My crusade against the border-adjustable tax (BAT) continues.

In a column co-authored with Veronique de Rugy of Mercatus, I explain in today’s Wall Street Journal why Republicans should drop this prospective source of new tax revenue.

…this should be an opportune time for major tax cuts to boost American growth and competitiveness. But much of the reform energy is being dissipated in a counterproductive fight over the “border adjustment” tax proposed by House Republicans. …Republican tax plans normally receive overwhelming support from the business community. But the border-adjustment tax has created deep divisions. Proponents claim border adjustability is not protectionist because it would automatically push up the value of the dollar, neutralizing the effect on trade. Importers don’t have much faith in this theory and oppose the GOP plan.

Much of the column is designed to debunk the absurd notion that a BAT is needed to offset some mythical advantage that other nations supposedly enjoy because of their value-added taxes.

Here’s what supporters claim.

Proponents of the border-adjustment tax also are using a dodgy sales pitch, saying that their plan will get rid of a “Made in America Tax.” The claim is that VATs give foreign companies an advantage. Say a German company exports a product to the U.S. It doesn’t pay the American corporate income tax, and it receives a rebate on its German VAT payments. But an American company exporting to Germany has to pay both—it’s subject to the U.S. corporate income tax and then pays the German VAT on the product when it is sold.

Sounds persuasive, at least until you look at both sides of the equation.

When the German company sells to customers in the U.S., it is subject to the German corporate income tax. The competing American firm selling domestically pays the U.S. corporate income tax. Neither is hit with a VAT. In other words, a level playing field.

Here’s a visual depiction of how the current system works. I include the possibility that that German products sold in America may also get hit by the US corporate income tax (if the German company have a US subsidiary, for instance). What’s most important, though, is that neither American-produced goods and services nor German-produced goods and services are hit by a VAT.

Now let’s consider the flip side.

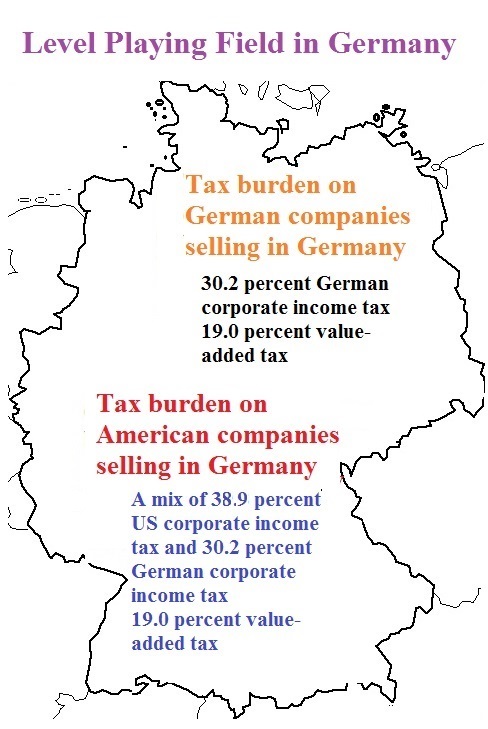

What if an American company sells to a customer in Germany? The U.S. government imposes the corporate income tax and the German government imposes a VAT. But guess what? The German competitor selling domestically is hit by the German corporate income tax and the German VAT. That’s another level playing field. This explains why economists, on the right and left, repeatedly have debunked the idea that countries use VATs to boost their exports.

Here’s the German version of the map. Once again, I note that it’s possible – depending on the structure of the US company – for American products to get hit by the German corporate income tax. But the key point of the map is to show that American-produced goods and services and German-produced goods and services are subject to the VAT.

By the way, it’s entirely possible that an American company in Germany or a German company in America may pay higher or lower taxes depending on whether there are special penalties or preferences. Those companies may also pay more or less depending on the cleverness of their tax lawyers and tax accountants.

But one thing can be said with total certainty: The absence of an American VAT does not result in a “Made-in-America” tax on American companies. Even Paul Krugman agrees that VATs don’t distort trade.

Moreover, Veronique and I point out that the lack of a VAT creates a big advantage for the United States.

One big plus for Americans is that Washington does not impose a VAT, which would enable government to grow. This is a major reason that the U.S. economy is more vibrant than Europe’s. In Germany, the VAT raises so much tax revenue that the government consumes 44% of gross domestic product—compared with 38% in America.

And to the extent that there is a disadvantage, it’s not because of some sneaky maneuver by foreign governments. It’s because of a self-inflicted wound.

America’s top corporate income tax of 35% is the highest in the developed world. If state corporate income taxes are added, the figure hits nearly 40%, according to the Congressional Budget Office. That compares very unfavorably with other nations. Europe’s average top corporate rate is less than 19%, and the global average is less than 23%… That’s the real “Made in America Tax,” and it’s our own fault.

The column does acknowledge that BAT supporters have their hearts in the right place. They are proposing that new source of revenue to help finance a lower corporate tax rate, as well as expensing.

But there’s a much better way to enable those pro-growth reforms.

If Congress simply limits the growth of outlays to about 2% a year, that would create enough fiscal space to balance the budget over 10 years and adopt a $3 trillion tax cut. If Republicans want a win-win, dropping the border-adjustment tax is the way to get one.

And what if Republicans aren’t willing to restrain spending? Then maybe the sensible approach is to simply cut the corporate tax rate and declare victory.

