With all the controversy over the failed and costly Obamacare program, it’s understandable that other entitlements aren’t getting much attention.

But that doesn’t mean there aren’t serious problems with Medicaid, Medicare, and Social Security.

Indeed, the annual Social Security Trustees Report was released a few days ago and the updated numbers for the government-run retirement program are rather sobering.

Thanks in part to sloppy journalism, many people only vaguely realize that Social Security is actuarially unsound.

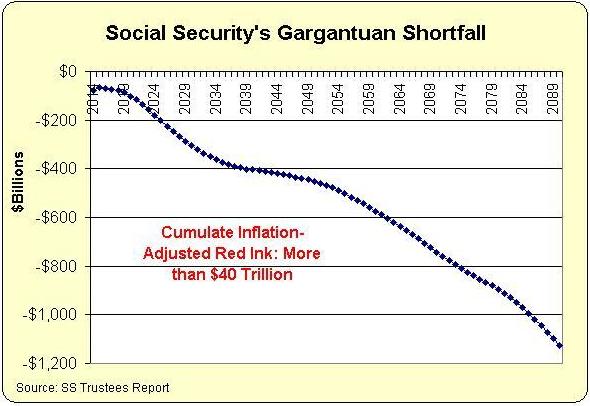

In reality, the level of projected red ink is shocking. If you look at the report’s annual projections and then adjust them for inflation (so we get an idea of the size of the problem based on the value of today’s dollars), we can put together a very depressing chart.

How depressing is this chart? Well, cumulative deficits over the next 75 years will total an astounding $40 trillion. And keep in mind these are inflation-adjusted numbers. In nominal dollars, total red ink will be far more than $150 trillion.

That’s a lot of money even by Washington standards.

Just as worrisome, the trend is in the wrong direction. Last year, the cumulative inflation-adjusted shortfall was $36 trillion. The year before, the total amount of red ink was $30 trillion. And so on.

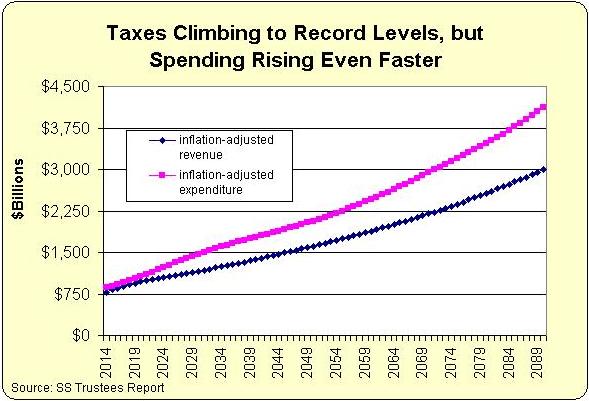

But regular readers know I’m not fixated on deficits and debt. I’m much more worried about the underlying problem of too much spending. So let’s look at the annual data showing how much payroll tax will be generated by Social Security and how much money will be paid out to beneficiaries.

As you can see, the problem is not inadequate tax revenue. Indeed, revenues will climb to record levels. The problem is that spending is projected to increase at an even faster rate.

Once again, don’t forget that these are inflation-adjusted numbers. In nominal dollars, the numbers are far bigger!

Why is the program becoming an ever-larger fiscal burden? The answer boils down to demographics. Simply stated, we will have more and more old people and fewer and fewer younger workers.

So if we do nothing, we’ll be Greece in 20 or 30 years.

That’s not a happy thought, so let’s close on a humorous note. Here’s a joke about how Social Security works, and you can enjoy some Social Security-themed cartoons here, here, and here.

P.S. I’m confident that few people will be surprised to learn that Obama’s supposed solution to this mess involves a huge tax increase.

P.P.S. The real solution is personal retirement accounts. I think Australia is the best role model, but Chile also is a big success.

P.P.S. The good news is that the American people are quite sympathetic to personal retirement accounts.

P.P.P.S. Statists try to scare people by claiming private investments are too risky, but one of my Cato colleagues showed that workers would be better off even if they retired after a stock market crash.

P.P.P.P.S. By the way, Social Security is a really bad deal for blacks and other minorities with lower-than-average life expectancies.

P.P.P.P.P.S. In the interests of fairness, I’ll admit the biggest weakness in the argument for personal accounts is that we might not be able to stop politicians from confiscating the money at some point in the future.

[…] previous years (2012, 2013, 2014), I’ve used this opportunity to play Paul Revere. But instead of warning that the British are […]

[…] That’s why the most appropriate way to measure the shortfall is to take all projected future deficits, adjust them for inflation, and calculate the total. When you do that, the Social Security shortfall is a staggering $40 trillion. […]

[…] That’s why the most appropriate way to measure the shortfall is to take all projected future deficits, adjust them for inflation, and calculate the total. When you do that, the Social Security shortfall is a staggering $40 trillion. […]

[…] main goal, as an American, is to achieve this important reform in the United […]

[…] main goal, as an American, is to achieve this important reform in the United […]

[…] shared lots of data from the Social Security Administration on the depth of the problem, but this cartoon puts it in […]

[…] shared lots of data from the Social Security Administration on the depth of the problem, but this cartoon puts it in […]

The $30 trillion liability is “cash equivalent”. The outstanding $17 trillion in debt of which the $3 trillion is a portion is “cash equivalent”. If you have no problem with “cash equivalence”, you have no problem.

