Whether at the federal level, state level, or local level, my biggest problem with bureaucrats is that many of them work for agencies and departments that should not exist.

My second biggest problem is that they are overpaid compared to workers in the productive sector of the economy.

And I could add other concerns, such as bureaucrat misbehavior, negative macroeconomic effects, and bureaucratic sloth.

But for today’s column, let’s focus on the narrower issue of pensions for state bureaucrats. But we’re not only going to be examining the overly generous guaranteed benefits that politicians have promised.

Those numbers are important. But, courtesy of Reason‘s Pension Integrity Project, we’re also going to see whether politicians have actually set aside the amount of money needed to fund those benefits.

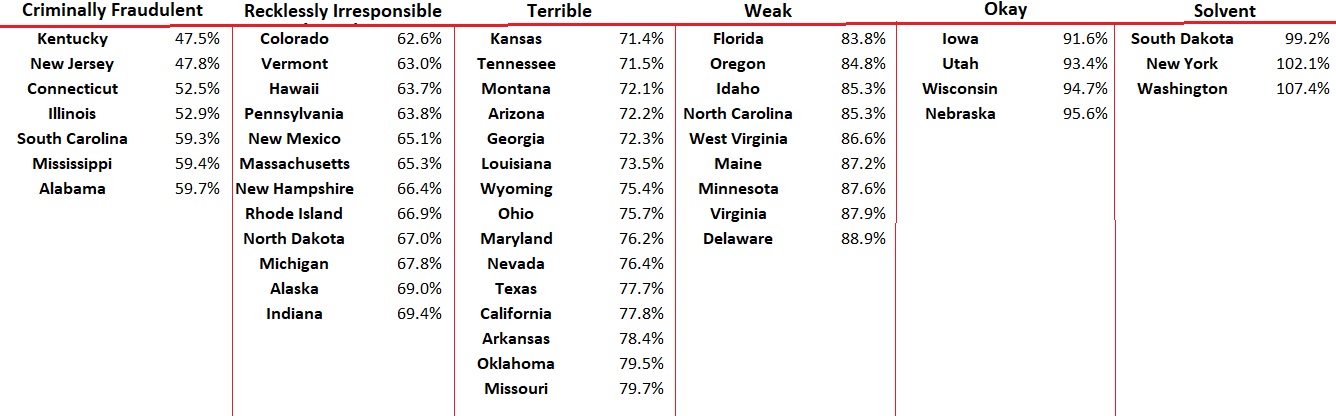

I put Reason‘s numbers into categories to see which states were saddling their residents with future problems (often referred to as unfunded liabilities).

What do we see? Lo and behold, only three states have solvent systems, with four others being in decent shape.

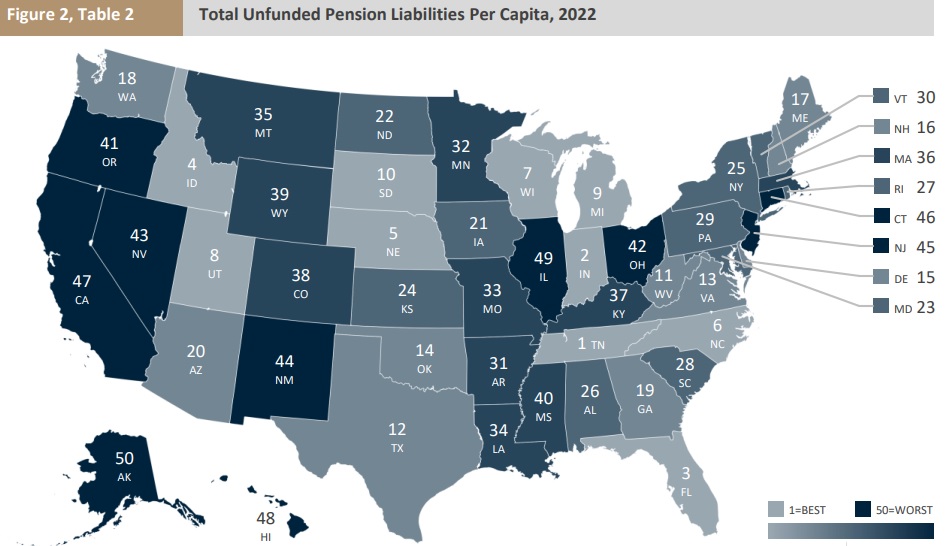

However, to properly assess the future danger to taxpayers, it’s also necessary to know the relative size of state pension plans.

For instance, if a state does not offer a lot of guaranteed benefits, then the future burden on taxpayers won’t be that large, even if the state hasn’t set aside the money to pay those benefits.

Which is why it’s also important to look at unfunded liabilities per capita. Here are those calculations, courtesy of the folks at the American Legislative Exchange Council.

Measured this way, Tennessee, Indiana, and Florida are in the best shape, even though they don’t look good in the Reason report.

Let’s conclude by seeing what states are in the top-10 and bottom-10 of both reports.

On this basis, the best states are South Dakota, Utah, Wisconsin, and Nebraska.

The worst states (to nobody’s surprise) are New Jersey, Connecticut, Illinois, Hawaii, and Mississippi.

[…] in many cases, they haven’t set aside enough money to fulfill those […]

[…] in many cases, they haven’t set aside enough money to fulfill those […]

graph after graph, table after table, color-coded map after color-coded map: I’m wondering why the heck I moved to Georgia. 😦

I would also consider if they are a sate loosing business and population or gaining businesses and population. Good stuff.

Public sector pensions need to be reformed, primarily because states that default on their pensions will seek (and probably receive) a bailout from the federal government. Here’s a good starting point:

1. The federal government should agree to provide a backstop to state and local pensions and guarantee pensions up to the level that private pensions are guaranteed by the Pension Benefit Guaranty Corporation ($81,000 for a 65 year old, $36,450 for a 55 year old, and $20,250 for a 45 year old).

2. In exchange for this guarantee, the state and local governments have five years to fund their pension funds and at the end of five years must reduce pensions to the funded portion. For instance, if a pension fund is only 60% funded today, the state has five years to become fully funded (which, of course, will result in higher taxes and/or reduced services). Just to be clear, if the pension fund was 80% funded at the end of year 5, all pensions (past and future) would be reduced by 20%. After year five, pensions will be adjusted year-to-year to match the percentage that they’re funded. Even with the guarantee, states will be required to continue funding the pensions–they just can’t walk away.

3. The guarantee will be available only to states that agree to both conditions. The rest of the states are on their own. Some states apparently have “constitutional” guarantees that pensions can’t be reduced (undoubtedly drafted by the public sector unions). Oops. Too bad. You don’t get the guarantee.

Let’s see how much the 90% of taxpayers who don’t get the gold plated public sector pensions want to sacrifice to keep intact promises made by corrupt politicians to public sector unions (my bet would be that pension funds are underfunded precisely because the cost of full funding would result in the tarring and feathering of the politicians who made promises without the ability to keep them). People need to wake up to the reality that their political overlords have bought current labor peace by making unfunded promises that will soon become due.

I have little sympathy for the public sector employees. Rather than trading for higher pensions and more generous pay and benefits, they should have required their leaders to ensure that pension promises were fully funded. The whole scheme is fraudulent to the point where it should be criminal.

Something that can’t go on–won’t. The only issue is how wee dig ourselves out of the hole we’re in at minimal cost to the responsible states. I suspect that there will be limited enthusiasm in Florida to bail out Illinois and New Jersey.