A few days ago, I observed in a television interview that economists are lousy forecasters.

This was not a new revelation. Back in early 2010, I shared a graph that succinctly illustrated why economists shouldn’t be trusted when they make economic forecasts (later that year, I pointed out that macroeconomists were the real problem).

This was not a new revelation. Back in early 2010, I shared a graph that succinctly illustrated why economists shouldn’t be trusted when they make economic forecasts (later that year, I pointed out that macroeconomists were the real problem).

In 2013, I wrote “Don’t Trust Economists, Part II” based on a remarkable example of fraud in Portugal.

Now it’s time for Part III.

We’ll start with a reminder that economists can’t forecast their way out of a wet paper bag. Here’s an excerpt from a 2001 article in the Economist.

As recently as February, 95% of American economists said it wouldn’t happen, but it has. America is now in recession… Even in early September few economists were forecasting a recession. Now it appears that one had already been under way for almost six months.

…Why are recessions so hard to forecast? A study published last year by the International Monetary Fund looked at the economists’ record. It is bad. Of 60 recessions in developed and developing economies during the 1990s, two-thirds remained undetected by consensus forecasts as late as April of the year in which the recessions occurred. In one-quarter of cases, the consensus forecast in October of that year still expected positive growth.

Robert Samuelson has a more recent and comprehensive list of how economists are miserably bad when they try to forecast major economic trends.

The most intriguing and indisputable thing we have learned about economists in recent decades is that they don’t know nearly as much as they thought they knew. …As an economic journalist for roughly half a century, I have slowly and somewhat reluctantly come to the conclusion that many economists (and this applies across the political spectrum) often don’t know what they’re talking about…

Time after time, economists have failed to foresee major economic trends. In recent years, global interest rates have plunged to historically low levels. …But most economists did not anticipate the declines and still can’t fully explain them. Going back a bit further, economists did not predict double-digit inflation (monthly peaks of 12 percent in 1974 and 1975 and 15 percent in 1980). …Now, ironically, inflation has unexpectedly remained low (generally less than 2 percent annually ), and many economists have been baffled by that, too. …Over the past five decades, I cannot remember one instance when economists have correctly forecast a major shift in productivity growth, whether up or down. …Of course, the most conspicuous example of this ignorance gap is the 2008-2009 financial crisis and the Great Recession. “Why did nobody notice it?” Queen Elizabeth famously asked. …The larger cause of the ignorance gap is the very complexity and obscurity of a $20 trillion economy (the United States) or an $85 trillion economy (the world). To say it is changing in detailed and often-unanticipated ways is simply to affirm that mere mortals, including economists, have never been very good at predicting the future.

In other words, this cartoon is very accurate.

So what’s the solution?

In my fantasy world, everyone would simply ignore economic forecasts and instead would focus on the conditions necessary for stronger long-run growth.

Sadly, that won’t happen.

So what about some sort of “quality control”?

That might be nice in theory, but it wouldn’t work in practice.

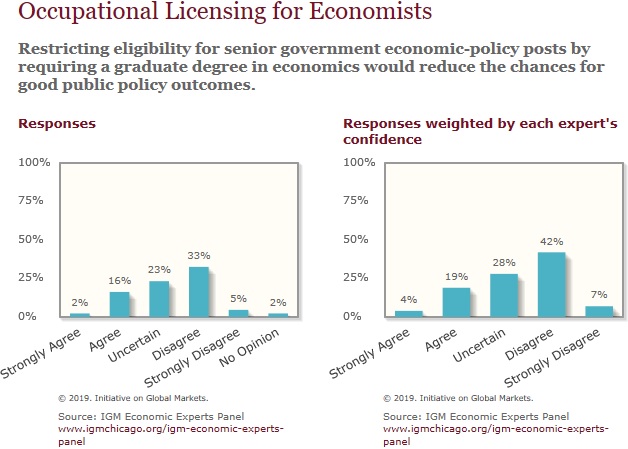

Which is why I’m happy that there isn’t much support in the profession for occupational licensing.

Let’s set aside the problem of economic forecasting.

Binyamin Applebaum of the New York Times has a column that criticizes economists for a different reason.

He frets that economists have enabled a big shift toward free markets.

As the quarter century of growth that followed World War II sputtered to a close, economists moved into the halls of power, instructing policymakers that growth could be revived by minimizing government’s role in managing the economy.

