A couple of days ago, I wrote about the new rankings from the World Economic Forum’s Global Competitiveness Report and noted that America’s private sector is considered world class but that our public sector ranks poorly compared to many other developed nations.

To elaborate on the depressing part of that observation, let’s now look at the Tax Foundation’s recently released International Tax Competitiveness Index.

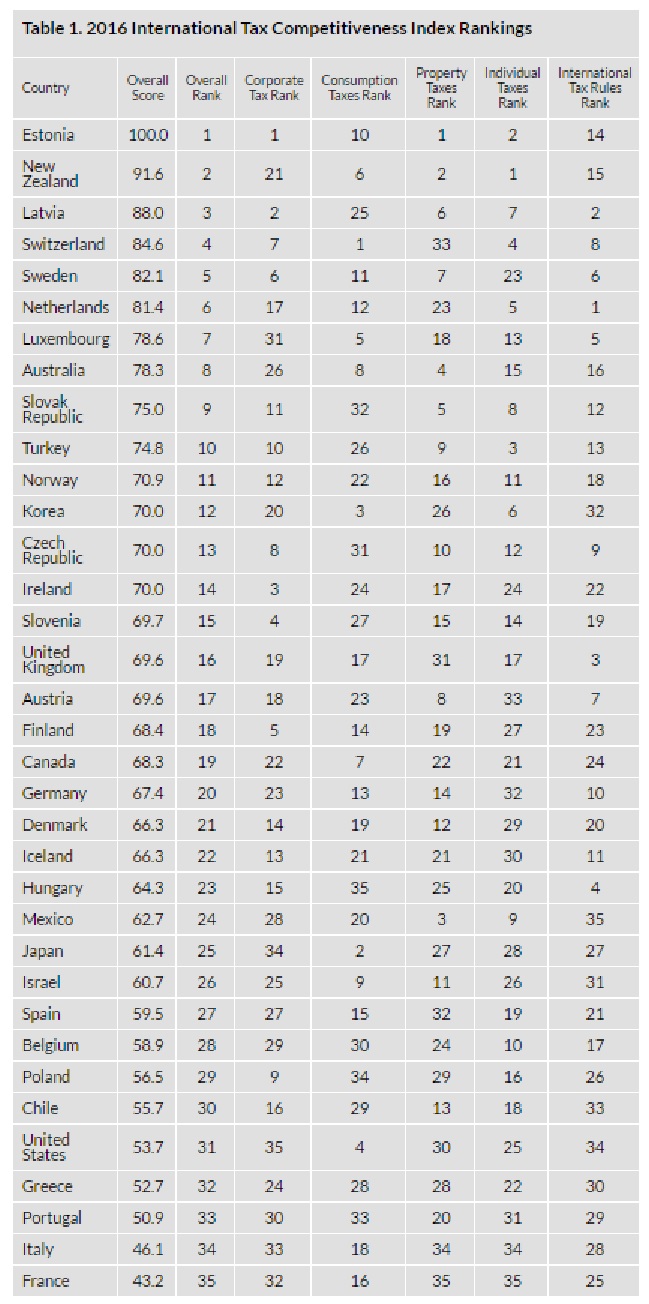

Lots of data and lots of countries. Estonia gets the top score, and deservedly so. It has a flat tax and many other good policies. It’s also no surprise to see New Zealand and Switzerland near the top.

If you’re curious about America’s score, you’ll have to scroll way down because the United States ranks #31, below even Belgium, Spain, and Mexico.

If you look at how the U.S. ranks in the various categories, we have uniformly poor numbers for everything other than “Consumption Taxes.” So let’s be very thankful that the United States doesn’t have a value-added tax (VAT). If we did, even France would probably beat us in the rankings (I hope Rand Paul and Ted Cruz are paying attention to this point).

And if you wonder why some nations with higher top tax rates rank above the U.S. in the “Individual Taxes” category, keep in mind that there are lots of variables for each category. And the U.S. does poorly in many of them, such as the extent to which there is double taxation of dividends and capital gains.