No one is ignoring the 3 trillion. It is invested in what investment professionals call ‘cash-equivlents’. That is a government security with a maturity of less than 30 days. Given that the government security has a redeem option, the maturity is considered less than 30 days.

Why is it that when a private pension buys a government security, it is a cash-equivalent and in your mind it is missing. There are trillions of dollars ‘missing’ from private pensions, and yet no one complains. These pensions buy ‘paper assets’ all the time. Where is the talk about the ‘raids’ on private pensions.

What everyone is ignoring is what these assets are suppose to pay for. The figure is nearly $30 trillion. It makes no difference how $3 trillion is invested. It isn’t going to pay for a $30 trillion dollar bill.

Joe:

You asked “Can you explain to me how someone ‘raids’ a paygo system?”

And then you answered, “The problem is that the first 50 years of retirees did not pay the full cost.” And, “entire excess funding is less than $3 trillion.”

The excess funding which should have been in the Social Security Trust fund is nothing but paper promises, not “real” assets. Sounds like a raid to me! And, I don’t think we should ignore a missing $3 trillion.

Regarding the outstanding liability, most projections go out 75 years, which includes those not yet working. Clearly, we’ll never get there.

Be that as it may, your solution is probably better economically, as are many of the solutions proposed by Dan. My solution is driven by what is politically possible, with the goal of structural change in the short run. Any politician will gladly exchange political suicide in the future for political suicide in the present.

Currently, the top 5% pay about 60% of all tax revenues. I believe that they would be happy to pay 65% of all tax revenues; if tax, welfare, and entitlement systems could be fixed; since they would be the primary beneficiaries. With the economy booming and maximum marginal rates of 25%; that 65% would be paid on a significantly higher gross personal revenues.

Can you explain to me how someone ‘raids’ a paygo system? The system was a paygo system from inception to 1983. It was the mid-90s before there was an substantive money in the system. The entire excess funding is less than $3 trillion which is basically a 1/10th the size of the shortfall. So how did anyone raid $10 for every $1 that is in the system?

Ida Mae Fuller is a single person. She by herself wasn’t a problem, and in fact the original law set-up funding to take care of her. The problem is that the first 50 years of retirees did not pay the full cost.

Here is the problem with your plan for me. These shortfalls were largely created by seniors who didn’t vote well. You want to put the cost of their poor voting upon my generation and the next. Yes, the economy will be better, but the improvement will not remotely get close to what I will lose in terms of benefits. All your proposal does is dumps the cost of dumb voting on someone who had no vote in the discussion.

You say that it will be political suicide to end the system without compensation. I suspect that eventually you will see that it will be political suicide to do nothing. This is an article on the changing demographics of the 3rd Rail. It is not favorable to Social Security.

fedsmith (dot) com/2014/07/30/the-third-rail-is-running-out-of-track/

The first Social Security recipient, Ida Somethingorother paid in about $25 and got back $22,000 (she lived to be over 100). Congress has spent any surpluses.

The system has already been raided. Ending it, without compensation to those who paid in would be political suicide. Some balance needs to be found while exiting.

The transition I propose provides enough time for people to change their saving patterns. The benefit to the productive who will fund the loss, is that the economy will benefit by the increased saving/investment and job opportunities will expand.

[Note that the solution described above is only 60% of my full Entitlement solution, which includes an enhanced prebate/basic income and a “painless tax” to get rid of the capital gains and estate taxes.]

For more watch:

Ned,

If you migrate it, someone is going to get nothing in exchange for funding the system. Whether you fund it with a payroll tax or income tax doesn’t matter. The only difference is the pocket which is picked.

I disagree with you about the must be honored. In one sense you say that one promise must be honored by breaking the promise to another generation. I do not see one set of retirees as more senior in the system. The system needs to serve all retirees.

In terms of raising the age, there is virtually no justification. You are talking about penalizing those who have contributed the most. Even with ‘longer life expectancies’ the group you wish to hurt has a negative return. How can you justify a system which pays-out a positive return to one generation and a negative one to another. Surely you aren’t going to penalize the group that put in the most and takes out the least.

If you are going to end it, just end it. The suggestion that you have asks future worker to pay a lot of existing retirees and get nothing in exchange beyond what they already have – the right to save for their own retirement.

Joe:

I agree that the shift to private accounts will be difficult. It cannot occur in one shot. Instead, we will need a migration path that may take 30-40 years.

Commitments have been made and they must be honored. However, if we were to shift to a flat tax, revenue collection would have to match current taxes including FICA, in order to meet those commitments.

However, this gives us an opening to fix the system. Those already retired are “fully vested” in that they paid FICA throughout their working careers. Those not yet retired are only “partially vested” in the current Entitlements.

