25% IRR. (IRR means Internal Rate of Return which is a complicated calculation, but can be described simply as follows. It is the interest rate that makes the net present value of all cash flows, both positive and negative, from a specified investment, equal to zero. It is not simply the total return divided by the time frame of the investment. It takes into account when the outflows and inflows occurred, based on the simple premise that one dollar invested today costs you more than one $1.00 invested a year from now, and one dollar earned today is worth more than $1.00 earned one year from now.)

Let’s go back to the two scenarios above and make a few calculations. The lawn mowing business earned $1,000,000 each year during its life before being sold. As the law reads today, this is what would happen on their tax returns. Worker would be allocated $500,000 of ordinary income and Money would be allocated $500,000 of ordinary income. Thus, the IRS would collect taxes on $1,000,000 at ordinary income tax rates. As many have proposed amending the law, any amount which Worker receives above his proportionate contribution would be deemed compensation. As such, Worker would be allocated 1% (Worker’s initial contribution of $100 divided by total contributions of $10,000) of the business net profits (1% of $1,000,000 = $10,000) and would be deemed to have received $490,000 of compensation (taxed of course at ordinary income tax rates) for a total of $500,000. Money would be allocated $990,000 of the net income earned by the business.

But wait you say! How can a lawn mowing business that earned $1,000,000 of total net income lead to its partners having to pay taxes on income totaling $1,490,000 ($490,000 of compensation to Worker, $10,000 of business profits allocated to Worker and $990,000 of profits allocated to Money)! It does not. If Worker has compensation of $490,000, someone paid it and is thus entitled to deduct the compensation on its tax return (a fact that most people discussing carried interest cannot seem to comprehend). Now the business only earned a net income of $510,000 ($1,000,000 minus compensation paid of $490,000). Allocation of profits to Worker and Money are now $10,000 and $500,000, respectively! (The actual allocation would be slightly different, but the precise calculation is not important). At the end of the day, the IRS collects ordinary income taxes on a total of $1,000,000 of income. Who cares? What is the difference? The only difference in tax receipts can come from different marginal tax rates between the two partners.

Let’s move ahead a few years. Real Estate LLC decides to sell its office building for $100,000,000, for a profit of $50,000,000 (once again, the calculation is more complicated than that, taking into account recapture and many other things, but the precise calculations are not material to our discussion). The profits from the sale of the building are long term capital gains, and thus subject to taxation at a different rate. Let’s see how the profits are allocated. Because a 25% IRR is a fairly high return, a 25% IRR from a real estate investment is usually only achieved, if at all, upon a sale of the property. Thus during the life of Real Estate LLC, the income would have been allocated 10% to Worker and 90% to Money. In order to make the calculations simpler and understandable, let’s also assume by some magical event, that Money’s 25% IRR was achieved on the day before the property was sold. We are now only dealing with the allocation of the capital gain. As we saw above, allocations of ordinary income on a disproportionate basis are immaterial.

Under current law and the Real Estate LLC operating agreement (where they split profits 50/50 after achieving the 25% IRR), the $50,000,000 of capital gain would be allocated $25,000,000 to each of Worker and Money. The IRS would thus collect capital gains taxes on a total of $50,000,000!

As proposed, any capital gains received by Worker in excess of his 10% share would now be deemed compensation and taxed to him as ordinary income. As in the lawn mowing business, if someone receives compensation, someone paid it! Real Estate LLC’s tax return now looks like this:

Worker Money Total

Compensation $20,000,000 $20,000,000

Deduction for Paying Compensation

($2,000,000)

($18,000,000)

($20,000,000)

Capital Gains $5,000,000 $45,000,000 $50,000,000

Total $50,000,000

As in the lawnmower case, at the end of the day the IRS collects capital gains taxes on $50,000,000, and nothing else. The difference to aggregate tax receipts can only come from differences in marginal tax rates. . As between Worker and Money, the tax implications are significantly different. Worker will now pay ordinary income tax rates on $20,000,000, a spread of roughly 20 percentage points, for an additional tax bill of $4,000,000 +/-. Money, on the other hand, will have an additional deduction of $18,000,000, leading to a tax savings of $7,800,000 +/-, which is partially offset by the additional capital gains taxes she will incur as a result of the allocation of the additional $20,000,000 of capital gains.

As best as I know, the proposed changes to tax law to deal with the perceived “unfairness” of special allocations (how can it be unfair if both parties agreed to it?) would be the first time ever that the tax rates applied to income were based upon whom received it as opposed to the underlying character of the income. Not to mention the almost assured unintended consequence of drastically altering how capital and talent are allocated! Doesn’t Congress have something more important to work on?