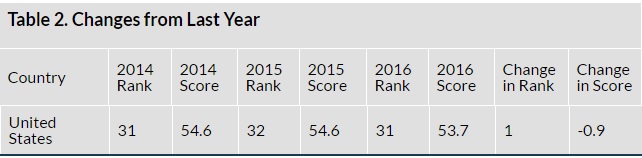

By the way, there is some “good” news. Compared to the 2014 ranking, the United States is doing “better.” Back then, there were only two nations with lower scores, Portugal and France. In the new rankings, the U.S. still beats those two nations, and also gets a better score than Greece and Italy.

But we’re only “winning” this contest of weaklings because the scores for those nations are falling faster than America’s score.

Here’s the 2014-2016 data for the United States. As you can see, we’ve dropped from 54.6 to 53.7.

P.S. The Tax Foundation’s International Tax Competitiveness Index is superb, but I hope they make it even better in the future by adding more jurisdictions. As of now, it only includes nations that are members of the OECD. That’s probably because there’s very good and comparable data for those countries (the OECD pushes very bad policy, but also happens to collect very detailed numbers for its member nations). Nonetheless, it would be great to somehow include places such as Hong Kong, Singapore, Bermuda, and the Cayman Islands (all of which punch way above their weight in the international economy). It also would be desirable if the Tax Foundation added an explicit size-of-government variable. Call me crazy, but Sweden probably shouldn’t be ranked #5 when the nation’s tax system consumes 50.4 percent of the economy’s output (this size-of-government issue is also why I asserted South Dakota should rank above Wyoming in the Tax Foundation’s State Business Tax Climate Index).

[…] United States ranked #22, which is bad but not as bad as it used to be. Kudos to the Baltic nations, as well as New Zealand and Switzerland. Sympathy for the mistreated […]

[…] “improbable success” of Estonia once again ranks #1. Just like in 2021, 2020, 2019, etc, […]

[…] “improbable success” of Estonia once again ranks #1. Just like in 2021, 2020, 2019, etc, […]

[…] the United States had been scoring near the bottom, year after year, before the Trump tax reform bumped America up to #21. So there was some […]

[…] the United States had been scoring near the bottom, year after year, before the Trump tax reform bumped America up to #21. So there was some […]

[…] the United States had been scoring near the bottom, year after year, before the Trump tax reform bumped America up to #21. So there was some […]

[…] the United States had been scoring near the bottom, year after year, before the Trump tax reform bumped America up to #21. So there was some […]

[…] the United States had been scoring near the bottom, year after year, before the Trump tax reform bumped America up to #21. So there was some […]

[…] to make matters simple, we can just copy Estonia, which has the world’s best system according to the Tax […]

[…] But let’s look at the glass as being half full rather than half empty. When the Tax Foundation launched this publication back in 2014, the United States was a lowly #32 out of 34 nations. And we were still mired near the bottom in 2016, ranked #31 out of 35 countries. […]

[…] Tax Foundation churns out lots of good information, but I especially look forward to their International Tax Competitiveness […]

[…] the way, I don’t think this Index is a perfect measure. As I pointed out back in 2016, it needs to include a size-of-government […]

[…] Tax Foundation’s State Business Tax Climate Index, which is sort of the domestic version of their equally fascinating (to a wonk) International Tax Competitiveness […]

[…] Foundation’s State Business Tax Climate Index, which is sort of the domestic version of their equally fascinating (to a wonk) International Tax Competitiveness […]

[…] Most anti-competitive tax system. […]

[…] And the recent tax plan only took a small step in that direction. How small? Well, the Tax Foundation just calculated that it only improved the United States from #30 to #25 in their International Tax Competitiveness Ranking. In other words, we have a long way to go before we catch up to Estonia. […]

[…] is so good (particularly its approach to business taxation) that the Tax Foundation ranks it as the best in the OECD. …Estonia…may be my favorite Baltic nation if for no other reason than the humiliation […]

[…] Congress and the White House decide to go for a more targeted tax cut, such as a big reduction in the corporate income tax (which would be a significant victory). […]

[…] Congress and the White House decide to go for a more targeted tax cut, such as a big reduction in the corporate income tax (which would be a significant victory). […]

