The standard argument against an easy-money policy is that it creates distortions in an economy that lead to either rapid increases in the price level, like we endured in the 1970s, or unsustainable asset bubbles, like we experienced last decade.

Those arguments are completely valid, but they only tell part of the story.

Central banks also should be criticized because “quantitative easing” and “zero interest rate policies” create major imbalances in capital markets.

A major new study from Swiss Re quantifies the damage to savers. Here are some excerpts from a CNBC report.

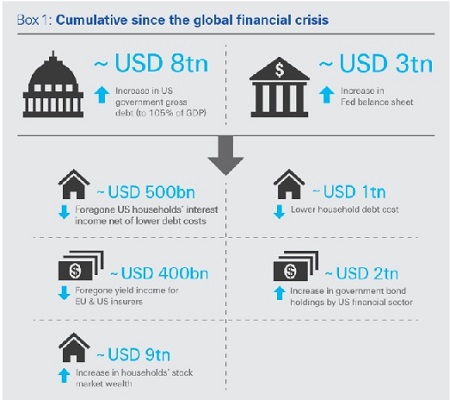

The Federal Reserve’s efforts to stimulate the U.S. economy after the financial crisis ended up costing savers nearly half a trillion dollars in interest income, according to report released Thursday. Since the central bank dropped interest rates to near zero at the end of 2008, savers have labored under plain-vanilla bank accounts and money market funds that have yielded close to nothing. …In a landmark report, Swiss Re quantifies just how much savers and others have languished… The reinsurance firm put the number at $470 billion in the 2008-13 period studied, so the number is likely even higher now. …”the impact of foregone interest income for households and long-term investors has become substantial.” …Swiss Re said the “financial repression” has taken its toll not only on savers but also on some areas of investing.

Here’s a chart from the Swiss Re report. As you can see, an easy-money policy is a massive tool for redistribution, with savers being hurt and government being subsidized.

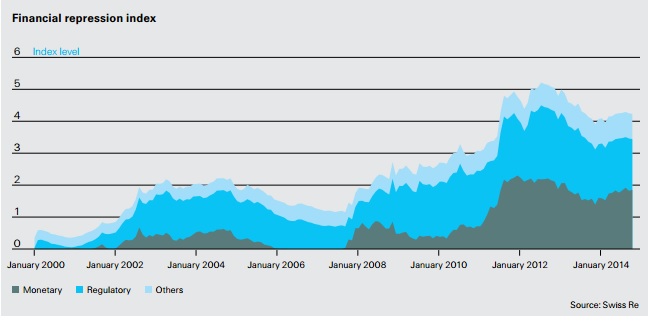

Indeed, Swiss Re actually calculates a “financial repression index.”

Financial repression reflects the ability of policymakers to direct funds to themselves that would otherwise go elsewhere.

And the level of this repression has been at record highs in recent years.

It is true that some households benefit from easy money and artificially low interest rates. Their debt expenses have been reduced and they also are enjoying higher asset values.

But those benefits may be fleeting if the end result is a bubble that bursts, as happened in 2008.

Writing for the Washington Times, my Cato colleague Richard Rahn agrees that central banks are hurting savers, but he augments this analysis by making the very important point that easy-money policies simply don’t work.

Government economic policymakers have been trying to solve a problem of too much government spending, taxing and regulation by inappropriately using monetary policy, which has not and cannot solve the fundamental problems (it is like using a hammer rather than a shovel to dig a hole). The major central banks have been holding down interest rates, which is actually a massive indirect tax levied on the world’s savers. Historically, savers would receive about 3 percent interest above the rate of inflation on their safest investments, but now interest rates often do not cover even the low inflation that is occurring in the developed countries. …Many economists expected savers to save less and consume more as a result of low or even negative interest rates… When businesses and individuals look at the world debt situation and the increased chances of another financial collapse, their rational response is to increase “precautionary” savings, even though they are not receiving interest on them.

So the bottom line is that central banks are engaging in “financial repression” today and creating risks of price instability and/or asset bubbles tomorrow.

But there’s no compensating benefit to make all these costs (and future risks) worthwhile.

That’s not a good deal.

So what’s the alternative?

In the short run, the best hope is that central bankers, including the ones at the Federal Reserve, will take their feet off the figurative gas pedal and follow some sort of monetary rule that precludes destructive intervention.

In the long run, the ideal answer would be a return to market-provided private currencies. This isn’t just silly libertarian fantasy. There actually have been countries that successfully used this “free banking” approach.

Professor Larry White has a must-read historical review of what happened before governments monopolized currency issue.

When we look into these episodes, we find a record of innovation, improvement, and success at serving money-users. As in other goods and services, competition provided the public with improved products at better prices. The least regulated systems were not only the most competitive but also by and large the least crisis-prone. …the record of these historical free banking systems, “most if not all can be considered as reasonably successful, sometimes quite remarkably so.”…Those systems of plural note issue that were panic prone, like those of pre-1913 United States and pre-1832 England, were not so because of competition but because of legal restrictions that significantly weakened banks. Where free banking was given a reasonable trial, for example in Scotland and Canada, it functioned well for the typical user of money and banking services.

The history of central banking, by contrast, is not nearly as successful. There’s been massive erosion in the value of money and central banks are largely responsible for the boom-bust cycle that has afflicted many economies.

At this point, you may be wondering why central banking triumphed over free banking if the latter is so superior.

The answer is simple. As Professor White explains, look at what’s in the best interest of the political elite.