They also warned that a society that sought to limit inequality would pay a price in the form of less growth. …In the four decades between 1969 and 2008, economists played a leading role in slashing taxation of the wealthy and in curbing public investment. They supervised the deregulation of major sectors, including transportation and communications. …they demonized trade unions and opposed worker protections like minimum wage laws.

While I hope his overall premise is accurate, his specific assertions are an incoherent mess.

He wants readers to believe that economists were largely ignored prior to 1969 and suddenly wielded great influence thereafter. Yet he offers zero evidence for that hypothesis.

Moreover, it was Arthur Okun’s work for Brookings (hardly a citadel of libertarian thinking) that increased awareness of the tradeoff between redistribution and growth.

Much more troubling, though, is his assertion that the free-market orthodoxy ruled between 1969-2008.

That’s ahistorical nonsense. The Nixon years, for instance, were probably the most statist period in America’s post-WWII history.

And we also got plenty of bad policy under Bush I, Bush II, and Obama.

Yes, policy did shift in the right direction under Reagan and Clinton. And it’s also quite possible that the progress during those years more than offset the bad policies of other presidents.

But it’s utterly absurd to think of 1969-2008 as an era of continuous economic liberty.

Here are some further excerpts.

Economists even persuaded policymakers to assign a dollar value to human life — around $10 million in 2019 — to assess whether regulations were worthwhile.

This is actually part of life-saving cost-benefit analysis.

And it’s not some sort of libertarian scheme, unless Applebaum thinks the folks at Brookings are part of some laissez-faire conspiracy.

Though I’m glad he gives some credit (from his perspective, blame) to Milton Friedman.

The most important figure, however, was Milton Friedman, an elfin libertarian who refused to take a job in Washington, but whose writings and exhortations seized the imagination of policymakers. Friedman offered an appealingly simple answer for the nation’s problems: Government should get out of the way. He joked that if bureaucrats gained control of the Sahara, there would soon be a shortage of sand.

He concludes by fixating on inequality.

The rise of economics is a primary reason for the rise of inequality. …Markets are constructed by people…and people can change the rules. It’s time to discard the judgment of economists that society should turn a blind eye to inequality. Reducing inequality should be a primary goal of public policy. …Willful indifference to the distribution of prosperity over the last half century is an important reason the very survival of liberal democracy is now being tested by nationalist demagogues. …our shared bonds will last longer if we can find ways to reduce the strain.

If he cares about the well-being of poor people, he should be fixated instead on growth.

For what it’s worth, I suspect he shares the IMF’s perspective and would willing to subject the poor to lower living standards if the rich suffered even bigger losses.

By the way, Ramesh Ponnuru is also quite critical of Applebaum’s column.

Let’s close with some humor.

Professor Michael Munger wrote a column for FEE analyzing economist jokes.

The whole thing is worth reading, but I’ll limit myself to sharing two of the jokes.

An economics graduate student was crossing a road one day when a frog called out to him and said, “If you kiss me, I’ll turn into a beautiful princess.” He bent over, picked up the frog and put it in his pocket. The frog spoke up again and said, “If you kiss me and turn me back into a beautiful princess, I will stay with you for one week.”

The graduate student took the frog out of his pocket, smiled at it, and returned it to his pocket. Desperate, the frog then cried out, “If you kiss me and turn me back into a princess, I’ll stay with you and do anything you want.” Again the grad student took the frog out, smiled at it and put it back into his pocket. Finally, the frog asked, “What is the matter? I’ve told you I’m a beautiful princess, that I’ll be your girlfriend and do anything you want. Why won’t you kiss me?” The grad student said, “Look, I’m an economist. I have no idea what it would even be like to have a girlfriend. But a talking frog has got to be worth a fortune.”

And here’s the second example.

A physicist, a chemist, and an economist are stranded on an island, with nothing to eat. A box washes ashore, and when they open it, it turns out to be a box of canned soup. But how to open the cans? The physicist says, “Let’s break the can open with a rock, using precisely the correct vector of force so the contents aren’t spilled.” The chemist says, “Let’s build a fire and heat the can just to the point where the contents break the metal but don’t explode.” The economist says, “Well, let’s do this in an a priori manner. First, assume that we have a can-opener…”

Last but not least, here’s Adam Smith’s contribution to the game of rock-paper-scissors.

Not as good as my collection of jokes about communism and socialism, but clever is a subtle way.

P.S. Are economists useless, despicable, and loathsome? I report, you decide.