[…] Congress and the White House decide to go for a more targeted tax cut, such as a big reduction in the corporate income tax (which would be a significant victory). […]

[…] Congress and the White House decide to go for a more targeted tax cut, such as a big reduction in the corporate income tax (which would be a significant victory). […]

[…] to make matters simple, we can just copy Estonia, which has the world’s best system according to the Tax […]

[…] certainly a more libertarian approach. Maybe we could, too, if America didn’t have virtually the most anti-competitive tax regime in the entire industrialized […]

[…] to make matters simple, we can just copy Estonia, which has the world’s best system according to the Tax […]

[…] to make matters simple, we can just copy Estonia, which has the world’s best system according to the Tax […]

[…] One key to their relative success is tax policy. All three nations have flat taxes. Estonia’s system is so good (particularly its approach to business taxation) that the Tax Foundation ranks it as the best in the OECD. […]

[…] spending under control? The case for unilateral free trade. How we lost economics. Dan Mitchell on America’s terrible tax system. The week in review from the Mises Institute. My friend Pete Klein says some favourable things […]

[…] Dan Mitchell. Can Brazil get spending under control? The case for unilateral free trade. How we lost economics. Dan Mitchell on America’s terrible tax system. […]

Dan

By now your loyal readers have gotten the message that we are shooting ourselves in the foot with our tax code, taxes on investment and estates are counter productive, government should operate under a spending cap, redistribution is destroying incentives, corporate tax rates should be lower, and a VAT would be very bad.

It’s time to step out of the box and get into the details:

Tax code – Clear up the confusion about what a “consumption” tax is, since income taxes are also embedded in prices paid. Recognize that forcing individuals to file tax forms annually is highly inefficient, and “businesses” [broadly defined] should be the collection point for all taxes. At risk of offending the FairTaxers, discuss the problems associated with eliminating income taxes, in favor of a FairTax, NST, or VAT [severe cost push inflation, exacerbated income inequality, and compliance issues].

Investment taxes – Somehow the population believes that the wealthy are like Scrooge McDuck, sitting on stacks of dollars and gold bars; when in fact wealth is a claim on resources, including: land, capital assets, and work product. When you tax wealth, land may change hands with little economic impact, however, a reduction of capital assets and jobs has severe repercussion on economic growth. Since wealth [other than land] is mobile, higher taxes force wealth elsewhere. Instead, wouldn’t it make sense to make the US the tax shelter for the world?

Spending Cap – Swell idea, however, how to implement, when all the political benefits push in the other direction. First, you would need to put a cap on “safety-net” expansion. Second, begin to wind down the biggies: Medicare, Social Security, and Medicaid. Finally, the area that legislators directly control, Discretionary Spending. Each of those need to be “capped” by using different approaches, let’s start discussing options.

Redistribution – It is not enough to say that current levels of redistribution are bad. That is obvious. As well, the current “nanny state” method of distribution is awful, and the disincentives created by means-testing are tragic. A discussion is needed, on how much support is appropriate [none/poverty level?], how do we eliminate welfare bureaucracies, and how do we co-ordinate support with the new tax code, so disincentives are not created?

Lower Corporate Tax Rates – If the tax revenues collected stay the same, a lower corporate rate will not have any impact, if you want prices to stay the same. The elimination of tax preferences to lower tax rates will affect companies differently, but the net impact will be zero. Raising individual rates to lower corporate rates will have no impact, except for top executives gaming the differing rates. Adding some form of sales tax to make up for lost corporate tax revenues, still leaves prices the same. Lowering tax rates across the board will have an impact and dynamic scoring would provide less than expected tax revenue destruction, but reducing the size of government must come first.

VAT – A VAT is not necessarily bad, in theory. However, if the public is shielded from direct impact, the tax rate can be manipulated easier than one could with an income tax increase. However, the same can be said of an NST or the FairTax. If a flat income tax remains for individuals, and the rate is flat for individuals and any of the three supposed “consumption” taxes, the tax rate would be much more sensitive to public opinion.

Reblogged this on My Blog.