I would propose that for every month FICA is not paid the “retirement date” be pushed back 1/3 of a month. Over 30 years, the retirement age would be pushed back to 76+, from the current 66+. [The “+” reflects current planned increases in retirement age.]

Zorba:

Good point on international markets holding down compensation to the productive.

However, as the productive look around for other markets to serve, one of the fastest growing markets will be the elderly and the non-productive, supported by taxes on the productive.

Capitalism is the process of the productive trading services or products for the production of others. Welfare capitalism is the process of trading services to get back the productive resources that were taken by government and given to others. It cannot work.

“Why is the program becoming an ever-larger fiscal burden? The answer boils down to demographics. Simply stated, we will have more and more old people and fewer and fewer younger workers.”

This is simply not true. The problem is that the system was underfunded for nearly 50 years. According to the Trustees, these shortfalls tend to grow over time like a debt with interest. In 2014, the system created 900 billion in broken promises solely because we changed the valuation date from 2012 to 2013. That is more money that the system collected.

Let’s hold worker to retiree ratios aren’t meaningful when the cost of the program is rising for the worker over time. Cost is up as much as 10 fold. The worker to retire ratio in 1950 was something like 16 to 1. Today we have 3 workers contributing 10 times what past workers contributed. If you look at today’s worker to retiree ratio in 1950 terms, we have something like 25 to 40 1950 workers to a retiree. Something else has changed….

Dan, The irony here is that you seriously understate the problem. Five years ago a near majority of voting aged-Americans expected to be completely unaffected by the shortfall. Today more than half of the public expects to retire after the trust fund is gone.

You are critical of sloppy journalism, so I would like to check some of your facts. The Trustees say that the present value of the short fall is 24.9 trillion. Here you say it is 36 trillion. Both numbers are quite large, but it would be helpful to understand why you think that the Trustees are overly conservative.

The data on racial payouts from Social Security dates back to the 1990s if you are looking at the material on the Cato site. That isn’t terribly relevant today because the cashflows have changed so much. Do you have any current research on the subject?

While you suggest that private accounts are better, you aren’t telling people the cost to implement them. It would be roughly 10 trillion dollars spread across benefit cuts and increased taxes. In fact if you plan to protect any class of reitree (66 or above), you will have to increase taxes from today’s levels. When you say that private accounts will do better, does that factor in the higher cost of outside taxes.

The problem with private accounts isn’t risk. It is how much today’s workers will have to contribute to payoff the political bribes of the past.

And… Remember, the budgetary projections implicitly assume young people who are expected to outcompete their peers worldwide (as they have been doing so far) so that the US can maintain its top productivity and thus the calculated revenue actually does materialize. But with American effort-reward curves resembling more and more the rest of the world, it is doubtful that such top competitiveness can be maintained.

[Politicians cannot control the prices the productive will charge for their services, but the international marketplace will exert such control — in the form of American company extinction].

Therefore, there is a vicious cycle on top of the projections which may bring things to a crisis long before the 20-30 year timeframe. Past the tipping point, where American workers become as motivated as workers in other welfare states, things will likely unravel fast for America.

Yet there’s one more vicious cycle on top of that:

As the decline suppresses American standard of living, voter-lemmings will vote themselves even more programs. ObamaCare is just this vicious cycle: Stressed by economic downturn? Get relief by voting ourselves some ObamaCare — to add to social security, Medicare and Medicaid.

It’s a classic death spiral, the death of many civilizations, and I have not seen anything yet in Americans that would tell me they will avoid the decline fate. They seem completely oblivious to the fact that America’s continued prosperity problem is mostly one of flattening effort-reward curves.

If Congress and the Presidents had not “borrowed” (stolen) money from the Social Insecurity fund, and then outright transferred the Social Insecurity fund, it would not be in the condition that it is in now. Of course, none of this can be undone because the federal government is bankrupt. This name has not been officially assigned to the situation, but what else can you call it?

Reblogged this on Public Secrets and commented:

Just a reminder of another fiscal bomb set to go off.

There is a huge misconception about future Social Security and Medicare debt. On a macro level, it is a net zero problem. Money will be taken (taxed) from some citizens and given to other citizens. No non-domestic groups are involved.

That being said, there are two huge micro problems:

1. Money is being taken from the productive [reducing incentive] and given to the unproductive.

2. The money taken reduces savings. Rather than being invested in the private economy the way individual retirement savings accounts would operate, the money is transferred to individuals who will immediately consume. This hurts long term growth.

Me-oh-my what will we do, when the Ponzi Trusts run out of money?

We are reaching a point where the productive will begin to control their own destiny. While the government can force them to fork over a significant portion of their productivity, government cannot control the prices they charge for that productivity.

As a depleting resource, the productive will demand that net pay increase in line with their improved bargaining power. If tax rates are raised, gross pay will have to accelerate even faster and prices will necessarily rise. Social Security recipients will find they are losing ground. If the COLA stays in place, we have the makings of hyper-inflation as each ratchet upward drives the other side higher.

Since the Ponzi Trusts are just paper, this is the real worry, not that the Trust Funds will run out of funny money.