Free banking often ended because the imposition of heavy legal restrictions or creation of a privileged central bank offered revenue advantages to politically influential interests. The legislature or the Treasury can tap a central bank for cheap credit, or (under a fiat standard) simply have the central bank pay the government’s bills by issuing new money. …Central banks primarily arose, directly or indirectly, from legislation that created privileges to promote the fiscal interests of the state or the rent-seeking interests of privileged bankers, not from market forces.

In other words, a system of competitive currencies is perfectly plausible, but it’s not in the interest of politicians (just as having no income tax is plausible, but also not in the interest of politicians).

For more information on free banking, here’s a video I narrated for the Center for Freedom and Prosperity.

Professor White also has a good video explaining why a central bank isn’t needed.

P.S. For those of you who like the gold standard, Professor George Selgin (now head of Cato’s Center for Monetary and Financial Alternatives) has some major concerns (at least if the government is in charge of it).

P.P.S. Don’t forget that the Federal Reserve also imposes a lot of costly regulation on the financial sector.

P.P.P.S. Thomas Sowell has some wise observations on why we shouldn’t grant more power to the Fed and John Stossel explains why monetary competition would be good.

P.P.P.P.S. To end with some humor, here’s the famous “Ben Bernank” video. And if that doesn’t exhaust your interest in the topic, here’s a snarky cartoon video mocking the Fed and another video with 10 reasons to dislike the Fed.

[…] but that will be offset by declines in other prices. Unless, of course, the central bank is creating too much liquidity, thus enabling an increase in the overall price […]

[…] but that will be offset by declines in other prices. Unless, of course, the central bank is creating too much liquidity, thus enabling an increase in the overall price […]

[…] basic message is that Biden ignored the real cause of inflation (bad monetary policy by the Federal Reserve) and instead came up with ideas (either bad or irrelevant) to addresses the […]

[…] basic message is that Biden ignored the real cause of inflation (bad monetary policy by the Federal Reserve) and instead came up with ideas (either bad or irrelevant) to addresses the […]

[…] basic message is that Biden ignored the real cause of inflation (bad monetary policy by the Federal Reserve) and instead came up with ideas (either bad or irrelevant) to addresses the […]

[…] the central bank also should be criticized for interfering with the allocation of credit. And financial repression as […]

[…] the central bank also should be criticized for interfering with the allocation of credit. And financial repression as […]

[…] the notion of “financial repression” since that’s a government policy that has a very direct adverse effect on people trying to build […]

[…] of course, that today’s rising prices are partly or even mostly transitory. But, given the easy-money policy we’ve had (including under Trump), it’s perhaps more likely that prices are going up as an inevitable […]

[…] you’re interested in this topic (and you should be), I shared some very worrisome analysis back in […]

[…] not a big fan of the Federal Reserve, mostly because of its Keynesian monetary […]

[…] Street can be blamed on Trump’s protectionist policies and statement (the Federal Reserve should be blamed for creating a fragile market with easy-money policies). But a trade war could […]

[…] are good reasons to reconsider the Federal Reserve, and we definitely should be angry about the perverse redistribution enabled by Fed […]

[…] are good reasons to reconsider the Federal Reserve, and we definitely should be angry about the perverse redistribution enabled by Fed […]

[…] are good reasons to reconsider the Federal Reserve, and we definitely should be angry about the perverse redistribution enabled by Fed […]

[…] Sowell is right. Don’t reward a bureaucracy’s poor performance by giving it even more […]

[…] I also recommend this column and this column for further information on how central bankers are endangering […]

[…] Street can be blamed on Trump’s protectionist policies and statement (the Federal Reserve should be blamed for creating a fragile market with easy-money policies). But a trade war could be the trigger that […]

[…] Easy money is also a tool for “financial repression,” which occurs when governments surreptitiously confiscate money from […]

[…] Moreover, it’s a good idea to be skeptical about the Federal […]

[…] Moreover, it’s a good idea to be skeptical about the Federal […]

[…] a very important issue. Indeed, if I was to pick the greatest risk to the economy, it’s that easy-money policies (such as artificially low interest rates) have created a bubble. And bursting bubbles can be very […]

[…] if the stock market is artificially inflated because of the Fed’s easy-money policy? If that’s the case, there almost certainly will be a correction and stock values will […]

[…] He’s right. The rich disproportionately benefit from rising asset values, while the rest of us suffer because of low interest rates on our savings accounts (though the rich may regret such policies if the result is a bubble that eventually bursts). […]

[…] He’s right. The rich disproportionately benefit from rising asset values, while the rest of us suffer because of low interest rates on our savings accounts (though the rich may regret such policies if the result is a bubble that eventually bursts). […]

[…] in Washington is sitting on their collective hands. The folks at the Federal Reserve have been trying to goose the economy with an easy-money […]

[…] in Washington is sitting on their collective hands. The folks at the Federal Reserve have been trying to goose the economy with an easy-money […]

The really big advantage for governments is that low interest rates lower their interest costs – that’s what happened to Greece and why it’s now in such a mess. The answer is to take control away from the politicians who like having their hands in the cookie jar.

The fear they give of deflation being terrible is not necessarily true. Aren’t there two sorts of deflation? (just as there are two main types of inflation – general and specific). It would be great if you could persuade Professor George Selgin to write an article explaining the difference, he had a great explanation in the hour long video you posted a while ago…

[…] For more information on free banking, here’s a video I narrated for the Center for Freedom WAIT, THERE’S MORE… […]