Three years ago, I shared two videos explaining taxation and deadweight loss (i.e., why high tax burdens are bad for prosperity).

Today, I have one video on another important principle of taxation. To set the stage for this discussion, here are two simple definitions

- The “average tax rate” is the share of your income taken by government. If you earn $50,000 and your total tax bill is $10,000, then your average tax rate is 20 percent.

- The “marginal tax rate” is the amount of money the government takes if you earn more income. In other words, the additional amount government would take if your income rose from $50,000 to $51,000.

These definitions are important because we want to contemplate why and how a tax cut helps an economy.

But let’s start by explaining that a tax cut doesn’t boost growth because people have more money to spend.

I want people to keep more of their earnings, to be sure, but that Keynesian-style explanation overlooks the fact that the additional “spending power” for taxpayers is offset when the government borrows more money to finance the tax cut.

I want people to keep more of their earnings, to be sure, but that Keynesian-style explanation overlooks the fact that the additional “spending power” for taxpayers is offset when the government borrows more money to finance the tax cut.

Instead, when thinking about taxes and prosperity, here are the three things you need to know.

1. Economic growth occurs when we increase the quantity and/or quality of labor and capital.

2. Taxes increase the cost of whatever is being taxed, and people respond by doing less of whatever is being taxed.

3. To get more prosperity, lower tax rates on productive behaviors such as work, saving, investment, and entrepreneurship.

All this is completely correct, but there’s one additional point that needs to be stressed.

4. The tax rate that matters is the marginal tax rate, not the average tax rate.

I discussed the importance of marginal tax rates in 2016, pointing out that Cam Newton of the Carolina Panthers was going to lose the Super Bowl (from a financial perspective) because the additional tax he was going to pay was going to exceed the additional income he would earn. In other words, his marginal tax rate was more than 100 percent.

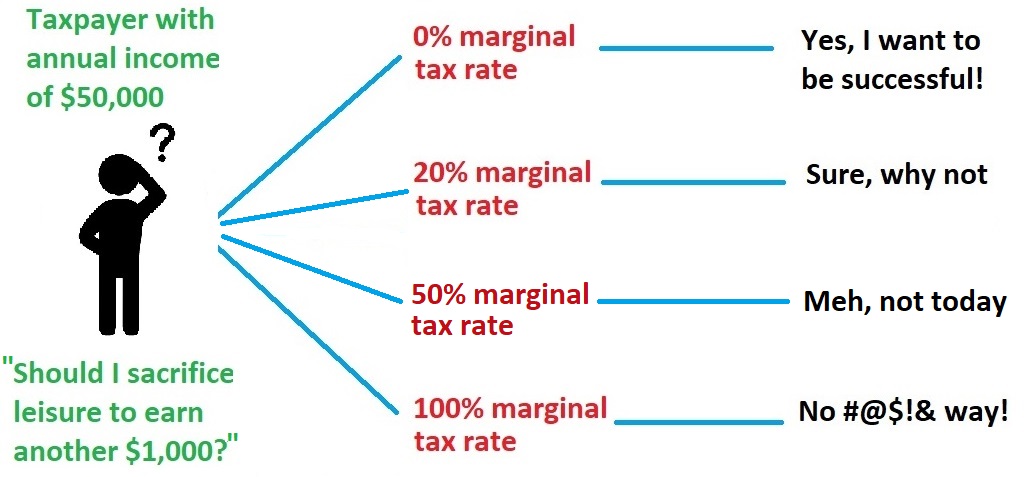

But I also included an example that’s more relevant to the rest of us, looking at our aforementioned hypothetical taxpayer with a 20 percent average tax rate on annual earnings of $50,000. I asked about incentives for this taxpayer to earn more money if the marginal tax rate on additional income was 0 percent, 20 percent, or 100 percent.

Needless to say, as shown in this expanded illustration, the incentive to earn $51,000 will be nonexistent if all of the additional $1,000 goes to government.

That’s why “supply-side economics” is focused on marginal tax rates. If we want more productive behavior, we want the lowest-possible marginal tax rates so people have the greatest-possible incentive to generate more prosperity.

Here’s a very short video primer on this issue.

One very important implication of this insight is that not all tax cuts (or tax increases) are created equal. For instance, as I explained in a three-part series (here, here, and here), there will be very little change in incentives for productive activity if the government gives you a tax credit because you have kids.

But if the government reduces the top tax rate or lowers the tax bias against saving and investment, the incentive for additional productive behavior will be significant.

And this helps to explain why the country enjoyed such positive results from the supply-side changes to tax policy in the 1920s, 1960s, and 1980s.

Let’s close with some good news (at least relatively speaking) for American readers. Compared to other industrialized countries, top marginal tax rates in the United States are not overly punitive.

Let’s close with some good news (at least relatively speaking) for American readers. Compared to other industrialized countries, top marginal tax rates in the United States are not overly punitive.

Admittedly, this is damning with faint praise. Our tax system is very unfriendly if you compare it to Monaco, Hong Kong, or Bermuda.

But at least we’re not France, where there’s a strong argument to be made that the national sport is taxation rather than soccer.

P.S. I’m not saying tax preferences for kids are wrong. But I am saying they’re not pro-growth.

P.P.S. I mentioned above that Cam Newton – based on his personal finances – lost the Super Bowl even before the opening kickoff. Well, there’s scholarly evidence that teams in high-tax states actually win fewer games.

P.P.P.S. Today’s analysis focuses on the individual income tax, but this analysis also applies to corporate taxation. A company with clever lawyers and accountants may have the ability to lower its average tax rate, but the marginal tax rate is what drives the incentive to earn more income. Which is why reducing the federal corporate rate from 35 percent to 21 percent was the best part of last year’s tax bill.