I don’t know whether I’ll live 3 more years or 30 more years.

But I’m increasingly convinced that my “Never-Answered Question” will still be unanswered when I kick the bucket.

But I’m increasingly convinced that my “Never-Answered Question” will still be unanswered when I kick the bucket.

One of the reasons for my confidence is that folks on the left have remarkably shoddy arguments on economic issues.

For instance, in a column for the New York Times, Mehrsa Baradaran condemns the “neoliberal” revolution in the United States.

A law professor from the University of California, Irvine, Ms. Baradaran is unhappy that this modern version of classical liberalism resulted in more economic freedom.

…an ideological coup quietly transformed our society over the last 50 years… The roots of this intellectual takeover can be traced to a backlash against socialism… Austrian School economist Friedrich A. Hayek was perhaps the most influential leader of that movement,

decrying governments who chased “the mirage of social justice.” Only free markets can allocate resources fairly and reward individuals based on what they deserve, reasoned Hayek. The ideology — known as neoliberalism — …leapt from economics departments into American politics in the 1960s, where it fused with conservative anti-communist ideas and then quickly spread throughout universities, law schools, legislatures and courts. By the 1980s, neoliberalism was triumphant in policy, leading to tax cuts, deregulation and privatization.

Since I’m a big fan of Prof. Hayek, I like this part of Professor Baradaran’s column.

And it is true that the United States became more “neoliberal” during the Reagan and Clinton years (though it’s definitely a huge exaggeration to think that pro-market ideas were dominant in “universities, law schools, legislatures and courts”).

to think that pro-market ideas were dominant in “universities, law schools, legislatures and courts”).

Indeed, the entire world moved in the direction of free markets during the last two decades of the 20th century, thanks is part to the “Washington Consensus” for more economic liberty.

Ms. Baradaran, however, does not approve of these developments.

And she specifically doesn’t like some of the folks on Wall Street.

The private equity industry embodies the neoliberal movement’s values, while exposing its inherent logic. Private equity firms use money provided by institutional investors like pension funds and university endowments to take over and restructure companies or industries. …In the last decade, private equity management has led to approximately 1.3 million job losses due to retail bankruptcies and liquidation.

I have no idea whether there’s any validity to the specific estimate of 1.3 million job losses as a result of private equity investors over the past 10 years (an average of 130,000 jobs per year).

But it certainly is true that lots of jobs are lost every year as a result of “creative destruction.” Indeed, 130,000 jobs are just a tiny fraction of the total losses.

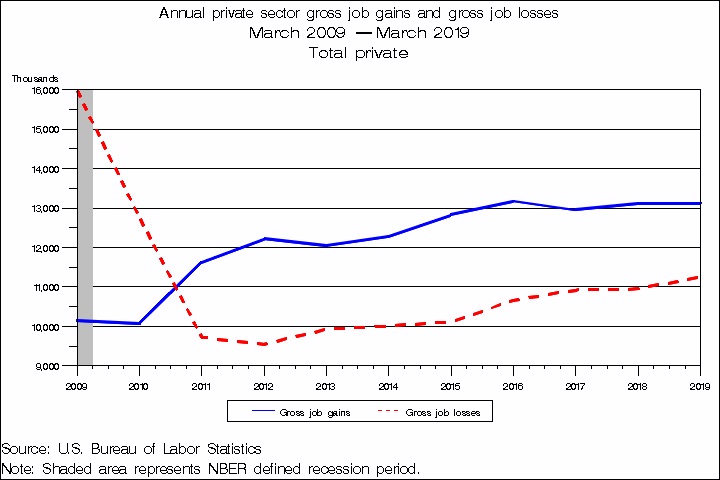

Here’s a chart taken directly from the Bureau of Labor Statistics showing that more than 10 million jobs are lost – on average – every single year.

That’s the bad news.

The good news is that average job gains have been even higher over the past decade, averaging more than 12 million per year.

Call me crazy, but this seems like a ringing endorsement of “neoliberalism.” Especially when you consider that Americans enjoy much higher living standards than their counterparts in European nations with bigger burdens of government.

There are two additional excerpts from her column that merit some attention.

First, she regurgitates the myth that the 2008 financial crisis was caused by free markets and deregulation.

An examination of the recent history of private equity disproves the neoliberal myth that profit incentives produce the best outcomes for society. …Faith in market magic was so entrenched that even the 2008 financial crisis did not fully expose the myth: We witnessed the federal government pick up all the risks that markets could not manage and Congress and the Federal Reserve save the banking sector ostensibly on behalf of the people. Neoliberal deregulation was premised on the theory that the invisible hand of the market would discipline risky banks without the need for government oversight.

At the risk of understatement, the Federal Reserve, along with Fannie Mae and Freddie Mac, deserve the lion’s share of the blame.

Also, she closes her column by embracing genuine socialism (i.e., government owning and operating parts of the economy).

Federal or state agencies can provide essential services like banking, health care, internet access, transportation and housing at cost through a public option. …we can move beyond the myths of neoliberalism…we should choose flourishing communities over profits.

At the risk of understatement, I don’t want more of our economy to be like the Post Office or DMV. I prefer private businesses, which face pressure to please consumers, rather than government-run businesses, which care mostly about pleasing politicians.

And I also think Ms. Baradaran needs a lesson from Walter Williams so she learns that profits make flourishing communities possible.

{kind=link}