[…] but not least, I can’t resist pointing out that Morici is flat wrong about the VAT and trade. Heck, even Paul Krugman agrees with me on that […]

I’m going to have to display some ignorance here with a question:

Is there a difference between selling “to” the United States as opposed to selling “in”?

In other words, if the seller is a foreign company and makes a sale to a US company, who then uses or re-sells the item – is by virtue of the sale the profits from the sale subject to the US corporate income tax? Or, if the foreign company never sets up a business in the US, but merely sells to US corporations, is that one way of shielding those profits from the US tax?

If it’s the latter (and based on my experience I think it is), then your argument is somewhat misleading. Sure, Honda or Toyota with their US Divisions pay the corporate tax on sales that they make into the US, but their direct sales from Japan to the US (not going through their US operations – i.e. to re-sellers like Home Depot or Amazon) might not be subject to that tax.

So there would be an advantage to VAT vs. non-VAT in that case.

There even might be some room for gaming sales into the US – let their US divisions sell at a loss, with the sale into the US (e.g. from Honda, Japan to Honda, USA) being at a higher price than the cost of the sale inside the US – so Honda, USA runs at a loss but then gets influxes of funding from Honda, Japan. Not sure if that would be legal – but to the extent it is – the room for gaming is tremendous.

And certainly sales of input goods – aluminum, steel, rubber, etc. – into the US wouldn’t seem to have the corporate tax on them.

(Note, I’m no fan of any tariff on inputs/materials/food, irrespective of dumping – too many downstream impacts – the dumping just makes our higher value industries more profitable; better to subsidize our own industries if there is a national-security related interest in keeping US production capabilities alive.)

Honestly, I’m no fan of taxes on business profits at all – too much room for gaming. I think Ted Cruz’s plan of a VAT-like (but non-VAT)annualized tax on all business receipts, with a limited set of deductions, would be a much better way for the US to go. Save money on tax gaming, much lower, more standardized tax. Plenty of U.S. cities have such taxes (e.g. Philadelphia).

E.g. a 3-4% business receipts tax in place of the corporate tax, with the choice between a $500,000 in sales standard deduction and itemized deductions limited to: 1) wages for US labor (up to, say, $1M per employee to appease liberals a bit); 2) health care subsidies for US labor, up to a cap, say $15K per employee of subsidy – but maybe with a multiple for the deduction (1.5? 1.25?) to incentivize provision of health insurance; 3) retirement subsidies (with a similar cap and potential multiple on tax deduction to incentivize 401K matching, etc.); and 4) 10 year depreciation of “permanent/hard” investments into the US (machinery, buildings, etc.). Maybe a couple more – but not much. It would also not exempt “not for profits” or “charities” – eliminating one more route for tax evasion.

This would make things so much simpler than the current system, and simplicity in rules itself has powerful pro-growth implications….

“If Congress simply limits the growth of outlays to about 2% a year, that would create enough fiscal space to balance the budget over 10 years and adopt a $3 trillion tax cut. If Republicans want a win-win, dropping the border-adjustment tax is the way to get one.”

Two lies in one sentence….

Congress can’t limit growth in entitlement spending (SS, Medicare, Medicaid, etc.) to 2%. And entitlement spending makes up 70% of the budget.

Also, what they left out of the above is that limiting growth in outlays only balances the “Discretionary” portion of the budget.

Hopefully one day Daniel will write an article addressing this false claim and the other big one; “Officialy” in FY 2016 (as reported by the news media) the National debt up only went up $578 billion while actually it went up some $1.4 Trillion as reported on the treasury website National Debt to the Penny !!!!!

I think it’s consumers who ultimately pay VATs anyway, not businesses.

It’s got nothing to do with favoring one countries products over another’s, consumption taxes are just a simple blanket approach to collecting tax revenues.

Germany?? Why not China or Vietnam or Brazil.

Some explanations about the numbers in the article for people who are interested:

Germany has a federal corporate tax rate of 15 % plus 5.5 % of those 15 % (that would be about .9 %) as a special tax to finance certain costs associated with Germany’s reunification. It sums up to roughly 15.9 %.

So what about the 30.2 % mentioned in the article? Local municipalities (cities, towns and sometimes counties) can add a local corporate tax in addition to the federal corporate tax. Obviously the tax rate can vary widely from town to town (actually the highest local corporate tax is 4.5 times higher than the lowest one). So 30.2 % is just an overall average. German companies can influence their corporate tax burden significantly by choosing the right place for their HQ and production sites.

VAT laws are the same in all EU member countries. But the VAT rate varies from country to country. Germany has a general VAT rate of 19 %. But a long list of goods and services fall into another category. Most notably most food products as well as printed goods (books, newspapers, magazines, but not ebooks) are taxed 7 % VAT. Certain other things like medical services provided by doctors or banking services are not taxed at all.

Unlike in the U.S. all consumer prices in Germany are gross. They already contain VAT. As a consumer you see on the label the price including VAT. Comfortable but also a good way to hide taxes from the mind of the consumer. B2B deals on the other hand are always net. Prices do not include VAT. Nevertheless the business customer has to pay VAT. When a business uses the aquired goods and services for their business it will get refunded the payed VAT by the German IRS. The goal is that only a private consumer at the end of the supply chain actually pays the VAT.